James W. Watkins, III, J.D., CFP Board EmeritusTM, AWMA

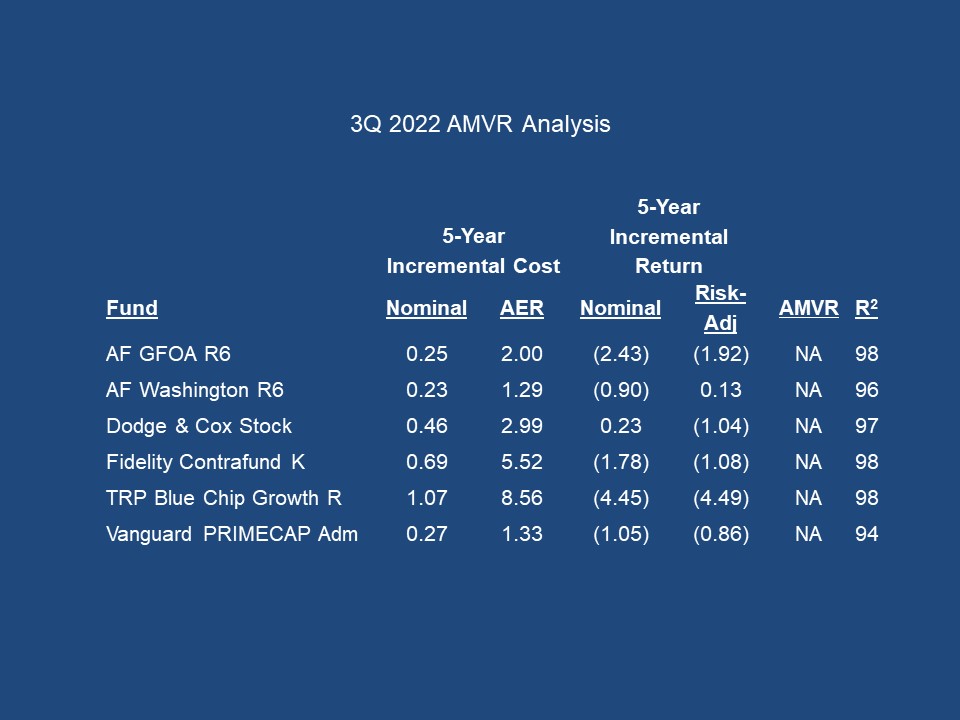

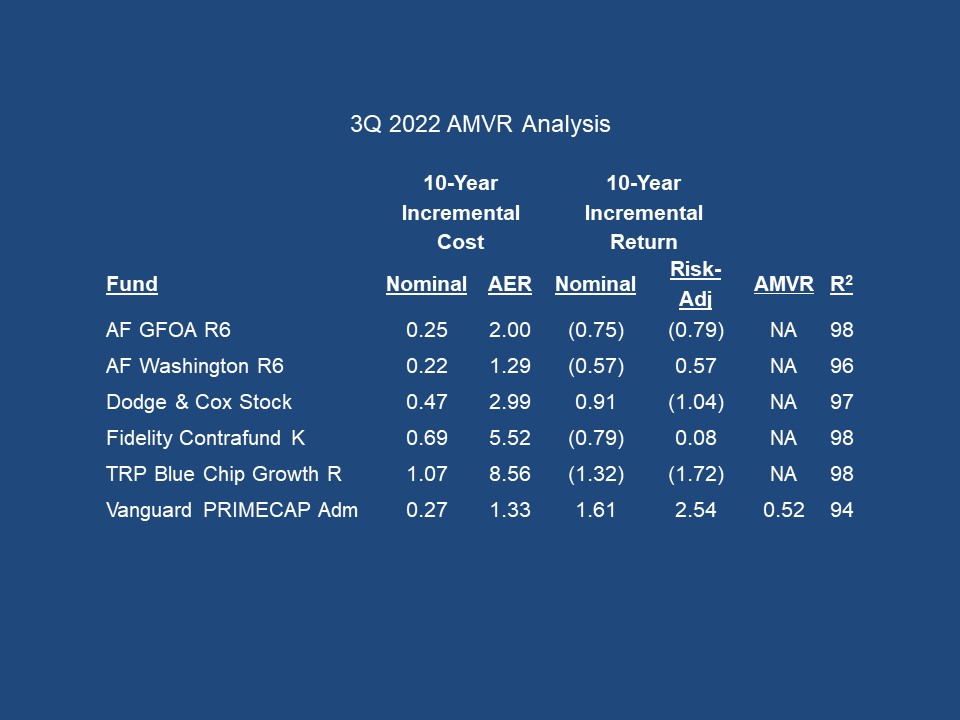

Given the recent performance of the markets, it should come as no surprise that the 5 and 10-Year AMVR analyses of the six most popular non-index mutual funds in U.S. defined contribution plans remain relatively unchanged.

Interesting to note that for both the 5 and 10-year period, only Vanguard PRIMECAP Admiral shares managed to qualify for an AMVR ranking.

Also interesting to note the importance of factoring in a fund’s risk-adjusted returns. On the 5-year AMVR analyses, factoring in risk-adjusted returns turned AF’s Washington Mutual Fund’s incremental return from (0.90) on nominal returns, to a positive 0.13. Admittedly, a small positive number, but still a significant change.

On the 10-year AMVR analyses slide, factoring in the fund’s risk-adjusted returns turned their incremental return from (0.57) (nominal) to 0.57 (risk-adjusted.) Likewise for Fidelity Contafund, where an incremental return of (0.79) (nominal) turned into a small, yet positive, 0.09.

Overall, the song remains the same, with the majority of actively managed funds being unable to overcome the combination of the weight of higher fees and cost and high r-squared/correlation of returns number to beat the index of comparable index funds

And so, we continue to see 401(k) actions alleging a breach of fiduciary duties by plan sponsors. Of note, we are seeing an increasing number of cases focusing on target date funds (TDFs). I expect to see more actions involving TDFs, as the AMVR provides compelling evidence of the imprudence of the active versions of such funds. I will post an updated analysis of the active and index versions of both the Fidelity Freedom and TIAA-CREF Lifestyle TDFs next week

