By James W. Watkins, J.D., CFP Board Emeritus™, AWMA®

The words that I remember

From my childhood still are true

That there’s none so blind

As those who will not see

– Justin Hayward/Moody Blues – “I Know You’re Out There Somewhere”

I know my reference to the Moody Blues will draw a chuckle from my friend, Robin Powell, leader of the evidence-based investing movement and owner of “The Evidence-Based Investor” blog (evidenceinvestors.com). We often joke about the fact that we may among the few that are still Moody Blues fans. But those lines still resonate with me because of the truth they tell, especially within the world of financial services and pensions plans.

The ongoing refusal of some to courts acknowledge SCOTUS’ recognition of the Restatement of Trusts as a legitimate resource in resolving disputes involving fiduciary issues is puzzling. More troubling is the fact that such refusal has resulted in the inequitable situation of the rights and guarantees promised by ERISA being decided on where one resides.

Fortunately, it appears that there may be hope on the horizon. Hopefully SCOTUS will have an opportunity to require that the legal system adhere to one consistent and equitable set of standards in deciding 401(k) and 403(b) litigation. That hope is the Matney v. Briggs Gold case1 currently pending in the Tenth Circuit of Appeals, a case that involves the two key issues that were involved in the Brotherston case2, namely the legitimacy of index funds as comparators in fiduciary prudence evaluations and the question of which party has the burden of proof regarding causation in 401(k)/403(b) actions.

The DOL recently weighed in on the burden of proof issue, stating that once the plan participants properly plead a breach of fiduciary duties, the plan sponsor should then have the burden of proof on the issue of causation, the burden of disproving the participants/ allegations, since they alone know what process they employed in making their decisions. The DOL cited the common law of trusts as a key factor in its position, just as the First Circuit Court of Appeals and the Solicitor General had done in Brotherston.

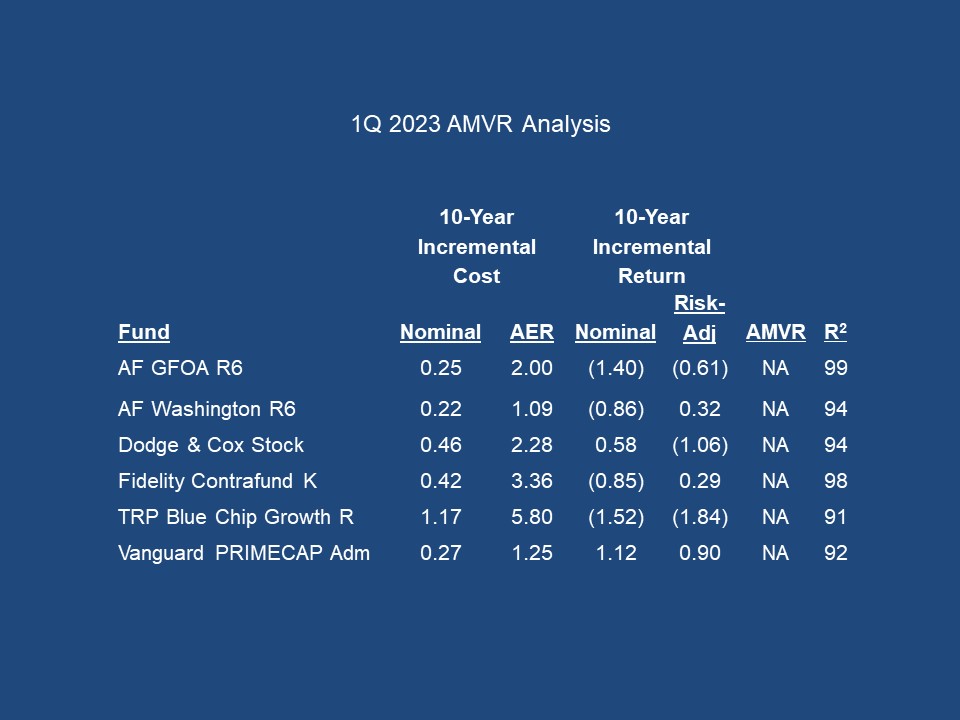

Once again, this past quarter’s Active Management Value Ratio (AMVR) “cheat sheets” clearly demonstrate why plan sponsors should closely monitor the progress of the Matney case. If ERISA plaintiff attorneys and the courts focus on the more meaningful factor of cost-efficiency rather than the antiquated and meaningless active/passive argument, I believe that plan sponsors will have an extremely difficult time carrying the burden of proof in proving that their decisions did not cause the resulting losses to the plan participants.

Once again, an actively managed fund’s AMVR score is calculated by dividing the fund’s incremental correlation-adjusted costs by its incremental risk-adjusted return. The costs and return calculations are based on comparisons to a comparable index fund.

The AMVR slides shown above also show how the prudence/imprudence of an actively managed fund can quickly be determined by just answering two questions:

(1) Does the actively managed mutual fund provide a positive incremental return relative to the benchmark being used?

(2) If so, does the actively managed fund’s positive incremental return exceed the fund’s incremental costs relative to the benchmark?

