Recently, the Sixth Circuit handed down its decision in the Smith v. CommonSpirit Health (“CommonSpirit) 401(k) action.1 My immediate reaction was “hello again SCOTUS,” as once again we have inconsistent and irreconcilable rulings between two circuits involving ERISA litigation

The decision raises a number of issues, including the Court’s suggestion that the alleged popularity of a fund has any relevance whatsoever in connection with the legal prudence of such fund. However I want to focus on what I consider to be the primary reason for the increase in 401(k) litigation and the simple solution that would provide a win-win situation for both plan sponsors and plan participants going forward, reducing litigation and its associated costs.

As the Solicitor General pointed out in the amicus brief it filed in connection with Brotherston v. Putnam Investments, LLC,2 (Brotherston) case, the rights and protections guaranteed under ERISA are simply too important to be determined on the basis of the jurisdiction in which a plan participant resides. And yet, just as in the Northwestern University 401(k) case3, that is exactly the situation we now face as a result of the CommonSpirit decision

SCOTUS denied Putnam’s request for certiorari, thereby arguably implicitly, if not expressly, agreeing with the First Circuit’s decision and the reasoning behind the decision. The Brotherston decision clearly discredited the lower court’s reliance on the “apples and oranges” defense, the suggestion that the use of index funds for benchmarking purposes is legally inappropriate due to inherent differences between active and index funds.

SCOTUS has made it clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected “Congress'[s] desire to offer employees enhanced protection for their benefits.”4

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes)”5

The First Circuit stated that while courts may determine questions of law, the lower court had effectively decided questions of fact, which is the exclusively the responsibility of a jury.

The Court then went on to suggest a way that 401(k) plans might avoid such litigation going forward:

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”6

In the CommonSpirit decision, the Sixth Circuit ignored both the Brotherston decision and the Restatement (Third) of Trusts, a resource that SCOTUS has acknowledged as a resource in resolving questions involving fiduciary prudence. The Sixth Circuit’s primary basis for dismissing the action was its position that index funds are not a “meaningful benchmark” for determining the fiduciary prudence of an actively managed mutual funds.

We accept that pointing to an alternative course of action, say another fund the plan might have invested in, will often be necessary to show a fund acted imprudently (and to prove damages). But that factual allegation is not by itself sufficient.7

That court explained that the two general investment options “have different aims, different risks, and different potential rewards that cater to different investors. Comparing apples and oranges is not a way to show that one is better or worse than the other.”8

That a fund’s underperformance, as compared to a “meaningful benchmark,” may offer a building block for a claim of imprudence is one thing. But it is quite another to say that it suffices alone, especially if the different performance rates between the funds may be explained by a “different investment strategy….”We would need significantly more serious signs of distress to allow an imprudence claim to proceed.9

The Sixth Circuit then went on to suggest that the alleged popularity of a fund and/or its Morningstar rating may be relevant in determining the prudence of a fund. This suggestion is clearly in conflict with other courts, which have consistently stated that the alleged popularity of a fund and/or third-party ratings are totally irrelevant in determining the fiduciary prudence of mutual funds.

The Court then stated that

publicly available performance information about an investment may show sufficiently dismal performance that this reality, when combined with “allegations about methods,” will successfully allege that a prudent fiduciary would have acted differently.10

The Court credited CommonSpirit with removing the AllianzGI Fund as an investment option in 2018, stating that is served as evidence “that CommonSpirit fulfilled its ‘continuing duty to monitor trust investments and remove imprudent ones’.11The Court apparently was unaware that the AllianzGI Fund was apparently closed in 2018, so it is possible that CommonSpirit had a choice in removing the fund from the plan’s menu of investment options

Building a Better, and Fairer, Mousetrap

While most 401(k) decisions address costs and returns, I have never seen any court take the next, and to me the obvious, step of combining the two to address the cost-efficiency of an actively managed fund relative to a comparable index fund.

Interestingly enough, the Sixth Circuit referenced Charles D. Ellis’s classic book, “Winning the Loser’s Game.” Unfortunately, the Court failed to reference arguably Ellis’ most important contribution to wealth management:

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns.

