By James W. Watkins, III, J.D., CFP Board Emeritus™, AWMA®

The first quarter of 2024 produced an interesting situation, resulting in an opportunity to demonstrate both the value of the Active Management Value Ratio (AMVR) and its nuances. The Fidelity Contrafund Fund K shares (FCNKX) reduced the fund’s expense ratio, from 47 basis points (0.47) to 32 basis points (0.32). A basis point equals 1/100th of one percent.

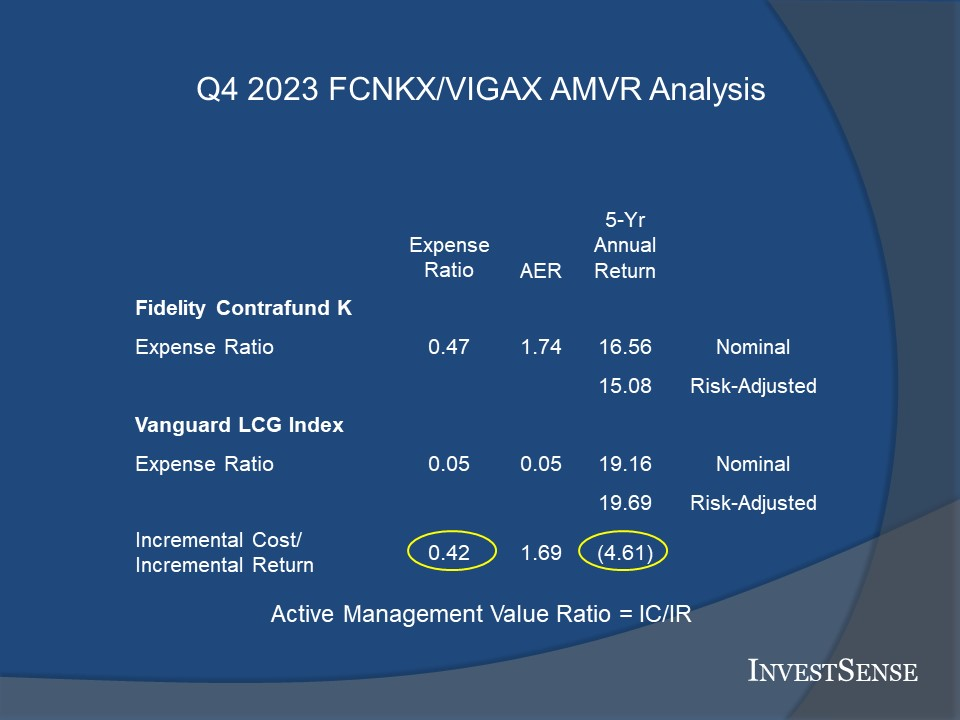

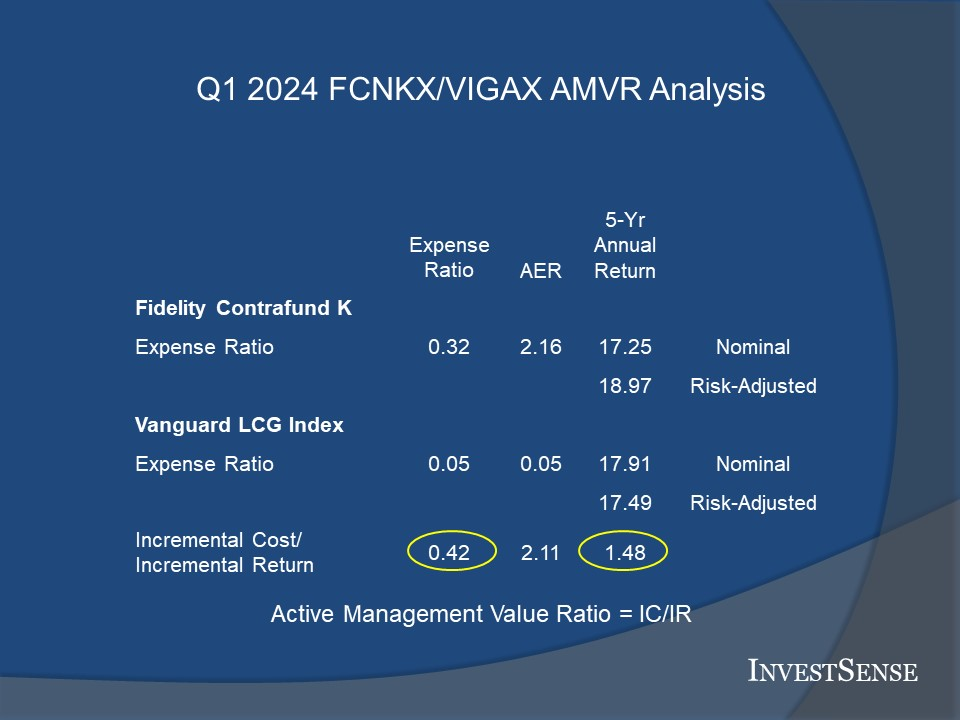

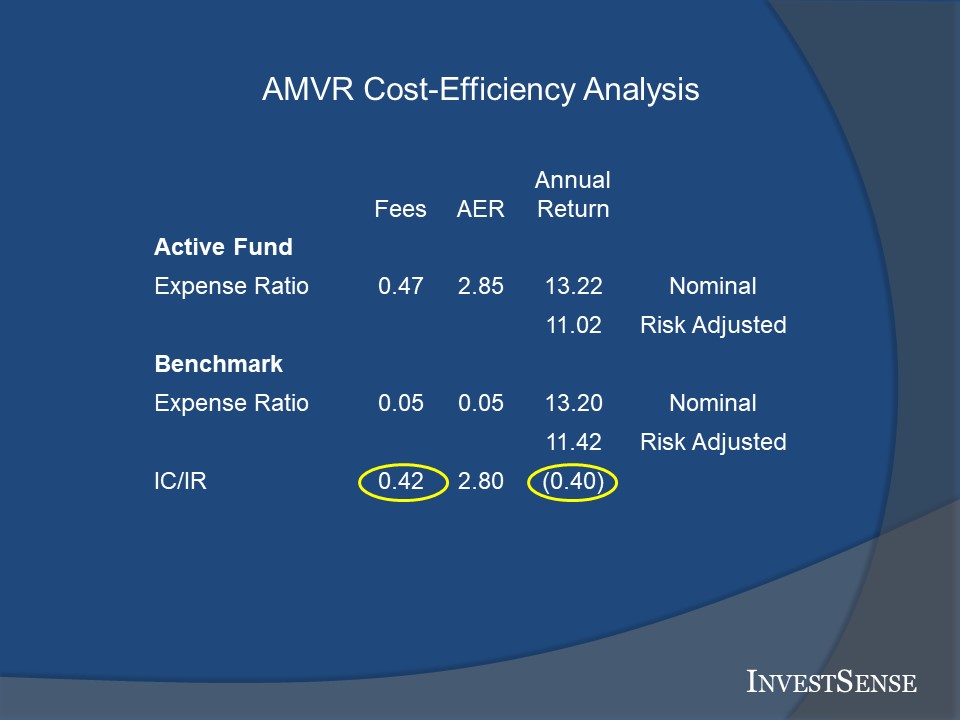

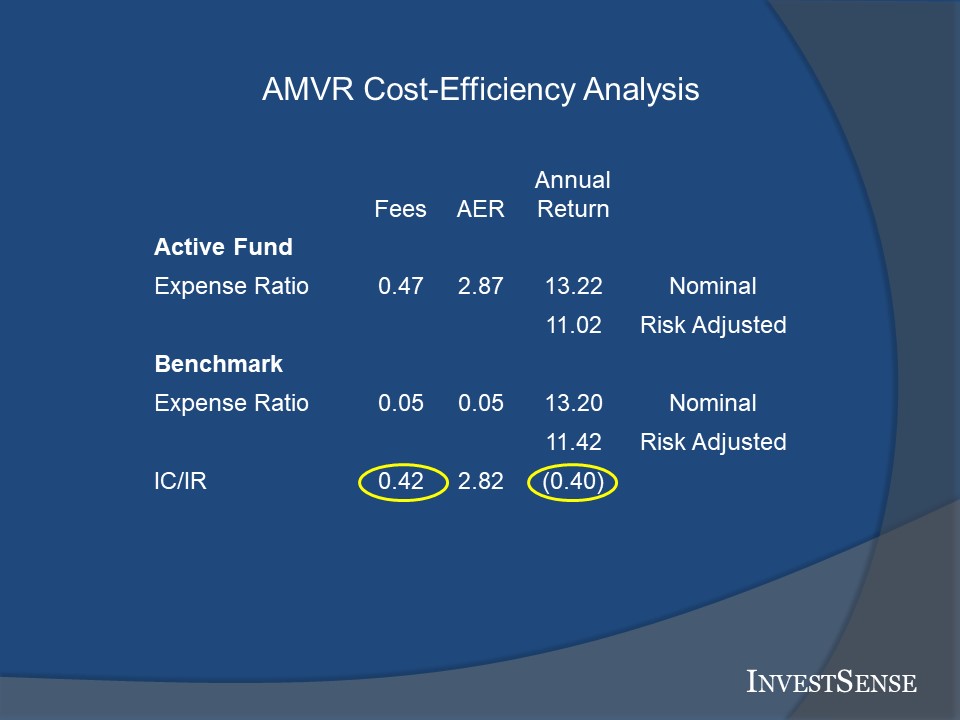

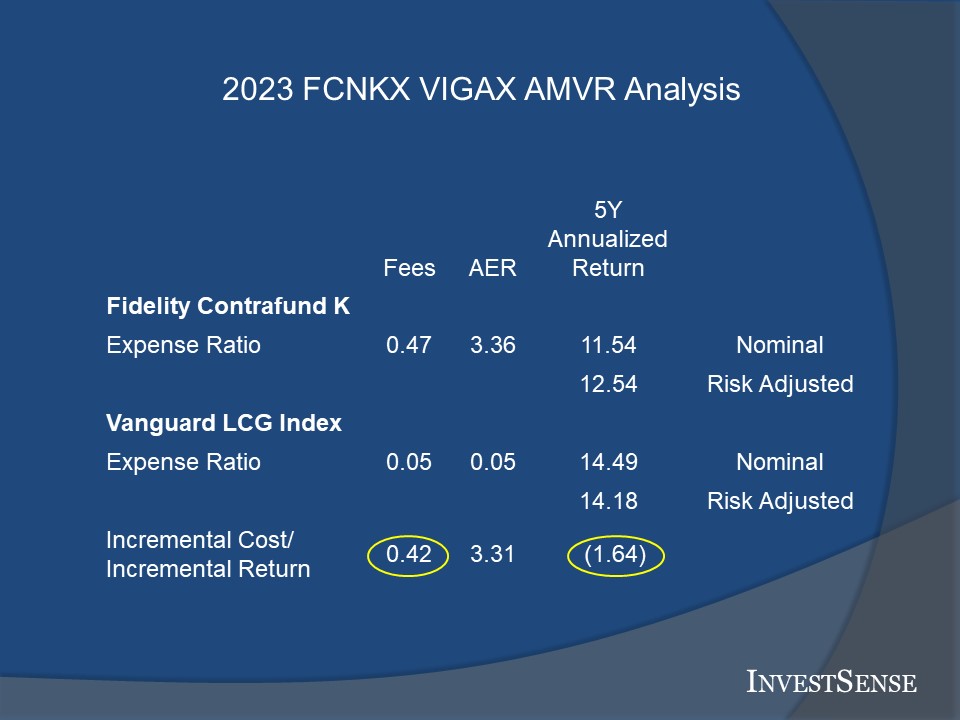

The AMVR slide below shows the results of an AMVR analysis between FCNKX and a comparable index fund, the Vanguard Large Cap Growth Index Fund Admiral shares (VIGAX), for the 5-year period ending on December 31, 2023. Shown below the Q4 2023 analysis is a 5-year AMVR analysis of the same funds, for the same five-year period ending on March 31, 2024.

My fiduciary clients immediately called and emailed me asking how to evaluate the AMVR results resulting from FCNKX’s significant reduction in its expense ratio. While such a significant reduction in a fund’s expense ratio is uncommon, the AMVR makes a new cost-efficiency analysis relatively simple.

The 2023 AMVR analysis resulted in FCNKX failing to provide a positive incremental risk-adjusted return, resulting in FCNKX failing to qualify for an AMVR score. Using Contrafund’s risk-adjusted 1Q 2024 returns resulted in FCNKX providing a positive incremental risk-adjusted return (1.48) relative to the benchmark Vanguard fund, resulting in an AMVR score of 0.18. Under the AMVR metric, a low AMVR score indicates a higher cost-efficiency rating.

However, if we recalculate those AMVR scores using Miller’s Active Expense Ratio1 (AER) and factoring in the correlation of returns between the two funds in each scenario, FCNKX would be considered cost-inefficient/imprudent relative to the benchmark Vanguard fund in both analyses.

While some investment professionals ignore the correlation, or r-squared, factor, fiduciaries who do so risk being deemed to have breached their fiduciary duties for not properly carrying out their required independent, thorough, and objective investigation and evaluation. When the returns of funds are highly correlated, an argument can be made that the actively managed fund is a “closet index” or “mirror” fund, charging higher fees based on the claim of providing active management. The higher an actively managed fund’s r-squared number, the higher the implicit expense ratio of such fund, making it less likely that the fund will pass the AMVR’s cost-efficiency standards.

In both of the scenarios provided, the correlation of returns was at or above 90 percent. As a result, the AER estimated that the actively managed fund only provided approximately 25.00 percent of active management. A strong argument can be made that a fund providing only 25.00 percent of active management hardly qualifies as an actively managed fund.

The Case for Risk-Adjusted Returns I am often asked why the AMVR uses a fund’s risk-adjusted returns. The investment industry often objects to risk-adjusted returns, parroting the industry line of “you can’t eat risk-adjusted returns.” My response is that the investment industry has no qualms about using Morningastar’s star system in advertising its products, even though Morningstar clearly states that they use risk-adjusted returns in determining their star system scores.

