In the midst of chaos, there is also opportunity – Sun Tzu

As an ERISA attorney, the Sixth Circuit’s recent CommonSpirit Health (CommonSpirit) decision1 concerns me. First, the Court completely ignored the First Circuit’s Brotherston decision2, the Restatement (Third) of Trusts (Restatement), and SCOTUS’ subsequent denial of Putnam’s appeal of that decision.

Second, the fact that the CommonSpirit decision has revived the meritless “apples and oranges” argument regarding fiduciary prudence, even though both the Brotherston decision and SCOTUS’ denial of cert discredited such an argument. As a result, the Sixth Circuit has arguably created an unnecessary divide within the circuits.

Upon a recent re-reading of the CommonSpirit decision, I realized that the Sixth Circuit may have actually provided a valuable opportunity to provide more certainty for plan sponsors and to clarify the guidelines going forward for 401(k)/403(b) administration and litigation.

Brotherston v. Putnam Investments, LLC

The Restatement calls “for determining whether and in what amount the breach has caused a `loss’ . . . by reference to what the results `would have been if the portion of the trust affected by the breach had been properly administered.'”3

Finally, the Restatement specifically identifies as an appropriate comparator for loss calculation purposes “return rates of one or more. . . suitable index mutual funds or market indexes (with such adjustments as may be appropriate).”4 (citing § 100 cmt. b(1)

ERISA itself is not so specific. Rather, it states that a breaching fiduciary shall be liable to the plan for “any losses to the plan resulting from each such breach.” Certainly this text is broad enough to accommodate the total return principle recognized in the Restatement. Behind the text, too, stands Congress’s clear intent “to provide the courts with broad remedies for redressing the interests of participants and beneficiaries when they have been adversely affected by breaches of fiduciary duty.”5 (cjtes omitted)

And as the Supreme Court has instructed, when we confront a lack of explicit direction in the text of ERISA, we often find answers in the common law of trusts. (citing Varity Corp. v. Howe, 516 U.S. 489, 496-97, 502, 506-07 (1996) (relying on “ordinary trust law principles” to fill gaps created by ERISA’s lack of definition regarding the scope of fiduciary conduct and duties).6

[T]he burden of showing that a loss would have occurred even had the fiduciary acted prudently falls on the imprudent fiduciary. By allowing its analysis on loss to be driven by its concern regarding the objective prudence of the Putnam funds, the district court in essence required plaintiffs to show causation as part of its case on loss-even as it correctly sought to reserve that requirement to defendants.7

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes).8

In concluding, Judge Kayatta made two significant points:

The Supreme Court has time and again adopted ordinary trust law principles to construe ERISA in the absence of explicit textual direction.9

[T]he Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected “Congress'[s] desire to offer employees enhanced protection for their benefits…. In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection than they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.10

CommonSpirit Health

Trust law informs the duty of prudence, as “an ERISA fiduciary’s duty is derived from the common law of trusts.”11

[The federal pleading] rules require the plaintiff to provide sufficient “facts to state a claim to relief that is plausible on its face.” Plausibility requires the plaintiff to plead sufficient facts and law to allow “the court to draw the reasonable inference that the defendant is liable for the misconduct alleged.” “The plausibility of an inference depends on a host of considerations, including common sense and the strength of competing explanations for the defendant’s conduct.”12

Even if CommonSpirit did not violate a fiduciary duty by offering actively managed plans in general, it is true, the company still could violate ERISA by imprudently offering specific actively managed funds. ERISA, in other words, does not allow fiduciaries merely to offer a broad range of options and call it a day. While plan participants retain the right to choose which fund is appropriate for them, the plan must ensure that all fund options remain prudent options.13

Nor does a showing of imprudence come down to simply pointing to a fund with better performance. We accept that pointing to an alternative course of action, say another fund the plan might have invested in, will often be necessary to show a fund acted imprudently (and to prove damages). But that factual allegation is not by itself sufficient. In addition, these claims require evidence that an investment was imprudent from the moment the administrator selected it, that the investment became imprudent over time, or that the investment was otherwise clearly unsuitable for the goals of the fund based on ongoing performance.14

That is why disappointing performance by itself does not conclusively point towards deficient decision-making, especially when we account for “competing explanations” and other “common sense” aspects of long-term investments. In context, such allegations standing alone do not move the claim from possible and conceivable to plausible and cognizable.15

We would need significantly more serious signs of distress to allow an imprudence claim to proceed….publicly available performance information about an investment may show sufficiently dismal performance that this reality, when combined with ‘allegations about methods,’ will successfully allege that a prudent fiduciary would have acted differently.16

An Opportunity Out of Chaos?

