By James W. Watkins, J.D., CFP Board Emeritus™, AWMA®

When I created the Active Management Value Ratio (AMVR) metric, the goal was to create a simple tool that would allow investors, investment fiduciaries, and attorneys to quickly and easily evaluate the cost-efficiency and, thus, the fiduciary prudence of an actively managed mutual fund. The metric itself is based on a combination of research and concepts of investment icons such as Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel.

T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.7

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!2

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.3

These three opinions formed the basis for the initial iteration of the AMVR. Further research led to the current version of the AMVR – AMVR 3.0 – which incorporates the research of Ross Miller and his Active Expense Ratio (AER) metric. Miller explains the importance of the AER as follows:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.4

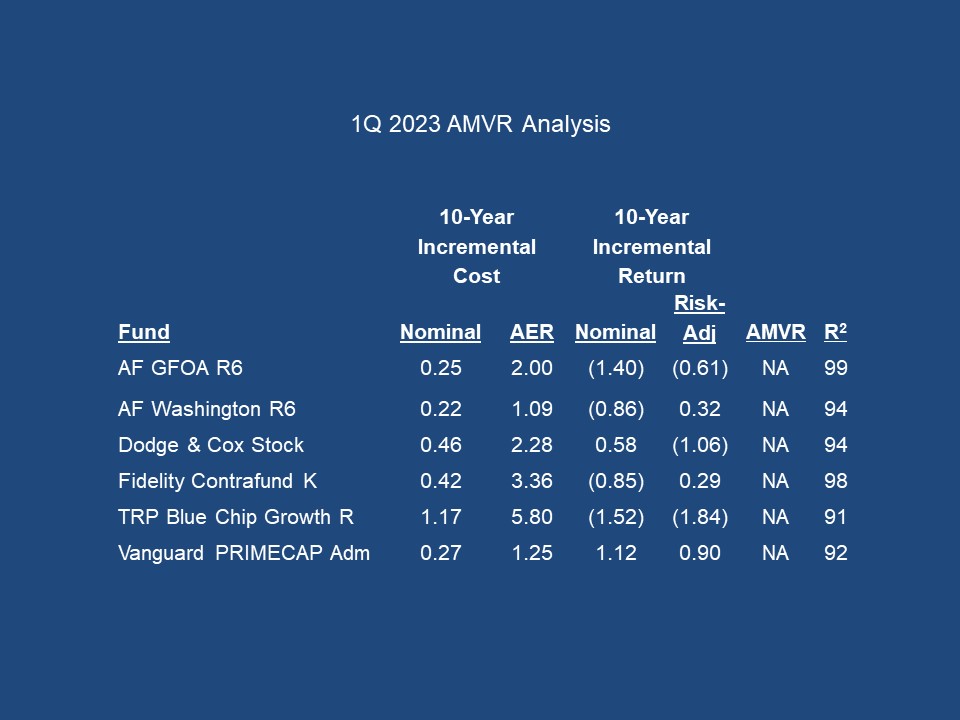

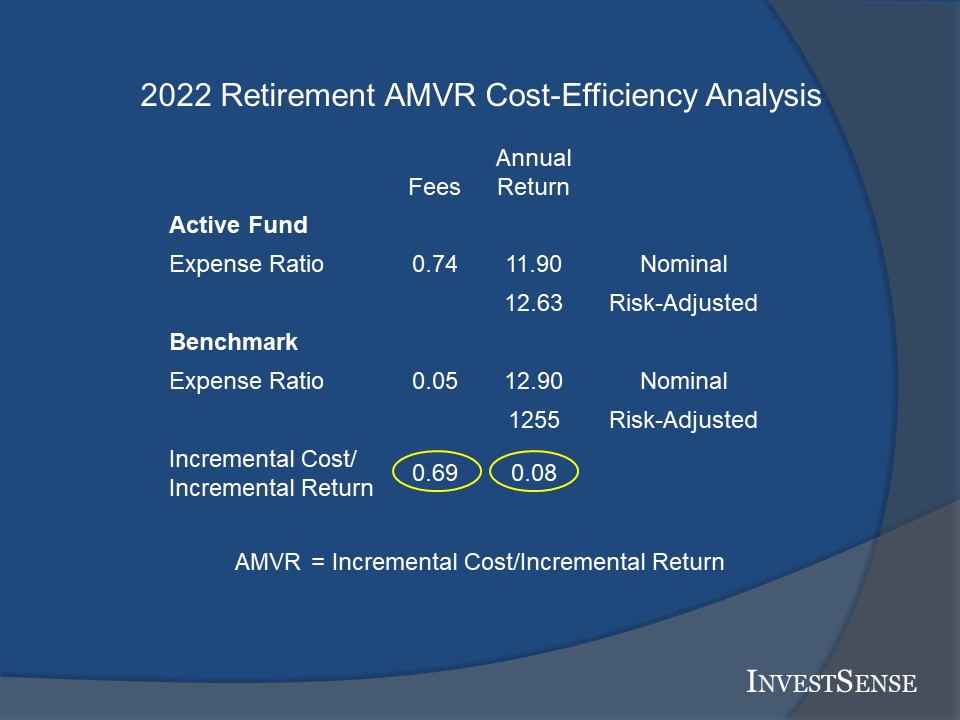

An example of an AMVR analysis of the retirement share of a well-known actively managed mutual fund is shown below.