If the answer to either of these questions is “no,” the actively managed fund is both cost-inefficient and unsuitable/imprudent according to the Restatement’s prudence standards, and the actively manged fund should be avoided. The goal for an actively managed fund is an AMVR number greater than “0” (indicating that the fund did provide a positive incremental return), but equal to or less than “1” (indicating that the fund’s incremental costs did not exceed the fund’s incremental return).

Is Active Management Much Ado About Nothing?

Some courts have consistently tried to justify the choice of various actively managed funds which fail the AMVR’s fiduciary prudence test. Said courts have tried to justify underperformance based on factors such as investment strategies, goals and preserving choices for plan participants. My response is that if the purpose and goals of ERISA are to be honored and furthered, then the comparative performance of a fund and the comparative benefits provided to the plan participants are the true tests of a fund’s prudence. As for the “choices” argument, common sense says that a cost-inefficient mutual fund is not, and never has been a legally viable “choice.”

In short, the actively managed fund had its chance to test its approach against a comparable index fund’s approach. More often than not, the actively managed fund loses. While a number of people took exception to Judge Kayatta’s suggestion in Brotherston that plan sponsors should choose index funds if they wish to avoid unnecessary liability exposure, he was simply telling the truth. Judge Kayatta’s position has been consistently supported by studies on the cost-efficiency of actively managed funds, studies with findings such as

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.3

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.4[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.5

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.6

Judge Kayatta’s position is further supported by John Langbein, who served as the Reporter on the committee that re-wrote the Restatement (Second) of Trusts over fifty years ago. Shortly after the release of the revised Restatement, Langbein wrote a law review article on the new Restatement. At the end of the article, he made a bold prediction:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.7

While all of these comments are true, they fail to address an even more fundamental question: How much active management do actively managed funds actually provide?

In a 2007 speech at the University of Pennsylvania Law School, Brian G. Cartwright, then general counsel of the SEC, asked the same question. Cartwright asked his audience to think of an investment in a mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s real holdings. Cartwright told the students,

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund — no overweightings or underweightings — then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?8

I would suggest that the AMVR provides such information. I would also suggest that combining the AMVR with Ross Miller’s Active Expense Ratio (AER) provides an even more meaningful evaluation of the prudence/imprudence of an actively managed fund.

The AER determines the Active Weight (AW) within an actively managed fund, then uses the fund’s AW to recalculate the implicit expense ratio that an investor in the fund is paying. Miller explained the importance of the AER, stating that

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.9

Using just a fund’s R-squared number and its incremental costs, Miller found that in terms of Active Weight, actively managed funds often provide very little active management, As a result, investors often pay an implicit expense ratio that is 300-400 percent, or even more, higher than the fund’s publicly stated expense ratio.

The slides above clearly show how the combination of a higher incremental cost and a high R-squared number result in a significantly higher AER. Under Miller’s AER, an R-squared of 98 equates to active weight of just 12.50 percent. I would suggest that referring to such a fund as “actively managed” might be questioned. One could also suggest that a refusal or failure to recognize and acknowledge such an inequitable situation constitutes “willful blindness” by a plan sponsor and an obvious breach of their fiduciary duties.

People often ask me why InvestSense uses the AER and correlation-adjusted costs in calculating a fund’s AMVR score. Simply because I believe that the AER provides a more accurate perspective of the costs an investor incurs. And as both the DOL and the GAO have stated, each additional 1 percent in fees/costs reduces an investor’s end-return by approximately 17 percent over a 20-year period10

Going Forward

In earlier posts, I had stated that I would announce a new metric, the “Fiduciary Prudence Score.” I shelved that metric, as some of my mentors suggested that it might confuse people and distract from the strength of the AMVR. Since I believe that the next 12-18 months are going to see a significant shift in the 401(k)/403(b) litigation arena, I do not want to do anything that would possibly detract from the simplicity and value of the AMVR.

If I am correct in my prediction for the next 12-18 months, plan sponsors should consider a fiduciary audit of their plan, an audit that uses both the AMVR and the AER as key fiduciary factors. When I meet with a prospective client, I suggest to them that they ask their current plan adviser to prepare an AMVR slide using exactly the same layout and criteria shown on the slides shown in this post. In most cases, the adviser has either totally refused to do so, or has made “improvements” to the AMVR calculation process. Once SCOTUS’ hears Matney, or a similar case, and shifts the burden of proof on causation to plans, plan sponsors will belatedly realize the true value of cost-benefit anaysis, such as the AMVR, as a fiduciary risk management tool.

Notes

1. Matney v. Barrick Gold of North America, No. 4045 (10th Cir.)

2. Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (2018) (Brotherston)

3. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

4. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

5. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

6. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

7. John H. Langbein and Richard A. Posner, Measuring the True Cost of Active Management by Mutual Funds, Journal of Investment Management, Vol 5, No. 1, First Quarter 2007 http://digitalcommons.law.yale.edu/fss_papers/498

8. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G. Cartwright). http://www.sec.gov/news/speech/2007/spch102407bgc.htm

9. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926

10. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Feess abd Expenses,” (“DOL Study”). http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes Needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study”).

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.