by James W. Watkins, III, J.D., CFP Board EmeritusTM AWMA®

The Seventh Circuit’s recent decision1 in Hughes v. Northwestern University simply reinforces my opinion that there is definitely a trend going on in 401(k) and 403(b) litigation, a trend reinforcing both the spirit and the letter of the law with regard both ERISA and the Restatement of Trusts. As I have stated before, I believe the next 12-18 months is going to see a significant change in the 401(k) and 403(b) landscape, once that restores fundamental fairness in litigation involving such areas.

As a result, the prudent plan sponsor will perform an independent and objective analysis of their plan to determine the extent of any potential fiduciary liability exposure. I believe that most plan sponsors truly want to provide their employees with a meaningful retirement plan. Unfortunately, the evidence suggests that most plan sponsors fail to do so due to a lack of understanding as to what their fiduciary duties actually require and how to properly perform such duties. Fortunately, compliance with ERISA is relatively simple to accomplish and maintain.

When I review an ERISA decision, the first thing I ask is whether the decision is sustainable on appeal, whether it is consistent with both ERISA and the Restatement of Trusts. If not, then the decision arguably does nothing more than create a false sense of security for a plan sponsor. I think we have seen too many of such decisions.

However, I think the Seventh Circuit’s recent reconsideration of its earlier Hughes decision is a continuation of a trend which seems to be trying to establish a sense of fundamental fairness in 401(k)/403(b) litigation, most notably with regard to allowing plaintiffs to have some degree of discovery. Given ERISA’s focus on the fiduciary process used by a plan sponsor and the obvious fact that only the plan sponsor can know what that process was, any attempt by a court to require the plan participants to prove the flaws in such process without at least “controlled” discovery is inequitable.

The Sixth Circuit recognized that fact in its TriHealth decision, as Chief Judge Sutton suggested that too many 401(k) cases were being prematurely dismissed due to plaintiffs not being a chance at reasonable discovery.

But at the pleading stage, it is too early to make these judgment calls. ‘In the absence of further development of the facts, we have no basis for crediting one set of reasonable inferences over the other. Because either assessment is plausible, the Rules of Civil Procedure entitle [the three employees] to pursue [their imprudence] claim (at least with respect to this theory) to the next stage….’ 2

This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth ‘investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares’ because ‘the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….’ Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.3

Common sense supports this argument. If in fact the plan sponsors conducted the legally required objective and thorough independent investigation and evaluation of the funds selected for a plan, discovery could easily be limited to producing any and all materials used and relied on by the plan sponsor. The time and costs involved in such controlled discovery should be minimal. Then again, as the Sixth Circuit points out, such controlled discovery would also expose plan sponsors who did not comply with ERISA’s fiduciary requirements.

The Seventh Circuit liberally cited from the Sixth Circuit’s TriHealth decision, pointing out that the plaintiff’s obligation to sufficiently plead its case is a separate and distinct obligation from proving causation. The Seventh Circuit’s consistent theme throughout the Hughes decision was on the concept of fundamental fairness to the parties and a balanced consideration of the facts.

“[P]laintiffs must have alleged enough facts to show that a prudent fiduciary would have taken steps to reduce fees and remove some imprudent investments.4

ERISA requires a fiduciary to assess whether a given fund is prudent in light of other investment options in a plan, comparable funds, and the expenses charged among other factors.5

Where alternative inferences are in equipoise-that is where they are all reasonable based on the facts, the plaintiff is to prevail in a motion to dismiss. (Citing TriHealth at 450), ‘Equally reasonable inferences…could exonerate[the plan sponsor]…[but] at the pleading stage, it is too early to make these judgment calls. This is because, at the pleading stage, we must accept all well-pleaded facts as true and draw reasonable inferences in the plaintiff’s favor.’6

A court’s role in evaluating pleadings is to decide whether the plaintiff’s allegations are plausible-not which side’s version is more probable. This, on a motion o dismiss, courts must give due regard to alternative explanations for an ERISA fiduciary’s conduct, but htye need not be overcome conclusively by the plaintiff.7

Another example of this “fundamental fairness” trend was evident in the Seventh Circuit’s Oshkosh decision, where the Court discredited the plan’s arguments that the expense ratios for the funds in the plan should be adjusted on a one-to-one basis to account for revenue sharing.

The problem is that the Form 5500 on which Albert relies does not require plans to disclose precisely where money from revenue sharing goes. Some revenue sharing proceeds go to the recordkeeper in the form of profits, and some go back to the investor, but there is not necessarily a one-to-one correlation such that revenue sharing always redounds to investors’ benefit. Albert’s ‘net investment expense to retirement plans theory’ assumes that there is such a correlation; if that assumption is wrong, then simply subtracting revenue sharing from the investment-management expense ratio does not equal the net fee that plan participants actually pay for investment management.8

The Hughes Decision and Cost-Inefficiency

As mentioned earlier, the Seventh Circuit specifically included cost as one factor that plan sponsors must consider in selecting investment options for their plan. The Court addressed this even further. stating that

[c]ost-conscious management is fundamental to prudence in the investment function, [and should be applied] not only in making investments but also in monitoring and reviewing investments.9 (citing RESTATEMENT (THIRD) OF TRUSTS Section 90, cmt. B, and Section 88, cmt. A)

Wasting beneficiaries’ money is imprudent.10 (citing UNIF. PRUDENT INVESTOR ACT SECTION 7, cmt. (UNIF. L. COMM”N 1995)

The Active Management Value Ratio (AMVR) could significantly help the parties and the courts properly evaluate the various claims and theories put forth in 401(k) and 403(b) litigation.

