James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

May it please the Court:

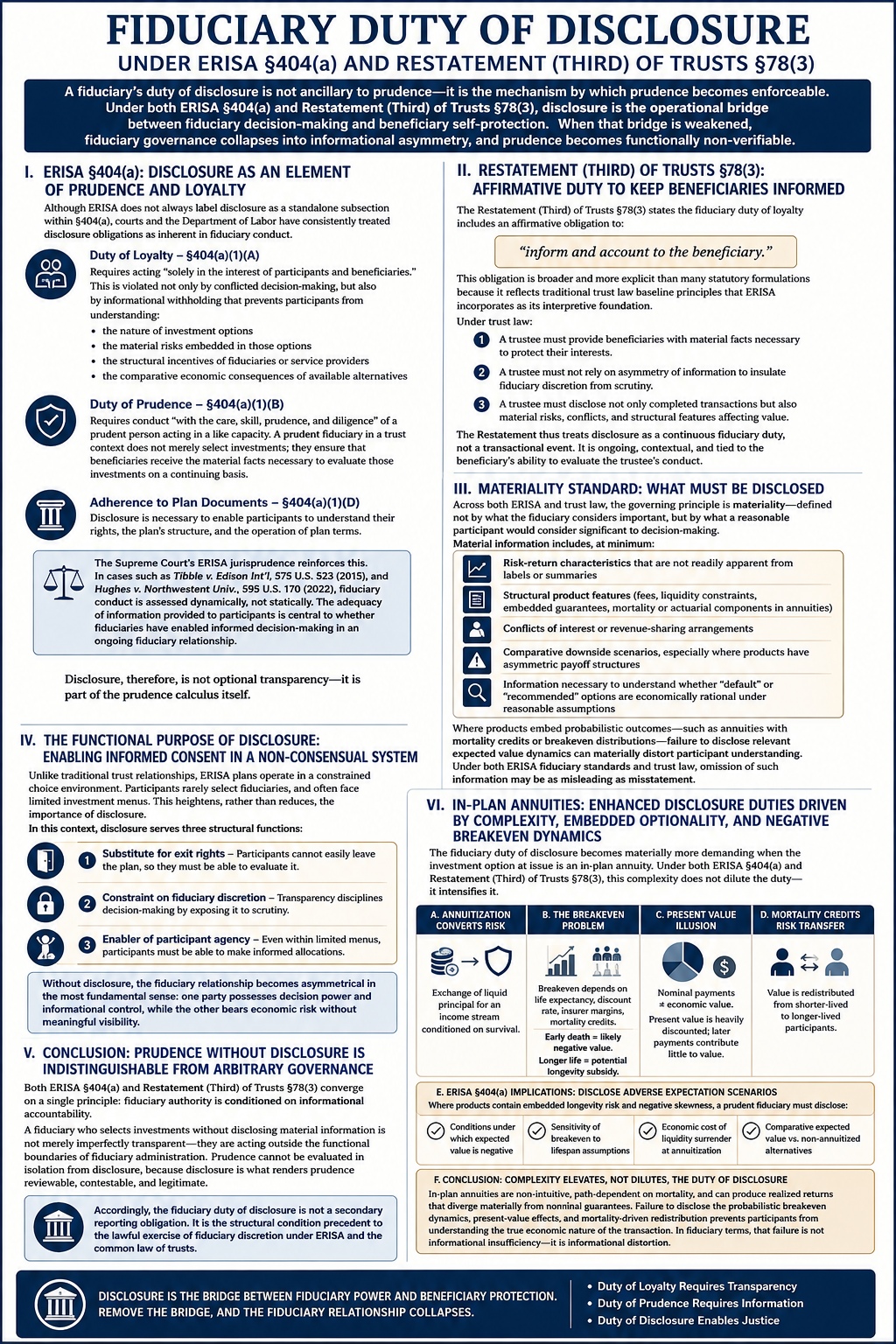

This case concerns a fundamental proposition that predates ERISA, predates modern securities law, and lies at the very heart of the law of trusts: a fiduciary cannot withhold material information from those to whom fiduciary duties are owed.

The issue before this Court is not whether a fiduciary acted with subjective good intentions, nor whether the fiduciary followed internal procedures, documented meetings, or retained consultants. The issue is whether fiduciaries discharged their affirmative duty of loyalty and disclosure by providing participants the information necessary to protect their own interests.

The answer is found in the law of trusts itself.