The Q1 2024 AMVR slide provides a perfect example of why the AMVR uses risk-adjusted returns. Risk and return are inextricably woven together. A key component in the prudence of any investment is whether the investment provides a commensurate return for the level of risk and cost assumed by an investor. In this case, using Contrafund’s risk-adjusted returns resulted in higher returns and a very favorable AMVR rating based on Contrafund’s nominal cost numbers. However, as mentioned earlier, the fund’s AMVR rating became cost-inefficient/imprudent when the fund’s correlation-adjusted costs were used in the calcuations.

Remember, when using the AMVR, the goal is a score between zero and 100. The lower the AMVR score, the higher the cost-efficiency. We also recommend that the user always prepare both a five and ten-year AMVR analysis, if possible, to evaluate possible prudence trends and/or inconsistencies.

Going Forward The two AMVR slides demonstrate the need to properly re-examine each investment in a plan on a regular basis. While the reduction in FCNKX’s expense ratio may increase the likelihood of additional positive AMVR evaluations, one period is not a sufficient period to deem a previously consistently cost-inefficient/imprudent fund under the AMVR metric suddenly a cost-efficient/prudent. The fund should be monitored interms of future performance.

While arguments can be made about the validity of the AER being factored in as part of the AMVR analysis, the key fact is that it creates a legitimate question of fact in terms of prudence and the question of “closet indexing.” As a result, it should prevent a court from dismissing the case and allow the plan participants the opportunity to have discovery to determine what process, if any, the plan sponsor used in conducting their investigation and evaluation. While the issue of “closet indexing” has not received as much attention in the U.S. as it has in other countries, the issue and the potential harm is real, as evidenced by studies such as those conducted in Canada and Australia.

Others have argued that high correlations of return, often referred to as a fund’s r-squared number, could be considered as fraud since the amount of active management an investor receives is significantly less than an investor has a right to expect from a fund holding itself as being actively managed and charging higher fees accordingly. Again, this creates a question of fact that is not proper for adjudication at the motion to dismiss stage.

These questions become even more important given the likelihood that SCOTUS may soon have the opportunity to decide which party has the burden of proof in 401(k) and 403(b) litigation. If SCOTUS decides that plan sponsors have the burden of proving that their actions did not cause the plan participants to suffer financial losses, the issues of cost-inefficiency and closet indexing could make the plan sponsor’s burden that much harder.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

By James W. Watkins, III, J.D., CFP Board Emeritus™, AWMA®

[A] fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan; and with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.1

The Department of Labor recently filed an amicus brief in the pending Home Depot 401(k) litigation. The DOL summed up a fiduciary’s duties vis-à-vis cost-consciousness perfectly, citing several provisions from the Restatement, including the following:

The judgement and diligence required of a fiduciary in deciding to offer any particular investment must include consideration of costs, among other factors, because a trustee ‘must incur only costs that are reasonable in amount and appropriate to the investment responsibilities of the trusteeship.’2

