James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

APPELLATE CLOSING ARGUMENT OPPOSING FAB 2026-01

May it please the Court:

At its core, this case presents a simple but critically consequential question:

Can the Department of Labor lawfully encourage fiduciaries to rely upon opaque, highly complex, and often commission-driven investment structures when ERISA expressly requires fiduciaries to conduct an independent and objective investigation of every investment option offered to plan participants?

The answer is no.

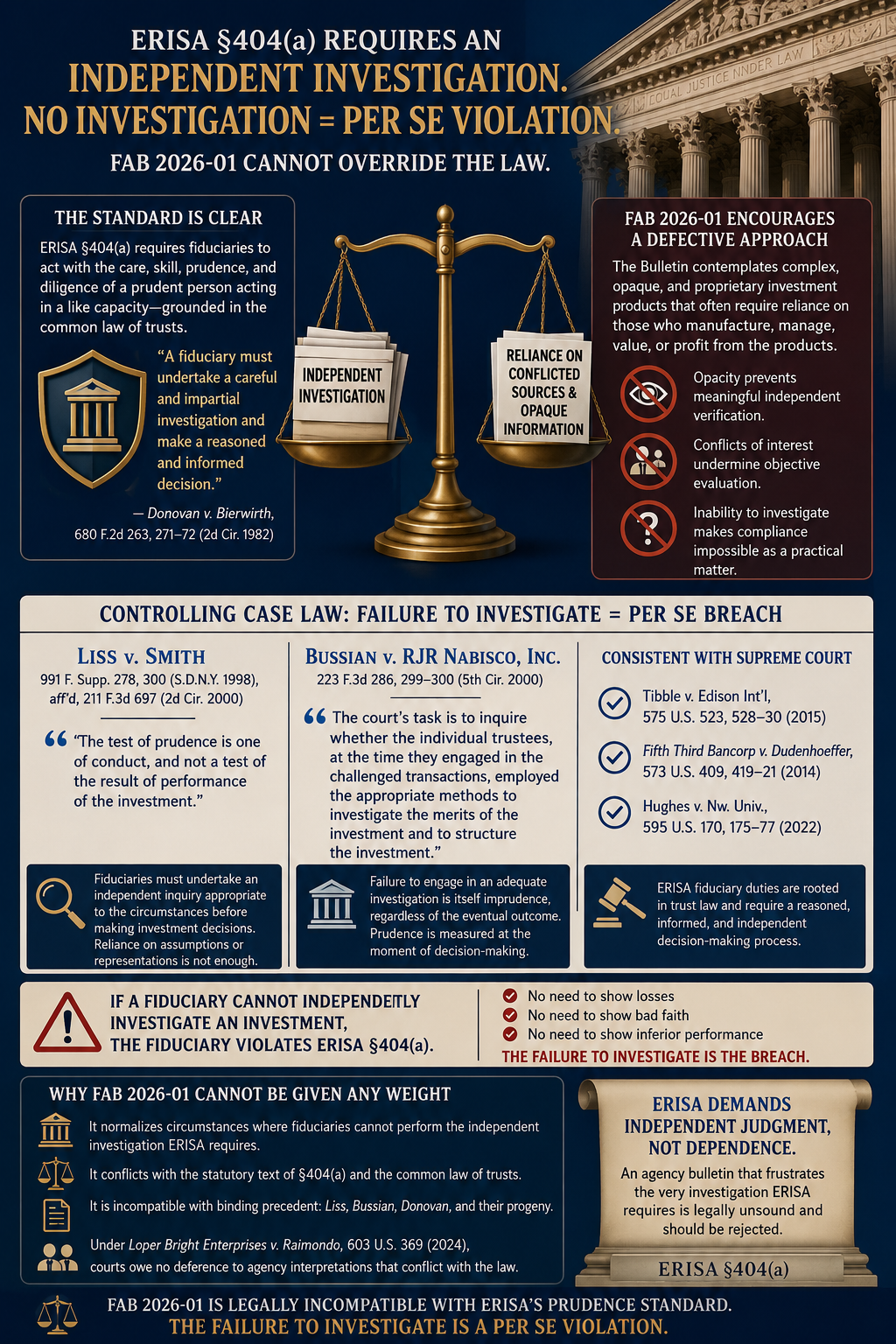

FAB 2026-01 {FAB} rests upon an assumption fundamentally at odds with ERISA’s fiduciary framework. The FAB repeatedly suggests that fiduciaries may satisfy their obligations through process-oriented reliance upon service providers, consultants, product manufacturers, and other market participants. Yet ERISA §404(a) imposes a duty far more demanding. A fiduciary must engage in an independent investigation and objective evaluation sufficient to determine whether an investment is prudent and in the best interests of participants.