I. The Restatement Recognizes an Affirmative Duty to Disclose Material Information

Section 78(3) of the Restatement (Third) of Trusts1 provides that:

“Except in discrete circumstances, a trustee has a duty to the beneficiaries to deal fairly and to communicate to the beneficiary material facts affecting the beneficiary’s interest which the trustee knows or should know the beneficiary needs to know for the protection of the beneficiary’s interests.”

This rule is neither novel nor aspirational. It represents centuries of trust law recognizing that loyalty requires candor. A fiduciary who possesses material information affecting a beneficiary’s interests cannot remain silent merely because the beneficiary failed to ask the correct question.

ERISA expressly incorporates the common law of trusts as its interpretive foundation. The Supreme Court has repeatedly instructed that courts must look to trust law in defining the content of fiduciary duties. See, e.g., ERISA cases such as Varity Corp. v. Howe2 and Tibble v. Edison International.3

The Restatement’s duty to disclose therefore supplies an essential component of ERISA’s duties of loyalty and prudence.

II. “Material” Information Must Carry Its Established Legal Meaning

The Restatement does not define materiality in a vacuum. The concept has long possessed an established legal meaning.

The Supreme Court’s securities decisions provide the most developed and widely accepted articulation of materiality in TSC Industries. Inc. v. Northway, Inc.4 The Court held that information is material if there exists:

“a substantial likelihood that a reasonable investor would consider it important.”

The Court further explained that material information is that which would have significantly altered the “total mix” of information available.

That standard was reaffirmed in Basic, Inc. v. Levinson5, which rejected both excessively narrow and excessively expansive definitions of materiality.

Although these cases arose under the securities laws, the underlying principle is universal. Materiality concerns information sufficiently important that a reasonable person would regard it as significant in making decisions affecting his or her economic interests.

ERISA participants make decisions regarding contributions, investments, rollovers, distributions, retirement timing, and benefit elections. The same reasonable-investor framework therefore provides the most logical and legally coherent standard for determining what information fiduciaries must disclose.

III. The “Knew or Should Have Known” Standard Imposes an Objective Duty

Section 78(3) is equally important because it rejects a purely subjective standard.

A fiduciary’s duty extends to information the fiduciary “knew or should have known.” This language imposes an objective obligation.

ERISA fiduciaries cannot avoid liability by remaining deliberately uninformed, by failing to investigate, or by compartmentalizing information among committees, consultants, and service providers. A fiduciary charged with managing retirement assets must exercise the diligence necessary to discover material information affecting participants’ interests.

This principle parallels ERISA’s prudent-investigation requirement recognized in decisions such as:

- Donovan v. Bierwirth6

- Tibble v. Edison International7

- Hughes v. Northwestern University8

A fiduciary cannot disclose information it never sought to obtain. Thus, the duties of prudence and disclosure operate together. The duty to investigate supplies the knowledge that the duty to disclose requires.

IV. Disclosure Is an Expression of Loyalty

The duty of loyalty demands more than the avoidance of self-dealing. A fiduciary acts loyally only when it places the beneficiary’s interests first. That obligation necessarily includes furnishing participants with information necessary to protect those interests.

Silence can itself constitute disloyal conduct. The Supreme Court recognized this principle in Varity Corp. v. Howe9, holding that fiduciaries may not materially mislead plan participants when communicating about plan benefits and participant interests.

A partial disclosure that omits material facts may be just as misleading as an outright falsehood. If fiduciaries know—or should know—that participants require certain information to protect their retirement interests, Section 78(3) requires disclosure.

V. Material Information in the ERISA Context

Material information may include:

- Significant investment risks.

- Conflicts of interest.

- Revenue-sharing arrangements.

- Material fees and expenses.

- Limitations of investment products.

- Information concerning fiduciary investigations.

- Known risks affecting retirement outcomes.

- Information bearing on the prudence of investment options.

- Facts necessary to evaluate the security of promised benefits.

The relevant inquiry is straightforward:

Would a reasonable participant consider the information important in making decisions concerning retirement assets or benefits?

If the answer is yes, the information is material.

VI. Procedural Formalities Cannot Substitute for Disclosure

The EBSA’s current position notwithstanding, a fiduciary cannot satisfy its obligations merely by conducting meetings, retaining consultants, or creating documentation. A flawless process that withholds material information from participants remains inconsistent with fiduciary principles.

Section 78(3) recognizes that beneficiaries frequently suffer from informational asymmetry. Fiduciaries possess information, expertise, and access that participants lack. The law therefore places the burden upon the fiduciary—not the beneficiary—to communicate material facts.

This principle is particularly important in defined contribution plans, where participants increasingly bear investment risks and retirement outcomes depend heavily upon information known by fiduciaries and service providers.