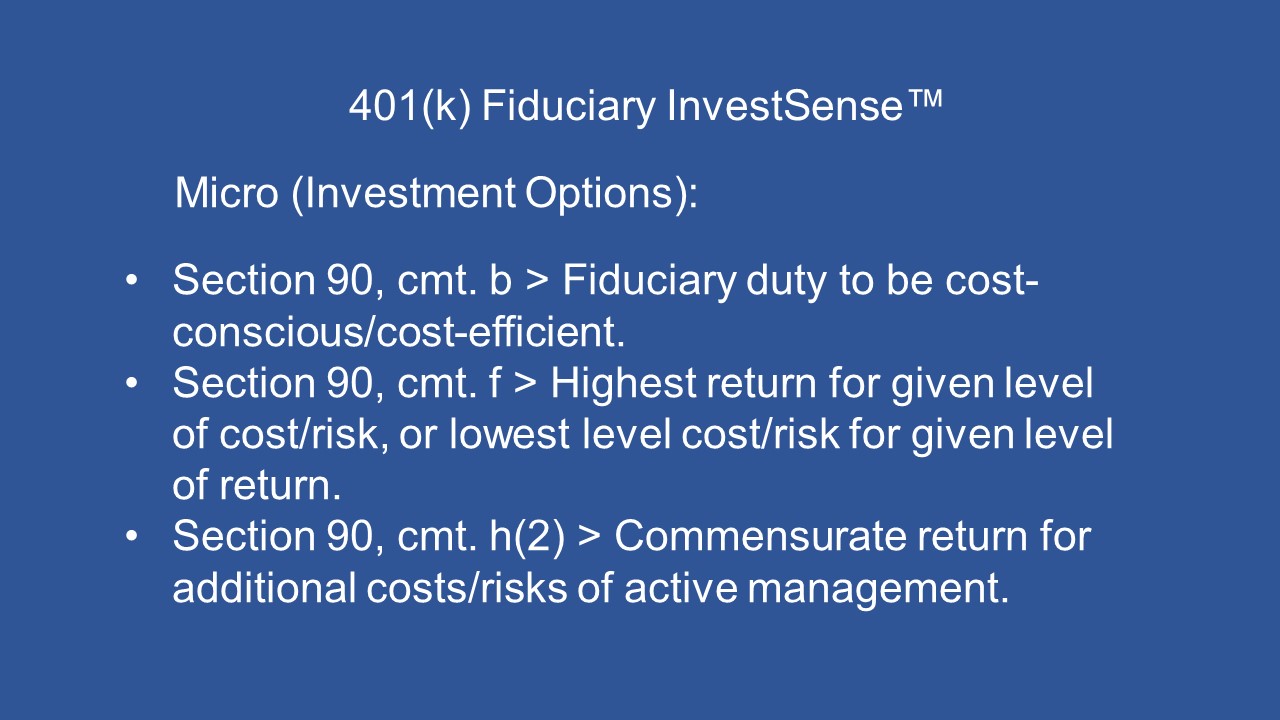

Both references emphasized the importance of reasonable costs. A fiduciary’s duty in terms of controlling costs is a consistent theme throughout the Restatement, specifically Section 90, more commonly known as the “Prudent Investor Rule.” Comments b, f, and h(2) are key sections of in understanding and interpreting Section 90:

At first glance, the issue of reasonable expenses would seem to be fairly straightforward, i.e., cost-efficiency, benefits exceed associated costs However, upon closer examination, cost issues are arguably potentially more complicated, especially in connection with more complicated investments such as annuities, which often lack the transparency of other investments. As a result, plan sponsors may mistakenly believe they understand an investment and its costs, while closer examination often reveals issues they had not initially considered.

In his classic, “Winning the Loser’s Game,”3 investment icon Charles D. Ellis discusses various alternative ways of interpreting fees and other costs. Ellis argues that the proper way to measure or describe fees is not as a percentage of assets since customers bring the assets with them when they invest.

Ellis argues that fees should be based and evaluated on a value-added basis using the returns provided by the investment manager. Ellis provides several examples to demonstrate how using a value-added approach provides a significantly different picture in terms of fiduciary prudence.

Ellis addresses the common “only 1 percent” fee argument. However, if the expected or actual return is 7 percent, Ellis argues that the effective fee would be approximately 14 percent (1/7), not 1 percent.4

I have seen several articles recently about the annuity industry’s planned campaign to increase the use of annuities in pension plans, specifically in the form of in-plan annuities and as components in target date funds. I have consistently advised plan sponsors and other investment fiduciaries to completely avoid offering or using annuities based upon both the fact that neither ERISA and fiduciary law require them to do so, and the fact that annuities present legitimate potential fiduciary liability “traps” for investment fiduciaries.

Ellis’ value-added proposition is equally applicable to annuities. The combination of value-added analysis and “humble arithmetic provide yet another reason for plan sponsors to totally avoid annuities and the potential of unnecessary fiduciary risk liability exposure.

Annuities often impose restrictions such as cap rates and/or participation rates on the amount of annual return that the annuity owner can receive. Annuities often further reduce the annuity owner’s realized return by imposing “spreads” on the owner’s return. Spreads are totally subjective and determined unilaterally by the annuity owner.

The combination of caps rates, participation rates, and spreads often results in significantly lower returns than annuity owners were led to believe they would receive when an annuity were recommended as a means of earning “guaranteed” retirement income. This is one reason that annuities are typically in the top ten of investor complaints to regulators.

A simple example will help explain the potential fiduciary liability issues for plan sponsors who offer annuities in their plans. A common annual cap rate in annuities seems to be 10 percent. This means that whatever return the annuity issuer is able to produce, the annuity owner’s realized return is limited to just 10 percent.

The annuity owner’s realized return is then further reduced by whatever spread amount the annuity issuer decides to apply. Annuity owners are often not aware of the actual amount of spread that is applied, as annuity issuer’s often embed, or “hide,” the actual amount of the spread as part of the annuity’s pricing.

Assume a scenario involving an annuity with an annual cap rate of 10 percent and a spread of 1-2 percent. A spread of 2 percent would further reduce the annuity owner’s realized return to just 8 percent.

The potential liability issue here for a plan spsonsor is that a legitimate argument can be made that inclusion of an annuity which could produce the described scenario could result in litigation alleging a breach of the plan sponsor’s fiduciary duty of prudence. While the annuity issuer may claim that they only applied a spread of 2 percent, “humble arithmetic” paints a different picture.

Since the annuity owner’s realized returns were limited by the 10 percent cap, the argument can be made that using Ellis’ value-added proposition, the effective spread or fee/cost is effectively 20 percent instead of 2 percent.

I believe a plan sponsor would have a hard time proving the prudence of a 20 percent spread/fee/cost in connection with any investment option given the number of more cost-efficient alternatives available in the market. As I have argued in other posts, including here and here, annuities simply do not make sense from a fiduciary risk management perspective, especially when there is no legal obligation to offer them with a pension plan.

Viewed objectively, most annuities ultimately fall victim to Supreme Court Justice Louis D. Brandeis referred to as “the relentless rules of humble arithmetic.”5 Neither ERISA nor basic fiduciary law expressly require a plan spsonsor to offer any specific category of investments, e.g., annuities, actively managed mutual funds, in order to be ERISA-compliant. Prudent plan sponsors do not expose themselves to unnecessary liability risk exposure.

Notes 1. 29 U.S.C.A. Section 404a; 29 C.F.R Section 2550.404a-1(a), (b)(i) and (b)(ii). 2. Amicus Brief of the Department of Labor in Pizarro v. Home Depot, Inc., No. 22-13643 (11th Cir. 2022). (DOL Amicus Brief) 3. Charles D. Ellis, “Winning the Loser’s Game: Timeless Strategies for Successful Investing,” 8th Ed., (2021). 4. Ibid, 172. 5. Louis D. Brandeis, “Other People’s Money and How the Banks Use It,” (1914)

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

By James W. Watkins, III, J.D., CFP Board Emeritus™, AWMA®

My decision to transition into fiduciary risk management was based largely on my love of the law and psychology. My minor in college was psychology, with a focus on cognitive behavior and decision-making.

The idea of combining behavioral psychology with fiduciary law came about largely as a result of Annie Duke’s excellent book, “Thinking in Bets.”1 While many know Dukes from her days a poker champion, she has a doctorate in behavioral psychology and provides seminars and consulting services on the topic of decision-making.

I am admittedly a psychology “geek.” That said, I could not put Duke’s book down due to the way she effectively combines technical psychology concepts with simple common sense. My immediate thought was that this is something that plan sponsors and other investment fiduciaries should consider to reduce their potential liability exposure and improve their overall effectiveness.

Duke’s basic argument is that far too often society incorrectly evaluates the quality of a decision based on the ultimate results rather than on the quality of the decision-making process that was used in making the decision. This focus on quality of process instead of results is the same standard that is used in ERISA litigation.

Based on my experience from working with investment fiduciaries, this is often the biggest bet, aka mistake, investment fiduciaries make, whether they realize it or not. Far too often product salespeople play “head games,” putting ideas in the heads of fiduciaries as part of a sales spiel, ideas that are often inconsistent with a plan sponsor’s duties and obligations under ERISA, thereby increasing a plan sponsor’s potential liability exposure.

One of the biggest challenges I face with new clients is de-programming them from such marketing spiels and bringing their actions in line with ERISA’s standards. Fortunately, developing an ERISA-compliant decision-making process is relatively simple once the fiduciary understands the importance of “controlling the controllables” as part of a prudent fiduciary process.

As Duke points out, evaluating decisions based purely on results is flawed in that often results are influenced by factors which are beyond anyone’s control. Fiduciaries should be evaluated on their ability to control the controllable.

THE Question I recently read an article on the annuity industry’s plans for marketing annuities and other “guaranteed income” products to 401(k) plans. In a ranking of the most common reasons why plan sponsors said they might consider adding ”guaranteed income” products and strategies, the number one response was that employers felt an obligation to provide employees with a means of generating additional income.

That is why the first question I always ask a potential fiduciary client is “what do you believe your fiduciary responsibilities require you to do?” The answers typically involve ensuring “retirement readiness” and/or ensuring a certain level of return. When I explain the importance of process over return in terms of ERISA compliance and potential liability exposure, my job becomes that much easier.

I go over the actual language of ERISA Section 404(a)2 and 404(c)3 and explain how to effectively address the potential compliance/liability issues under both sections. Nowhere in either section does ERISA require a plan sponsor to include annuities, actively managed mutual funds, or any other specific type of investment product or strategy.

Other than section 404(c)’s requirement that a plan offer a minimum of three broadly diversified investment options, neither section requires a plan to offer a minimum number of investment options. After SCOTUS’s Hughes decision4, a valid argument can be made that less is more, that each additional investment option offered within a plan potentially raises the likelihood of a fiduciary breach due to the inclusion of an imprudent investment option. And yet, we continue to see plans offering 15-20, or more, investment options, many of which are cost-inefficient and, thus, imprudent

As the annuity industry tries to convince more plans to include annuities and other guaranteed income products into their plans, I point out that Section 404(a) includes language requiring a plan to always act in the best interest of both the plan participant and their beneficiaries. (emphasis added)

I am still waiting for someone to truthfully explain to me how a product is in the best interests of a plan participant and their beneficiaries when that product requires the annuity owner to

surrender ownership of the annuity contract and the accumulated value to the annuity issuer in order to receive the contractual alleged, with no guarantee of the investor receiving a commensurate return,

incur excessive, and often counterintuitive, fees, potentially reducing an investor’s end-return by one-third or more, and

forego any estate plans of providing any remainder interests for one’s heirs.

