James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

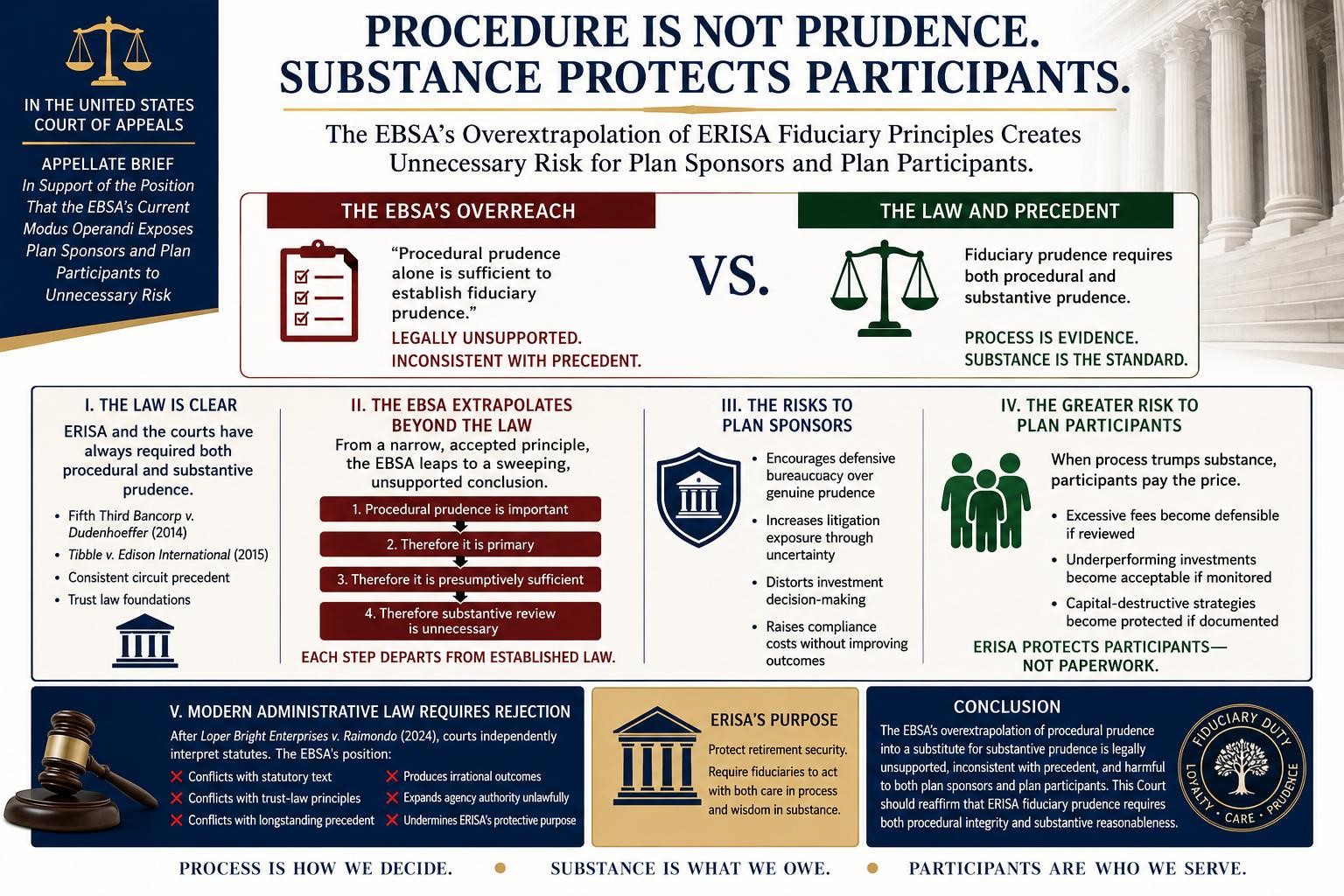

Employee Benefits Security Administration (“EBSA”) may not transform generally accepted fiduciary concepts into categorical legal mandates untethered from statutory text, judicial precedent, or established trust-law principles.

