by James W. Watkins, III, J.D., CFP®, AWMA®

I have written several posts on this blog critiquing the Sixth Circuit’s decision in Smith v. CommonSpirit Health (CommonSpirit). The decision, particularly the court’s “apples and oranges” argument is inconsistent with the both the First Circuit’s decision in Brotherston v. Putnam Investments, LLC, and the Restatement (Third) of Trust’s explicit approval of index funds for benchmarking purposes by fiduciaries. The fact that SCOTUS denied Putnam’s petition for certiorari clearly indicates that the Court agrees with both the First Circuit’s decision and the rationale behind the decision.

In retrospect, I believe the CommonSpirit decision may have done plan participants and ERISA plaintiff’s attorney a favor by opening “Pandora’s Box” as to a common issue with some 401(k)/403(b) plans and plan advisers/providers, that question being

Are plan sponsors and ERISA plaintiff’s attorneys overlooking a potentially significant breach of a plan sponsor’s fiduciary duties of loyalty and prudence?

ERISA case law is very clear that a plan sponsor’s fiduciary duties extend to the selection and monitoring of a plan’s plan advisers and providers.

[W]here the trustees lack the requisite knowledge, experience and expertise to make the necessary decisions with respect to investments, their fiduciary obligations require them to hire independent professional advisors….1

Failure to utilize due care in selecting and monitoring a fund’s service providers constitutes a breach of a trustees’ fiduciary duty. At the very least, trustees have an obligation to (i) determine the needs of a fund’s participants, (ii) review the services provided and fees charged by a number of different providers and (iii) select the provider whose service level, quality and fees best matches the fund’s needs and financial situation. Trustees also have an ongoing obligation to monitor the fees charged and services provided by service providers with whom a fund has an agreement, to ensure that renewal of such agreements is in the best interest of the fund.2

In the recent CommonSpirit decision, it appears that that very issue was never raised by plaintiff’s attorney. The issue may have been raised implicitly or collaterally in addressing other alleged fiduciary breaches. To be honest, I do not even remember a case where that specific issue was raised as a separate fiduciary breach by a plan sponsor.

I believe the timing is right to address the following question: Does a plan sponsor breach their fiduciary duties of loyalty and prudence if they select and/or maintain a plan adviser and/or provider who is affiliated with an investment company that offers various investment products for a 401(k)/403(b) plan, but the investment company does not make available all of its investment products to such plans, effectively forcing them to settle for less prudent investment products in order to financially benefit the investment company and/or the plan adviser/provider