I have previously stated my position with regard to annuities in ERISA plans:

To the extent that an annuity requires the annuity owner to surrender ownership of the annuity contract and conrol of the accumulated value of the annuity to receive the alleged benefit promised by the annuity, with no guarantee of the annuity owner even breaking even/receiving a commensurate return, and the terms of the annuity contract written in such a way as to essentially ensure that the annuity issuer and/or other third parties will reap a windfall at the annuity owners expense, such an annuity is a breach of an investment fiduciary’s duties of loyalty and prudence.

Betting on Actively Managed Mutual Funds Most 401(k) and 403(b) plans are still dominated by actively managed funds. Studies have consistently shown that the overwhelmingl majority of actively managed funds are imprident under fiducairy law since they are cost-inefficient, with some not being able to even cover their costs.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.5

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.6

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.7

I teach my clients how to use a metric that I created, the Active Management Value RatioTM (AMVR). The AMVR allows investment fiduciaries, attorneys, and investors to quickly calculate the cost-efficiency of an actively managed mutual fund realtive to a comparable index fund. The AMVR is based on the research of investment icons, including Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel.

The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.8

So, the incremental fees for an actively managed mutual fund realtive to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that the incremental fees for active management are really, really high – on average, over 100% of incremental returns.9

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.10

A sample AMVR analysis is shown below. The beauty of the AMVR is its simplicity. In interpreting a fund’s AMVR scores, an attorney, fiduciary or investor must only answer two simple questions:

Does the actively managed mutual fund produce a positive incremental return?

If so, does the fund’s incremental return exceed its incremental cost?

If the answer to either of these questions is “no,” then the fund does not qualify as cost-efficient under the Restatement’s guidelines.

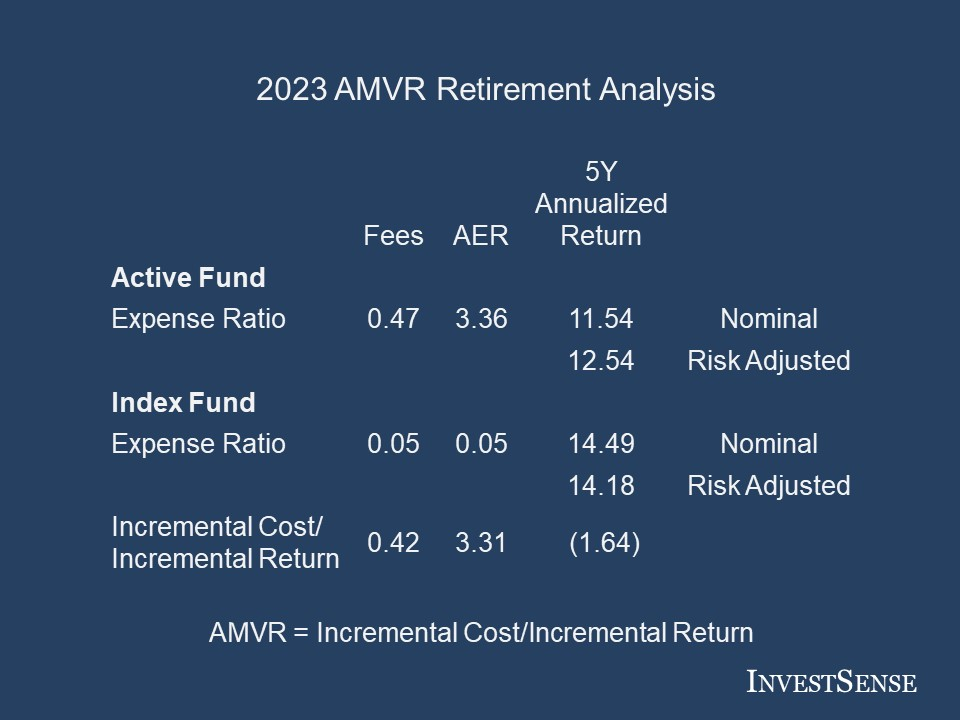

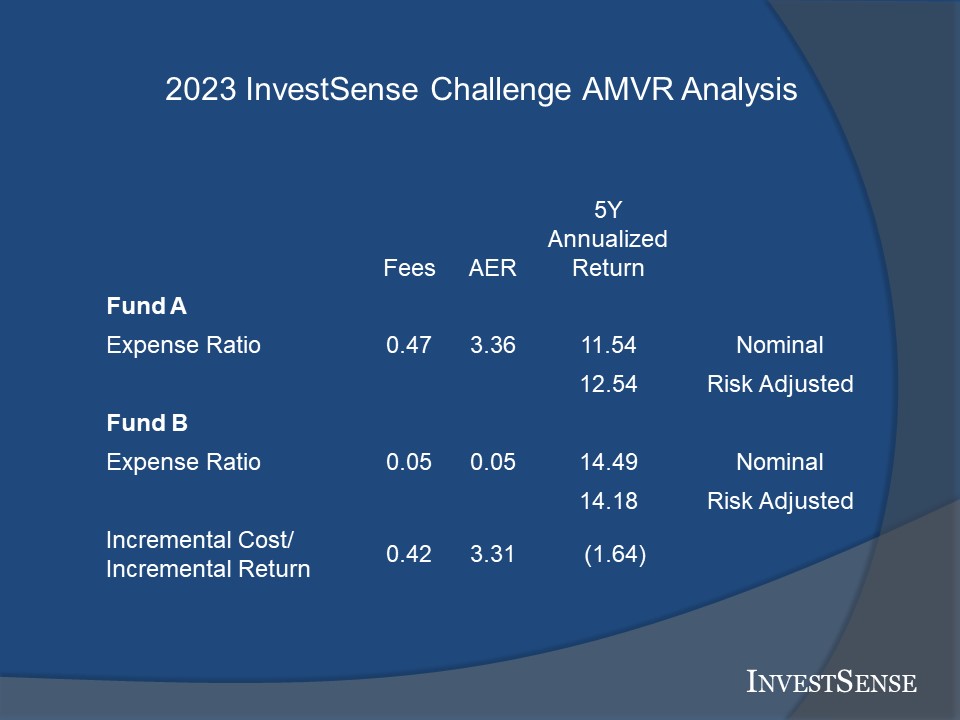

The AMVR slide shown above is a cost/benefit analysis comparing the retirement shares of two popular large cap growth mutual funds, one an actively managed fund, the other an index fund.

The AMVR slide shows that the actively managed fund’s incremental costs (42 basis points) exceed the fund’s incremental returns, which are negative. Therefore, an investor in the actively managed fund paid a fee and received absolutely no corresponding benefit. (A basis point equals 1/100th of one percent.} Since costs exceed returns, this results in the actively managed fund being cost-inefficient relative to the index fund for the time period studied. If we analyze the incremental costs of the actively managed fund using Miller’s Active Expense Ratio, which factors in the correlation between two funds. the cost-inefficiency increases over 700 percent (42 basis points to 331 basis points)

It is important that investment fiduciaries remember that both returns and costs compound over time. The Securities and Exchange Commission and the General Accountability Office have both found that each additional 1 percent in costs/fees reduces an investor’s end-return by approximately 17 percent over a twenty year period.11

Using the nominal/publicly stated data, if we treat the incremental underperformance of the actively managed fund as an opportunity cost, and combine that number with the incremental costs, based on the fund’s stated expense ratio, the projected loss in end-return would be approximately 35 percent, 2.06 basis points times 17.

But does the nominal/stated cost version of the AMVR actually reflect the costs incurred by plan participants if the actively managed fund is selected within a plan?

The Active Expense RatioTM There are somepeople, myself included, that feel that an actively managed fund’s stated expense ratio does not accurately reflect the implicit cost of an actively managed costs. Fortunately, Ross Miller introduced a metric, the Active Expense Ratio (AER), which allows fiduciaries and investors to calculate both the amount of acrtive management provided by an actively managed fund and the implicit costs of such active management. Miller explains the importance of the AER as follows:

“Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark indexs.”12

In the AMVR example shown, using nothing more than just the actively managed fund’s r-squared/correlation of returns number and its incremental cost, the AER estimates the actively managed fund’s implicit expense ratio to be 3.36, resulting in incremental correlation-adjusted expense ratio/costs of 3.31. Combined with the actively managed fund’s underperformance, and using the DOL’s and GAO’s findings, that would result in a projected loss in end-return of approximately 84 percent over a twenty year period.

So, combining behavioral psychology and the law of fiduciary prudence, which is the better bet for a plan, the actively managed fund or the comparable index fund?

Betting on Annuities In my first draft of this post, I had prepared a detailed analysis of both the various types of annuities and the inherent potential fiduciary liability issues. A colleague reminded me that I had already done numerous posts addressing such issues on my blogs, such as here, here, and here. My colleague suggested that I keep this post simple by using my standard response to advocates for annuities in pension plans – ERISA does not require that a plan sponsor offer an annuity, in any form, within an ERISA plan.

