In my last post, I published the “cheat sheets” for six of the most commonly used non-index-based funds in U.S. defined contribution plans. However, those funds did not include any target date funds (TDFs).

TDFs are diversified asset allocation funds which supposedly provide a simple way for investors to work toward “retirement readiness” and “financial well-being.” However, questions have started to arrive as to the prudence of TDFs in terms of both safety and cost-efficiency. As a result. TDFs have become the targets themselves of 401(k) and 403(b) litigation.

Two of the largest litigation targets have been Fidelity’s Freedom TDFs and TIAA-CREF’s Lifecycle TDFs. One of the primary issues in litigation involving these two groups of TDFs has been the fact that both offer both active and passive versions of their TDFs.

In both cases, the active versions of the TDFs charge higher fees. Most 401(k) and 403(b) plans have chosen the active versions of the TDFs, despite their consistent underperformance over time relative to the less expensive passive, or index, versions of the funds.

Several courts have dismissed 401(k) and 403(b) cases citing the alleged failure of the plan participants to properly plead their cases. Under the federal rules of civil procedure, the plan participants are required to provide sufficient facts to show that it is plausible to believe that the plan’s sponsor failed to properly perform their fiduciary duties of loyalty and/or prudence.

Some courts have accepted evidence of the disparity between a fund’s costs and returns as providing sufficient evidence of the plausibility that a plan sponsors failed to properly perform their fiduciary duties. One such case is the Leber v. Citigroup 401(k) action1, where highly respected Judge Sidney Stein denied Citigroup’s motion to dismiss the case, citing the fact that the plan participants had shown that in some cases the expense ratios of the funds in question were 200 percent of more higher than the expense ratios of comparable Vanguard funds.

Judge Stein’s recognition of both the impact of a disparity in expense ratios and the legitimacy of Vanguard funds as comparators in 401(k) and 403(b) cases should not go unnoticed. Nevertheless, some courts continue to ignore and/or reject similar evidence as establishing the plausibility of a fiduciary breach, as required in 401(k) and 403(b) cases.