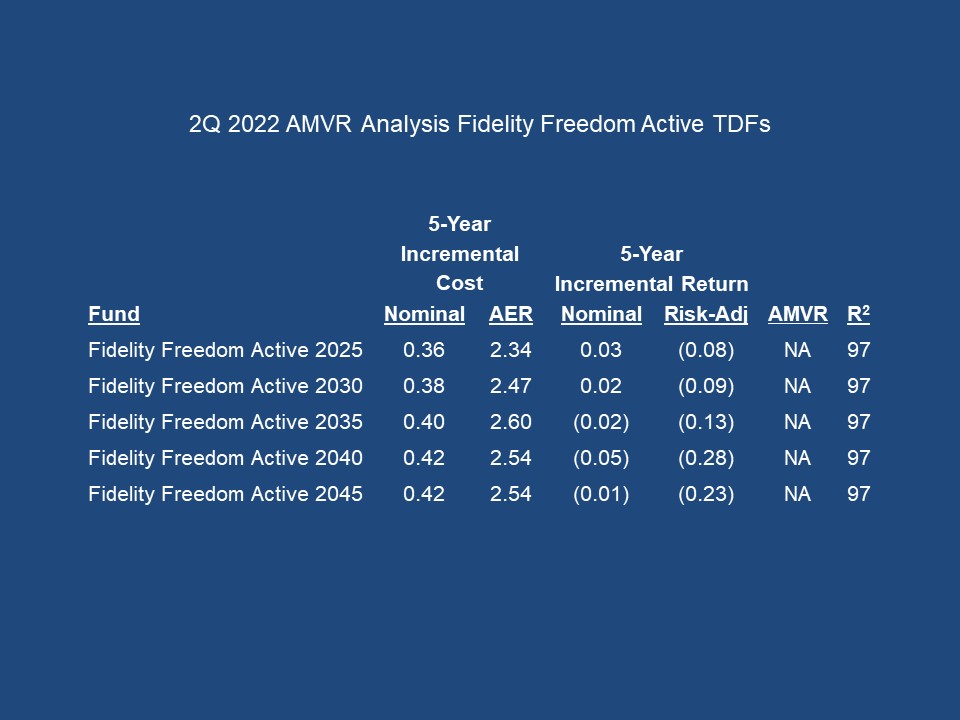

In CommonSpirit, the primary issue involved the plan’s choice of the active suite of Fidelity Freedom TDF funds. A forensic analysis comparing the active suite of the Fidelity Freedom 2035 TDF to the comparable index version of the same fund is shown below. InvestSense’s proprietary metric, the Active Management Value Ratio (AMVR), was used to perform the forensic analysis.

The combination of underperformance relative to the index version and the incremental cost, with no commensurate return at all, would indicate that the active suite version is cost-inefficient relative to the index version of the fund and, thus, imprudent.

And yet, the plan sponsor chose and continued to offer the active suite of Fidelity Freedom TDFs within the plan. Based on the discussion within the decision, Fidelity may not make the index version of the Fidelity Freedom TDFs available to 401(k) or 403(b) plans.

A similar AMVR analysis of several of the other active suite Fidelity Freedom TDFs suggests that the funds analyzed are also imprudent based on cost-inefficiency.

The results shown on the two slides raise obvious questions with regard to possible fiduciary breaches by the CommonSpirit plan sponsor and other plan fiduciaries. Even if Fidelity does not allow the Fidelity Freedom index funds within 401(k) plans, that would not excuse a plan sponsor ignoring the findings from the AMVR forensic analyses. Fidelity clearly had more prudent investment options available. Fidelity apparently simply chose not to offer them to CommonSpirit to financially benefit their own investment company.

As SCOTUS stated in its Northwestern University decision, each individual investment option must be prudent. A plan sponsor has an ongoing duty to monitor all investment options offered within its plan and promptly remove any imprudent option.

Fidelity’s Contrafund fund (Contrafund) has long been one of Fidelity bellwether funds, both in retail accounts and pension plans. Of note, Morningstar recently downgraded the fund.

Fidelity created a series of index funds to compete with Vanguard’s popular index funds. Fidelity’s index funds have proven to be a true competitor to Vanguard’s index funds, both in terms of price and performance.

Morningstar rates Contrafund as a large cap growth (LCG) fund. Fidelity offers a comparable LCG index fund. Using the AMVR metric, a forensic analysis comparing the two LCG Fidelity funds provided some interesting results.

Once again, the actively managed Fidelity fund proved to be imprudent relative to a comparable Fidelity index fund. Keep in mind, in assessing the damages of a fiduciary breach, the underperformance of an actively managed fund is properly considered as an opportunity cost. Therefore, the underperformance is combined with the incremental costs of the actively managed funds in computing potential damages resulting from a fiduciary breach.

Rethinking the Fiduciary Disclaimer Clause

During my fiduciary audits of 401(k) and 403(b) plans, I always review the plan’s advisory contract. More often than not, I find that the plan advisor has inserted a fiduciary disclaimer clause in the contract. As a result, the plan advisor will claim that any advice and services that they provide to a plan is not required to meet the stringent fiduciary standard’s loyalty and prudence requirements.

More often than not, I find that the advice and services provided by the plan advisor has definitely not met such standards. As a result, the plan sponsor is left fully exposed for all fiduciary liability.

