I have been reading a number of articles from some very impressive law firms suggesting that the attorneys for 401(k)/403(b) firms should file combine motions to dismiss with motions for summary judgment in order to deny plan participants from obtaining discovery. Fortunately, I believe most judges understand that such a move would simply ensure that SCOTUS would review the case and address the current state of 401(k)/403(b) litigation.

I have written two previous posts about the courts improperly confusing the plan participants’ duty to plausibly plead the elements of their case with a duty of one of the parties to prove what caused alleged losses. Plan participants can plausibly plead their breach of fiduciary duty claims by showing that a plan sponsor breached their fiduciary duties and the resulting losses. That is easily accomplished by using my simple Active Management Value Ratio (AMVR) metric, which allows attorneys, investment fiduciaries and investors to determine the cost-efficiency, i.e., prudence, of an actively managed fund relative to a comparable index fund.

The first forensic AMVR analysis compares the K shares of the well-known Fidelity Contrafund Fund (FCNKX) with the popular Fidelity Large Cap Growth Index Funds (FPSGX). As the analysis shows, not only does FCNKX underperform FSPGX by 237 basis points, but a plan participant would incur an even greater loss by having to pay an incremental fee of 70 basis points. Add the two losses together and, assuming similar annual results, a plan participant choosing FCNKX would suffer an annual loss of over 300 basis points.

Per the General Accounting Office (GAO), each additional one percent in costs and fees reduces an investors end-return by approximately seventeen over a twenty-year period. So, by choosing FCNKX instead of FSPGX, the plan sponsor essentially ensures that a participant in the plan may lose over half of their end return from FSPGX.

So, the obvious question is why would a prudent plan sponsor choose FCNKX over FSPGX as an investment option in their plan. One plan sponsor quickly pointed out that she chose FCNKX over FSPGX because Fidelity does not offer FSPGX to 401(k)/401(b) plans. As I explained to her, that still would not justify the choice of a cost-efficient and imprudent investment option.

So, how would FCNKX match up with the Admiral shares of Vanguard’s version of a Large Cap Growth Index Fund (VIGAX)? As the chart shows, FCNKX would still be an imprudent choice for a fiduciary, underperforming VIGAX by 96 basis points and forcing an investor to incur an incremental loss of 69 basis points, for a combined loss of 165 annually and Better, but still imprudent and a breach of the plan sponsor’s fiduciary duties.

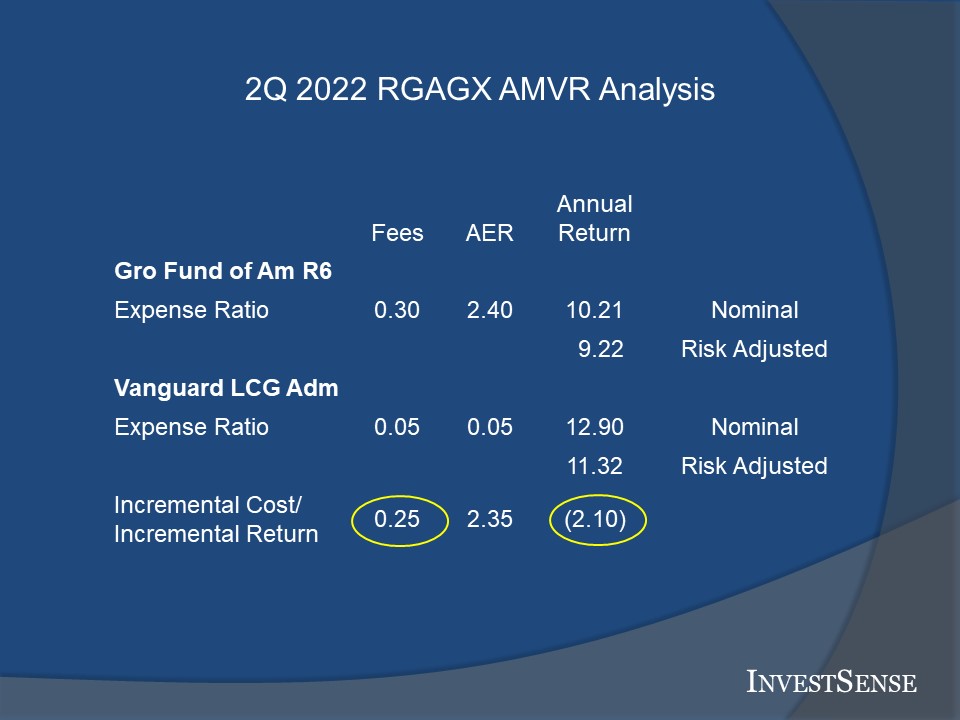

American Funds’ Growth Fund of America (GFOA) is another investment option in 401(k)/403(b). Comparing the R-6 shares of GFOA (RGAGX) with VIGAX produce similar result to the FCNKX results.