Most 401(k) litigation focuses on the nominal returns of the investment options within a plan. Both the First Circuit and the Sixth Circuit agree on the importance of trust law in interpreting ERISA. As the Brotherston decision points out, the Restatement explicitly authorizes the use of index funds as comparators, discrediting the “apples and oranges” argument.

However, the Restatement provides other valuable guidelines in determining fiduciary prudence. Section 90 of the Restatement sets out several relevant cost-efficiency standards in determining whether a fiduciary has fulfilled its fiduciary duty of prudence, including

- A fiduciary has a duty to be cost-conscious.17

- A fiduciary has a duty to select mutual funds that offer the highest return for a given level of cost and risk; or, conversely, funds that offer the lowest level of costs and risk for a given level of return.18

- Actively managed mutual funds that are not cost-efficient, that cannot be “justified by realistically evaluated expectations” to provide a commensurate return for the additional costs abd risks typically associated with active management are imprudent.19

Given these guidelines, the research on the cost-efficiency of actively managed mutual funds suggest that plan sponsors face a daunting challenge in trying to justify the inclusion of actively managed mutual funds in a 401(k) plan:

- 99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.20

- Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.21

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.22

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.23

However, the Sixth Circuit insisted on “more serious signs of distress” and the use of publicly available performance information to show “sufficiently dismal performance” to establish that a plan sponsor breached their fiduciary duties

The Active Management Value Ratio™

I have suggested for some time that the Active Management Value Ratio (AMVR) is a valuable tool in analyzing the prudence of plan sponsors and other investment fiduciaries. The CommonSpirit decision seems to be the perfect opportunity to prove my assertions.

As I have noted in previous posts on this site, the AMVR is based on the investment research of investment notables such as Nobel Laureate Dr. William F. Sharpe, Charles D. Ellis, Burton L. Malkiel, and Ross Miller. The fundamental premise behind the AMVR is cost-efficiency, a criticial factor in assessing fiduciary prudence under the Restatement.

As Ellis has consistently suggested,

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!24

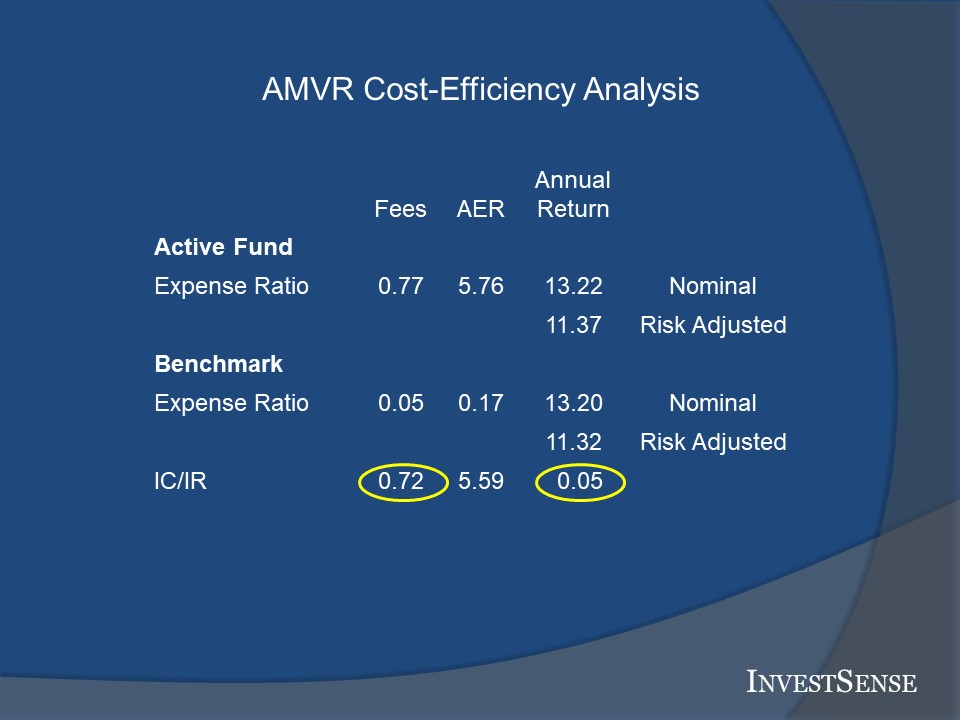

A sample of an AMVR analysis supports Ellis’ position.