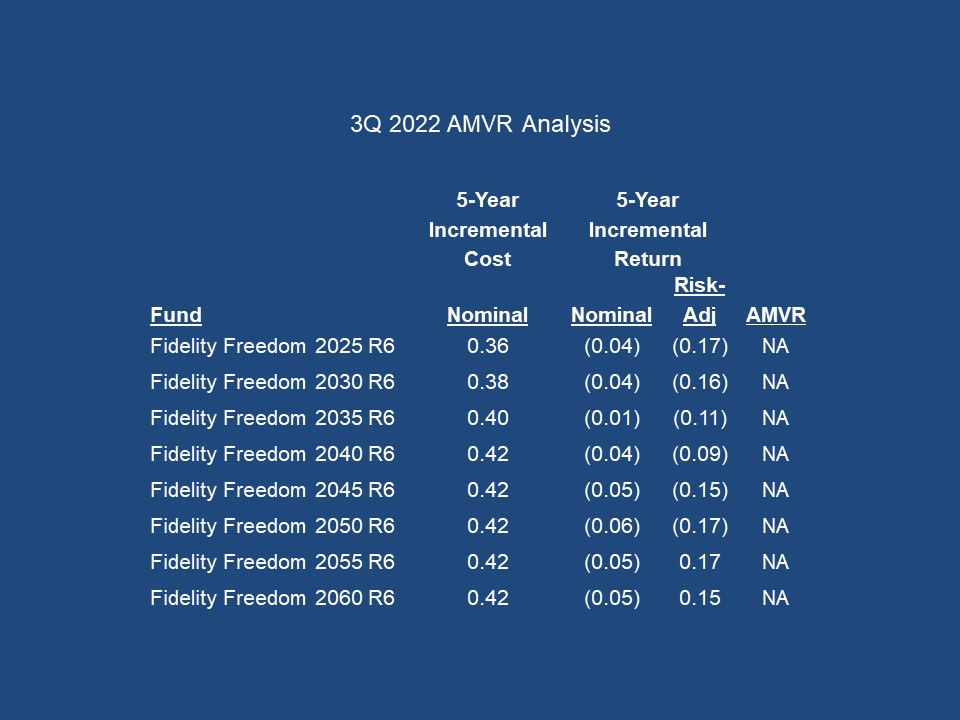

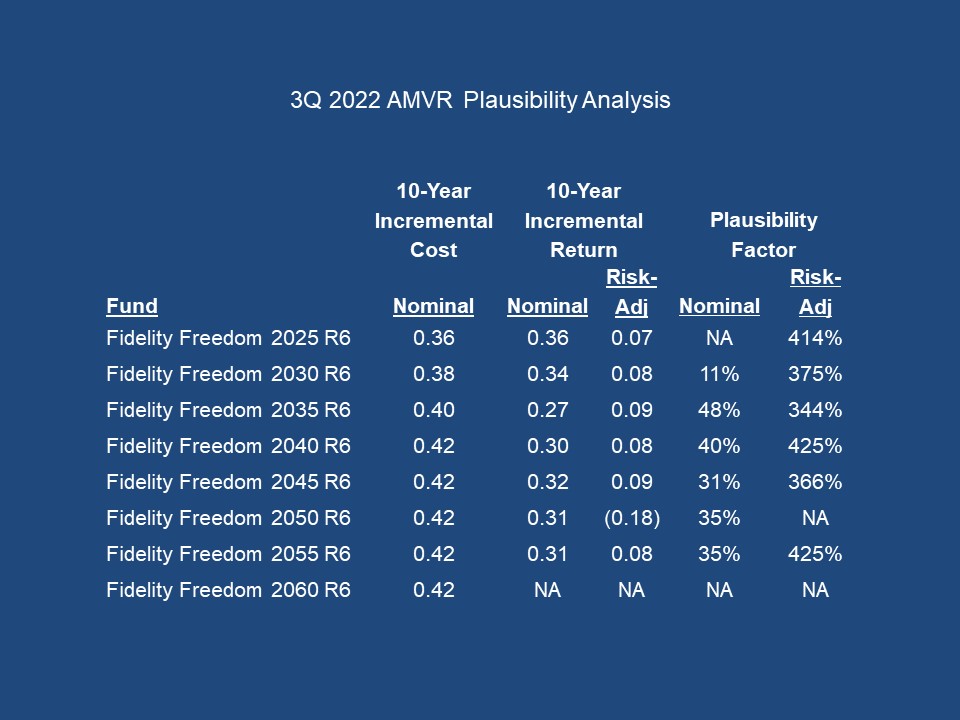

In my practice, I also calculate a “plausibility factor” based upon my Active Management Value Ratio (AMVR) analyses. In the case of the two charts shown above, the plausibility should be resolved for the five-year period by the fact that with the exception of two cases,none of the TDFs even managed to provide a positive incremental return at all. In the two cases where the funds did produce a positive incremental return, the funds’ incremental costs exceeded such returns, making them cost-inefficient.

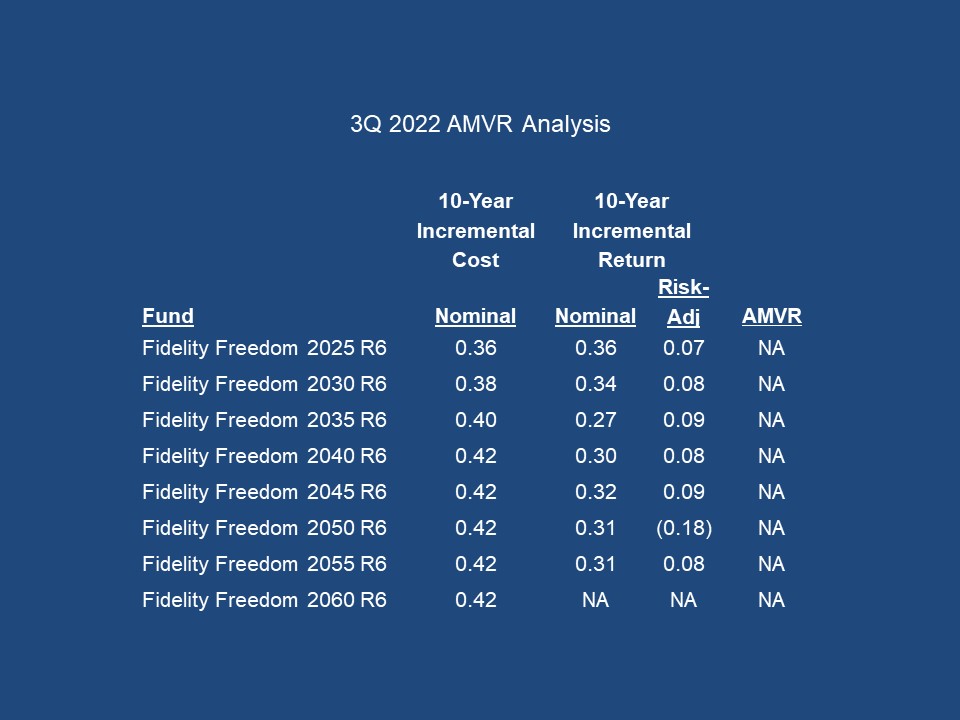

The plausibility analysis for the ten-year AMVR analysis not only shows the significant percentage disparity in incremental costs and incremental returns, but also how important it is for a fiduciary to factor in risk in order to obtain a meaningful “apples to apples” assessment and to avoid unnecessary exposure to fiduciary liability.

Interestingly, while pension plans and the financial services that argue for “apples to apples” comparisons, they generally dismiss risk-adjusted analyses. This plausibility chart may help explain why.

Going Forward

I am on record as saying that plan participants should never lose a properly vetted 401(k)/403(b) case. My position is based on the ease with which plan participants and their attorneys can establish both the plausibility and the legitimacy of the damages in their case through the use of the AMVR metric and plausibility analysis. Both analyses require nothing more than simple math and provide compelling evidence of any fiduciary breach. As John Adams said, “facts are stubborn things.”

Notes

1. Leber v. Citigroup 401(k) Plan Inv. Committee, 2014 WL 4851816.

You must be logged in to post a comment.