An AMVR analysis can be calculated for any time period. In this case, a five-year analysis comparing an actively managed fund and a comparable index fund shows that the actively managed fund is cost-inefficient, as it fails to provide a positive incremental return (1.33), so naturally the incremental costs exceed the incremental returns. A cost-inefficient fund is an imprudent investment under the Restatement (Third) of Trusts.

The example show above is far from an anomaly. Research has consistently shown that the overwhelming majority of actively managed funds are cost-inefficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.5

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.6

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.7

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.8

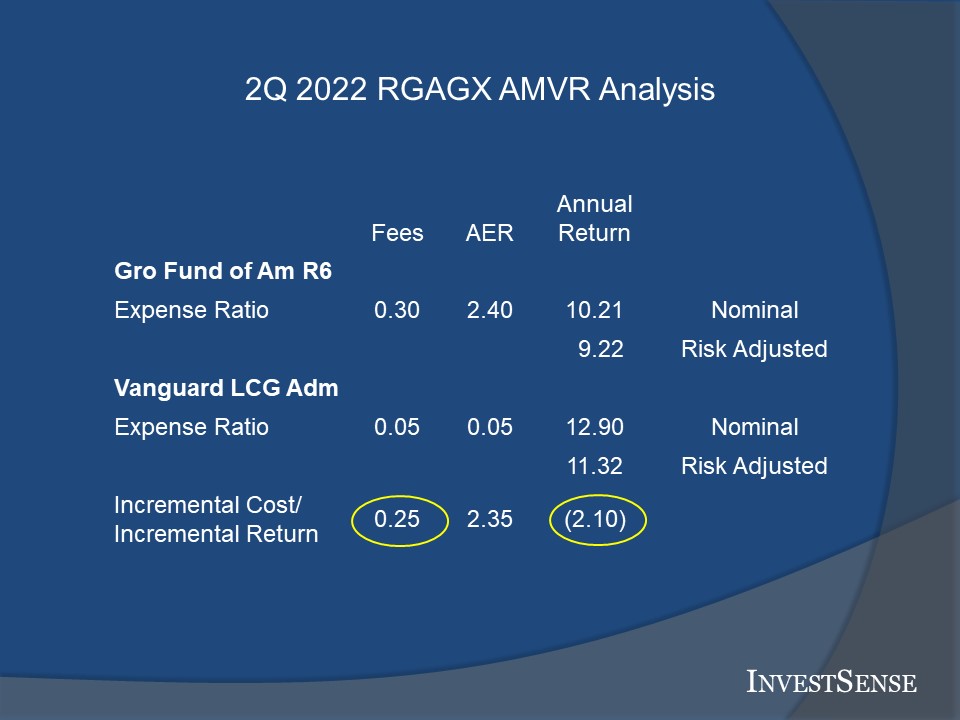

The cost-inefficiency in the example is even more serious if measured using the AER, In this case, the high incremental costs of the funds combined with the fund’s high correlation of return to the benchmark (98) results in an AER of 5.67.

In Tibble,9 SCOTUS recognized the Restatement (Third) of Trusts (Restatement) as a legitimate resource in resolving fiduciary disputes, including questions regarding fiduciary duties under ERISA. The Restatement clearly recognizes the importance of cost-efficiency, stating that fiduciaries should carefully compare the costs associated with a fund, especially when considering funds with similar objectives and performance. The Restatement advises plan fiduciaries that in deciding between funds that are similar except for their costs, the fiduciary should only choose an active fund with higher costs and/or risks if

the course of action in question can reasonably be expected to compensate for its additional costs and risk,…10

Studies by both the DOL and the GAO have found that each additional one percent in fees/costs reduces an investor’s end-return by 17 percent over a 20-yeat period.11 In our example, that would result in a projected loss of 45 percent using the nominal incremental cost/underperformance numbers (2.63), and 94 percent using the AER incremental cost/underperformance numbers (5.52).

The Active Expense Ratio – Fiduciary Risk Management’s “Little Secret”

Whenever I show a prospective fiduciary risk management client a sample AMVR analysis, one of the first questions is about the AER column and why is it important. Miller’s quote obviously addresses the significance of the AER.

In my last post, I referenced a similar quote in a 2007 speech from then SEC General Counsel, Brian G. Cartwright. Cartwright asked his audience to think of an investment in an actively managed mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s real holdings.