When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!12

Add to that the contributions of both Nobel Laurerate Dr. William D. Sharpe and investment icon Burton L. Malkiel:

[T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.13

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.14

Based upon the Restatement and the studies of Ellis, Sharpe, and Malkiel, I created a simple metric, the Active Management Value Ratio™ (AMVR), that allows investors, investment fiduciaries and attorneys to quickly determine the cost-efficiency of an actively managed mutual fund relative to a comparable index fund. For more information about the AMVR, including the calculation process, click here (iainsight.wordpress.com).

Once the AMVR is calculated for an actively managed fund, the investor or investment fiduciary only needs to answer two simple questions:

(1) Does the actively managed mutual fund provide a positive incremental return relative to the benchmark being used?

(2) If so, does the actively managed fund’s positive incremental return exceed the fund’s incremental costs relative to the benchmark?

If the answer to either of these questions is “no,” the actively managed fund is both cost-inefficient and unsuitable/imprudent according the the Restatement’s prudence standards, and should be avoided. The goal for an actively managed fund is an AMVR number greater than “0” (indicating that the fund did provide a positive incremental return), but equal or less than “1” (indicating that the fund’s incremental costs did not exceed the fund’s incremental return).

The AMVR metric provides extremely useful information regarding the cost-efficiency of an actively managed mutual fund using just a fund’s nominal, or publicly reported, costs and returns. However, a cost-efficiency analysis should not end there if one wants a truly accurate cost-efficiency analysis of an actively managed mutual fund.

Professor Ross Miller did a study on the impact of closet indexing, focusing primarily on the relationship between an actively managed mutual fund’s r-squared number, “closet index” status, and the resulting overall financial impact of the two. “Closet index” funds are actively managed funds whose returns are essentially the same as a comparable index fund, but who charge much higher fees than the index fund. The higher an actively managed fund’s r-squared number, the greater the likelihood that the actively managed fund can be classified as a closet index fund.

An r-squared rating of 98 would indicate that 98 percent of an actively managed mutual fund’s returns could be attributed to the performance of a comparable index fund, rather than the active fund’s management team.

There is no universally agreed upon level of r-squared that designates an actively managed mutual fund as a closet index fund. I use an r-squared correlation number of 90 as my threshold indicator for closet index status. Others, including Morningstar, use much lower r-squared numbers.

Miller’s findings were extremely interesting, namely that

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.15

As a result of his study, Ross Miller, created the Active Expense Ratio (AER) metric. What Miller discovered was that once a fund’s r-squared correlation number is factored in, an active fund’s AER, the fund’s implicit, or effective, expense ratio is significantly higher than the fund’s stated expense, often as much as 400-500 percent higher. Investors and investment fiduciaries should remember John Bogle’s advice on investment costs, “you get what you don’t pay for,” as well as the fact that simple mathematics proves that each one percent in fees and expenses reduces an investor’s or fiduciary’s end-return by approximately seventeen percent over a twenty-year time period.16

The AMVR and the CommonSpirit Health Decision

The Plaintiffs in the CommonSpirit case did not include a cost-inefficiency argument in their complaint. While the AMVR has gained increasing recognition and support among investment fiduciaries and some plaintiff’s attorneys, many attorney still refuse to even consider the metric. Attorneys often cite the simplicity of the AMVR and the fact that many judges still dislike the use of index funds, particularly Vanguard index funds, as comparators due to their inherent advantages over comparable actively managed funds

First, I believe that the simplicity of the AMVR is one of its main advantages. The AMVR requires very little time to learn and use effectively. The calculations are based primarily on online data from free sites such as morningstar.com and yahoo.finance.com and marketwatch.com. Once one becomes familiar with the AMVR calculation process and downloads the relevant data, the calculations themselves usually take less than a minute or two.

Second, with regard to judges’ resistance to the use of index funds as comparators, I believe that the Brotherston decision and the Restatement (Third) of Trusts clearly establish that index funds, including Vanguard index funds, are “meaningful benchmarks” under the law. The First Circuit and the U.S. District Court for the Southern District of New York17, aka Wall Street’s federal court, have recognized the propriety of benchmarking in connection with 401(k) actions. As a result, I have suggested to attorneys that they should always include a cost-inefficiency claim in their 401(k) actions cases, if for no other reason than to preserve the issue on appeal.

