I am on record as saying that (a) ERISA plaintiff’s attorneys should never lose a properly vetted 401(k)/403(b) action, and (b) the amount of 401(k)/403(b) litigation is going to continue to increase. Those opinions are based on three trends within those industries.

1. Many plan sponsors do not even realize that they are fiduciaries.

A J.P. Morgan survey found that 43% of plan sponsors surveyed were not aware that they are plan fiduciaries.1 Subsequent studies suggest that the problem still persists. It is highly unlikely that plan sponsors who do not even realize that they are fiduciaries realize what their fiduciary duties are in compliance with same.

1. Why do you offer so many investment options within the plan?

2. Why do you offer these specific investment options?

Far too often, the response is either “that’s what our plan adviser told us to do” or a simple shrug of the shoulders. My response – “What you are actually doing is unnecessarily exposing yourself to potential fiduciary liability. Simplicity is the new sophistication.”

Most plans try to qualify for ERISA 404(c) status in order to reduce their liability exposure. There are approximately 20-25 requirements that a plan must satisfy in order to qualify for 404(c) status. Fred Reish, one of the nation’s leading ERISA attorneys, has stated that many plans mistakenly believe that they have satisfied 404(c)’s requirements.

One thing has always fascinated me about the language in 404(c)’s requirements:

(3) Broad range of investment alternatives.

(i) A plan offers a broad range of investment alternatives only if the available investment alternatives are sufficient to provide the participant or beneficiary with a reasonable opportunity to:

(A) Materially affect the potential return on amounts in his individual account with respect to which he is permitted to exercise control and the degree of risk to which such amounts are subject;

(B) Choose from at least three investment alternatives:

(1) Each of which is diversified;

(2) Each of which has materially different risk and return characteristics;

(3) Which in the aggregate enable the participant or beneficiary by choosing among them to achieve a portfolio with aggregate risk and return characteristics at any point within the range normally appropriate for the participant or beneficiary; and

(4) Each of which when combined with investments in the other alternatives tends to minimize through diversification the overall risk of a participant’s or beneficiary’s portfolio…. (emphasis added)2

A valid argument can be made that a plan could comply with the three investment alternatives requirement simply with a plan consisting of a broad-based equity index fund, a broad-based fixed income index fund, and a money market fund. I would suggest that a plan at least add a broad-based international index fund to this three-investment plan, and possibly one or two other funds.

Many plan advisers have told me that this type of simplified plan is absurd and will expose plan sponsors to liability, that their 15-20 investment options plans are absolutely compliant and legally appropriate. To that, I respond with my friend Rick Ferri’s quote–“Complexity is just job security.”

When it comes to designing 401(k)/403(b) plans, the adage “less is more” definitely holds true as far as exposing plan sponsors to unnecessary liability. As the Supreme Court recently pointed out, each individual investment must be prudent.3 Consequently, the more investment options a plan offers, the greater the chances of a breach of the plan sponsor’s fiduciary duties.

Another issue I often see is plan sponsors mistakenly believing that they have a duty to ensure the ultimate performance of the investment options chosen for a plan. A plan sponsor’s fiduciary duties only involve the prudent selection of the plan’s investment options, not the eventual performance of such investments. Again, another example of plan sponsors making compliance with ERISA more difficult than it actually is, which provides a nice transition into my third point.

3. The Reg BI “reasonably available alternatives” vs. ERISA “fiduciary prudence” liability trap.

401(k) and 403(b) plans often hire third-parties to help them in administering the plan. These consultants are often what are known as 3(21) or 3(38) fiduciaries. While a lengthy discussion of the differences between the two is beyond the scope of this post, a simplified explanation is that a 3(21) adviser provides investment advice, while a 3(38) adviser provides investment management.

These consultants are often stockbrokers or dually registered stockbrokers/investment adviser representatives. Under Regulation “Best Interest”4 (Reg BI), the SEC’s new standard of conduct for stockbrokers, the stockbroker is required to always put a customer’s best interest first and to consider various factors, including the cost associated with any product recommendations.

