James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

May it please the Court:

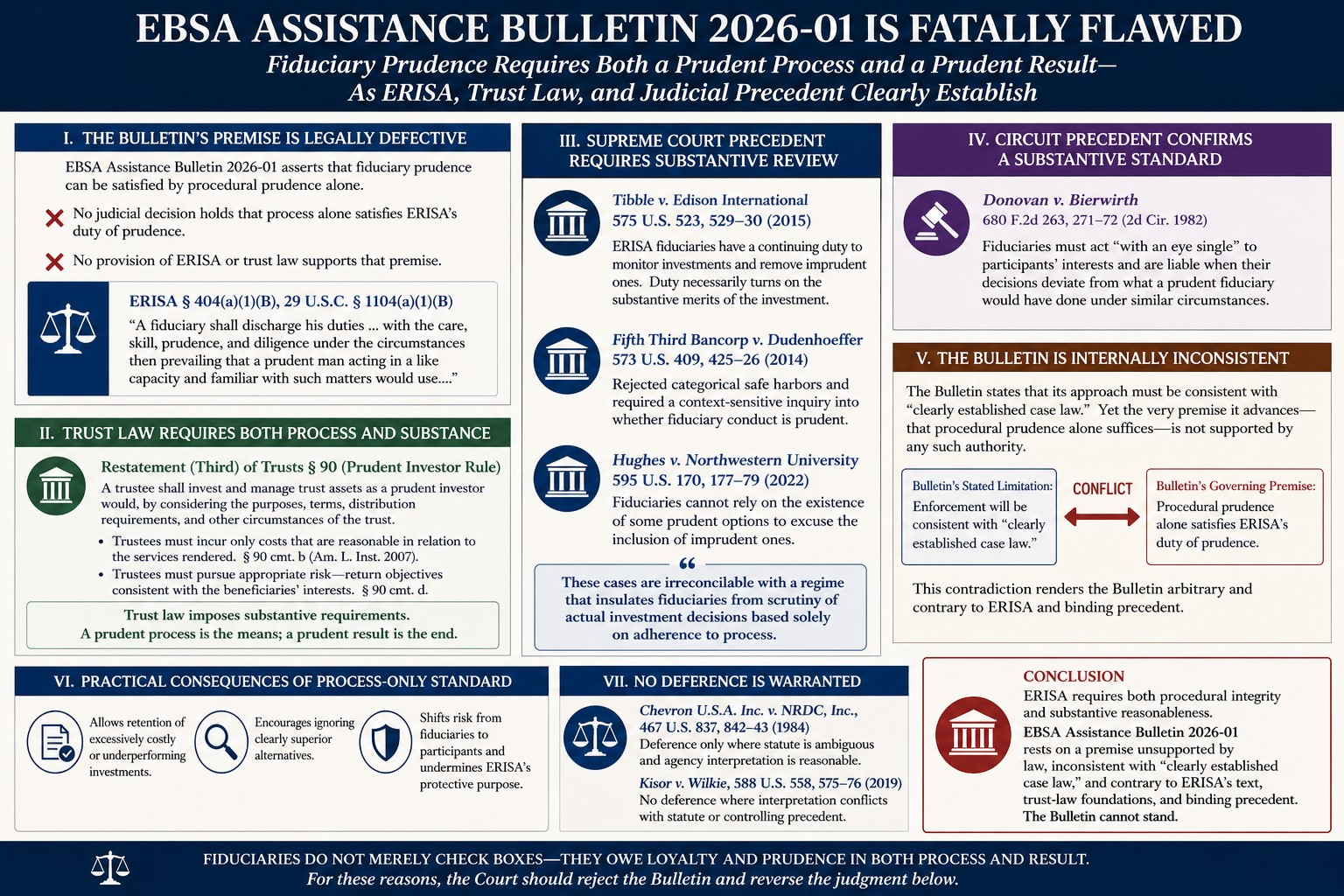

EBSA Assistance Bulletin 2026-01 (Bulletin) contains a defect that is not merely analytical, but structural: it is internally inconsistent on its face. The Bulletin expressly conditions enforcement on alignment with “clearly established case law,” yet the governing premise it adopts—that fiduciary prudence may be satisfied by process alone—is unsupported by, and in tension with, the very body of law it invokes. That contradiction is fatal.

Start with the agency’s own limiting principle. By tethering enforcement to “clearly established case law,” EBSA concedes that its authority is bounded by existing judicial interpretations of ERISA and its incorporated trust-law standards. That concession should end the inquiry, because no such “clearly established” authority endorses a purely procedural conception of prudence. To the contrary, the case law uniformly requires a combined assessment of process and substance.