Conclusion

Section 78(3) of the Restatement (Third) of Trusts establishes an affirmative fiduciary duty to disclose material information that fiduciaries knew or should have known beneficiaries needed to protect their interests.

Materiality should be evaluated using the objective standards articulated by the Supreme Court in TSC Industries and Basic: whether there exists a substantial likelihood that a reasonable participant would consider the information important, and whether disclosure would significantly alter the total mix of information available.

ERISA’s trust-law foundations compel this result.

The duty of loyalty requires candor.

The duty of prudence requires investigation.

The duty of disclosure requires communication.

Together, these principles ensure that retirement plan participants are not left to navigate critical financial decisions in informational darkness while fiduciaries possess material facts affecting their interests.

The law of trusts does not permit such silence. ERISA does not permit such silence. And this Court should not permit such silence.

The Fiduciary Duty of Disclosure Applied to In-Plan Annuities

The foregoing principles become particularly significant when applied to in-plan annuities because the fiduciary disclosure obligation extends not merely to the existence of a guaranteed lifetime income feature, but to all material facts that a fiduciary knew or should have known that participants would need to protect their retirement interests.

If a fiduciary offers an in-plan annuity while possessing—or while reasonably being expected to possess—information indicating that many participants are unlikely to achieve economic breakeven, such information may constitute material information under both Section 78(3) and ERISA’s fiduciary standards.

VII. In-Plan Annuities and the Duty to Disclose Material Information

In-plan annuities present a classic case of informational asymmetry.

The plan sponsor, fiduciary committee, consultants, insurers, and recordkeepers generally possess sophisticated actuarial, financial, and mortality information that the average participant neither possesses nor can independently obtain.

Participants frequently hear only the appealing phrase:

“Guaranteed income for life.”

However, Section 78(3) requires disclosure of material facts necessary for participants to protect their interests. That duty extends beyond marketing descriptions.

A fiduciary that knows, or should know, that certain economic characteristics materially affect the participant’s decision must disclose those characteristics. Such information may include:

- Expected breakeven ages.

- Present-value losses associated with annuitization.

- Mortality probabilities.

- The likelihood of recovering principal.

- The cost of optional death-benefit riders.

- Inflation effects.

- Opportunity costs.

- The economic consequences of irrevocable elections.

These are not peripheral considerations. They are material information that central to the participant’s decision. They are necessary to satisfy ERISA Section 404(a)’s requirement that a plan sponsor provide a plan particiapnt with “sufficient information to make an informaed decision.”

VIII. Materiality Under the Supreme Court Standard

Under the materiality standard established in TSC Industries and Basic, information is material if there is a substantial likelihood that a reasonable participant would consider it important in making a retirement decision.

Few facts could be more important to a reasonable participant than:

- The probability of living long enough to break even.

- The present-value reduction required to purchase lifetime guarantees.

- The possibility that premature death results in forfeiture of principal.

- The fact that principal protection often requires additional riders and additional costs.

If disclosure of these facts would significantly alter the “total mix” of information available to the participant, they are material as a matter of law.

A participant who hears only that an annuity provides “guaranteed income for life” receives an incomplete picture if the participant is not informed that actuarial probabilities may indicate a substantial likelihood that the participant will never recover the value of the premium transferred to the insurer.

IX. Breakeven Analysis as Material Information

A properly prepared breakeven analysis generally incorporates:

- Present value of future payments.

- Mortality probabilities.

- Time value of money.

- Inflation effects.

- Opportunity costs.

- Probability of principal recovery.

The present-value analysis is particularly important because a dollar received twenty years in the future is worth substantially less than a dollar retained today. The mortality analysis is equally important because the economic value of an income annuity depends heavily upon surviving beyond the actuarial breakeven age.

The mathematical relationship may be illustrated as follows:

$

%

PMT is starting amount; r is rate; n is number of periods.

When mortality probabilities are incorporated into the present-value calculation, many participants may discover that:

- They must survive substantially beyond normal life expectancy to realize positive economic value.

- They face a meaningful probability of dying before recovering their principal.

- Their heirs may receive little or nothing absent additional riders.

- Riders designed to preserve principal often reduce income and increase costs.

These facts directly affect the participant’s economic decision. Therefore, these are material facts that are required to be disclosed to a plan’s particiapnts.

A reasonable participant might decide differently if informed that actuarial analysis indicates only a modest probability of achieving an economic breakeven, of recovering their original presence and additional retirement income payments. To quote Mark Twain, “I’m not so concerned about the income ON my money as I am the return OF my money.”