The CommonSpirit decision validates the AMVR and the processes and fiduciary principles upon which it is based. This opinion is based on the Court’s dacknowledgement of the importance of investment costs:

“One feature of the active/passive management debate deserves focus. It is easy for investors at a given time to preoccupy themselves with the present-day or year-to-year value of their portfolio—the part of a financial statement usually placed most squarely in view. But just as compounding can dramatically increase the value of a mutual-fund investment over time, so the costs of that investment can dramatically eat into that investment over time…. Over time, management fees, like taxes, are not trivial features of investment performance.”17

The Sixth Circuit’s acknowledgment of the importance of investment fees and others costs, including the fact that the impact of such fees, like returns, compound over time, cannot be overemphasized. The costs associated with underperformance are obvious and often discussed, both in terms of the financial loss and opportunity costs.

Costs and cost-efficiency generally do not receive the same amount of attention that returns receive. When the Securities and Exchange Commission (SEC) announced and implemented Regulation “Best Interest” (Reg BI), then SEC chairman Jay Clayton acknowledged the importance of cost-efficiency of investments:

rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.18

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.19

The financial services industry quickly announced its opposition to Reg BI. The financial services industry opposition was based largely on the regulation’s requirement that costs must be factored into any investment recommendation provided my brokers.

Section 90, comment h(2) of the Restatement states that that due to higher costs and risks associated with actively managed funds, actively managed funds are imprudent unless it can be objectively estimated that the funds will provide a commensurate return for the additional costs and risks incurred, i.e., are cost-efficient.20

The financial services industry does not like to discuss cost-efficiency, as studies have consistently shown that the overwhelming majority of actively managed mutual funds are cost-inefficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.21

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.22[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.23