The Supreme Court’s ERISA jurisprudence leaves no room for EBSA’s position. In Tibble v. Edison International, the Court grounded ERISA’s fiduciary duties in trust law and emphasized the ongoing duty to monitor and remove imprudent investments—an obligation that necessarily turns on the substantive merits of the investment, not merely the process used to select it. 575 U.S. 523, 529–30 (2015). In Fifth Third Bancorp v. Dudenhoeffer, the Court rejected categorical presumptions that would insulate fiduciaries from meaningful scrutiny, insisting instead on a context-sensitive evaluation of whether fiduciary conduct is actually prudent. 573 U.S. 409, 425–26 (2014). And in Hughes v. Northwestern University, the Court made explicit that fiduciaries cannot rely on the existence of some prudent options to excuse the inclusion of imprudent ones. 595 U.S. 170, 177–79 (2022). That holding is irreconcilable with a regime in which process alone suffices.

Lower courts have applied the same integrated standard. In Donovan v. Bierwirth, the Second Circuit held that fiduciaries must act “with an eye single” to participants’ interests and are liable where their decisions deviate from what a prudent fiduciary would have done. 680 F.2d 263, 271–72 (2d Cir. 1982). That inquiry is inherently substantive: it evaluates the economic reasonableness of the decision, not just the procedural steps taken to reach it.

The trust-law principles ERISA incorporates confirm the same point. The Restatement (Third) of Trusts § 90 does not reduce prudence to process. It imposes a duty to incur only reasonable costs and to pursue appropriate risk–return objectives for beneficiaries. Restatement (Third) of Trusts § 90 cmt. b, d (Am. L. Inst. 2007). Those are substantive constraints. A fiduciary who follows a careful process but selects objectively inferior or excessively costly investments has not satisfied the duty of prudence under trust law.

Against that backdrop, the Bulletin’s internal contradiction becomes clear. It purports to require adherence to “clearly established case law,” yet it advances a standard—procedural prudence alone—that no such case law recognizes. That is not an interpretation; it is a departure. And it is a departure in a direction the Supreme Court has repeatedly rejected: toward categorical insulation of fiduciary conduct from substantive review.

This inconsistency has concrete consequences. By anchoring enforcement to “clearly established law” while simultaneously redefining that law in a way that strips out substantive review, EBSA creates an illusory constraint. The Bulletin appears to narrow agency discretion, but in practice expands it—allowing fiduciaries to claim compliance based on process alone, even where outcomes are economically indefensible. That result cannot be reconciled with ERISA’s text, which requires fiduciaries to act with the “care, skill, prudence, and diligence” of a prudent person, 29 U.S.C. § 1104(a)(1)(B), nor with ERISA’s purpose of protecting plan participants. See 29 U.S.C. § 1001(b).

Nor is this a gap in the law that the agency may fill. Where the Supreme Court and the circuits have already articulated the governing standard, there is no ambiguity for the agency to resolve. See Chevron U.S.A. Inc. v. Natural Resources Defense Council, Inc., 467 U.S. 837, 842–43 (1984). And even if there were, an interpretation that conflicts with those precedents would be unreasonable as a matter of law. Cf. Kisor v. Wilkie, 588 U.S. 558, 575–76 (2019).

In short, EBSA cannot have it both ways. It cannot invoke “clearly established case law” as a limiting principle while advancing a fiduciary standard that no such law supports. The Bulletin’s premise is not merely unpersuasive—it is unmoored from ERISA, from trust law, and from controlling precedent. That internal inconsistency renders the Bulletin arbitrary, legally unsound, and undeserving of judicial acceptance. For those reasons, and for the reasons previously stated, the Court should reject EBSA’s formulation and reaffirm that fiduciary prudence under ERISA requires both procedural integrity and substantive reasonableness.Discuss the fact that the EBSA’s arguments suggesting stronger pleading standards and restrictions on discovery are inconsistent with the Federal Rules of Civil Procedure, as are the EBSA’s attempts to decide cases on their merits, which is the exclusive province of the courts, not federal agencies

That aspect of the Bulletin presents an additional—and independently disqualifying—legal flaw. EBSA is not merely misreading ERISA’s fiduciary standard; it is attempting to reshape federal litigation itself in a manner that conflicts with governing procedural law and exceeds its institutional role.

First, the Bulletin’s suggestion that ERISA claims should be subject to heightened pleading standards is incompatible with the framework established by the Federal Rules of Civil Procedure. Rule 8(a)(2) requires only “a short and plain statement of the claim showing that the pleader is entitled to relief.” The Supreme Court’s decisions in Bell Atlantic Corp. v. Twombly, 550 U.S. 544, 555–56 (2007), and Ashcroft v. Iqbal, 556 U.S. 662, 678–79 (2009), clarified that complaints must be “plausible,” not that they must plead detailed evidence or prove their case at the outset. Nothing in those decisions authorizes an agency—through sub-regulatory guidance—to impose ERISA-specific super-pleading requirements.