X. The “Knew or Should Have Known” Standard

Section 78(3) imposes an objective duty of disclosure. Plan fiduciaries selecting in-plan annuities frequently retain severeal types of experts, including, but not limited to,:

- Attorneys.

- Fiducairy risk management consultants.

- Actuaries.

- Insurance consultants.

- Investment consultants.

- Recordkeepers.

- Insurance carriers.

These parties routinely possess mortality assumptions, pricing models, payout factors, and actuarial analyses.

A fiduciary therefore cannot plausibly claim ignorance of facts that reasonably should have been investigated during the annuity selection process. If a prudent investigation would reveal that many participants face unfavorable breakeven probabilities, the fiduciary “should have known” those facts. Once known, or reasonably knowable, Section 78(3) requires disclosure if those facts are material to participant decision-making.

XI. The Absence of Principal Protection

Many immediate and deferred income annuities require irrevocable annuitization.

The participant exchanges a liquid asset for a stream of payments contingent upon survival. Without refund features or death-benefit riders:

- Remaining principal may be forfeited.

- Beneficiaries may receive nothing.

- The insurer retains the remaining economic value.

The availability of principal protection often requires:

- Period-certain guarantees.

- Refund provisions.

- Death-benefit riders.

These protections frequently reduce monthly income or increase costs. As both the DOL and GAO have noted, over a twenty year peroid, each additional 1% in fees/costs reduces an investor’s end-return by approximately 17%.10 Thus the economic tradeoff between income guarantees and principal protection is itself material information.

A participant may reasonably conclude that a lower-yielding bond ladder, Treasury portfolio, CDs or systematic withdrawal strategy better satisfies their objectives if informed of these tradeoffs.

XIII. The Speculative Nature of Mortality Credits

Proponents of annuities frequently argue that “mortality credits” justify the economic value of lifetime income products. The theory is that individuals who die earlier than expected subsidize payments to individuals who survive longer than expected, thereby creating additional returns unavailable from conventional investments.

While mortality credits are a legitimate actuarial concept at the insurer’s pool level, their use in evaluating an individual participant’s expected benefit raises significant fiduciary disclosure concerns.

A. Mortality Credits Are Contingent Upon an Unknown Event

Unlike investment returns, interest payments, or bond coupons, mortality credits are not earned at a determinable rate. Their realization depends upon a single unknowable variable:The participant’s actual longevity.

No participant knows:

- Whether they will survive to the actuarial breakeven age.

- Whether they will survive long enough to receive meaningful mortality credits.

- Whether they will die before recovering their principal.

- Whether they will live sufficiently long to benefit from the experience of shorter-lived annuitants.

Consequently, mortality credits are not guaranteed returns. They are contingent benefits that become valuable only if a participant survives long enough to receive them.

B. Mortality Credits Exist at the Pool Level, Not the Individual Level

Insurers price annuities using population-level mortality assumptions.

The insurer knows that:

- Some annuitants will die early.

- Some will live exceptionally long.

- The law of large numbers allows the insurer to predict aggregate experience.

The individual participant, however, experiences only one outcome. The participant either:

- Lives sufficiently long to benefit from mortality pooling; or

- Dies before receiving those benefits.

Thus, mortality credits that appear certain at the insurer level remain entirely uncertain at the participant level.

From the participant’s perspective, the alleged benefit remains speculative until longevity actually occurs.

C. Fiduciary Analysis Should Distinguish Between Guaranteed Payments and Speculative Benefits

A prudent breakeven analysis should separate:

- Guaranteed contractual payments.

- Return of principal.

- Present-value calculations.

- Speculative mortality benefits.

Combining these elements risks presenting uncertain future benefits as though they possess the same economic certainty as fixed income payments. A participant may reasonably believe:

“The annuity is expected to produce superior returns.”

When, in reality, the superior outcome may depend entirely upon surviving substantially beyond normal life expectancy. This distinction is material.

D. The Supreme Court’s Materiality Standard Supports Disclosure

Under TSC Industries and Basic, the question is whether a reasonable participant would consider information important.

A reasonable participant would likely consider it important to know:

- That mortality credits are not guaranteed.

- That they are contingent upon longevity.

- That the participant may never realize them.

- That economic breakeven may require survival well beyond average life expectancy.

Such information significantly alters the total mix of information available to the participant. Accordingly, the contingent nature of mortality credits itself constitutes material information.

E. The “Known or Should Have Known” Standard

Section 78(3) imposes a duty to disclose material information that fiduciaries knew or should have known.

Insurers, consultants, and fiduciary advisers routinely understand:

- Mortality assumptions.