This appeal presents a fundamental question concerning the permissible boundaries of administrative interpretation under the Employee Retirement Income Security Act of 1974 (“ERISA”): whether the Employee Benefits Security Administration (“EBSA”) may transform generally accepted fiduciary concepts into categorical legal mandates untethered from statutory text, judicial precedent, or established trust-law principles.

The answer is no.

The EBSA’s emerging modus operandi reflects a recurring pattern of regulatory overextrapolation whereby narrow, context-dependent judicial observations are elevated into rigid doctrinal propositions. This phenomenon is particularly evident in the agency’s treatment of “procedural prudence.” While courts have long recognized procedural prudence as an important evidentiary component of fiduciary conduct, the EBSA has increasingly suggested—either explicitly or functionally—that adherence to procedural formalities alone is sufficient to establish fiduciary prudence under ERISA.

That position is irreconcilable with ERISA jurisprudence.

The governing case law uniformly establishes that fiduciary prudence under ERISA contains both procedural and substantive dimensions. A prudent process is relevant because it is evidence bearing on the ultimate question of prudence—not because process itself constitutes prudence as a matter of law. The distinction is critical. By collapsing substantive prudence into mere procedural formalism, the EBSA effectively substitutes bureaucratic box-checking for genuine fiduciary accountability.

The consequences are severe.

For plan sponsors, the EBSA’s approach creates regulatory uncertainty, increased litigation exposure, distorted fiduciary incentives, and compliance regimes divorced from actual participant welfare. For participants, the approach risks legitimizing economically harmful investment decisions merely because fiduciaries can demonstrate the existence of a superficially documented process.

ERISA was enacted to protect retirement security, not to create a safe harbor for imprudent outcomes cloaked in procedural ritualism.

Under modern administrative law principles, including the Supreme Court’s rejection of reflexive agency deference in Loper Bright Enterprises v. Raimondo, courts must independently determine whether the EBSA’s interpretations are consistent with statutory text, trust-law principles, and binding precedent. The EBSA’s procedural-prudence-only framework fails that inquiry.

STATEMENT OF THE ISSUE

Whether the EBSA exceeds its lawful interpretive authority under ERISA by extrapolating the generally accepted principle that procedural prudence is relevant to fiduciary analysis into the unsupported proposition that procedural prudence alone is sufficient to establish fiduciary prudence, notwithstanding longstanding precedent requiring both procedural and substantive prudence.

STANDARD OF REVIEW

Questions involving statutory interpretation, the scope of agency authority, and the legal meaning of fiduciary obligations under ERISA are reviewed de novo.

Following Loper Bright Enterprises v. Raimondo, courts are no longer required to defer reflexively to agency interpretations merely because statutory ambiguity exists. Rather, courts must exercise independent judgment in determining the best interpretation of the statute.

Accordingly, the EBSA’s interpretive assertions regarding fiduciary prudence are entitled only to the persuasive weight justified by their reasoning, consistency, and fidelity to ERISA’s statutory framework and common-law trust principles

ARGUMENT

I. ERISA FIDUCIARY PRUDENCE HAS ALWAYS REQUIRED BOTH PROCEDURAL AND SUBSTANTIVE PRUDENCE

ERISA’s fiduciary framework derives substantially from traditional trust law. Section 404(a)(1)(B) requires fiduciaries to act:

“with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use.”

This language imposes a duty concerning conduct and outcomes alike.

Courts consistently recognize that procedural prudence is important because it provides evidence regarding whether fiduciaries acted prudently. But courts have never held that procedural compliance itself conclusively establishes prudence.

Indeed, the entire structure of ERISA litigation presupposes that procedural evidence is probative rather than dispositive.

