James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

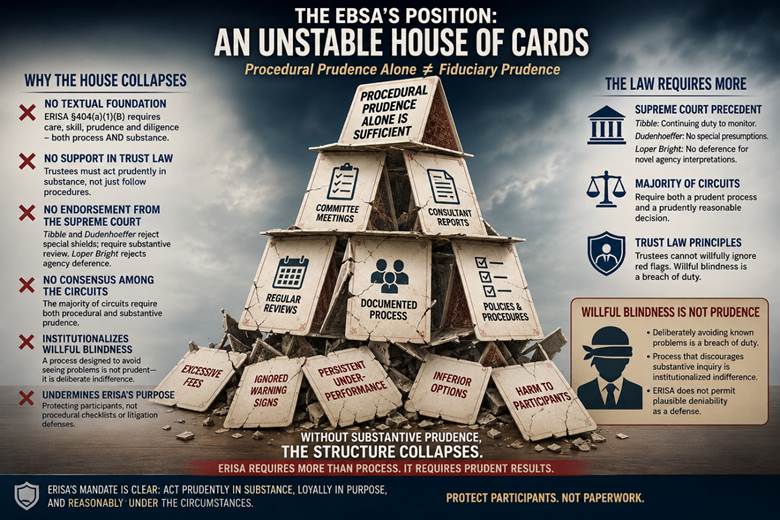

The issue before this Court is not whether procedural prudence matters under ERISA. It unquestionably does. The issue is whether the Employee Benefits Security Administration (EBSA) may lawfully transform procedural prudence from an evidentiary consideration into a substitute for fiduciary prudence itself. That proposition is not merely unsupported. It is irreconcilable with ERISA’s text, the law of trusts, and decades of controlling judicial precedent.

The EBSA’s current position rests upon a fundamentally unstable premise — a legal “house of cards” constructed by incrementally extrapolating beyond what courts have actually held. The agency begins with a legitimate proposition: fiduciaries must employ a prudent process. But it then extends that proposition far beyond recognition, asserting in substance that the existence of a procedurally elaborate process is itself sufficient to establish fiduciary prudence, irrespective of whether the resulting decision was objectively reasonable, loyal, or substantively defensible. That leap finds no support in ERISA, trust law, or Supreme Court jurisprudence.

ERISA does not impose a mere paperwork standard. Congress enacted a fiduciary regime grounded in substantive protection of plan participants and beneficiaries. Section 404(a)(1)(B) requires fiduciaries to act “with the care, skill, prudence, and diligence under the circumstances then prevailing” that a prudent person would use in a like capacity. That language incorporates both method and outcome-oriented reasonableness. A fiduciary process is relevant because it helps determine whether the fiduciary actually acted prudently — not because process itself magically converts imprudent conduct into prudent conduct.

The Supreme Court has repeatedly treated procedural prudence as evidence of prudence, not as prudence per se. In Tibble v. Edison International1, the Court emphasized the continuing duty to monitor investments under trust-law principles. The Court did not suggest that a fiduciary could satisfy that duty merely by documenting meetings, retaining consultants, or following internal protocols while ignoring objectively unreasonable outcomes. To the contrary, Tibble reaffirmed that ERISA fiduciary obligations derive from trust law — a body of law that has never equated procedural formality with substantive prudence.

Likewise, in Fifth Third Bancorp v. Dudenhoeffer2, the Court rejected special presumptions insulating fiduciaries from substantive review. The Court instead demanded context-sensitive judicial scrutiny of fiduciary conduct. That framework is fundamentally incompatible with the EBSA’s apparent effort to create a de facto safe harbor based solely upon procedural ritualism.

Most importantly, the Supreme Court’s recent administrative law jurisprudence forecloses the degree of interpretive elasticity the EBSA now seeks to employ. Under Loper Bright Enterprises v. Raimondo3, agencies are not entitled to deference merely because they advance a plausible policy preference. Courts must independently determine the best reading of the statute. And the best reading of ERISA does not permit an agency to collapse substantive fiduciary review into a checklist-driven procedural exercise.

Indeed, the majority of federal circuit courts have consistently recognized that fiduciary prudence under ERISA contains both procedural and substantive dimensions. Courts routinely examine whether fiduciaries engaged in a reasoned process, but they also examine whether the resulting decisions were objectively reasonable under prevailing circumstances. The two inquiries are interconnected but distinct.

The EBSA’s contrary position attempts to erase that distinction altogether.

Under the agency’s apparent framework, a fiduciary could:

- retain expensive and underperforming investments indefinitely,

- ignore materially superior alternatives,

- impose excessive costs upon participants,

- or structure portfolios in ways inconsistent with accepted investment principles,

yet still claim prudence merely because committees met regularly, minutes were recorded, consultants were retained, and procedural boxes were checked.