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund — no overweightings or underweightings — then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?12

The AER provides investors, investment fiduciaries, and ERISA attorneys with just the tool to provide such information. The AER for an actively managed fund can be calculated with just the actively managed fund’s r-squared information and the fund’s incremental cost data.

In the AMVR analysis above, the actively managed fund had an r-squared, or correlation of returns, number of 98. Miller then provides an equation for calculating the percentage of active management provided by the actively managed fund relative to a comparable index fund. In this case, the r-squared number of 98 equates to an implied active weight of 12.50 percent.

Over the last decade or so, it has not been uncommon for U.S. domestic equity funds to have r-squared numbers of 95 and above, resulting in relatively low active weight numbers, typically less that 25 percent. The list below shows the active weights associated with r-squared number of 95 and above.

99 > .0913

98 > .1250

97 > .1537

96 > .1695

95 > .1866

The AER is then calculated by dividing the actively managed fund’s incremental costs by the actively managed fund’s active weight number. Here, the actively managed fund’s incremental costs (0.42) divided by the fund’s active weight (.125) results in an AER score of 3.36, or seven times the actively managed fund’s publicly reported expense ratio.

Another way of combining the AMVR and the AER is to use the data to determine how you would have rationalized the imprudence of a choice of the actively managed fund in a 401(k)/403(b) action. ERISA plaintiff attorneys are increasingly using the AER in bracketing estimated damages. The argument would be given the actively managed fund significantly underperformance the comparable index fund, the index fund would have not only have provided plan participants with a significantly better return, but the incremental return would not have been incurred, thereby increasing the plan participants’ returns even more. As John Bogle was fond of saying, “Investors keep what they don’t pay for.”

Going Forward

As some courts continue to try to justify the use of cost-inefficient active funds in 401(k) plans, an often-unaddressed issue involves the fundamental issues of just how much active management do “actively” managed funds actually provide and at what cost to investors

The high correlation of returns that is being seen between U.S. domestic equity funds and comparable index funds naturally raises the question of “closet indexing.” Closet index funds tout the alleged benefits of active management and try to justify higher expenses ratios and costs on such alleged benefits.

The financial implications of closet indexing for investors are well-known.

[A] large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by paying fees for active management that they do not receive or receive only partially….13

The AER makes plan sponsors and other investment fiduciaries address the uncomfortable question of closet indexing and the resultant cost-inefficiency and legal imprudence of such funds. The AER recognizes that a high correlation of returns between a “actively managed” fund and a comparable index fund suggests that active management is contributing little, if anything, in terms of performance and return for an investor. The AER recognizes that the combination of a high r-squared number and high incremental costs increases a fund’s implicit costs and overall cost-inefficiency.

The AER should make courts and plan sponsors realize that the implicit costs of funds that provide a low level of active management, funds with a low active weight/active contribution, are naturally going to be higher than a fund that truly provides active management. The AER raises the fundamental question of how much “active management” must a fund provide to qualify as an actively managed fund and avoid potential allegations of fraud and misrepresentation under federal securities laws.

The Department of Labor (DOL) recently filed an amicus brief in a pending 401(k) action. The significance of the amicus brief is that the DOL sided with both several other federal circuit courts of appeal and the common law in taking the position that plan sponsors, not plan participants, have the burden of proof with regard to the issue of causation in 401(k)/403(b) litigation. This issue is currently involved in two pending federal 401(k) litigations.

Now that the DOL has taken a position that is consistent with both a previous amicus brief filed with SCOTUS by the Solicitor General in the Brotherston14 case and a significant portion of the federal courts of appeal, I believe that SCOTUS will ultimately agree the burden of proof on the issues of causation shifts to the plan sponsor once the plan participants properly plead their case.

With ERISA plaintiff attorneys already incorporating the AER in calculating damages, plan sponsors need to ask themselves whether they could carry that burden of proof. I believe that the studies referenced herein, as well as the AMVR, raise genuine doubts about the ability of plan sponsor to meet that challenge. That is many of my fiduciary risk management clients are already proactively using both the AMVR and the AER to estimate and reduce the extent of any potential fiduciary liability exposure.

Notes

1. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm.

2. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online athttps://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c

3. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460.

4. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926.

5. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

6. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

7. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

8. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

9. Tibble v. Edison International, 135 S. Ct 1823 (2015).

10. Restatement (Third) Trusts (American Law Institute), cmt. h(2). All rights reserved. (Restatement)

11. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (“DOL Study”); “Private Pensions: Changes Needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (“GAO Study”).

12. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G. Cartwright). http://www.sec.gov/news/speech/2007/spch102407bgc.htm

13. Martijn Cremers and Quinn Curtis, Do Mutual Fund Investors Get What They Pay For?:The Legal Consequences of Closet Index Funds, https://papers.ssrn.com/sol/papers.cfm?abstract_id=2695133 (Cremers), 5, 42.

14. Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (2018). (Brotherston)

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.