When I perform an AMVR analysis, I provide two sets of numbers, one set being based on the funds’ nominal, or publicly reported, numbers, the other set being based on the funds’ correlation-adjusted costs and risk-adjusted returns. Experience has shown that the investment and 401(k) industries typically prefer the nominal numbers, while ERISA plaintiff attorneys prefer the adjusted numbers.

The AMVR is simple and straightforward, requiring only the ability to compare the data between an actively managed fund and a comparable index fund by simple subtraction. A plan sponsor, or any other investment fiduciary, then just has to answer two simple questions:

- Did the actively managed funds provide a positive incremental return?

- If so, did the actively managed fund’s incremental return exceed the fund’s incremental costs?

If the answer to either question is “no,” then the actively managed fund is cost-inefficient/imprudent relative to the comparable index fund.

The AMVR slides speak for themselves. Situations where an investment’s incremental costs exceed its incremental returns is never a desirable, or prudent, investment scenario. Cost-inefficient investment alternatives within a 401(k) plan are not legally valid “choices.” Additional details on the calculation and interpretation of the AMVR are available on this website.

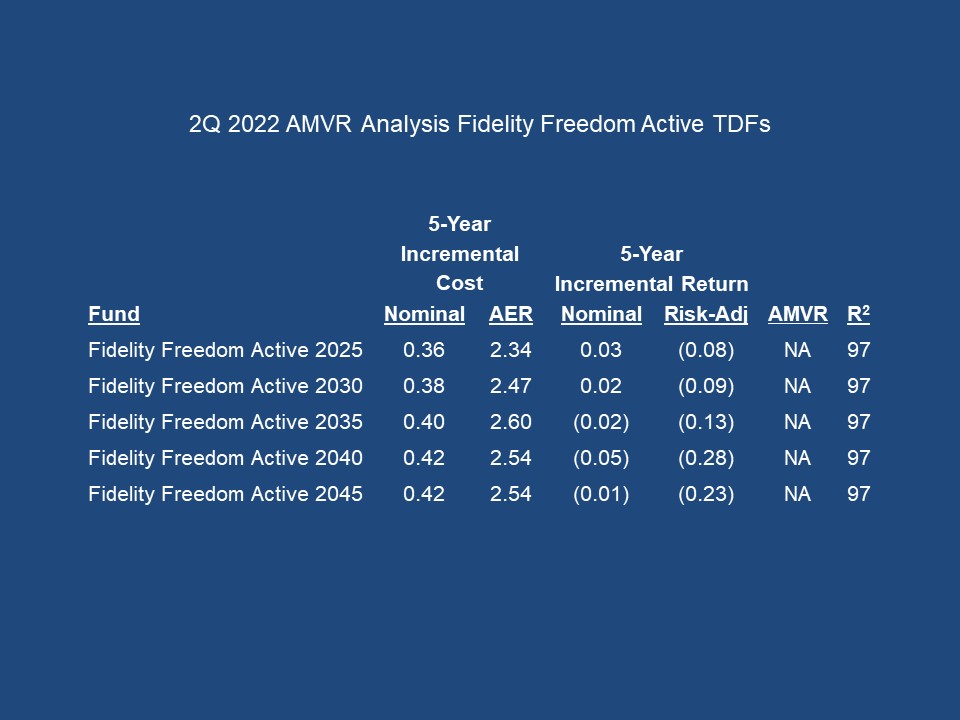

In CommonSpirit, the primary issue was the alleged imprudence/ cost-ineffficiency of Fidelity’s Freedom Funds (Active Suite) compared to Fidelity’s Freedom Funds Index Funds. I performed an AMVR analysis on several of the funds to determine the merits of the plaintiffs’ case.

The results of an AMVR analysis on several of the other Freedom funds provide similar results.

The AMVR analyses clearly show that in most cases the Active Suite not only underperformed the comparable index shares, but such opportunity cost/loss was further compounded by the fact that an investor incurred additional incremental costs in connection with such funds, while receiving actually nothing in return for such costs. This is the antithesis of fiduciary prudence.

The situation becomes even worse if the costs are adjusted for the correlation between the active suite funds and the comparable index funds, shown here based on Miller’s Active Expense Ratio (AER). Miller described the importance of the AER:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.25

The second slide shows just how much of an impact the combination of a fund with high incremental costs and a high correlation of returns can have on the effective costs that an investor pays for a active management, further reducing the cost-efficiency of an investment and overall prudence.