In deciding on investment recommendations, a stockbroker is required to consider and compare “reasonably available alternatives.” However, as the saying goes, “the devil is in the details.”

In the Proposing Release, we provided guidance on what types of recommendations would or would not be in the best interest of a particular retail customer. In particular, the Proposing Release stated that where a broker-dealer is choosing among identical securities available to the broker-dealer, it would be inconsistent with the Care Obligation to recommend the more expensive alternative for the customer. Similarly, in the Proposing Release, we noted our belief that it would be inconsistent with the Care Obligation if the broker-dealer made a recommendation to a retail customer in order to: maximize the broker-dealer’s compensation, further the broker-dealer’s business relationships,…”5

We also stated that under the Care Obligation a broker-dealer generally should consider reasonable alternatives, if any, offered by the broker-dealer in determining whether it has a reasonable basis for making the recommendation….6

Further, the Proposing Release indicated that under the Care Obligation, when a broker-dealer recommends a more expensive security or investment strategy over another reasonably available alternative offered by the broker-dealer,….(emphasis added)7

And yet, I would argue that that is exactly what is happening by allowing plan advisers to artificially restrict their recommendations to the investment menu offered by their broker-dealer, to investments that benefit the plan adviser’s broker-dealer’s preferred providers.

“Open architecture” refers to an investment platform where a stockbroker can offer a wide variety of investment products, including no-load and index funds. Most of the major broker-dealers do not operate on an open architecture platform. Most broker-dealers usually restrict investment recommendations to the products offered by their “preferred providers,” mutual fund companies and other product vendors who have either paid for or arranged special deals for the privilege of accessing the broker-dealer’s stockbrokers.

The problem with this arrangement and Reg BI’s qualifying language, “reasonably available alternatives offered by the broker-dealer,” is that the investment products offered by preferred providers are often overpriced, consistently underperforming, i.e., cost-inefficient, products, the antithesis of both ERISA’s fiduciary prudence and loyalty requirements, as well as Reg BI’s goals.

Further complicating the situation is that plan sponsors often blindly rely on their plan adviser’s recommendations, even though the courts have consistently ruled that such blind reliance is a breach of a plan sponsor’s fiduciary duties, especially when commissioned salespeople are involved.

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.8

A determination whether a fiduciary’s reliance on an expert advisor is justified is informed by many factors, including the expert’s reputation and experience, the extensiveness and thoroughness of the expert’s investigation, whether the expert’s opinion is supported by relevant material, and whether the expert’s methods and assumptions are appropriate to the decision at hand. One extremely important factor is whether the expert advisor truly offers independent and impartial advice.9

Defendants relied on FPA, however, and FPA served as a broker, not an impartial analyst. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.10

A 3(21) adviser is technically a co-fiduciary with the plan sponsor. However, 3(21) advisers routinely insert fiduciary disclaimer clauses in their advisory contracts in attempt to avoid any fiduciary liability exposure, perhaps knowing the true quality of the advice they are going to provide to a plan.

Addressing the Reg BI/ERISA Fiduciary Duties “Trap”

Perhaps the best advice on how plan sponsors should address the reasonably available alternatives/fiduciary prudence liability gap was offered by Judge Kayatta in the Brotherston decision.

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss incurred as a result.11

The Brotherston decision and the Solicitor General’s amicus brief in connection with Putnam Investment’s application for review by the Supreme Court provide an excellent overview of a plan sponsor’s fiduciary duties. I wrote a post on fiduciary prudence in a post-Brotherston 401(k) world.12

Further support for this position can be found in the studies which have consistently concluded that the overwhelming majority of actively managed funds are not cost-efficient.