- Breakeven ages.

- Longevity probabilities.

- Sensitivity analyses.

- The dependence of mortality credits upon survival.

If fiduciaries know that the economic value of the annuity depends heavily upon longevity, participants may reasonably require that information to protect their interests. Failure to disclose that dependency may leave participants with an incomplete understanding of the risks and expected benefits.

F. Mortality Credits Are Better Viewed as Contingent Insurance Benefits

Mortality credits may therefore be more accurately characterized as contingent insurance benefits rather than investment returns.

They resemble:

- Insurance proceeds contingent upon a covered event.

- Longevity insurance.

- Survival-contingent benefits.

Unlike interest or dividends, mortality credits cannot be independently earned, realized, or reinvested prior to the occurrence of the underlying contingency.Their value remains uncertain until the participant actually survives long enough to receive them.

Although mortality credits represent a legitimate actuarial concept at the pooled level, their use in individual participant analyses requires careful fiduciary treatment.

Because mortality credits:

- Depend entirely upon uncertain longevity,

- Cannot be guaranteed to any individual participant,

- May never be realized,

- Are unavailable to participants who die prematurely, and

- Often determine whether an annuity ultimately produces economic value,

A legitimate argumnt can be made that their speculative nature constitutes material information under Section 78(3) of the Restatement (Third) of Trusts

XII. Loyalty Requires More Than Marketing Narratives

ERISA fiduciaries are not salespersons. They are fiduciaries.

The duty of loyalty prohibits presenting only favorable characteristics while omitting economically signif icant disadvantages.A communication emphasizing “Income you cannot outlive,while failing to disclose:

- Low probabilities of economic breakeven,

- Present-value losses,

- Principal forfeiture risk,

- Mortality dependence, or

- Additional costs necessary to preserve principal,

may deprive participants of information necessary to protect their interests. Section 78(3) exists precisely to prevent such informational asymmetry.

Conclusion

ERISA plaintiff’s attorneys are increasingly adding fiduciary breach of duty claims based on the inadequacy or complete lack of necessary disclosures, as required under both ERISA Section 404(a) and Section 78(3) of the Restatement (Third) of Trusts.

What’s become increaisingly clear is that far too may plan sponsors are unaware of their disclosure resposibilities to plan participants, as well as the seriousness of the consequences for a failure to make the disclosures. The fiducairy duty to make the required duties is especially important with regard to in-plan annuities due to the complexity of the investment itself.

Applied to in-plan annuities, Section 78(3) of the Restatement (Third) of Trusts requires fiduciaries to disclose material information that they knew or should have known participants needed to protect their interests.

Under the Supreme Court’s materiality standards, information concerning:

- Mortality-adjusted breakeven ages,

- Present-value losses,

- Probability of principal recovery,

- Likelihood of achieving a commensurate return,

- Costs of principal-protection riders, and

- The possibility of forfeiting principal,

would frequently qualify as material because a reasonable participant would consider such information important in deciding whether to annuitize retirement assets.

The promise of lifetime income may be a benefit for some participants. But fiduciary law requires that participants receive mopre, that they the entire, complete economic picture. A fiduciary’s obligation is not merely to disclose the existence of a guarantee. It is to disclose the material facts necessary for participants to evaluate the value of that guarantee, thet they have sufficient infpormation to make an informed decision.

ERISA’s trust-law foundations, Section 78(3)’s affirmative duty of disclosure, and the Supreme Court’s objective materiality standards all point to the same conclusion: when fiduciaries know, or should know, that actuarial and economic analyses materially affect a participant’s decision to purchase an in-plan annuity, those facts must be disclosed. Silence is not neutrality. Under trust law, silence concerning material facts is itself a fiduciary act subject to judicial scrutiny.

Notes

1.Restatement (Third) of Trusts, Section 78(3). All rights reserved..

2.Varity Corp.v. Howe, 516 U.S. 489 (1996)(Varity)

3.Tibble v. Edison International, 575 U.S. 523, 528-30 (2015) (Tibble).

4.TSC Industries, Inc. v. Northway, Inc., 426 U.S. 438 (1976).

5. Basic, Inc. v. Levinson, 435 U.S.224 (1988).

6. Donovan v. Bierwirth, 680 F.2d 263 (E.D.N.Y. 1981).

7. Tibble, supra.

8. Hughes v. Northwestern University, 595 U.s. 170 (2022).

9. Restatement, Section78(3), supra.

10.Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study).

© Copyright 2026 InvestSense, LLC. All rights reserved.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

You must be logged in to post a comment.