I often get calls and emails from clients and non-clients telling me that the plan adviser or a sales consultant has shown them articles or sales literature indicating that plan participants want some type of product that guarantees them income, preferably for life. As I recently posted, my response is, and always will be the following:

“A plan sponsor’s fiduciary reality is defined by ERISA and the Restatement of Trusts, not by what plan participants allegedly want or what plan advisersand/or consultants may recommend.

I also share my legal experiences with the annuity industry with regard to their polls and research. When legal actions involve potentially large damage awards, the insurance company usually requests that the court require that the injured plaintiff accept an annuity as a large part of the terms of any settlement The annuity industry based such demand on alleged research that showed that over 90 percent of plaintiffs quickly dissipated settlement funds.

The annuity industry engaged in this type of intentional misrepresentation in legal actions for years. Finally, when pressured about the source of their alleged research, the annuity industry admitted there was no such reseach, that the annuity industry had simply made it up.13 This is why plan sponsors and other investment fiduciaries should always consider the source when the annuity industry, or any other industry, announces self-serving results from alleged studies and polls.

As I tell my fiduciary clients, if annuities is the answer, you are asking the wrong question. Or, as one of my financial planning colleagues says, “annuities are always your fifth best option.”

Once again, plan sponsors have no legal, moral, or any other type of obligation to offer annuities, in any form, within an ERISA plan. Plan participants interested in annuities are free to purchase one outside of the plan, without subjecting the plan sponsor to potential liability.

Going Forward At the beginning of this post, I stated that the biggest bet that plan sponsors and other investment fiduciaries often make is not knowing and understandoing what their fiduciary duties do and do not require them to do. Hopefully, the examples provided herein have convinced plan sponsors of the value of objectively researching all investments being considered by their plan.

The idea of thinking in bets in connection with fiduciary prudence goes beyond just evaluating potential investment option within a plan. I advise my plan sponsor clients to use three simple questions, my proprietary “Why Go There” tool, in connection with any fiduciary decision:

Does ERISA explicitly require a plan sponsor to take or not to take the action?

Would or could the action result in potential liability exposure?

If the action is required by ERISA, is there a more effective option that would/could reduce any potential liability exposure?

I continue to see plan sponsors who agree to advisory contracts that include a fiduciary disclaimer clause. A fiduciary disclaimer clause is a provision that provides that the plan adviser assumes no fiduciary responsibility and/or liability in connection with any and all services and recommendations that the plan adviser provides to the plan. There are ERISA attorneys, myself included, that argue that a plan sponsor who agrees to the inclusion of a fiduciary disclaimer clause in the plan’s advisory contract has breached their fiduciary duties of loyalty and prudence.

My position is that a fiduciary disclaimer clause is essentially an admission that the plan adviser has no confidence in its intended advice and/or product recommendations. Otherwise, why insert such a clause that protects the best interest of the plan adviser at the cost of the plan sponsor and the plan participants? If the plan advisor has no faith in their own products and recommendations, why should the plan sponsor have any faith in the plan advisor. Common sense alone should tell you that plan advisers who insist on fiduciary disclaimer clauses are a bad bet.

As I mentioned ealier, I advise my clients to always require a plan adviser and any consultants to (1) agree, in writing, that they will be serving in a fiduciary capacity, with all relative duties and obligations, and (2) that they will provide written documentation providing a breakeven analysis on all products and/or strategies recommended to the plan, including an AMVR analysis on all actively managed mutual funds, using the AMVR format provided herein, with no alleged “improvements.” Be sure that your contract has language providing any and all such breakeven analyses are automatically incorporated into the original advisory contract or, in the alternative, that the original advisory contract is amended to add such a provision.

Fair warning, my experience has been that most plan advisers and consultants refuse to provide such documentation since they know the true quality of the advice they are providing and the potential liability involved. At the same time, I think TIAA-CREF summed up a plan sponsor’s legal obligations in selecting and monitoring plan advisory personnel perfectly when it stated that a plan sponsor has an obligation to look beyond prices and objectively and accurately determine the value being provided to a plan by such parties.14

NOTES 1. Annie Duke, “Thinking in Bets: Making Smarter Decisions When You Don’t Have All the Facts,” (Penguin Books: 2019) 2. 29 C.F.R. § 2550.404(a); 29 U.S.C. § 1104(a). 3. 29 C.F.R. § 2550.404(c); 29 U.S.C. § 1104(c). 4. Hughes v. Northwestern University., 142 S. Ct. 737, 211 L. Ed. 2d 558 (2022) 5. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 6. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 7. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 8. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm. 9. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 10. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 11. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study). 12. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926. 13. Jeremy Babener, “Structured Settlements and Single-Claimant Qualified Settlement Funds: Regfulating in Accordance With Structured Settlement History,” New York University Journal of Legislation and Public Policy, Vol . 13, 1 (March 2010) 14. https://www.tiaa.org/public/pdf/performance/ReasonablenessoffeesWP_Final.pdf.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

The courts have consistently recognized the inherent conflict of interest that exists in the investment industry between investment advisers/consult and clients:

“In this conflict of interest, the law wisely interposes. It acts not on the possibility, that, in some cases, the sense of that duty may prevail over the motives of self-interest, but it provides against the probability in many cases, and the danger in all cases, that the dictates of self-interest will exercise a predominant influence, and supersede that of duty.”1

In his new book, “Investing in U.S. Financial History: Understanding the Past to Forecast the Future,” Mark Higgins addresses the issue of investment consultants and conflicts-of-interest. Prior to publication, Higgins was kind enough to allow me to review the chapter that addresses such inherent conflicts of interest, He correctly identifies the basic problem with investment consultants, namely overstating their value propositions, with “[t]he inevitable outcome [being] subpar preformance and higher fees,”, in other words, cost-inefficiency.2

Higgins reportedly spent over four years researching his book, as evidenced by the fifty pages of footnotes. His book is an incredible resource for the financial services industry, investment advisers, attorneys, and investors in general.

The Devil Is In the Details As a fiduciary risk management consultant, part of my services includes educating my clients on the potential fiducairy liability issues resulting from conflicted investment advice and how to detect such tainted advice. Fortunately, the Active Management Value RatioTM (AMVR) metric makes it relatively easy to detect and address such conflicted advice.

The AMVR is based on the investment research and concepts of investment icons such as Charles D. Ellis and Nobel laureate Dr. William F. Sharpe. The AMVR allows investment fiduciaries to follow the Restatement (Third) of Trusts’ standards by evaluating the prudence of an actively managed fund in terms of commensurate return relative to the increased costs and risks commonly associated with actively managed funds.

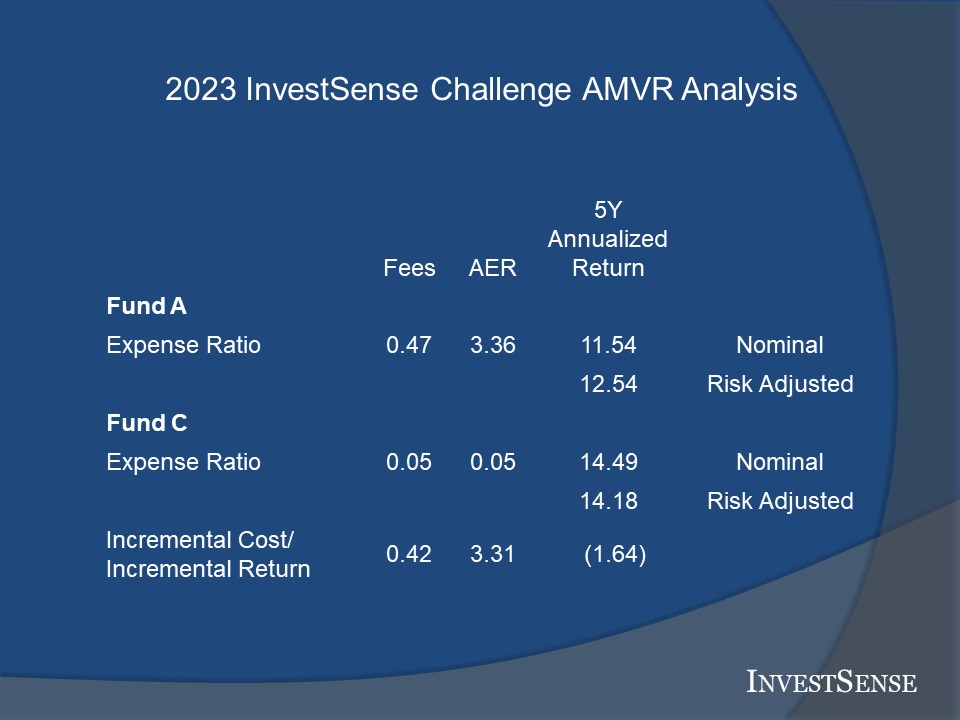

Dr. Sharpe is on record as saying the best way to evaluate the performance of an actively managed mutual fund is to compare the active fund to a comparable index fund.3 The sample AMVR slide shown here is a good example of conflicte advice, as it compares two Fidelity large cap growth funds, the K shares of the popular Fidelity Contrafund Fund (Contrafund) and the shares of Fidelity’s Large Cap Growth Index Fund (LCG). The slide demonstrates how the AMVR provides several methods of detecting potentially conflicted advice.

1. A basic cost/benefit analysis shows that the Contrafund underperformed the LCG fund and resulted in excess costs of approximately 43 basis points. (A basis point is equal to 1/100th of 1 percent.)

2. Actively managed mutual funds typically combine the fees for active and passive management, making it difficult for investment fiduciaries and investors to determine the cost-efficiency of the active management component of the fund.