I have often noted SCOTUS’ recognition that an ERISA fiduciary’s duties are “derived from the common law of trusts. In determining the contours of an ERISA fiduciary’s duty, courts often must look to the law of trusts.”1

This statement from SCOTUS should not come as a surprise. Courts have often noted that ERISA is essentially a codification of the common law of trusts, as reflected in the Restatement of Trusts (Restatement). This similarity is especially noticeable in the fact that two consistent themes run throughout both of them-the importance of cost-consciousness and risk management.

As an ERISA attorney, I created the Active Management Value (AMVR) metric as a means of focusing on these topics in the context of fiduciary liability, specifically liability based on cost-inefficiency and ineffective risk management.

The basic AMVR is based primarily on the research of Charles D. Ellis and Nobel laureate Dr, William F. Sharpe. Dr. Sharpe has offered the following advice for analyzing the prudence of mutual funds:

Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs…. The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.2

Noted wealth management expert, Ellis, goes further, stating that

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!3

The financial services industry and 401(k)/403(b) plan advisers like to avoid the issues of fiduciary duties, transparency, and cost-inefficiency by avoiding comparisons of fund performance and only discussing returns in terms of nominal, or publicly stated, returns. Unfortunately, nominal returns are often misleading when fiduciary duties and potential fiduciary liability is involved.

AMVR FAQs

As the basic AMVR has gained increased recognition and use by investment fiduciaries and attorneys, there has also been increased recognition of the potential for the power of the advanced version of the AMVR, aka AMVR+. The basic AMVR is simply the cost/benefit analysis many of us used in our Econ 101 class, with the inputs being incremental costs and incremental returns.