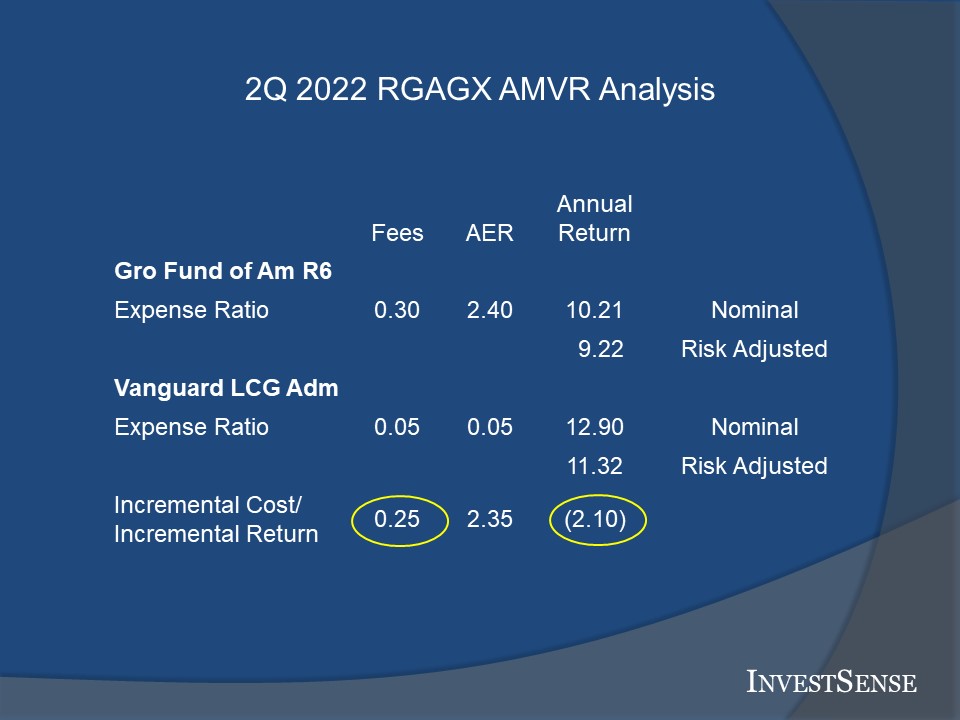

Reports and publications consistently rank the American Funds Growth Fund of America Fund (RGAGX) as one of the most common investment options within 401(k) and 403(b) plans. The following AMVR slide could help evaluate the fiduciary prudence of the fund.

Two things that immediately stand out on the AMVR slide:

1. RGAGX fails to provide a positive incremental return relative to the benchmark, the Vanguard Large Cap Growth Index Fund (VIGAX).

2. RGAGX has nominal incremental costs relative to VIGAX, without any commensurate return for such costs.

The DOL and the GAO have both stated that each additional 1 percent in fees/costs reduces an investor’s end-return by 17 percent over a twenty-year period.11 If we treat RGAGX’s relative underperformance (201 basis points) as an opportunity cost and combine such cost with RGAGX’s relative incremental cost (25 basis points), the projected reduction in end-return would be over 38 percent. I am not sure how a plan sponsor could successfully argue that causing an investor to suffer such a loss was a prudent investment choice when VIGAX was an available investment option.

Going Forward

I have previously stated that I believe that the next 12-18 months are going to be a pivotal period for the 401(k)/403(b) industry, for both plan sponsors and plan advisers. The combination of the currently emerging “fundamental fairness” trend within the courts and the simple and straightforward “Humble Arithemetic” evidence of the AMVR could prove difficult for plan sponsors to overcome if they wish to avoid unnecessary fiduciary liability exposure.

Those that follow me know that I believe that the final piece of the 401(k)/403(b) fiduciary prudence puzzle will be the Matney v. Barrick Gold of North America12 case (Matney). Matney is currently pending in the 10th Circuit Court of Appeals. Matney provides the legal system with an opportunity to resolve two ongoing ERISA issues, (1) the validity of the “apples and oranges” argument regarding comparison of actively managed mutual funds and index mutual funds, and (2) the question of who carries the burden of proof on the issue of causation.

Both of these issues were presented to SCOTUS in the Brotherston appeal in 2018. SCOTUS denied Purnam Investments’ petition for certiorari at that time. Matney gives SCOTUS another opportunity to resolve the two issues and end a split on the issues in the federal courts, guaranteeing employees an equitable and uniform standard of legal review in the courts.

Notes

1. Hughes v. Northwestern University, No. 18-2569, March 23, 2023 (7th Cir. 2023) Hughes)

2. Forman v. TriHealth, Inc., 40 F.4th 443, 450 (6th Cir. 2022)

3. TriHealth, Ibid.

4. Hughes, 17

5. Hughes, 11

6. Hughes, 19

7. Hughes, 20

8. Albert v. Oshkosh Corp., 47 F.4th 570, 581 (2022)

9. Hughes, 14

10. Hughes, 15

11. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Feess abd Expenses,” (“DOL Study”). http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study”).

12. Matney v. Barrick Gold of North America, No. 4045 (10th Cir.)

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.