Ross Miller’s Active Expense Ratio4 provides a means for investment fiduciaries to separate the two fees and to determine the implicit cost of the active management component. In this case, the AMVR indicates that the implicit cost of the fund’s active management component is 3.48, over 7 times greater than the fund’s stated expense ratio.

3. Using InvestSense’s proprietary Fiduciary Prudence RatioTM (FPR) , Contrafund’s FPR score would be zero since the FPR’s numerator is the positive incremental return provided by an the actively managed fund. Contrafund underperformed the benchmark LCG fund, resulting in Contrafund’s FPR score of zero relative to the benchmark.

It should be noted that Fidelity reportedly does not make the LCG index fund available to pension plans. My guess is that they fear that the LCG fund would essentially cannibalize the Contrafund given the LCG fund’s superior performance and lower fees.

The fiduciary risk maangement point here is that Fidelity has no obligation to make the LCG fund available to pension plans. However, plan advisers and other investment consultants providing services and/or advice to pensions plans in a fiduciary capacity do have an obligation to pension plans to properly investigate their recommendations and only recommend those funds that are cost-efficient and otherwise legally prudent under all applicable laws and regulations.

The fact that the LCG index fund is not made available in no way justifies a breach of one’s fiduciary duties of loyalty and prudence by recommending a legally questionable second choice. Despite what the investment industry may want you to believe, a cost-inefficient mutual fund is never a legally acceptable “choice.”

Annuities, Conflicted Advice, and Breakeven Analysis Conflicted investment advice is normally thought of in terms of advice which promotes the investment adviser’s best interests ahead of those of the investor. Since plan sponsors and other investment fiduciaries must satisfy their fiduciary duties of loyalty and prudence,

Breakeven analysis is especially effective in exposing conflicted annuity advice. Annuity advocates constantly use the marketing line of “guaranteed income for life.” Before even considering any type of an annuity, an investment fiduciary’s response to such marketing should always be “at what cost?” Breakeven analysis is an effective method of answering that question and exposing conflicted advice.

Shown below is an example of the sort of breakeven analysis plaintiff attorneys often use in cases involving catastrophic injuries and significant damages. The insurers and their defense attorneys often propose the use of annuities in such cases to prevent the insurer from having to payout a very large sum at one time.

When I first posted this analysis, I included similar analyses using interest rates of 4 and 6 percent. A mistake that insurance advocates make when presenting such breakeven analyses is to forget to discount the value of the annuity in terms of both present value and mortality risk. Mortality risk addresses the odds that the annuity owner will even be alive to receive the annuity’s annual payment. As the chart shows, factoring in mortality risk has a significant impact of when, or if, an annuity owner will even break even.

However, the conflict of interest issues and the insurer’s intentional fraudulent conduct was finally exposed when they were challenged by the plaintiff and the court as to the source of their statistics. The insurer admitted that they had lied, that there was not, and never had been, any studies substantiating their rapid dissipation claim.5

Similarly, current advocates for annuities based on the “guaranteed income for life” mantra try to avoid discussing the potential liability risk management topics that investment fiduciaries should focus on – breakeven analysis and commensurate return. More often than not, a breakeven analysis reveals that the odds are against an investor in such products breaking even and receiving a commensurate return, due primarily to the underlying design of and excessive fees commonly associated with such products.

The chart shown above is a “pure insurance” analysis. When I first published the chart online, some annuity advocates immediately pointed this fact out, claiming that current securities-related annuities provide a better and fairer return. But do they?

Conflicts of Interest, Framing, and Bayesian Theory “Framing” refers to the manner in which a question or product is presented, often with the goal of ensuring a certain response For instance, “would you like to receive guaranteed income for life?” Who wouldn’t?

Investment fiduciaries must always factor in fiduciary duties and potential fiduciary liability exposure. As a result, I suggest more appropriate, realistic and liability-driven ways of framing the “guaranteed income for life” question. For example, I often frame the value of a variable annuity as follows:

A variable annuity can provide a stream of income for life. However, in order to receive such benefit you will be required to annuitize your variable annuity, to surrender ownership and control of the annuity contract, as well as the accumulated value of the annuity itself, with no guarantee that you will ever receive a commensurate return on your investment.

While a variable annuity usually provides a death benefit in the event that, at the time of your death, you have not anuitized your variable annuity and the value of the annuity is less than your your actual investment in the annuity. The death benefit is not free. You will be charged an annual fee, a so-called mortality fee, to supposedly cover the annuity issuer’s cost of covering their potential liability under the death benefit. However, many annuity issuer’s base their annual mortaility fee calculations on the current accumulated value of the variable annuity rather than their actual legal/contractual death benefit liability, which, again, is typically limited to the owner’s actual contributions to the annuity, a figure which is typically significantly less that the variable annuity accumulated value as a result of the returns earned via the variable annuity’s subaccounts.

This practice of basing the annual mortality fee on the annuity’s accumulated value, commonly known as inverse pricing, often produces a signnificant windfall for the annuity issuer at the annuity owner’s expense. If an investment fiduciary is involved in the ecommendation and/or sale of a variable annuiy that uses inverse pricing, many consider this a clear violation of the fiduciary duties of loyalty and prudence.

One additional thing that variable annuity advocates often fail to mention with reagrd to variable annuities is that the investment subaccounts offered within a variable annuity are often actively managed mutual funds, perhaps even proprietary mutual funds of the annuity issuer and/or an affiliated subsidiary. Research has consistently shown that actively manged mutual funds are overwhelingly cost-inefficient, meaning they consistently underperform and charge higher fees than comparable index funds.

Still want to provide variable annuities within your defined contribution plan?

The framing example I just provided is an example of what is known as the Bayesian Theory. Bayesian theory suggests that the odds of making a correct decision increase with each relevant and accurate piece of information provided to the decision-maker. The framing example definitely provides more meaningful information for an investment fiduciary to process in the investment decision process.

Bayesian theory is consistent with ERISA’s concern with sufficient and meaningful disclosure to allow plan particicipants to make informed decisions. Bayesian theory essentially argues that the more meaningful information provided, the better the chnacesof making an accurate decision. One can also argue that greater transparency called for by the Bayesian Theory is the antithesis of the financial service and annuity industries positions on disclosure.

Simply touting “guaranteed income for life” hardly discloses a complete and accurate list of factors that plan spsonors and other investment fiduciaries must consider in choosing prudent investment options. As a result, plan spsonsors and other investment fiduciaries are often exposed to unnecessary fiduciary liability

Going Forward So why have I taken the time to discuss Bayesian Theory, probabilty, breakeven analyses, cost-efficiency, and commensurate return First, as a fiduciary risk mangement consultant, I consider these topics to be an intergral part of my services and responsibilities to my clients, my value-added proposition.

Second, I believe that we are going to see a signficant change in the areas of ERISA and basic fiduciary litigation. Hopefully, that change will begin with SCOTUS having an opportunity to review the Home Depot 401(k) decision and render a decision that will result in greater uniformity in the interpretation and enforcement of ERISA’s protections and guarantees. If this does come true, I anticipate seeing a significant and immediate increase in ERISA-related litigation, both in terms of plan participant/plan sponsor litigation and plan sponsor/plan adviser litigation.

As part of a plan sponsor’s fiduciary duties of loyalty and prudence, ERISA requires plan sponsors to perform an independent and objective investigation and evaluation of each investment option chosen for a pension plan. Basic fiduciary law requires the same standards for investment fiduciaries in general.

I advise all of my fiduciary risk management clients to insist that a plan consultant/plan adviser justify all recommendations with either a written AMVR analysis, strictly following the model that InvestSense created, with no so-called “improvements,” or, in the case of annuities, a written breakeven analysis of any recommended annuity, including all assumptions and data upon which the breakeven analysis was based.

In the case of variable annuities, fixed indexed annuities and any other annuity whose returns are tied to the stock market and/or market indices, I advise my clients to insist on a comparison to the performance of the underlying index over specific time periods, e.g., 5 and 10 years, specific information as to the amount of any spreads that will assessed by the annuity issuer, and a simple, plain English explanation of the interest crediting methodolgy that the annuity issuer will use. This information will hopefully allow plan sponsors to provide the “sufficient information” required under ERISA 404(c), and thereby qualify for the “safe harbor” protections offered by Section 404(c).

Notes 1. Hughes v. Securities and Exchange Commission, 174 F.2d 969, 975 (D.C. Cir. 1949) 2. Higgins, Mark J., Investing in U.S. Financial History: Understanding the Past to Forecast the Future. Greenleaf Book Group Press: Austin, TX, 2024, 420-421. 3. William F. Sharpe, “The Arithmetic of Active Investing,” https://web.stanford.edu/~wfsharpe/art/active/active.htm. 4. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926. 5. Jeremy Babener, “Structured Settlements and Single-Claimant Qualified Settlement Funds: Regfulating in Accordance With Structured Settlement History,” New York University Journal of Legislation and Public Policy, Vol . 13, 1 (March 2010)

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Simplicity is the new sophistication.– Steve Jobs

Complexity is job security. – Rick Ferri

I recently conducted a fiduciary prudence audit for a 401(k) plan. During the review of my audit findings, I focused on two significant issues: 1. The inclusion of a variable annuity in the plan, and 2. The inclusion of duplicate mutual funds in the plan, resulting in the inclusion of numerous cost-inefficient funds.