The Supreme Court’s decision in Fifth Third Bancorp v. Dudenhoeffer emphasized careful context-sensitive scrutiny of fiduciary decision-making, not blind reliance on procedural formalities. Likewise, Tibble v. Edison International reaffirmed that fiduciaries possess a continuing duty to monitor investments substantively, not merely to document periodic review procedures.

Numerous circuit courts similarly have rejected the notion that process alone immunizes fiduciaries from liability. Courts routinely examine:

- The economic substance of fiduciary decisions;

- The reasonableness of fees;

- Comparative performance;

- Risk-adjusted characteristics;

- Availability of superior alternatives;

- Participant impact; and

- Long-term economic consequences.

Such inquiries would be legally irrelevant if procedural prudence alone established fiduciary compliance.

The EBSA’s apparent extrapolation therefore conflicts directly with the judicial understanding of prudence as an integrated substantive and procedural standard.

II. THE EBSA’S EXTRAPOLATION CONSTITUTES IMPROPER ADMINISTRATIVE BOOTSTRAPPING

The agency’s reasoning reflects a classic form of administrative bootstrapping.

The original proposition—that procedural prudence is relevant evidence of fiduciary prudence—is uncontroversial. From that modest premise, however, the EBSA appears to infer progressively broader conclusions:

- Procedural prudence is important;

- Therefore procedural prudence is primary;

- Therefore procedural prudence is presumptively sufficient;

- Therefore substantive review becomes secondary or unnecessary.

Each inferential step departs further from established law.

This interpretive inflation mirrors the precise administrative excesses modern separation-of-powers jurisprudence seeks to prevent. Agencies may clarify statutory obligations; they may not manufacture novel legal standards by exaggerating isolated concepts beyond their logical and legal limits.

ERISA nowhere states that fiduciary prudence may be satisfied through procedural documentation alone. Nor has any controlling court adopted such a principle.

The EBSA’s approach effectively rewrites ERISA’s prudence requirement into a “reasonable paperwork” standard.

But ERISA protects retirement assets, not administrative appearances.

A fiduciary who meticulously documents a catastrophically imprudent investment decision has not fulfilled ERISA’s fiduciary obligations merely because meeting minutes exist.

Likewise, a fiduciary cannot satisfy the duty of prudence by engaging consultants, holding committee meetings, or generating extensive reports if the underlying investment decisions remain objectively unreasonable relative to participant interests.

To conclude otherwise would sever fiduciary law from economic reality.

III. THE EBSA’S POSITION IS INCONSISTENT WITH TRUST-LAW FOUNDATIONS UNDERLYING ERISA

ERISA fiduciary duties are informed by the common law of trusts. Traditional trust law never treated procedure as a substitute for substantive prudence.

The prudent-investor rule evaluates whether fiduciaries exercised reasonable judgment in pursuing beneficiary interests under prevailing circumstances. Process matters because it informs the reliability of fiduciary judgment—not because it independently satisfies fiduciary obligations irrespective of substantive consequences.

The Restatement principles underlying modern fiduciary law repeatedly emphasize that fiduciaries must act reasonably in light of risk, return, diversification, preservation of capital, and beneficiary objectives.

Under trust law:

- A carefully documented imprudent investment remains imprudent;

- A formally reviewed excessive-fee arrangement remains excessive;

- A procedurally vetted economically irrational strategy remains irrational.

The EBSA’s procedural formalism therefore represents a departure not only from ERISA precedent but from the trust-law heritage Congress incorporated into ERISA itself.

IV. THE EBSA’S APPROACH CREATES SYSTEMIC RISKS FOR PLAN SPONSORS

The agency’s framework creates profound practical and legal instability for plan sponsors.

A. It Encourages Defensive Bureaucracy Rather Than Genuine Prudence

If procedural documentation becomes the primary determinant of prudence, fiduciaries are incentivized to prioritize process optics over substantive participant outcomes.

This creates a culture of defensive compliance characterized by:

- excessive consultant reliance;

- overdocumentation;

- procedural redundancy;

- checkbox governance; and

- litigation-oriented record creation.

