I am often asked what I see as the current trends in 401(k) and what fiduciary risk management steps plan sponsors should consider in order to reduce any potential fiduciary risk exposure. With the end of the year approaching, now seems like an appropriate to post my opinions and forecasts

Five issues in particular have often been relied on plans and some courts to dismiss 401(k) cases:

1. The requirement that plaintiff properly plead plausibility.

2. The questions as to which party has the burden of proof regarding causation of the alleged damages.

3. The “menu of options” defense.

4. The “apples and oranges” defense.

5. Dismissal of cases based on presumed cost of discovery.

Pleading Plausibility

There is no issue here. Under the Federal Rules of Civil Procedure, a plaintiff must plead their case in such a way as to establish the plausibility of the wrongdoing and the resultant damages.

The Solicitor General’s office did an excellent job of addressing the plausibility pleading requirement in the amicus brief that it filed with SCOTUS in connect with the Hughes v. Northwestern University case.

Petitioners state a plausible claim for relief in part of Count V by alleging that respondents selected investment options for the Plans “with far higher costs than were and are available for the Plans based on their size.”1

That is not to say that an ERISA plaintiff could state a claim for relief by alleging merely that alternative investment funds with lower management fees than those included in a plan were available in the marketplace.2

Petitioners did not merely present a conclusory assertion that the Plans’ recordkeeping fees were too high; they substantiated their claim with specific factual allegations about 15 market conditions, prevailing practices, and strategies used by fiduciaries of comparable Section 403(b) plans.3

This is a message that runs consistently through 401(k) litigation, the need to support allegations with supporting factual evidence. At the same time, as both the Solicitor General and several SCOTUS justices pointed out in oral arguments in Hughes v. Northwestern University4, at the pleading stage, the level of proof need not be at the same level as needed at the proof of causation stage.

Under the law, at the pleading stage, a court is required to accept all allegations as true. The general rule of pleading under the federal rules is simply that the plaintiff provide enough information so that the defendant understand the nature of the plaintiff’s claims.

Burden of Proving Causation

The party charged with the burden of proof on the issues involved in the case has to meet a higher level of providing specific information as to the alleged fiduciary violations and the damages resulting from such violations. The party facing the burden of proof has a challenging responsibility.

The general rule is that the plaintiff must prove its case. However, in Brotherston v. Putnam Investments, LLC5 (Brotherston),the First Circuit pointed out that under trust law, that burden is typically shifted due to the involvement of fiduciary duties and the fact that the necessary information is solely within the trustee. The Solicitor General subsequently supported that position in an amicus brief to SCOTUS.

There is currently a split within the federal courts as to whom carries the burden of proof in 401(k) litigation. As a result, there are employees that are being inequitably denied the rights and protections guaranteed to them under ERISA.

ERISA does expressly resolve the issue. In the Tibble v. Edison International6 decision, SCOTUS stated that the courts often look to the Restatement Third of Trusts (Restatement) to resolve fiduciary issues. The Solicitor General’s amicus brief in Hughes noted several relevant provisions of the Restatement:

The judgment and diligence required of a fiduciary in deciding to offer any particular investment fund must include consideration of costs, among other factors, because a trustee must “incur only costs that are reasonable in amount and appropriate to the investment responsibilities of the trusteeship.”7 (citing Restatement § 90(c)(3))

[C]ost-conscious management is fundamental to prudence in the investment function.”8 (citing Restatement § 90 cmt. b(1))

Trustees, like other prudent investors, prefer (and, as fiduciaries, ordinarily have a duty to seek) the lowest level of risk and cost for a particular level of expected return.”9 (citing Restatement § 90 cmt. f(1)).

For mutual funds specifically, trustees should pay “special attention” to “sales charges, compensation, and other costs” and should “make careful overall cost comparisons, particularly among similar products of a specific type being considered for a trust portfolio.”10 (citing Restatement § 90 cmt. m)

Other federal courts adhere to the general rule and seemingly disregard the Restatement’s positions. Placing the burden of proof on the plan participants becomes even more inequitable when some courts refuse to recognize the fact that the pleading stage and the proof of causation are two separate and distinct stages. Furthermore, combining the pleading and proof stages denies plaintiffs an opportunity for discovery to learn how, or even whether, the plan conducted its legally required independent investigation and evaluation of the plan’s investment options.

Reading the First Circuit’s Brotherston decision and the Solicitor General’s amicus brief together, it seems likely that SCOTUS will either hold that the burden of proof on causation will be shifted to the plan in 401(k)/403(b) litigation, or that the pleading and proof of causation stages will be clearly separated to ensure that the plan participants will have an opportunity for discovery going forward. The question is clearly ripe, in fact well overdue, to ensure an equitable decision in ERISA litigation.

“Menu of Options” Question

This is no longer an issue, as SCOTUS ruled in Hughes that such provisions violate ERISA’s clear requirement that each investment option within a plan must be separately prudent under applicable fiduciary laws.