The duplicity of funds is easy to resolve. When it comes to 401(k)/403(b) compliance and risk management, less is usually more as long as a prudent selection process is used.

Variable Annuities in Plans In my opinion, nothing raises a 401(k) compliance red flag more than the inclusion of an in-plan annuity. I have written several posts on the issues of the inclusion of annuities in plans. Chris Tobe, one of my co-founders of the web site, “The CommonSense 401(k) Project,” has posted several articles on the site with regard to the inherent fiduciary issues with annuities. Chris previously worked at a well-known annuity distributor designing annuities.

Rather than repeating all the issues discussed in our previous posts, I will just provide a few of the key risk management issues that plan sponsors should consider before including an in-plan annuity within their plan:

1. Duplicative Tax Benefits – A 401(k)/403(b) plan already provides plan participants with the benefit of deferred taxation. So, an in-plan annuity does not provide a benefit in that regard. 2. Lack of an ERISA Requirement – Neither ERISA nor any other law requires that a plan offer an in-plan annuity within their plan. I have heard stories about annuity advocates falsely representing that the SECURE Act and SECURE 2.0 require a plan to offer annuities and/or guaranteed retirement income products within a plan. Simply not true.

ERISA Sections 404(a)1nd 404(c)2 do not require that any specific category of investments be offered within a plan. Both sections simply require that each investment offered within a plan be legally prudent. The most common standards for determining legal prudence are the fiduciary prudence standards established by the Restatement of Trusts (Restatement). 3. Impact on Participant Fees – In reviewing potential investment options for a plan, a plan sponsor should focus on the cost-efficiency of the investment. Plan sponsors often only focus on nominal, or reported, returns. However, the Restatement emphasizes the importance of cost-consciousness/cost-efficiency.3

The Department of Labor recently filed an amicus brief in the pending Home Depot 401(k) litigation.# They summed up a fiduciary’s duties vis-à-vis perfectly, citing several provisions from the Restatement.

The judgement and diligence required of a fiduciary in deciding to offer any particular investment must include consideration of costs, among other factors, because a trustee ‘must incur only costs that are reasonable in amount and appropriate to the investment responsibilities of the trusteeship.4

Variable annuities are especially insidious in assessing inappropriate and inequitable fees. For example, many annuity issues assess annual fees to supposedly cover the cost of the variable annuity’s death benefit. However, the annuity issuers often base the annual death benefit fee on the accumulated value of the annuity, even though annuity issuers often limit their liability under the death benefit to the amount of the variable annuity owner’s actual contributions to the annuity.

As a result of this deceptive practice, known as “inverse pricing,” the annual death benefit fee is neither reasonable nor appropriate, thereby resulting in a violation of a plan sponsor’s fiduciary duties. The fact that this also results in a windfall for the annuity issuer at the annuity owner’s expense is an additional violation of a plan sponsor’s fiduciary duties of prudence and loyalty.

When I asked the plan sponsor what factored in the plan’s decision to include the variable annuity in the company’s, he responded that he simply wanted to help his employees and, based on what the plan adviser had told him, the annuity would help his employees.

This is consistent with a recent LIMRA article, “Are In-Plan Annuities at a Tipping Point?”6 The article evaluated common reasons that employers offered for offering in-plan annuities. The top three reasons were

Feel obligation to help employees generate income in retirement – 43%

Recommendation of plan consultant/advisor – 39%

Feel best place to generate retirement income is from the plan – 37%

As for the first and third reasons, as previously discussed, there is simply no such obligation legally. Nice thought, but poor judgment in terms of fiduciary risk management given the excessive fees and often cost-inefficient investment subaccounts offered within the annuity,

The fact that the plan participant will typically be required to annuitize the annuity contract to receive the guaranteed stream of income, surrendering both control of the annuity and ownership of the value within the annuity to the annuity issuer, with no guarantee of receiving a commensurate return, raises obvious question with regard to the plan sponsor’s fiduciary duties of prudence and loyalty.

The second reason raises a number of interesting questions. Mark Higgins of Index Fund Advisers has recently written an article on the issue of quality of advice provided by plan advisers. In “The Unspoken Conflict of Interest at the Heart of Investment Consulting,”7 Higgins specifically addresses plan advisers’ conflicts-of-interest and the need for plan sponsors to be aware of and address such issues to avoid unnecessary fiduciary liability exposure.

Higgins recommends that trustees and other investment fiduciaries recognize that the advice they receive from investment consultants is often tainted by conflicts of interest which calls into question the basic value of such advice. Once fiduciaries recognize the conflict-of-interest issue, Higgins suggests that fiduciaries search for less complex and less costly strateg[ies’]

Higgins has also recently written a book, “Investing in U.S. Financial History: Understanding the Past to Forecast the Future “, which is scheduled for release on February 27. One of the chapters in his book addresses the issue of the complexity often associated with advice from investment consultants, which would include plan advisers.

Higgins was kind enough to let me read the chapter from his book which addresses the unnecessary complexities that advisors and consultants build into their advice. Rick Ferri’s quote at the beginning of this post suggests that the inclusion of such complexities is deliberately self-serving, and further proof of the conflict-of-interest plan sponsors, trustees, and other investment fiduciaries must deal with. The late Charlie Munger had a similar quote – “Show me the incentives and I’ll show you the outcome.”

Higgins and I are both fans of investment icon Charley Ellis. Higgins perfectly sums up Chapter 25, “Manufacturing Portfolio Complexity,” and the never-ending challenges investment fiduciaries and investors fact with this quote from Ellis:

Consultants’ agency interests…are economically focused in keeping the largest number of accounts for many years as possible. These agency interests are not well aligned with the long-term principal interests of the client institution.

Going Forward

As a general rule, the more complexity that exists in a Wall Street creation, the faster and further investors should run. – David Swensen8

Simplicity is the hallmark of truth – we should know better, but complexity continues to have a morbid attraction….The sore truth is that complexity sells better.” – Morgan Housel9

Swensen’s and Housel’s quotes are equally applicable for plan sponsors and other investment fiduciaries. Prudent fiduciaries do not expose themselves to unnecessary complexity or fiduciary risk. One of Warren Buffett’s basic tenets is that an investor should not invest in anything they do not understand.

Higgins has written a valuable contribution to the ongoing battle for investor protection and the development of fiduciary law. Higgins basically argues that investors and investment fiduciaries should avoid the unnecessary complexity, and the conflicts-of-interest, that are often built into modern investments.

For my part, I have developed two simple, yet powerful, metrics, the Active Management Value Ratio™ and the Fiduciary Prudence Ratio™, to provide investment fiduciaries, investors, and attorneys with a means of quickly assessing whether actively managed mutual funds are truly in the best interest of their clients and themselves.

The byline on my sister site, “CommonSense InvestSense, is “the power of the Informed Investor.” As my discussion about the inclusion of an in-plan annuity suggests, far too often investment fiduciaries may find themselves facing unwanted fiduciary liability due to the failure of a plan advisor to provide material information to the plan sponsor and/or the plan sponsors’ failure to ask necessary questions due to the plan sponsor’s lack of experience with and/or understanding of important investment principles.

Transparency and disclosure are the financial services industry’s kryptonite. Such lack of transparency and disclosure is often deliberate to hide the conflicts-of-interest and unnecessary complexity that Higgins discusses in his book.

Plan sponsors need to remember this in dealing with stockbrokers and insurance agents. The courts have consistently warned plan sponsors that they cannot blindly rely on third parties.

I always advise my fiduciary risk management clients to insist that their plan advisor document all advice provided, and the reasoning behind same, in writing. Many advisors refuse to do so, knowing the true quality of their advice. Refusal to provide such documentation should be an immediate red flag to a plan sponsor.

P.S. Whenever I give a presentation about the perils of offering in-plan annuities within a plan, I typically get follow-up emails or calls asking for help in addressing the problem. As a former securities compliance director, I am all too familiar with the problem with annuities, as our brokers often obtained new customers that had been convinced to purchase an unsuitable annuity.

There are possible solutions to addressing the in-plan annuity conundrum. However, plan sponsors should not attempt to resolve such problems without the aid of an experienced securities attorney, a knowledgeable ERISA attorney, and possibly a good tax attorney.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Most pension plans use mutual funds as the primary investment options within their plan. The Restatement of Trusts (Restatement) states that fiduciaries should carefully compare the costs and risks associated with a fund, especially when considering funds with similar objectives and performance.1 The Restatement advises plan fiduciaries that in deciding between funds that are similar except for their costs and risks, the fiduciary should only choose the fund with the higher costs if the fund “can reasonably be expected” to provide a commensurate return for such additional costs and/or fees.2

Given the historical underperformance of many actively managed mutual funds, factoring in commensurate returns can be a significant hurdle that pension plan fiduciaries too often fail to properly consider. A fund with higher costs that fails to provide a commensurate return to a plan participant, namely a higher positive incremental return than the fund’s incremetnal costs, has no inherent value to an investor and is clearly imprudent.

A common argument by the financial services industry, and even some courts, is that a fiduciary is not legally bound to select the least expensive investment option. However, that argument, focusing only on costs, can be misleading, as other factors must be considered. TIAA-CREF properly summed up a plan sponsor’s fiduciary obligations with regard to factoring in an investment’s costs, stating that

[p]lan sponsors are required to look beyond fees and determine whether the plan is receiving value for the fees paid. This should include an evaluation of vital plan outcomes, such as retirement readiness, based on their organization’s values and priorities.3

So, how does one determine whether a plan is “receiving value,” an actual benefit from a plan adviser’s advice? Businesses often use a cost/benefit analysis to determine whether to pursue a project based on the cost-efficiency of the project. When a cost/benefit analysis indicates that the projected costs exceed the projected benefits, the project is usually deemed cost-inefficient and is not worth pursuing.