Such conduct increases plan costs without necessarily improving participant welfare.

B. It Increases Litigation Exposure Through Regulatory Ambiguity

The EBSA’s shifting and expansive interpretations create substantial uncertainty concerning what fiduciaries must actually do to satisfy ERISA obligations.

Plan sponsors face a paradoxical environment where:

- formal procedures may be deemed sufficient during investigations,

yet - plaintiffs may still challenge substantive outcomes in litigation.

This inconsistency produces precisely the unpredictability ERISA was intended to avoid.

C. It Distorts Investment Decision-Making

A process-centric regime may discourage fiduciaries from considering innovative or participant-beneficial investment structures if such structures deviate from conventional procedural templates.

Fiduciaries may instead default toward “litigation-safe” decisions rather than economically superior decisions.

That distortion harms retirement outcomes.

V. THE GREATEST RISKS FALL UPON PLAN PARTICIPANTS

The ultimate victims of procedural formalism are plan participants.

ERISA exists to protect beneficiaries’ retirement security, purchasing power, and long-term financial welfare. A framework that elevates process above substance undermines those objectives.

Under the EBSA’s apparent approach, participants could suffer substantial economic harm while fiduciaries remain insulated because procedural artifacts exist demonstrating meetings, reviews, and consultant involvement.

Such a regime creates the dangerous possibility that:

- excessive fees become defensible if periodically reviewed;

- underperforming investments become acceptable if monitored;

- capital-destructive strategies become protected if documented.

This transforms fiduciary prudence from a substantive duty of loyalty and care into an exercise in administrative self-protection.

ERISA does not tolerate such a result.

VI. MODERN ADMINISTRATIVE LAW REQUIRES REJECTION OF THE EBSA’S OVEREXPANSIVE INTERPRETATIONS

Under Loper Bright Enterprises v. Raimondo, courts must independently determine statutory meaning rather than defer automatically to agency preferences.

The EBSA’s procedural-prudence-only extrapolation warrants little persuasive weight because it:

- conflicts with statutory text;

- conflicts with trust-law principles;

- conflicts with longstanding precedent;

- produces economically irrational outcomes;

- expands agency authority without congressional authorization; and

- undermines ERISA’s participant-protection purposes.

Moreover, the Supreme Court’s recent administrative-law jurisprudence repeatedly warns against agency efforts to discover transformative powers in vague statutory language.

The EBSA’s attempt to redefine fiduciary prudence through interpretive escalation is precisely the type of administrative overreach courts are now obligated to scrutinize skeptically.

CONCLUSION

The EBSA’s current interpretive trajectory reflects an increasingly problematic pattern of regulatory overextrapolation whereby modest and generally accepted legal principles are transformed into sweeping doctrinal assertions unsupported by statutory text, trust law, or judicial precedent.

Exhibit A is the agency’s apparent suggestion that procedural prudence alone may establish fiduciary prudence under ERISA.

That proposition is legally indefensible.

ERISA fiduciary prudence has always required a synthesis of procedural and substantive prudence. Process is evidence—not destiny. Documentation is relevant—not dispositive. Administrative ritual cannot substitute for genuine fiduciary judgment directed toward participant welfare.

By elevating procedural formalism above substantive fiduciary accountability, the EBSA exposes plan sponsors to regulatory confusion, increased litigation risk, distorted incentives, and unnecessary compliance burdens while simultaneously exposing participants to economically harmful fiduciary decisions shielded by superficial procedural compliance.

The Senate HELP committee should reject the EBSA’s unsupported extrapolations and reaffirm that ERISA fiduciary prudence remains grounded in both procedural integrity and substantive reasonableness, consistent with statutory text, trust-law principles, and longstanding jurisprudence, and require the EBSA to act accordingly going forward,

© Copyright 2026 InvestSense, LLC. All rights reserved

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

You must be logged in to post a comment.