James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

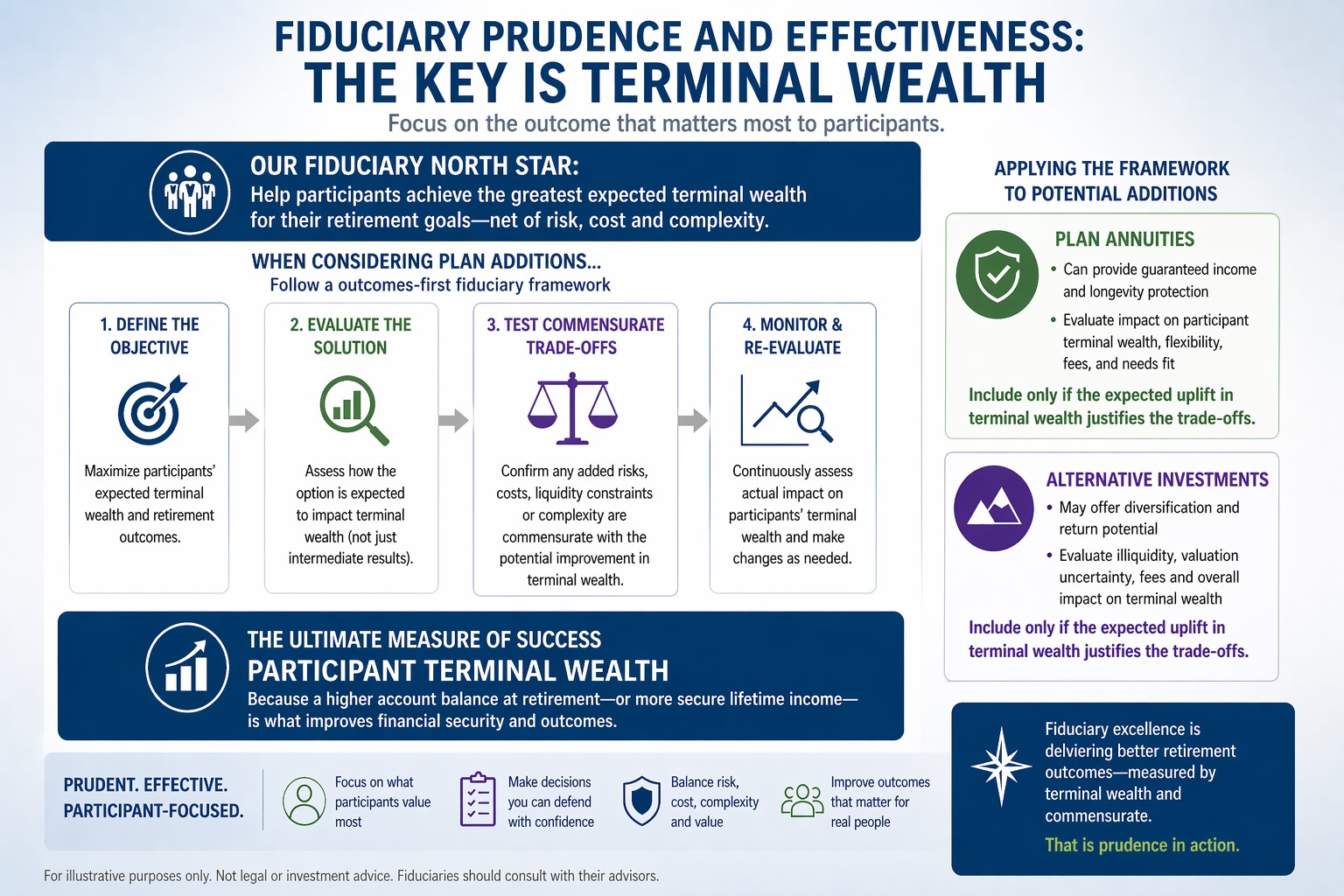

A sound evaluation of fiduciary prudence must ultimately be anchored in outcomes, not just process—and in the context of long-term financial decision-making, the most meaningful outcome is terminal wealth. Fiduciaries are entrusted not merely with following procedures, but with stewarding assets in a way that maximizes the beneficiary’s financial position at the end of the investment horizon. While process-oriented metrics like diversification, cost control, and adherence to policy statements are important, they are only proxies for what truly matters: the financial result delivered.

This principle becomes especially clear when annuities that require annuitization enter the analysis. Such products fundamentally alter the nature of wealth by converting a liquid, inheritable asset base into an irreversible income stream. Once annuitization occurs, the remaining capital is no longer accessible, transferable, or responsive to changing circumstances. That decision locks in a terminal wealth outcome at the moment of conversion, often eliminating residual value altogether unless specific (and typically costly) riders are in place.

A fiduciary evaluating whether to recommend or include such an annuity must therefore weigh not just the stability of income provided, but the impact on total terminal wealth. An income stream may appear attractive in isolation, but if it comes at the cost of significantly reduced aggregate wealth—particularly when compared to alternative strategies that preserve liquidity and optionality—it raises serious questions about prudence. The fiduciary duty of care demands a holistic comparison, not a narrow focus on income smoothing or behavioral benefits.

Moreover, terminal wealth captures critical dimensions of financial well-being that annuitization can compromise. These include legacy goals, flexibility in response to unforeseen expenses, and the ability to adapt to market or personal changes. A strategy that maximizes guaranteed income but leaves no residual estate may fail to align with a client’s broader objectives, even if it appears “safe” on the surface. Prudence, in this sense, cannot be reduced to minimizing volatility or ensuring predictability; it must incorporate the full economic trade-offs involved.