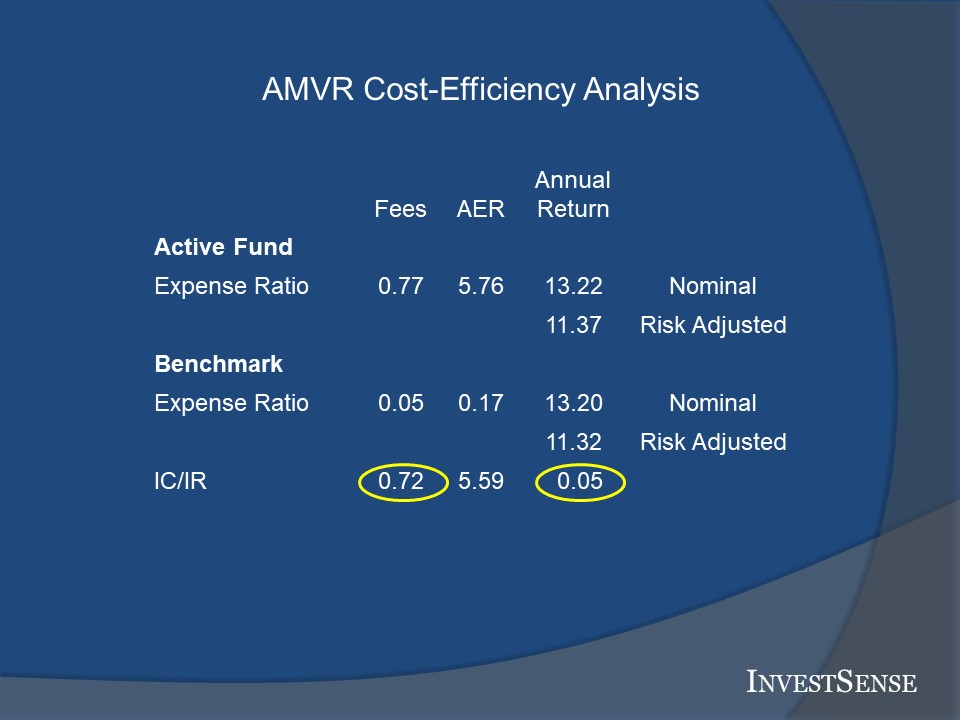

In analyzing an AMVR analysis, the user only needs to answer two simple questions:

(1) Did the actively managed fund provide a positive incremental return?

(2) If so, did actively managed fund’s positive incremental return exceed the fund’s incremental costs.

If the answer to either of these questions is “no,” then, under the Restatement’s standards, the actively managed fund is imprudent relative to the benchmark index fund.

Here, the active fund’s incremental costs (72 basis points) exceed the fund’s incremental returns (5 basis points). “Basis points” is a term used in the financial services industry. I often tell people to just monetize the results by thinking in terms of dollars. Would you give someone $72 in exchange for $5. The prosecution rests.

Sadly, this scenario is common in 401(k)/403(b) plans. As a result, the number of ERISA actions against 401(k)/403(b) plans continues to increase.

The AMVR could easily help 401(k)/403(b) plans avoid such unnecessary liability exposure. Most AMVR analyses can be accomplished in 1-2 minutes and require no more than what one judge described as “third grade math…but very persuasive third grade math,” as he denied a plan’s motion to prevent the use of the AMVR in a 401(k) action.

Advanced AMVR Analysis

A well-known saying in the investment industry is that “amateurs focus on returns; professionals focus on risk management.” Search “investment risk management Charles D. Ellis” and you will find his familiar statement that the secret of successful investing is the informed management of investment risk. Perform the same search using the names of investment icons Benjamin Graham and Paul Tudor Jones and you will find similar statements.

Plan sponsors and other investment fiduciaries are gradually recognizing the power of the AMVR as a risk management tool. The advanced version of the AMVR, AMVR+, addresses three types of risk:

1. The risk of cost-inefficiency,

2. The risk of underperformance, and

3. The risk of the investment risk, aka volatility.

The Risk of Cost-Inefficiency

The basic premise of cost-inefficiency is simple to express–costs exceeding benefits/returns. In connection with investing and the AMVR, it is incremental costs exceeding incremental benefits aka returns. An investment in a cost-efficient investment means an investor would actually be losing money. The fact that costs, like returns, compound over time only exacerbates the investment risk and resulting damage.