That is not fiduciary law. That is administrative formalism masquerading as fiduciary protection.

Even more troubling, the EBSA’s position effectively institutionalizes a form of legally sanctioned willful blindness.

Under traditional trust principles, a fiduciary cannot deliberately avoid confronting evidence that its decisions are harming beneficiaries. A trustee may not shield itself behind process while consciously disregarding substantive warning signs. Yet the EBSA’s approach incentivizes precisely that behavior. So long as fiduciaries can demonstrate that meetings occurred and procedures were followed, they are tacitly encouraged not to ask the harder substantive questions:

- Are participants actually receiving prudent investment options?

- Are fees objectively excessive relative to available alternatives?

- Are persistent underperformance patterns being meaningfully addressed?

- Are fiduciaries evaluating economic realities, or merely preserving litigation defenses?

A regime that rewards procedural insulation while discouraging substantive inquiry creates a dangerous moral hazard. Fiduciaries become incentivized to cultivate plausible deniability rather than genuine prudence. The resulting process ceases to function as a tool for protecting participants and instead becomes a mechanism for avoiding accountability.

That is the essence of willful blindness: constructing systems designed not to discover imprudence.

And courts have repeatedly rejected analogous attempts in other legal contexts to substitute formal compliance mechanisms for actual substantive responsibility. The law does not permit actors to avoid liability by intentionally narrowing their field of vision. ERISA fiduciaries should not become the sole exception to that foundational principle.

Trust law has never tolerated such a result. A trustee who carefully documents an irrational decision does not become prudent by virtue of documentation alone. Nor does a fiduciary become prudent by deliberately refusing to confront evidence inconsistent with a preferred narrative of compliance. Process matters because it tends to produce prudent decisions. But when process becomes detached from substantive reasonableness, it degenerates into empty ceremony — or worse, into a sophisticated form of institutionalized indifference.

The danger of the EBSA’s position is therefore not merely doctrinal. It is systemic.

By elevating procedural optics above substantive participant outcomes, the agency creates perverse incentives throughout the retirement system. Fiduciaries become incentivized to maximize defensibility rather than participant welfare — to generate committee records instead of investment value, to prioritize consultant memoranda over economic reality, and to engage in defensive bureaucracy rather than genuine fiduciary stewardship.

That approach undermines the very purpose of ERISA.

Congress enacted ERISA because participants lacked the expertise and leverage necessary to protect themselves against imprudent fiduciary conduct. The statute was designed to impose meaningful fiduciary accountability — not to create a litigation-resistant compliance theater in which process alone immunizes objectively harmful decisions.

Nor can the EBSA evade this problem by characterizing substantive review as impermissible hindsight. Courts are fully capable of distinguishing between prohibited hindsight bias and legitimate evaluation of objective prudence. Federal courts have done so for decades. The existence of market uncertainty does not eliminate the requirement that fiduciary decisions possess a rational substantive foundation when made.

The EBSA’s position also produces a profound logical contradiction. If procedural prudence alone establishes fiduciary prudence, then substantive prudence effectively disappears from ERISA altogether. Yet ERISA’s statutory language does not distinguish between procedural prudence and substantive prudence because the statute contemplates both as components of a unified fiduciary obligation. The agency’s interpretation therefore impermissibly rewrites the statute by excising substantive accountability from fiduciary review.

This Court should reject that effort.

An agency cannot manufacture legal authority through repetition. It cannot bootstrap a novel fiduciary theory from selective quotations stripped of their doctrinal context. And it cannot convert isolated judicial references to “process” into a wholesale abandonment of substantive fiduciary review when neither Congress nor the Supreme Court has authorized such a transformation.

At bottom, the EBSA’s position is unstable because it lacks the essential structural support that legitimate legal doctrines require:

- no textual foundation in ERISA,

- no grounding in traditional trust law,

- no endorsement from the Supreme Court,

- no meaningful consensus among the federal circuits,

- and no principled answer to the obvious danger of willful blindness inherent in its framework.

Without those supports, the theory collapses under its own weight.

It is, in every meaningful sense, a house of cards.

And because ERISA exists to protect plan participants rather than bureaucratic abstractions, this Court should decline the invitation to replace genuine fiduciary prudence with procedural symbolism. The law requires more than documented process. It requires fiduciaries to act prudently in substance, loyally in purpose, and reasonably under the circumstances actually confronting them.

Anything less would reduce ERISA’s fiduciary protections from a substantive safeguard into a merely procedural illusion

Notes

1. Tibble v. Edison, 575 U.S. 523 (2015).

2. Fifth Third Bancorp v. Dudenhoeffer, 573 573 U.S. 409 (2014).

3. Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024).

© Copyright 2026 InvestSense, LLC. All rights reserved

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

.

You must be logged in to post a comment.