Importantly, focusing on terminal wealth does not imply ignoring risk—it reframes it. The relevant question is not simply whether an approach reduces short-term uncertainty, but whether it does so efficiently relative to the long-term cost. Annuities that require annuitization often embed significant fees, mortality credits, and insurer profit margins, all of which can erode expected value. A fiduciary who overlooks these impacts in favor of superficial guarantees risks prioritizing form over substance.

In conclusion, terminal wealth serves as a unifying metric that integrates return, risk, cost, and constraint into a single, outcome-oriented standard. Especially when dealing with irreversible decisions like annuitization, it provides a clear lens through which fiduciary prudence can be judged. A process may be compliant, and an income stream may be stable, but if the end result unnecessarily diminishes the client’s total financial position, the fiduciary has fallen short of their fundamental obligation.

For fiduciary prudence purposes, compare two paths for a 65-year-old female investing $100,000:

- Option A: Immediate annuity (fully annuitized, no residual value)

- Option B: Laddered portfolio of Treasury notes/CDs (principal preserved, modest yield, terminal wealth remains)

Key Assumptions

- Immediate annuity payout: ~$6,500/year (typical for a 65F, no inflation adjustment)

- Life expectancy: ~21 years (to age 86)

- Discount rate (risk-free benchmark): 3.5%

- Laddered portfolio yield: 3.5% annually

- Portfolio withdrawals: matched to annuity income ($6,500/year)

- Residual portfolio value remains accessible (terminal wealth)

1. Present Value & Terminal Wealth Comparison

| Metric | Immediate Annuity | Laddered T-Notes/CD Portfolio |

| Initial Investment | $100,000 | $100,000 |

| Annual Income | $6,500 | $6,500 (self-withdrawal) |

| Present Value of Income (21 yrs @ 3.5%) | ~$96,000 | ~$96,000 |

| Terminal Wealth at Life Expectancy | $0 | ~$100,000 |

| Liquidity | None | Full (subject to ladder structure) |

| Mortality Credit Benefit | Yes | No |

| Residual Estate Value | None | Preserved |

2. Mortality-Adjusted Breakeven Analysis

To determine when the annuity “wins” on a terminal wealth basis, we calculate the age at which cumulative annuity payments (discounted) exceed both:

- The initial $100,000, and

- The preserved terminal wealth from the ladder strategy

| Age | Years of Payments | Cumulative Payments | PV of Payments @3.5% | Ladder Terminal Wealth | Net Advantage |

| 75 | 10 | $65,000 | ~$54,000 | ~$100,000 | Ladder dominates |

| 80 | 15 | $97,500 | ~$77,000 | ~$100,000 | Ladder dominates |

| 86 (life expectancy) | 21 | $136,500 | ~$96,000 | ~$100,000 | Ladder slightly ahead |

| 90 | 25 | $162,500 | ~$110,000 | ~$100,000 | Rough breakeven |

| 95 | 30 | $195,000 | ~$130,000 | ~$100,000 | Annuity dominates |

3. Interpretation for Fiduciary Prudence

- At normal life expectancy (86):

The annuity does not fully recover its opportunity cost when evaluated on a present value + terminal wealth basis. - Breakeven occurs ~age 90+:

The annuity requires above-average longevity to justify its irreversible loss of capital. - Mortality risk is the pivot:

The annuity only outperforms if the individual lives significantly longer than expected, effectively “earning” mortality credits. - Terminal wealth gap is decisive:

The ladder strategy preserves ~$100,000 in estate value, while the annuity reduces this to zero.

4. Fiduciary Conclusion

From a fiduciary prudence perspective grounded in terminal wealth:

- The annuity represents a longevity insurance bet, not a wealth-maximizing strategy under average conditions.

- The laddered portfolio dominates under expected mortality, offering equivalent income, retained liquidity, and preserved terminal wealth.

- Recommending annuitization without clear evidence of above-average longevity or strong income certainty needs risks subordinating total economic value to income framing.

The breakeven analysis shows that annuitization must be justified not by its guarantees alone, but by a probabilistic expectation of extended lifespan sufficient to overcome the embedded loss of capital. Prudent investors and prudent investment fiduciaries simply do not voluntairly forfeit capital without even the opportunity to receive a commensurate return. My investors shaerw the same sentiments of Mark Twain – “I am not so concerned about the return ON my investment as I am the return OF my investment! Yet, a simple breakeven analysis of most in-plan annuities, once present value and mortality risk are factored in, shows that is the likely result.

This is why we advised our fiduciary risk minimization clients to insiste that anyone recommending an in-plan annuity for their plan provide them with a properly prepared written breakeven analysis similar to the one contained herein. Why written? It can conveniently serve as “Exhibit A” if litigation becomes necessary. Requiring such documentation also helps establich a plan sponsor’s due diligence process, which is always a good thing in fiduciary litigation. Full disclosure: Don’t expect an in-plan annuity peddler to agree to your request. After they know the quality of their products. Now so do you. As arguably the nation’s leading ERISA attorneys, Fred Reish, is fond of saying: “Forewarned is forearmed.”

© Copyright 2026 InvestSense, LLC. All rights reserved.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

You must be logged in to post a comment.