While many people continue to debate the relative merits of active management versus passive management, I maintain that issue is, and always has been, a meaningless debate. The more meaningful question is cost-efficiency versus cost-inefficiency.

A cost-inefficient investment can never be a prudent investment choice, especially for an investment fiduciary. Even the Restatement acknowledges this fact.

The cost-inefficiency of many actively managed funds may be even worse than it appears at first glance. Ross Miller’s Active Expense Ratio suggests that the effective expense ratio of many actively managed funds is often understated by as much as 400-500 percent. Miller explained the importance of the Active Expense Ratio and AW as follows:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.4

The Risk of Underperformance

Again, a simple concept. An actively managed fund that fails to provide a positive incremental return when compared to a comparable index fund represents an opportunity cost equal to the incremental return that could have been realized by investing in the better performing index fund.

Studies have consistently shown that the overwhelming majority of actively managed funds underperform comparable index funds.5 Given the higher costs typically associated with active management, including higher management fees and trading costs, these findings should come as no surprise, especially given the high correlation of returns between most U.S. domestic equity funds and their index counterparts.

The high correlation of return, often 95 and above, raises the issue of potential “closet indexing.” Closet indexing refers to the practice of actively managed funds marketing the benefits of the active management they allegedly provide, only to provide similar, in many cases lower returns. than a comparable index fund

Correlations of 95 and above raise genuine issues of whether active management was provided at all, and the issue of exactly how much active management was provided. Ross Miller’s Active Expense Ratio metric calculates the Active Weight (AW), or the percentage of active management provided by a fund. AW can be calculated simply through the use of an actively managed fund’s expense ratio and its r-squared, or correlation of returns, number.

With so many active funds having a correlation of 95 and above to comparable index funds, it is interesting to note the estimated AW of such funds. Miller found that there is not a one-to-one correlation between r-squared to the percentage of active management provided. For instance, Miller found that active funds with a correlation number of 98 only provide an estimated 12.50 percent in active management.

Miller’s studies clearly demonstrate the value of factoring in correlations of return between actively managed funds and comparable index funds. This is why we use Miller’s Active Expense Ratio in calculating correlation-adjusted costs in order to provide a more meaningful cost-efficiency analysis in our AMVR+ analyses.

The Risk of Investment Risk/Volatility

Studies have consistently shown that investment returns are influenced by the level of investment risk assumed, the so-called risk-return equation.

Section 90, comment h(2). of the Restatement (Third) of Trusts is a fundamental principle of fiduciary law and prudent investing. Section 90(h)(2) states that the use of actively managed strategies is imprudent unless it can be reasonably predicted that the active strategy will provide a commensurate return for the additional costs and risks typically associated with active investing.

As mentioned previously, most actively managed funds simply cannot meet this requirement, due largely to the burden of higher management fees/expenses and trading costs. This is the reason InvestSense factors in a fund’s risk-adjusted return in our AMVR+ cost-efficiency analyses. While many advocates of active management dislike the use of risk-adjusted returns, the fact is that factoring in risk often improves the cost-efficiency numbers for actively managed funds since it is a factor that they can actually control.

Going Forward

The evidence clearly establishes the potential benefits of the AMVR and AMVR for investment fiduciaries, attorneys, and investors. Investment fiduciaries can avoid unnecessary and unwanted fiduciary liability exposure. Attorneys and easily establish the merits of their case and comply with applicable pleading standards. Investors can analyze the prudence of their investment and hopefully better protect their financial security.

Notes

1. Tibble v. Edison International, 135 S. Ct 1823 (2015)

2. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm.

3, Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online at https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c.

4. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-4.

5. Laurent Barras, Oliver Scaillet, and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010); Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, https://www.ft.com/content/6b2d5490-d9bb-eb37a6aa8e; Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE 57-58 (1997); Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Funds Advisors, L.P., August 2016.

You must be logged in to post a comment.