“Apples and Oranges” Question

The First Circuit did an excellent legal analysis on this issue of whether actively managed funds can be compared to comparable index funds in assessing both a plan sponsor’s prudence in selecting investment options for a plan and the alleged damages for any fiduciary breaches.

Finally, the Restatement specifically identifies as an appropriate comparator for loss calculation purposes “return rates of one or more. . . suitable index mutual funds or market indexes (with such adjustments as may be appropriate).”11 (citing Restatement § 100 cmt. b(1)

a breaching fiduciary shall be liable to the plan for ‘any losses to the plan resulting from each such breach.’ Certainly, this text is broad enough to accommodate the total return principle recognized in the Restatement. Behind the text, too, stands Congress’s clear intent ‘to provide the courts with broad remedies for redressing the interests of participants and beneficiaries when they have been adversely affected by breaches of fiduciary duty….’ And as the Supreme Court has instructed, when we confront a lack of explicit direction in the text of ERISA, we often find answers in the common law of trusts.12 (cites omitted

More importantly, the Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected ‘Congress'[s] desire to offer employees enhanced protection for their benefits…. In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection than they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.’3

To further emphasize the legitimacy of index funds as comparators in 401(k) actions, Judge Keyatta added the following observation:

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry ‘wolf.’14

Just like the burden of proof issue, the “apples and oranges” issue is ripe for discrediting, as it has absolutely no merit either factually or legally. As I have previously posted, the lack of the factual merit in the “apples and oranges” argument can be shown by the ERISA plaintiff’s bar shifting the legal paradigm from one that focuses on the antiquated active/passive argument to one that focuses on the proven cost-inefficiency between actively managed and index funds.

The research on the cost-efficiency of actively managed mutual funds suggest that plan sponsors face a daunting challenge in trying to justify the inclusion of actively managed mutual funds in a 401(k) plan:

- 99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.15

- Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.16

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.17

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.18

The fact that most U.S. domestic-equity based actively managed mutual funds have an R-squared rating of 90 and above, many with 95 and above, relative to comparable index funds further weakens any argument that index funds are not meaningful comparators in 401(k) litigation. What some courts seemingly want to ignore is the inconvenient truth of the relative cost-inefficiency of actively managed funds.