To the contrary, the Supreme Court has repeatedly rejected efforts to impose categorical or heightened barriers at the pleading stage in ERISA fiduciary litigation. In Hughes v. Northwestern University, 595 U.S. 170, 177–79 (2022), the Court reversed dismissal of fiduciary breach claims precisely because the lower courts had demanded too much at the pleading stage. The Court emphasized that ERISA claims must be evaluated under ordinary pleading standards, with context-specific analysis—not judicially or administratively imposed shortcuts that truncate meritorious claims before discovery.

Second, the Bulletin’s effort to restrict access to discovery is equally inconsistent with the Rules. Under Rule 26(b)(1), parties are entitled to obtain discovery regarding any nonprivileged matter that is relevant to any party’s claim or defense and proportional to the needs of the case. In ERISA fiduciary breach cases, discovery is often indispensable because the relevant information—fee structures, benchmarking data, fiduciary deliberations—is uniquely within the control of the fiduciaries themselves. The Supreme Court recognized this asymmetry in Fifth Third Bancorp v. Dudenhoeffer, 573 U.S. 409, 425 (2014), cautioning courts to balance the need to weed out meritless claims against the reality that plaintiffs frequently require discovery to substantiate their allegations.

EBSA’s position effectively inverts that balance. By encouraging early merits-based screening and constrained discovery, it imposes evidentiary burdens at the pleading stage that the Federal Rules do not permit. That is not an interpretation of ERISA; it is an attempt to rewrite the procedural architecture governing federal litigation.

Third—and most fundamentally—the Bulletin intrudes into the adjudicative function itself. Determining whether a fiduciary’s conduct was prudent under ERISA is a merits question entrusted to Article III courts. See, e.g., Firestone Tire & Rubber Co. v. Bruch, 489 U.S. 101, 110–11 (1989) (grounding ERISA adjudication in trust-law principles applied by courts). Agencies may enforce statutes and promulgate rules within delegated authority, but they do not decide private ERISA breach claims on their merits. By framing certain categories of conduct as effectively compliant—based on process alone—and by encouraging dismissal prior to factual development, EBSA is functionally pre-judging cases that Congress assigned to the judiciary..

Finally, this procedural overreach reinforces the Bulletin’s internal inconsistency. EBSA claims fidelity to “clearly established case law,” yet no such case law authorizes an agency to heighten pleading standards, curtail discovery, or effectively adjudicate fiduciary prudence through guidance documents. The governing authorities—Rule 8, Rule 26, and decisions such as Twombly, Iqbal, Hughes, and Dudenhoeffer—point in the opposite direction: toward ordinary pleading standards, context-sensitive analysis, and fact development through discovery.

That separation-of-functions problem is not abstract. It has concrete doctrinal consequences. The Federal Rules reflect a deliberate allocation of responsibility: pleadings test legal sufficiency; discovery develops the factual record; and summary judgment or trial resolves the merits. EBSA’s approach collapses those stages into a single, front-loaded inquiry dominated by agency-preferred factors. That approach is incompatible with the Rules Enabling Act framework and with the Supreme Court’s repeated insistence that ERISA fiduciary claims be evaluated through ordinary litigation processes—not through categorical screens or presumptions imposed from outside the judiciary.

In short, EBSA’s litigation-focused positions are not merely unpersuasive—they are ultra vires. They conflict with the Federal Rules of Civil Procedure, encroach on the judiciary’s exclusive role in adjudicating ERISA claims, and further underscore that the Bulletin is not an application of “clearly established law,” but a departure from it.

As a result, the Senate should schedule EBSA oversight hearings as soon as possible to detrmine if the totality of the EBSA actions thus far have constitutued a bretrayal of American workers. One can easily argue , with merit, that the unexplainied decision not to pursue the appeal of the Retirement Security Rule was a betryal of American wrol=kers, especially given given the support of both the the support the Rule and the process that the DOL employed, by two prominent federal judges, Judge Barbara Lynn of the Northernern District of Texas, and Judge Carl Stewart of the Fifth Circuirt, who openly dissented from the Fiffth Circuit in the courts’s decision to stay the enforcement of the Rule.

The Senate should also inquire into why the EBSA, in connection with the decision not to pursue the Retirement Security Rule decision, promised that a new version of the Rule would be forthcoming, only to have the EBSA subsequently announce that no such revision would be forthcoming, with no meaningful explanantion for the change in plans. During this time, the EBSA has issued several amicus briefs, all supporting and advocating on behalf of the best interests of plan sponsors and the insurance industry, at the expense of plan participants and their beneficiries, the very parties that ERISA states are to be protected.

© Copyright 2026 InvestSense, LLC. All rights reserved.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

You must be logged in to post a comment.