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.24

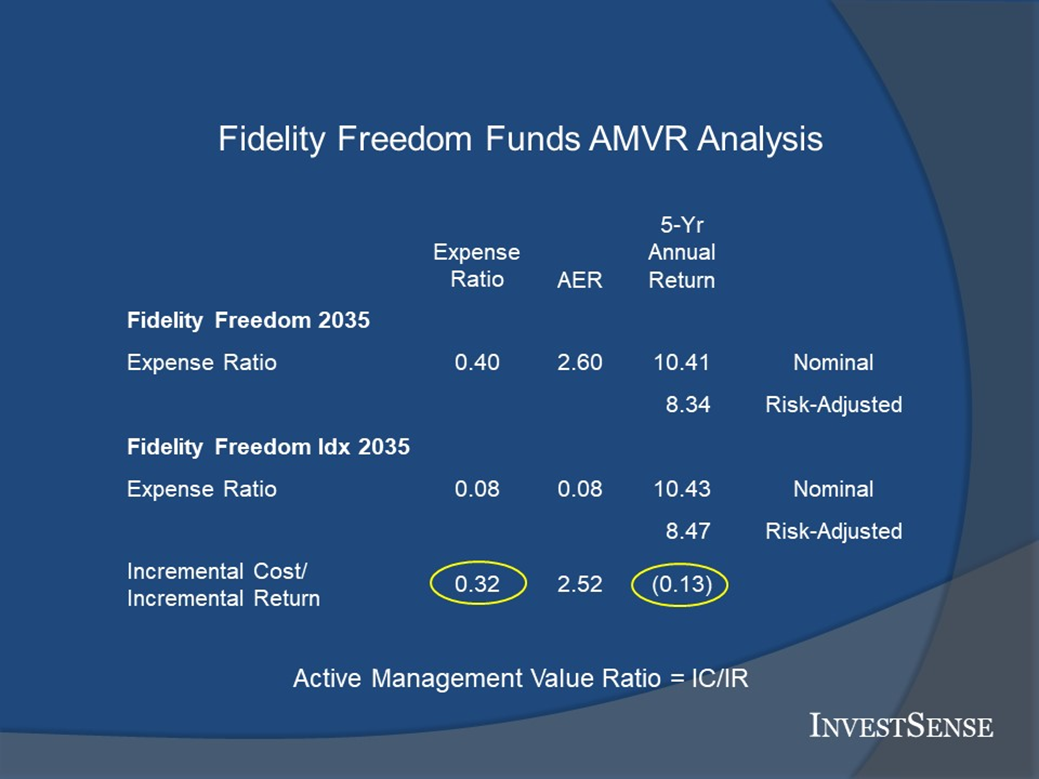

Critics of the AMVR often claim that it is simply a way to promote Vanguard funds. The CommonSpirit decision provided me with an opportunity to discredit that allegation by performing an AMVR forensic fiduciary prudence analysis comparing some of the the Fidelity Freedom active funds to comparable Fidelity Freedom Index funds.

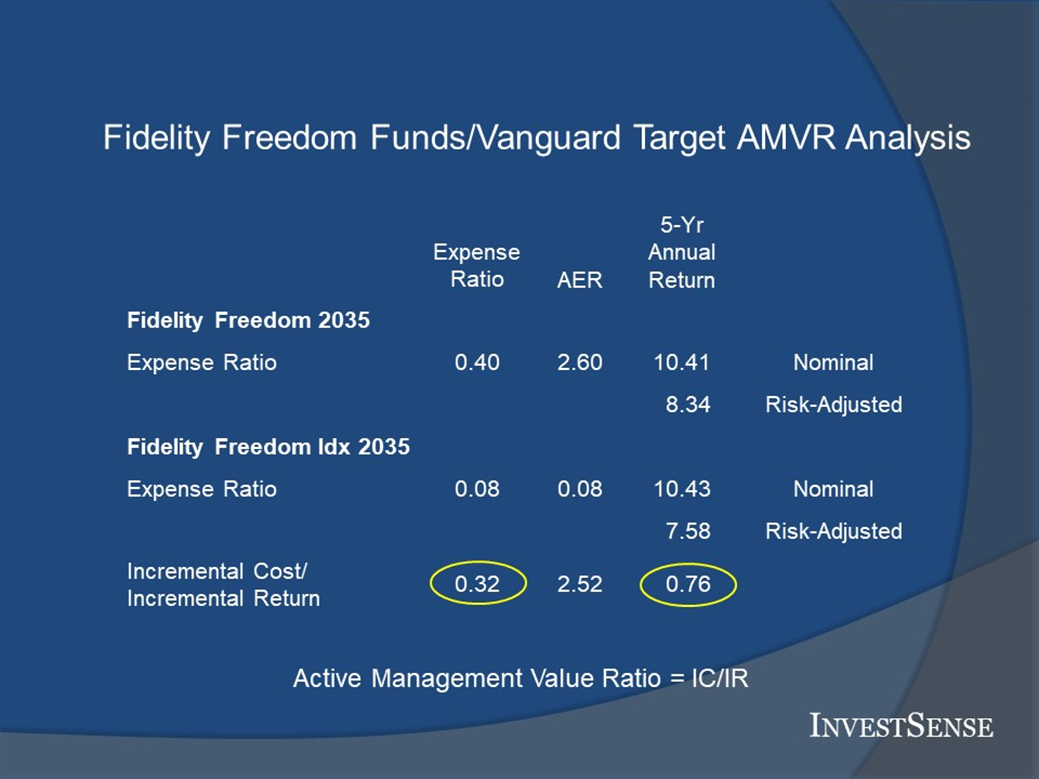

I decided to also perform a similar AMVR fiduciary prudence analysis comparing some of the Fidelity Freedom active funds to comparable Vanguard TDF funds.

In the Fidelity Freedom active/inedx analysis, the active funds failed to provide a positive incremental return. So, arguably, the Fredom Active/Freedom Index AMVR analysis would have helped the plaintiff in the CommonSpirit case establish the cost-inefficiency of the active suite of funds, the “more” that courts keep demanding in meeting the required plausibility pleading standard. Conversely, the Fidelity Freedom active/Vanguard TDF AMVR analysis shows the importance of selecting the appropriate comparator index funds, as using Vanguard’s comparable index funds would have undermined the plaintiff’s case.