When I point out the fiduciary disclaimer clause in their advisory contract and its implications, the plan sponsor will quickly claim that they were not aware of such language and would never have agreed to such conditions. The challenge for plan sponsors is in detecting such language, as it rarely clearly set out.

Fiduciary disclaimer language is often buried within the advisory contract and stated in such a way as not to arouse suspicion. An example of some commonly used language is often along the line of

“Plan, plan sponsor and plan adviser hereby acknowledge and agree that plan adviser shall only provide advice to the plan and plan sponsor, and that plan and plan sponsor alone shall be responsible for making the ultimate responsibility as to whether to implement plan advisers’ advice and recommendations, in whole or in part.”

Translated – we disclaim all fiduciary responsibilities regarding the plan, plan sponsors, or any plan participants. Fiduciary disclaimer clauses are often, but not always, expressed in negative terms, what they will not provide.

People often accuse me of picking on Fidelity in connection with 401(k) and 403(b) plans. Let me be clear, Fidelity has some excellent products. In taking advantage of a fiduciary disclaimer clause to avoid any fiduciary liability by only offering 401(k) and 403(b) plans, they are simply doing what plan sponsors should be doing – protecting their best interests. That said, plan sponsors may still have recourse against plan advisers and providers. through the courts plan sponsors based on legal grounds such as breach of contract, negligence, and fraud

Liability-Driven 401(k) Plan Design

My experience has been that plan sponsors rarely consult with ERISA attorneys regarding fiduciary risk management and designing a liability-driven plan, a win-win plan that both reduces their personal risk while also ensuring a plan that genuinely promotes and protects the best interests of their plan participants.

Marcia Wagner is one of America’s top ERISA attorneys. I first heard about the liability-driven ERISA plan design concept when I read an excellent Lexis-Nexis article she co-wrote with Barry Saelkin. The article itself focused on using the liability-driven concept in selecting investments for defined benefit plans. As I read the article, I realized how perfectly the concept dovetailed with the AMVR metric in connection with defined contribution plans.

Two key points from the article regarding liability-drive plans:

(1) plan sponsors should always employ effective “de-risking” techniques and strategies to minimize the potential liability exposure they may face from selecting and monitoring investment options within a plan;

(2) plans should always hire independent and experienced outside experts to help them design, monitor and maintain an effective liability-driven plan.

Ask any experienced ERISA attorney and they will tell you that most ERISA plans will mistakenly tell you that they are ERISA compliant. Plan sponsors and plan investment committees quickly realize otherwise when I show them the results of my AMVR forensic analyses and my fiduciary prudence audit.

Plan sponsors typically ask what they could have/should have done differently. In addition to having originally designed the plan using liability-driven concepts, I usually remind them that the plan adviser/provider would have been a co-fiduciary with the same fiduciary liability responsibilities and exposure – had the plan not released them from such duties by virtue of the fiduciary disclaimer clause. The clause arguably allowed them to provide the plan with imprudent, substandard advice and services – with arguably no liability to the plan.

Going Forward

I am a firm believer in the liability-driven plan concept for fiduciary accounts, including 401(k) and 403(b) plans. Plan advisers typically emphasize the nominal returns of their recommendations, with little or no discussion of the potential risks and liabilities associated with such recommendations, e.g., excessive volatility, overall cost-inefficiency, and other unsuitability concerns. The liability-driven plan concept should be even more appealing as the number of ERISA actions continue to increase.

The bad news is that most plans have no idea just how much potential personal liability is hidden in their current plan. The good news is that it is relatively easy to design, implement and maintain a liability-driven 401(k) or 403(b) plan. Furthermore, by using liability-driven concepts to “de-risk” a 401(k)/403(b) plan, a plan can be designed to provide significant benefits for both plan sponsors (risk management and reduced potential liability exposure) and plan participants (improved investment performance).

Notes

1. Liss v. Smith, 991 F.Supp 278, 297 (S.D.N.Y. 1998).

2. Liss, 300.

© Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.