A simple cost/benefit analysis would seem to be a part of a prudent process for plan sponsors to use evaluating the fiduciary prudence of investment products in defined contribution plans (DCPs). However, based on the evidence, very few plans seem to use cost/benefit analyses as part of their fiduciary prudence process. Furthermore, even when plans do use cost/benefit analysis, there are often legitimate questions as to whether such analyses were properly conducted.

An obvious question would be why some plans not use cost/benefit analyses in conducting their legally required independent and objective investigation and evaluation of investment options for their plan. Costs that exceed benefits would seem to be a simple enough standard.

Perhaps the answer lies in the fact that actively managed mutual funds continue to compose the majority of investment option within plans. Studies havev consistently shown that the overwhelming majority of actively managed mutual funds are cost-inefficient, as they fail to even cover their costs.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.4

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.5

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.6

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.7

The Active Management Value RatioTM Research has consistently shown that most people are more visually oriented when it comes to understanding and retaining information. Therefore, as a plaintiff’s attorney, I created a simply metric, the Active Management Value Ratio™ (AMVR) to provide a visual representation of the academic studies’ findings with regard to the performance of actively managed mutual funds, most notably the research of investment icons, including Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel.

[T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.8

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns.9

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.10

The beauty of the AMVR is its simplicity. In interpreting a fund’s AMVR scores, an attorney, fiduciary or investor only must answer two simple questions:

1. Does the actively managed mutual fund produce a positive incremental return? 2. If so, does the fund’s incremental return exceed its incremental costs?

If the answer to either of these questions is “no,” then the fund does not qualify as cost-efficient under the Restatement’s guidelines.

The AMVR slide shown above is a cost/benefit analysis comparing the retirement shares of two popular large cap growth mutual funds, one an actively managed fund, the other an index fund.

A simple analysis shows that the actively managed fund’s incremental costs exceed the fund’s incremental negative returns. Since costs exceed returns, this would result in the actively managed fund being cost-inefficient relative to the index fund for the time period studied.

The Securities and Exchange Commission and the General Accountability Office have both found that each additional 1 percent in costs/fees reduces an investor’s end-return by approximately 17 percent over a twenty year period.11 If we treat the incremental underperformance of the actively managed fund as an opportunity cost, and combine that number with the incremental costs, based on the fund’s stated expense ratio, the projected loss in end-return would be approximately 35 percent.

But does the nominal/stated cost version of the AMVR actually reflect the costs incurred by plan participants if the actively managed fund is selected within a plan?

The Active Expense RatioTM In a 2007 speech, then SEC General Counsel, Brian G. Cartwright, asked his audience to think of an investment in an actively managed mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s combined costs.

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund-no overweightings or underweightings-then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?12

Fortunately, Ross Miller introduced a metric, the Active Expense Ratio (AER), which allows fiduciaries and investors to perform the type of analysis Cartwright suggested. Miller explains the importance of the AER as follows:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.13

In the AMVR example shown, using nothing more than just the actively managed fund’s r-squared number and its incremental cost, the AER estimates the actively managed fund’s implicit expense ratio to be 3.36, resulting in incremental correlation-adjusted expense ratio/costs of 3.31. Combined with the actively managed fund’s underperformance, and using the DOL’s and GAO’s findings, that would result in a projected loss of approximately 84 percent over a twenty year period.

The Fiduciary Prudence Ratio™ The AMVR provides all of the information needed to perform several types of cost/benefit analysis. The AMVR equation, incremental correlation-adjusted costs divided by incremental risk-adjusted return, provides an analysis of the premium paid by anyone investing in the actively managed mutual fund, relative to an investment in the benchmark index fund.

While the AMVR is simple enough, some have suggested that a more traditional metric focusing on return relative to costs would be more helpful and easier to uderstand. For some, the issue with the AMVR format seems to be that funds that do not produce a positive incremental return do not earn an AMVR rating.

The AMVR metric makes it easy to produce a more return-focused cost/benefit analysis by flipping the original equation so that the incremental risk-adjusted return becomes the numerator and the incremental risk-adjusted costs becomes the denominator. This new metric is known as the Fiduciary Prudence Ratio™ (FPR).

In using the FPR, the goal would be a ratio above 1.00, which would indicate that the actively managed fund’s incremental risk-adjusted return was greater than the fund’s incremental costs. The higher the fund’s FPR, the greater the value provided.

In the AMVR example shown above, the actively managed fund’s FPR would be zero due to the fund’s failure to provide a positive incremental risk-adjusted return. The zero score would indicate that the fund would be imprudent under the Restatement (Third) of Trust’s fiduciary prudence standards.

Some people have indicated an aversion to working with decimal points. In that case, simply multiply the FPR discussed above by 100 to get the more common 1-100 format. Anyone deciding to use the 1-100 format must keep in mind that the FPR score produced is a relative score, not an absolute score. In interpreting the FPR using the 1-100 format, a score above 100 would be needed to establish that the actively managed fund provided value, provided incremental risk-adjusted returns that were greater than the fund’s incremental costs.

While other benchmarks could obviously be tested, using either form of incremental costs as the numerator, the cost-consciousness/cost-efficiency requirements of the Restatement would also have to be considered.

Going Forward

[A plan sponsor’s fiduciary duties are] “the highest known to the law.”14

In reviewing some recent court decisions in DCP fiduciary breach actions, some courts have seemingly lost sight of ERISA’s stated goal, that being to protect workers and to help them prepare for retirement. Some courts rarely address the issue of whether the DCP’s investment options produce value for plan participants. As mentioned earlier, a prudent DCP investment option is one that is cost efficient, one whose benefits are at least commensurate with the fund’s extra cost and risks.

The problem for many DCP plan sponsors and other DCP fiduciaries is the history of consistent underperformance by many actively managed mutual funds relative to passively managed index funds. The FPR could reduce the time and costs of performing the legally required independent investigation and evaluation of each investment option chosen for a plan.

The simplicity of both the AMVR and the FPR should improve the quality of investments chosen for a DCP plan, thereby reducing the risk of litigation and unwanted fiduciary liability exposure. The combination of the AMVR and the FPR could easily expose situations where the plan adviser is not providing value for the plan or its participants, in which case a prudent plan sponsor should consider replacing the plan provider in order to reduce any potential future fiduciary liability exposure.

By combining the AMVR and the FPR, DCP plan sponsors should be able to use “humble arithmetic” to easily create and maintain win-win DCP plans that provides value for both the plan sponsor, the plan participants, and their beneficiaries.

Notes 1. Restatement (Third ) Trusts §90 cmt m. Copyright American Law Institute. All rights reserved. 2. Restatement (Third) Trusts §90 cmt h(2). Copyright American Law Institute. All rights reserved. 3. TIAA-CREF, “Assessing the Reasonableness of 403(b) Fees,” https://www.tiaa.org/public/pdf/performance/ReasonablenessoffeesWP_Final.pdf. 4. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 5. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 6. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 7. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997). 8. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm. 9. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 10. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 11. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study). 12. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G. Cartwright). http://www.sec.gov/news/speech/2007/spch102407bgc.htm 13. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926. 14. Restatement of Trusts 2d § 2, comment b (1959). ” Donovan v. Bierwirth, 680 F.2d 263, 272 n.8 (2d Cir. 1982)

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

I was at a professional reception over the holidays when someone introduced themselves and asked the “what do you do for a living” question. The rest of the conversation went something like this:

“I am a fiduciary risk management counsel.”

“What does a fiduciary risk management counsel do?

“I mainly reverse engineer 401(k) and 403(b) pension plans.”

I explained that I basically evaluate pension plans in terms of fiduciary prudence/cost-efficiency using the Active Management Value Ratio (AMVR) metric. He eventually asked me what I thought was the most common mistake plan sponsors make. That’s easy – they expose themselves to unnecessary fiduciary liability exposure because they do not truly understand what is legally required of them.

From there, I basically made my typical marketing pitch. When I asked him what he thought a plan sponsor’s legal duties were, he told me (1) to help plan participants achieve “retirement readiness,” and (2) to offer plan participants as many investment options as possible, to provide them with a “meaningful” choice of investments. And yes, he said “meaningful.”

We ended up talking for a little over thirty minutes and I actually enjoyed it. I always enjoy seeing a plan sponsor actually understand their true legal duties, which allows them to effectively manage their fiduciary risk.

A plan sponsor’s fiduciary duties do not include helping plan participants achieve “retirement readiness,” “financial wellness,” or any of the other marketing buzzwords that plan advisors often use. Why? Simply because, just like a stockbroker or financial adviser, a plan adviser cannot guarantee the performance of any mutual fund or the stock market in advance.

Any liability exposure that stockbrokers, financial advisers, and plan advisers face is due to the quality of their advice at the time that such advice is provided. It’s just that simple. In terms of 401(k) and 403(b) plans, plan sponsors should absolutely be familiar with Sections 404(a) and 404(c) of ERISA, as well as the relevant regulations, The regulations are often overlooked, but they are important as they provide practical advice and information beyond ERISA’s generic framework.

ERISA Section 404(a) states as follows:

(a) Prudent man standard of care

(1)[A] fiduciary shall discharge his duties…

with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims;…1