Going Forward

I would argue that there are several issues with the Sixth Circuit’s CommonSpirit decision. However, I believe the bigger issue in connection with 401(k) litigation and fiduciary in general is the opportunity it provides to divert attention from the active/passive debate and place the attention to a much more meaningful issue, the value of cost-efficiency and the AMVR in assessing fiduciary prudence/ liability and determining damages and in 401(k)/fiduciary actions. The simplicity and straightforward nature of the AMVR, combined with the fact that it is consistent with the fiduciary standards established by the Restatement, suggest that it is a “meaningful benchmark” that so many courts require to meet the federal pleading standards.

The AMVR exposes the irrelevancy of the defenses courts and the financial services industry often cite in 401(k) actions in defense of active management, e.g., differences in strategies, methodolgy, goals. The AMVR counters such arguments and tangential issues, essentially saying “ I do not care HOW you allegedly provided me with a benefit, but whether you actually DID provide me with a benefit at all.”

Businesses use cost-benefit analysis every day. The AMVR is simply the cost/benefit equation using incremental cost and incremental returns as the imputs.

The Brotherston and Leber25 decisions, along with the Restatement effectively rebut any suggestions that index funds, including Vanguard index funds, are not “meaningful benchmarks.” The focus of the courts should be determining whether 401(k) plans provided plan participants with “meaningful choices” within their plans, cost-efficienct investment options that provided genuine benefits to the plan participants and their benefits as required by ERISA.

In closing, I think the validity and the value of the AMVR can be summed up in two relevant quotes. In a 2007 speech at the University of Pennsylvania Law School, Brian G. Cartwright, then general counsel of the SEC, asked his audience to think of an investment in a mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s real holdings. Cartwright told the students,

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund — no overweightings or underweightings — then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?26

The second quote is from John Langbein, who served as the Reporter on the committee that wrote the Restatement (Second) of Trusts over fifty years ago. Shortly after the release of the revised Restatement, Langbein wrote a law review article on the new Restatement. At the end of the article, he made a bold prediction:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.27

I would suggest that that day has arrived and that the AMVR will be an indispensable tool in making both speaker’s predictions become reality for the benefit of both investors and investment fiduciaries.

Notes

1. Smith v. CommonSpirit Health, No. 21-5964, June 21, 2022 (6th Cir. 2022).(CommonSpirit)

2. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Circuit 2018)(Brotherston)

3. Hughes v. Northwestern University, 142 S.Ct. 737 (2022)

4. Brotherston, 37

5. Brotherston, 34

6. Brotherston, 39

7. CommonSpirit, II.A

8. CommonSpirit, II.A

9. CommonSpirit, II.A

10. CommonSpirit, II.A

11. CommonSpirit, II.A

12. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online at https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c

13. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm

14. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460.

15. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926

16. Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study”), http://www.gao.gov/new.item/d0721.pdf

17. CommonSpirit, I.A

18. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G.Cartwright).(SEC Speech) http://www.sec.gov/news/speech/2007/spch102407bgc.htm

19. SEC Speech

20. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt h(2).

21. Laurent Barras, Oliver Scaillet, and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANE 179, 181 (2010)

22. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, https://www.ft.com/content/6b2d5490-d9bb-eb37a6aa8e

23. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE 57-58 (1997)

24. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Funds Advisors, L.P., August 2016

25. Leber v. Citigroup 401(k) Plan Inv. Committee, 2014 WL 4851816

26. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G. Cartwright). http://www.sec.gov/news/speech/2007/spch102407bgc.htm

27. John H. Langbein and Richard A. Posner, Measuring the True Cost of Active Management by Mutual Funds, Journal of Investment Management, Vol 5, No. 1, First Quarter 2007 http://digitalcommons.law.yale.edu/fss_papers/498

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

Pingback: An Inconvenient Truth: Cost-Inefficiency and Closet Indexing in 401(k) Plans | The Prudent Investment Fiduciary Rules