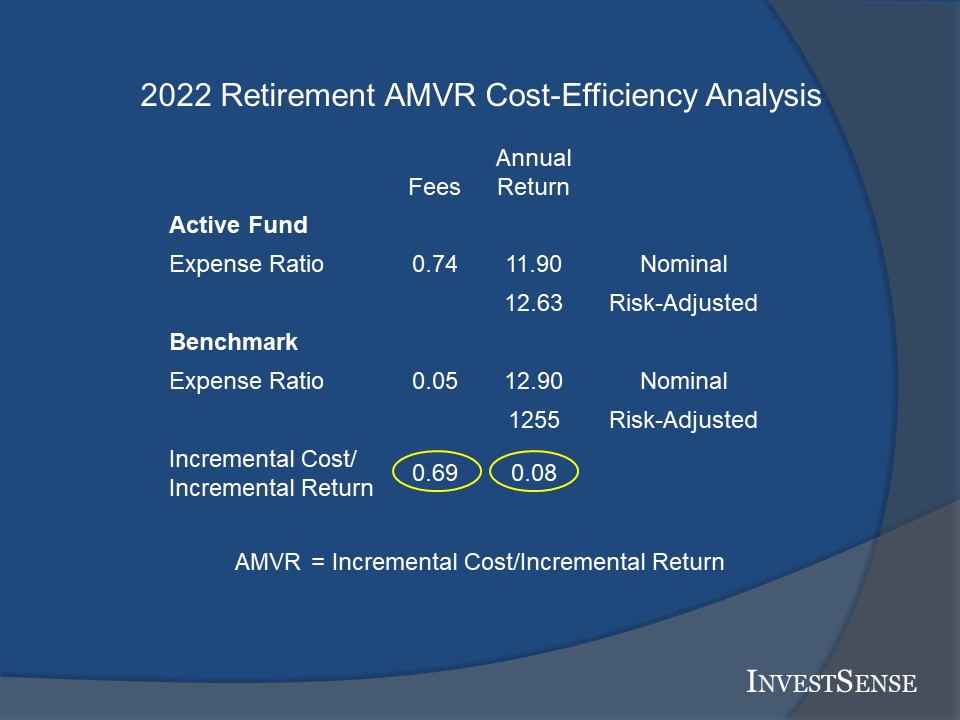

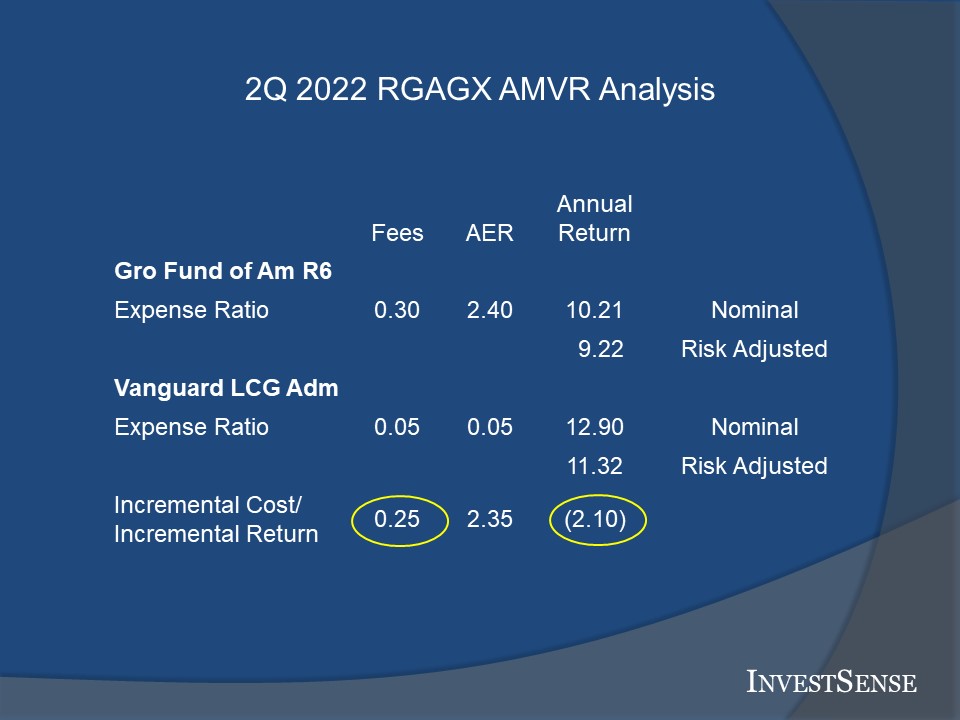

Fortunately, this relative cost-inefficiency can be proven to the courts through the use of a simple metric I created, the Active Management Value Ratio (AMVR). The AMVR is based on the research and concepts of investment notables such as Nobel laureate Dr. William F. Sharpe and Charles D. Ellis. The AMVR is simply an adaptation of the well-known cost/benefit equation, using the incremental correlation-adjusted costs and the incremental risk-adjusted returns between an actively managed fund and a comparable index fund. As the sample charts below show, while the AMVR is simple to calculate, it can provide a powerful message.

By simply adding the cost-inefficiency evidence and supporting AMVR illustrations, I believe the ERISA plaintiff’s bar can easily discredit the “apples and oranges” argument and some courts continuing support of same.

Dismissal of 401(k) Actions Based on Cost of Discovery

Courts forcing the plan participants to assume both the pleading and proof of causation responsibilities have often tried to justify such actions on the need to avoid unnecessarily placing the costs of discovery on plans. Such courts have seemingly totally ignored the inequity of such decisions.

Fortunately, a recent Sixth Circuit Court of Appeals recognized the lack of fairness and merit in such arguments. In the TriHealth16 decision, Chief Judge Sutton addressed the issue, stating that

This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth “investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares” because “the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….” Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.17

Hopefully, Judge Sutton’s insight will discredit the cost of discovery argument and result in a more equitable and fairer 401(k) litigation process.

Going Forward

Maybe it is just wishful thinking, but I believe that 2023 may actually be the year that the legal system agrees to “sing from the same ERISA hymnal,” to decide cases on a universal intrepretation of ERISA. If someone seeks cert for SCOTUS to address the “apples and oranges” and burden of proof issues. I believe the First Circuit’s Brotherston decision, and the amicus brief filed with SCOTUS by the Solicitor General in connection with Putnam’s appeal, together provide sufficient legal arguments and evidence to discredit both of said issues so that employees across America get equal and fair enforcement of the rights and protections guaranteed to them under ERISA. At the same time, I believe Judge Sutton’s endorsement of “controlled” discovery may reduce the number of 401(k) actions and allow more cases to be decided on the merits than on a questionable procedural basis.

In the Solicitor General’s amicus brief in Brotherston, the SG made a simple statement that still carries weight vis-a-vis the “apples and oranges” and the burden of proof as to causation issues:

The court of appeals correctly decided both questions.

Yes it did. Now time will tell if SCOTUS will have the opportunity to make ERISA meaningful and fair by revisiting those decisions in 2023.

Notes

1. Solicitor General’s Amicus Brief in Hughes v. Northwestern University, 9. (Hughes Amicus)

2. Hughes Amicus, 10.

3. Hughes Amicus, 14.

4. Hughes v. Northwestern Universsity, 142 S.Ct. 737 (2022).

5. Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (2018).

6. Tibble v. Edison International, 135 S.Ct.1193 (2015).

7. Hughes Amicus, 12.

8. Hughes Amicus, 12.

9. Hughes Amicus, 12.

10. Hughes, Amicus 12.

11. Brotherston, 31.

12. Brotherston, 32.

13. Brotherston, 37.

14. Brotherston, 39.

15. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

16. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

17. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

18. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

19. Forman v. TriHealth, Inc., 40 F.4th 443 (2022) (TriHealth).

20. TriHealth, 453.

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.