Plan participants investing in RGAGX would suffer an opportunity loss of 210 basis points and 25 basis points in incremental costs, for total damages of 245 basis points annually. Using GAO’s formula, that means that a plan participant would suffer approximately a 41 loss in end-return over 20 years.

So, plan participants’ attorneys using the AMVR metric should have no problem satisfying the federal plausible pleading requirement. Having done so, plan participants should be allowed to proceed with full discovery in the action.

Who’s Responsible for Proving Causation of Damages

Once the plan participants have shown both a fiduciary breach and the resulting losses, the next question is who is responsible for causing such damages. Ah, there’s the rub.

ERISA itself does not expressly state who is responsible for proving causing the losses incurred. So naturally, we have a split between the federal Courts of Appeal on the issues.

Both the First Circuit Court of Appeals and the Solicitor Genral addressed this issue in connection with the Brotherston case. As mentioned earlier, I have written two posts addressing the proof of causation conundrum – “Brotherston v. CommonSpirit Health: An Opportunity, and a Need, to Shift the 401(k) Litigation Paradigm,” and “Game Changer-Why Hughes v. Northwestern University Matters.”

As both the First Circuit and the Solicitor General have pointed out, a number of the federal courts have exacerbated the problem by deliberately and improperly trying to force plan participants to prove causation in connection with motion to dismiss proceedings. In essence, by denying plan participants any discovery whatsoever, some courts are forcing the plan participants to speculate as to why the plan sponsor chose obviously imprudent investments and thereby breached their fiducairy duties, as that information is known only by the plan sponsor.

First, from the First Circuit and Judge Kayatta:

The Restatement calls “for determining whether and in what amount the breach has caused a `loss’ . . . by reference to what the results `would have been if the portion of the trust affected by the breach had been properly administered.’”1

Finally, the Restatement specifically identifies as an appropriate comparator for loss calculation purposes “return rates of one or more. . . suitable index mutual funds or market indexes (with such adjustments as may be appropriate).”2 (citing § 100 cmt. b(1)

ERISA itself is not so specific. Rather, it states that a breaching fiduciary shall be liable to the plan for “any losses to the plan resulting from each such breach.” Certainly this text is broad enough to accommodate the total return principle recognized in the Restatement. Behind the text, too, stands Congress’s clear intent “to provide the courts with broad remedies for redressing the interests of participants and beneficiaries when they have been adversely affected by breaches of fiduciary duty.”3 (cjtes omitted)

And as the Supreme Court has instructed, when we confront a lack of explicit direction in the text of ERISA, we often find answers in the common law of trusts. (citing Varity Corp. v. Howe, 516 U.S. 489, 496-97, 502, 506-07 (1996) (relying on “ordinary trust law principles” to fill gaps created by ERISA’s lack of definition regarding the scope of fiduciary conduct and duties).4

[T]he burden of showing that a loss would have occurred even had the fiduciary acted prudently falls on the imprudent fiduciary. By allowing its analysis on loss to be driven by its concern regarding the objective prudence of the Putnam funds, the district court in essence required plaintiffs to show causation as part of its case on loss-even as it correctly sought to reserve that requirement to defendants.5

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes).6

As to the responsibility for proving causation, Judge Kayatta stated that

[T]here is what the Supreme Court has called the “ordinary default rule.” Under this rule, courts ordinarily presume that the burden rests on plaintiffs “regarding the essential aspects of their claims.” That normal rule, however, “admits of exceptions….” For example, “[t]he ordinary rule, based on considerations of fairness, does not place the burden upon a litigant of establishing facts peculiarly within the knowledge of his adversary,” although there exist qualifications on the application of this exception.7

That exception recognizes that the burden may be allocated to the defendant when he possesses more knowledge relevant to the element at issue…. Common sense strongly supports this conclusion in the modern economy within which ERISA was enacted. An ERISA fiduciary often — as in this case — has available many options from which to build a portfolio of investments available to beneficiaries. In such circumstances, it makes little sense to have the plaintiff hazard a guess as to what the fiduciary would have done had it not breached its duty in selecting investment vehicles, only to be told “guess again.” It makes much more sense for the fiduciary to say what it claims it would have done and for the plaintiff to then respond to that.8

In concluding, Judge Kayatta made two significant points:

The Supreme Court has time and again adopted ordinary trust law principles to construe ERISA in the absence of explicit textual direction.9

[T]he Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected “Congress'[s] desire to offer employees enhanced protection for their benefits…. In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection than they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.10

Next, from the Solicitor General as to the issue of pleading plausibility:

Considering those allegations together and taking them as true at the pleading stage, the Amended Complaint plausibly states a claim that respondents acted imprudently….11

Petitioners did not merely present a conclusory assertion that the Plans’ recordkeeping fees were too high; they substantiated their claim with specific factual allegations about market conditions, prevailing practices, and strategies used by fiduciaries of comparable Section 403(b) plans.12

Going Forward

Full disclosure: I am, by nature, a plaintiff’s attorney. I fully support the federal rules requiring that plaintiffs establish the plausibility of their actions. I fully acknowledge that ERISA does not expressly provide that plan sponsors have the burden of proof with regards to causation of damages. However

However, I do agree with Judge Kayatta that since only plan sponsors know whether they fulfilled their fiduciary duties by conducting an independent investigation and evaluation of each investment option selected for a plan, as well as the methodology they employed in connection with such duties, it would make sense to shift the burden of proof on causation to the plan sponsor.

If a court is determined to force the plan participants to carry the burden of proof regarding causation, it is clearly inequitable and arguably a blatant violation of the spirit and purpose of ERISA to deny plan participants the opportunity to conduct meaningful discovery to determine whether a plan sponsor did in fact breach their fiduciary duties by not properly conducting their independent investigation and evaluation of the plan’s investment options, or not performing such duties at all. In many cases, the results of an AMVR analysis on each investment option in the plan results in strong circumstantial suggestions of the latter being true

One could argue, with merit, that by confusing the burden of proof with the duty of plausible pleading and denying plan participants the rights and protections provided for them under ERISA, some courts are guilty of the very same sort of abusive actions that ERISA was created to protect employees against. In this case, the only difference is that the legal system is the offending party.

But judges are smart people; they have to understand that the duty to plead plausibly and the burden of proof are properly two separate duties which, while related, are legally understood to be two distinct proceedings, primarily to allow the party carrying the burden of proof to gather the necessary information and evidence. So why are some courts seemingly determined to blatantly deny plan participants their ERISA rights and protections in order to protect plan sponsors who breach their fiduciary duties? My guess they will never allow us to discover the answer to that question.

In the meantime, I am advising my clients to ignore all the celebratory announcements, articles, and posts when a court dismisses a 401(k) or 403(b) action. Why? When SCOTUS eventually addressed these issues, just as in the Northwestern University case, and SCOTUS vacated the Seventh Circuit’s decision, it was neither the plan adviser, who provided the improper advice, nor the Seventh Circuit, who misinterpreted the plain language of ERISA, who faced renewed liability and damages. It was only the plan sponsor, Northwestern University, the faced the renewed liability exposure.

I try to read every decision handed down in connection with 401(k)/403(b) actions to determine whether the decisions are based on solid legal reasoning and consistent with applicable laws or regulations. As I tell my fiduciary clients, without those two foundations, a decision in favor of a plan sponsor often accomplishes nothing more than create a temporary and false sense of security, while the plan participants decide whether to appeal.

One final point. Thus far, the recent decisions dismissing 401(k)/403(b) actions have ignored both the First Circuit’s decision and the court’s reasoning and excellent analysis of the applicability of the common law of trusts and the Restatement (Third) of Trusts (Restatement). The decisions have ignored SCOTUS’ recognition of the Restatement as a resource in settling fiduciary disputes. More specifically, the decisions have ignored the commonsense standards of fiduciary prudence set forth in the Section 90 of the Restatement, otherwise known as the “Prudent Investor Rule,” such as comments b, f, and h(2).

SCOTUS had an opportunity to address these issues earlier when Putnam Investments asked the Court to review the case. It was the perfect case to resolve these issues. However, SCOTUS followed the Solicitor General’s advice and refused to hear the appeal, as the appeal was what is known as an interlocutory appeal, meaning the case was still in progress in the First Circuit Court of Appeals. The case eventually settled.

As the Solicitor has noted several times, ERISA is simply too important to not have the courts apply the law consistently and equitably. It has been estimated that approximately 30 percent of the nation’s wealth in tied up in 401(k) and 403(b) plans. The potential economic harm to both plan participants and plan sponsors from the current inconsistent and inequitable trends in 401(k)/403(b) litigation are just too important to continue to be unaddressed and unresolved.

Notes

1. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 31 (2018) (Brotherston).

2. Brotherston, 31.

3. Brotherston, 31.

4. Brotherston, 31.

5. Brotherston, 33.

6. Brotherston, 34.

7. Brotherston, 36.

8. Brotherston, 36.

9. Brotherston, 37

10. Brotherston, 31.

11. Brief for the United States as Amicus Curiae, Hughes v. Northwestern University, United States Supreme Court, No. 19-1401, 14. (Amicus Brief)

12. Amicus Brief, 14.

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.