The Sixth Circuit’s decision in Gregg v. Transportation Workers of America International1, 343 F.3d 833 (6th Cir. 2003), demonstrates precisely why FAB 2026-01 cannot be reconciled with ERISA. There, the court rejected the notion that fiduciaries may simply rely upon recommendations from individuals whose compensation and incentives are tied to the sale of the very products under consideration. The court emphasized that “one extremely important factor is whether the expert advisor truly offers independent and impartial advice.” The court further recognized that a broker compensated through commissions is not an objective analyst because such a person possesses a financial incentive to consummate transactions rather than provide disinterested fiduciary guidance. The Sixth Circuit accordingly held that reliance upon conflicted advisors could not automatically satisfy ERISA’s fiduciary obligations.

That principle is fatal to the reasoning underlying FAB 2026-01. The investments promoted or facilitated under the FAB frequently involve private markets, alternative assets, structured vehicles, insurance products, collective investment arrangements, proprietary valuation methodologies, layered fee structures, and complex risk-transfer mechanisms. These products are characterized not by transparency but by opacity. They often depend upon assumptions, internal valuations, proprietary algorithms, illiquid markets, and information unavailable to plan sponsors and participants alike.

The practical consequence is unavoidable: the more complex and opaque the investment, the more dependent the fiduciary becomes upon the very parties selling, managing, valuing, or promoting the product. That dependency is precisely what Gregg warned against.

A fiduciary cannot conduct an independent investigation when critical information is unavailable for independent verification. A fiduciary cannot objectively evaluate an investment when the underlying valuation methodology is proprietary. A fiduciary cannot meaningfully assess costs, risks, liquidity constraints, or expected performance when those elements are disclosed only through the representations of interested parties. And a fiduciary cannot satisfy ERISA’s duty of prudence merely by documenting meetings, collecting presentations, and recording procedural steps if the substantive information necessary for independent evaluation remains inaccessible.

Indeed, FAB 2026-01 creates a paradox that the Department never addresses .ERISA §404(a) requires independent investigation. The products contemplated by FAB 2026-01 often require reliance on information controlled by interested market participants. The greater the opacity of the investment, the less capable the fiduciary becomes of conducting the independent investigation ERISA demands. Thus, the very characteristics of these products make compliance with §404(a) increasingly difficult and, in many circumstances, practically impossible.

The Department attempts to solve this problem by elevating procedure over substance. But neither trust law nor Supreme Court precedent permits such a substitution.

ERISA derives directly from the common law of trusts. Under trust law, prudence is not established by the mere appearance of diligence. A trustee’s process has value only insofar as it leads to a prudent substantive decision based upon reliable and adequately investigated information. A checklist cannot transform unknowable facts into known facts. Documentation cannot cure informational asymmetry. Procedure cannot eliminate conflicts of interest.

The informational asymmetry inherent in many alternative and proprietary investment products is especially troubling because it prevents meaningful verification. Plan sponsors must ultimately rely upon the representations of those who design, sell, manage, value, and profit from the investments. Participants face an even greater disadvantage. They lack access to the underlying data, valuation assumptions, risk models, and compensation arrangements necessary to independently assess the prudence of the investments selected on their behalf.

The result is a fiduciary regime increasingly dependent upon trust in market intermediaries rather than independent fiduciary judgment. That is not what Congress enacted.

ERISA was designed to impose the highest duties known to the law. Those duties require fiduciaries to act as skeptical investigators, not passive recipients of sales presentations. They require objective evaluation, not deference to product sponsors. They require verification, not assumption.