- 99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.13

- [I]ncreasing numbers of clients will realize that in toe-to-toe competition versus near-equal competitors, most active managers will not and cannot recover the costs and fees they charge.14

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.15

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.16

One of the key points in Reg BI was the requirement that stockbrokers would be required to factor in the costs associated with any investment product recommendations. The release announcing the adoption of Reg BI supported the importance of cost-efficiency, stating that

A rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest expected net benefit in light of the investor’s investment objective that maximizes expected utility.17

This simply reiterates comments on the importance of cost-efficiency from Section 90 of the Restatement. The Restatement establishes a number of fiduciary standards with regard to a fiduciary’s duty of prudence. Three of the key standards are

- a fiduciary has a duty to be cost-conscientious in investing.18

- a fiduciary has a duty to seek the highest return for a given level of cost and risk or, conversely, the lowest level of cost and risk for a given level of return.19

- that due to higher costs and risks associated with actively managed funds, actively managed funds are imprudent unless it can be objectively estimated that the funds will provide a commensurate return for the additional costs and risks incurred, i.e., are cost-efficient.20

Nevertheless, the fact is that actively managed mutual funds still dominate 401(k) and 403(b), largely because, as the Gregg quote noted, those are the investment products stockbrokers recommend, primarily from their broker-dealer’s preferred provider list.

Fortunately, there are some simple steps that plan sponsors can take to protect themselves and their plan participants. First, do not sign any advisory contract that includes a fiduciary disclaimer clause. These clauses are often subtle and buried within an advisory contract. If a plan sponsor has any questions, they should consult with an experienced ERISA plaintiff’s attorney.

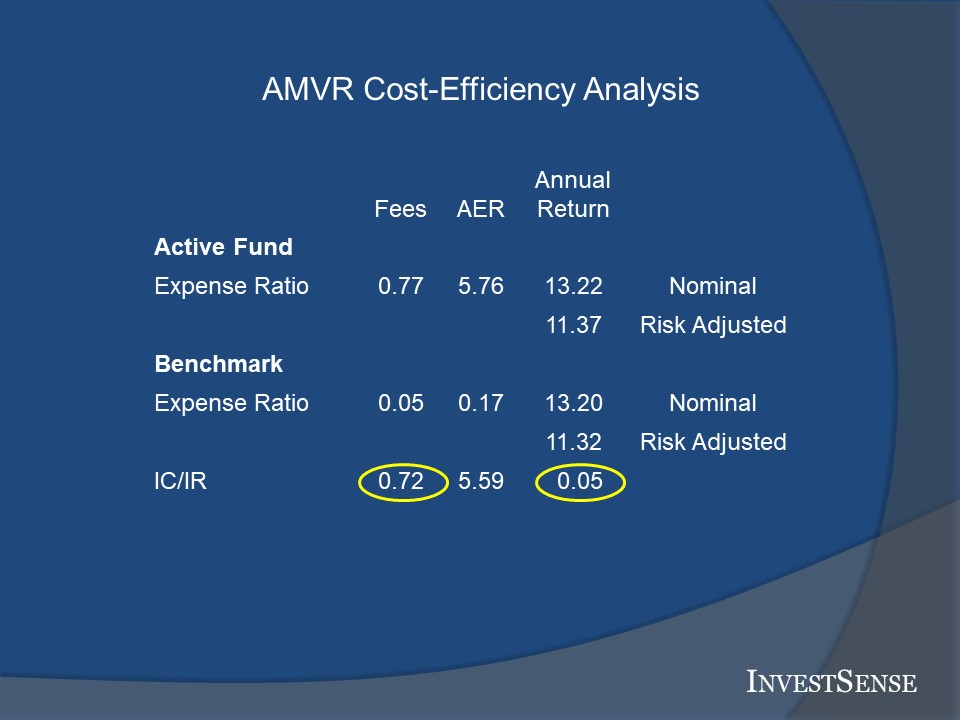

Second, the Active Management Value Ratio (AMVR) metric provides a free and simple tool that plan sponsors can use to detect cost-inefficient investment recommendations. Plan sponsors should assess the cost-efficiency of any recommended investment option using a universal “reasonably available alternatives” menu, not Reg BI’s unduly restricted “reasonably available alternatives” standard.