Going Forward: An Opportunity Amidst Chaos

The Sixth Circuit has created a division between itself and the First Circuit on the issue of whether index funds are valid comparators, “meaningful benchmarks,” in 401(k) actions. The two circuits do agree with SCOTUS that the common law of trusts provides insight on fiduciary law issues, including on questions involving fiduciary prudence. The two circuits also agree on the importance of costs.

The Restatement is just that, a restatement of the common law of trusts. In Tibble26, SCOTUS specifically noted that the courts often turn to the Restatement for guidance in resolving questions involving fiduciary law, including questions involving ERISA.

As the First Circuit noted, Section 100 the Restatement expressly approves of the use of index funds as comparators in 401(k) litigation. The AMVR can be used by plan sponsors and attorneys to easily prove that in the overwhelming majority of cases, the inclusion of actively managed mutual funds in a 401(k) plan cannot satisfy the Restatement’s requirement that the use of actively managed funds/strategies be justifiable by “realistically evaluated return expectations” of providing a commensurate return for the additional costs and risks associated with active management, are imprudent.

“Wilful blindness” is a legal term often defined as “a conscious avoidance, a judicially-made doctrine that expands the definition of knowledge to include closing one’s eyes to the high probability a fact exists.” Despite acknowledging the importance of the common law of trusts, the Sixth Circuit has seemingly decided to ignore the Restatement’s positions with regard to both index funds as acceptable benchmarks in 401(k) litigation and the concerns over a fiduciary’s use of active management strategies and/or products. However, “facts do not cease exist because they are ignored.”

The Sixth Circuit states asserts that plaintiffs must do more than simply pleading the underperformance of an actively managed fund. Under the federal pleading rules, the Sixth Circuit says that in order to satisfy federal pleading rules, plan participants must plead facts that establish the plausibility, not just the possibility, that a plan sponsor breached of their fiduciary.

The AMVR provides plan plaintiffs and their attorneys with a simple means to provide the “more” that both the Sixth Circuit and the plausibility pleading standard demand. By combining the AMVR with the overwhelming research establishing the cost-efficiency of actively managed, plan participants can establish both the underperformance of actively managed funds, and the resulting cost-efficiency of such funds due to the fact that such funds’ incremental costs exceeding incremental returns, if any, provided by such funds.

The AMVR also eliminates the need for courts and plan sponsors to consider immaterial collateral issues such as a fund’s classification (active, passive, large cap, small cap) and/or investment strategy (growth, income), as the use of cost-efficiency as the comparator cuts across such factors to provide an evaluation based on the stated purpose of ERISA, that being the best interests of the plan participants and their beneficiaries.

The plaintiffs have not announced whether they intend the to appeal the Sixth Circuit’s CommonSpirit decision. I hope that the decision is appealed in order to shift the paradigm in connection with 401(k) plans and to clarify the applicable standards in 401(k) and 403(b) litigation. Such a final resolution would provide much needed clarity for both plan sponsors and the courts as to the applicable guidelines for plan administration and allow plan sponsors to design win-win 401(k)/403(b) plans that actually promote the best interests of both plan participants and plan sponsors.

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

Notes

1. Smith v. CommonSpirit Health, No. 21-5964, June 21, 2022 (6th Cir. 2022). (CommonSpirit)

2. Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (2018) (Brotherston)

3. Brotherston, 31.

4. Brotherston, 31.

5. Brotherston, 31.

6. Brotherston, 33.

7. Brotherston, 34.

8. Brotherston, 36.

9. Brotherston, 36.

10. Brotherston, 37.

11. CommonSpirit, Section II.A.

12. CommonSpirit, Section II.A.

13. CommonSpirit, Section II.A.

14. CommonSpirit, Section II.A.

15. CommonSpirit, Section II.A.

16. CommonSpirit, Section II.A.

17. Restatement (Third) Trusts, Section 90, Introductory Comment. American Law Institute. All rights reserved. (Restatement)

18. Restatement, Section 90 cmt. f. All rights reserved.

19. Restatement, Section 90 cmt. h(2). All rights reserved.

20. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

21. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

22. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

23. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

24. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online at https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c.

25. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-4.

26. Tibble v. Edison International, 135 S. Ct 1823 (2015).

Pingback: Who Will Tell the Plan Sponsors?: The Truth About the Looming Fiduciary Liability Trap in 401(k) and 403(b) Litigation | The Prudent Investment Fiduciary Rules

Pingback: 401(k) Litigation Trends to Watch in 2023 | The Prudent Investment Fiduciary Rules