The Sixth Circuit recognized in Gregg that reliance upon conflicted advisors cannot substitute for independent fiduciary judgment. The same principle applies with even greater force here, where the products themselves are so complex that independent verification may be unattainable. If fiduciaries cannot independently investigate and evaluate the investment, then they cannot establish that the investment satisfies ERISA’s prudence requirements. No amount of procedural documentation can alter that reality.

Ultimately, FAB 2026-01 asks fiduciaries to navigate a world in which critical information is controlled by interested parties, independent verification is often unavailable, and substantive prudence is presumed from procedural effort. That approach reverses ERISA’s design. It shifts the focus from whether an investment is objectively prudent to whether a fiduciary can document a process surrounding information it cannot independently verify.

The statute demands more.

The common law of trusts demands more.

Gregg demands more.

For these reasons, the Court should reject the reasoning embodied in FAB 2026-01 and reaffirm that ERISA §404(a) requires what it has always required: a genuinely independent, objective, and substantively meaningful investigation of every investment option offered to plan participants—an obligation that cannot be satisfied through reliance upon conflicted sources, opaque products, or procedural formalities divorced from verifiable facts.

Our argument is particularly strong when paired with the precedent established by the decisions in Donovan v. Bierwirth2, Tibble v. Edison International3, Hughes v. Northwestern University4, and Loper Bright Enterprises v. Raimondo5, because together those authorities reinforce that ERISA fiduciary duties are grounded in trust-law principles, require substantive prudence rather than mere procedural compliance, and are not subject to agency reinterpretation that departs from the statute’s common-law foundations. Henry Friendly’s requirement of a “careful and impartial investigation,” quoted favorably in Gregg, is especially useful because it directly links independent investigation to the fiduciary duty of prudence.

A FAILURE TO CONDUCT AN INDEPENDENT INVESTIGATION CONSTITUTES A PER SE VIOLATION OF ERISA’S PRUDENCE REQUIREMENT AND FURTHER DEMONSTRATES THE LEGAL DEFICIENCIES OF FAB 2026-01

The fundamental defect in FAB 2026-01 is not merely that it encourages fiduciaries to consider investment products characterized by substantial opacity, valuation uncertainty, and informational asymmetry. The FAB’s more profound legal flaw is that it effectively diminishes ERISA’s threshold requirement that fiduciaries conduct an independent investigation and evaluation before selecting or retaining plan investments.

Federal courts have repeatedly recognized that the duty to investigate is not a subsidiary component of prudence; rather, it is the essential predicate to any determination that an investment decision is prudent. Where a fiduciary fails to conduct the investigation required by ERISA § 404(a), the fiduciary commits a breach of duty irrespective of whether the investment subsequently performs well or poorly.

As the Second Circuit explained in Liss v. Smith6:

“The test of prudence is one of conduct, and not a test of the result of performance of the investment.”

The court further emphasized that fiduciaries must undertake an independent inquiry appropriate to the circumstances before making investment decisions. The fiduciary’s obligation is not satisfied by reliance upon assumptions, representations, or post hoc justifications. Rather, prudence requires a process capable of producing an informed decision.

Similarly, in Bussian v. RJR Nabisco, Inc7., the Fifth Circuit held that:

“The court’s task is to inquire whether the individual trustees, at the time they engaged in the challenged transactions, employed the appropriate methods to investigate the merits of the investment and to structure the investment.”

The Fifth Circuit further explained that a fiduciary’s failure to engage in an adequate investigation itself constitutes imprudence, regardless of the eventual outcome of the investment decision. Prudence is measured at the moment of decision-making, not through hindsight and not through subsequent performance.

These principles derive directly from trust law and have been repeatedly recognized throughout ERISA jurisprudence. Courts consistently hold that a fiduciary who fails to investigate cannot later justify the decision by pointing to favorable outcomes, nor can procedural formalities substitute for the substantive inquiry required by law.

This principle is especially significant in the context of FAB 2026-01. The FAB contemplates investment products whose complexity, illiquidity, proprietary valuation methodologies, layered fee structures, and limited transparency frequently prevent plan fiduciaries from independently verifying the information necessary to evaluate prudence. In many instances, fiduciaries must necessarily rely upon information generated by the very entities that manufacture, manage, value, market, or profit from the investment products.