The AMVR is simple and straightforward, requiring only the ability to compare the data between an actively managed fund and a comparable index fund by simple subtraction. A plan sponsor, or any other investment fiduciary, then just has to answer two simple questions:

- Did the actively managed fund provide a positive incremental return?

- If so, did the actively managed fund’s incremental return exceed the fund’s incremental costs?

If the answer to either question is “no,” then the actively managed fund is cost-inefficient, i.e., imprudent, relative to the comparable index fund and should be avoided.

That has always been my advice to plan sponsors. However, a reader of our “The Prudent Investment Adviser Rules” blog and a member of his plan’s investment committee recently sent me an email asking me whether I thought a plan adviser should provide an AMVR analysis for every recommendation they make. I believe that would be a reasonable request to better protect the plan; but that it is highly unlikely that they would do so using the exact AMVR format, especially using the correlation-adjusted costs. The AMVR quickly exposes cost-inefficient investments.

In his case, the plan adviser actually did provide an AMVR analysis based on the nominal numbers, but substituted some strange analysis in lieu of a correlation-adjusted analysis based on the Active Expense Ratio. The AMVR, as constructed, is the investment industry’s worst nightmare, as it forces a plan adviser to provide greater transparency, which is the financial services’ kryptonite.

Going Forward

As I mentioned at the start of this post, I am on record as saying that (a) ERISA plaintiff’s attorneys should never lose a properly vetted 401(k)/403(b) action, and (b) the amount of 401(k)/403(b) litigation is going to continue to increase. My job as a fiduciary risk management counsel is to alert my clients to such trends and teach them how to minimize their exposure to liability and litigation.

A key to accomplishing these goals is to make sure that plan sponsors truly understand what their fiduciary duties do, and do not, require. Fortunately, compliance with ERISA is just not that complicated if a proper system of policies and procedures is created and properly maintained.

Not much has been written about the fiduciary liability trap created by the disconnect between Reg BI’s “reasonably available alternatives offered by the broker-dealer” language and ERISA’s fiduciary prudence and loyalty requirements. The seriousness of this gap in compliance language and its potential consequences cannot be overstated, especially with the Department of Labor reportedly considering implementing its own fiduciary guidelines, including incorporating the provisions of Reg BI.

Far too often regulators have “dropped the ball” when it comes to protecting investors and employees against the very abuses that the securities regulations and ERISA were created to prevent. While many may have overlooked the potential implications of Reg BI’s cleverly drafted “reasonably available alternatives” language, it is imperative that plan sponsors recognize the issues discussed herein in order to protect both themselves and their plan participants.

Caveat fiduciarius

Notes

1. https://www.prnewswire.com/news-releases/jp-morgan-defined-contribution-survey-shows-plan-sponsors-aiming-to-strengthen-plans-finds-fiduciary-misperceptions-remain-300495423.html.

2. 29 CFR §2550.404c-1 – ERISA Section 404(c) Plans

3. Hughes v. Northwestern University,

4. SEC Release 34-86031, Regulation Best Interest: The Broker-Dealer Standard of Conduct (Reg BI), 278

5. Reg BI, 279.

6. Reg BI, 279.

7. Reg BI, 285.

8. Liss v. Smith, 991 F. Supp. 278, 291 (S.D.N.Y. 1988).

9. Gregg v. Transportation Workers of America Int’l, 343 F.3d 833, 841-42. (Gregg)

10. Gregg, 841-42.

11. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Cir. 2018)

12. “Plan Sponsor Special Report: 401(k) Fiduciary Liability Risk Management in a Post-Brotherston World” https://bit.ly/3Q3MEkK

13. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

14. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

15. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

16. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

17. Reg BI, 378.

18. RESTATEMENT (THIRD) TRUSTS, (American Law Institute),Section 90, cmt b.

19. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt f.

20. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt h(2).

You must be logged in to post a comment.