The problem is not merely one of potential conflict. The problem is that such dependence may render the independent investigation required by ERISA impossible as a practical matter.

Under Liss, Bussian, and numerous related authorities, the inability to perform an independent investigation is itself legally consequential. If a fiduciary lacks sufficient information to independently evaluate an investment’s risks, costs, liquidity constraints, valuation methodology, and expected performance characteristics, then the fiduciary cannot satisfy the duty of prudence imposed by ERISA § 404(a). The breach occurs at that point.

The fiduciary need not select a demonstrably inferior investment.

The fiduciary need not cause immediate losses.

The fiduciary need not act in bad faith.

The failure to undertake the investigation required by ERISA constitutes the violation.

This principle is consistent with the foundational decision in Donovan v. Bierwirth,8 where the Second Circuit Court of Appealsheld that fiduciaries must employ the care, skill, prudence, and diligence of a prudent person acting in a like capacity and must conduct a thorough and impartial investigation before acting.

Likewise, the Supreme Court has repeatedly emphasized that ERISA fiduciary duties are derived from the common law of trusts and require fiduciaries to engage in a reasoned and informed decision-making process9: Taken together, these authorities establish a straightforward proposition:

A fiduciary who cannot independently investigate an investment cannot establish that the investment is prudent.

A fiduciary who does not independently investigate an investment violates ERISA.

And an agency interpretation that implicitly encourages fiduciaries to proceed despite informational barriers that prevent such investigation cannot be reconciled with ERISA’s statutory framework.

Accordingly, FAB 2026-01 suffers from a defect that extends beyond mere policy disagreement. The FAB 2026-01 effectively normalizes circumstances in which fiduciaries may be unable to perform the very investigation that courts have repeatedly identified as a prerequisite to prudent decision-making.

Under Loper Bright Enterprises v. Raimondo10, 603 U.S. 369 (2024), courts must exercise independent judgment in determining the meaning of statutes and need not defer to agency interpretations that conflict with the governing law.

Because FAB 2026-01 cannot be reconciled with ERISA’s statutory text, trust-law foundations, and the extensive body of precedent requiring an independent fiduciary investigation, the Bulletin is not merely unpersuasive. It is legally incompatible with the standards governing fiduciary conduct under ERISA and therefore should be afforded no weight in judicial proceedings.

The Court should reject any suggestion that procedural documentation, reliance upon conflicted sources, or acceptance of unverifiable information can substitute for the independent investigation and evaluation required by ERISA § 404(a). The case law demonstrates that such failures constitute fiduciary breaches at the moment they occur, rendering FAB 2026-01 fundamentally inconsistent with governing law, effectively a fiduciary breach trap for plan sponsors.

In summation:

“FAB 2026-01 assumes that fiduciaries may prudently select investments whose complexity and opacity prevent meaningful independent verification. Yet Bussian, Liss, Donovan, and their progeny establish the opposite rule: where a fiduciary cannot perform the investigation required by ERISA § 404(a), prudence cannot be established. The failure to investigate is not merely evidence of imprudence—it is the breach itself. An agency bulletin premised upon circumstances that frustrate the very investigation ERISA requires cannot be reconciled with the statute and therefore merits no judicial consideration under Loper Bright.”

Notes

1. Gregg v. Transportation Workers of America International1, 343 F.3d 833 (6th Cir. 2003).

2. Donovan v. Bierwirth, 680 F.2d 263 (E.D.N.Y 1981).

3. Tibble v. Edison International, 575 U.S. 523, 528–30 (2015)

4. Hughes v. Northwestern University, 595 U.S. 170, 175–77 (2022)

5. Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024).

6. Liss v. Smith, 991 F. Supp. 278, 300 (S.D.N.Y. 1998), aff’d, 211 F.3d 697 (2d Cir. 2000).

7. Bussian v. RJR Nabisco, Inc., 223 F.3d 286, 299–300 (5th Cir. 2000).

8. Bierwirth, supra.

9. Tibble, supra; Fifth Third Bancorp v. Dudenhoeffer, 573 U.S. 409, 419–21 (2014); Hughes, supra.

10. Loper Bright Enterprises v. Raimondo,

© Copyright 2026 InvestSense, LLC. All rights reserved

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

You must be logged in to post a comment.