“Facts do not cease to exist because they are ignored” – Aldous Huxley

The Sixth Circuit Court of Appeals’ recent decision in the CommonSpirit Health (CommonSpirit)1 401(k) action has brought renewed attention to several key 401(k) compliance and fiduciary liability issues. While many in the financial services and 401(k) industry have suggested that the decision signifies a new approach to 401(k) litigation, I would argue that that decision is premature.

I have over 27 years of combined experience in securities/RIA/ERISA compliance, I am a firm believer in the value of the black letter law, the actual statutes and regulations that govern an area of the law, as opposed to legal decisions interpreting such laws.

A prime example of that was SCOTUS’ recent decision in the Northwestern University case.2 As the Court pointed out, ERISA’s own language clearly indicated that the Seventh Circuit’s “menu of options” defense had no merit, to the point that Justice Kagan even asked the school’s attorney whether he actually believed his own argument. His answer – “no.”

We now have the same situation presenting itself as a result of the CommonSpirit decision, with the court renewing the anti-index funds “meaningful benchmarks” and “apples and oranges” argument. Both of these arguments were discredited in the First Circuit’s Brotherston decision3, and SCOTUS’ subsequent refusal to hear the case on appeal.

As a result of the CommonSpirit decision, we once again have two federal appellate courts with inconsistent and irreconcilable decisions that threaten the rights and protections guaranteed under ERISA. Fortunately, I would argue that the First Circuit has already provided the answer, stating that

[T]he Restatement specifically identifies as an appropriate comparator for loss calculation purposes’ return rates of one or more…suitable index mutual funds or market indexes….’

ERISA itself is not so specific. Rather, it states that a breaching fiduciary shall be liable to the plan for ’any losses to the plan resulting from each such breach.’ Certainly this text is broad enough to accommodate the total return principle recognized in the Restatement….And as the Supreme Court has instructed, when we confront a lack of explicit direction in the text of ERISA, we often find answers in the common law of trusts.4

ERISA is essentially a codification of the common law of trusts. The Restatement of Trusts essentially reflects the common of trusts. The First Circuit’s points perhaps explain the fact that the Sixth Circuit mentioned neither the Brotherston decision nor the Restatement of Trusts in its CommonSpirit decision.

Nevertheless, the CommonSpirit decision invites a deeper examination of the “why” regarding the current 401(k) litigation trend in general. While the amount of 401(k) litigation is a much-discussed topic, far too often the argument is disingenuous, as it ignores two key facts – most 401(k) plans are non-ERISA compliant due to the amount of cost-efficient and/or “closet index” funds offered within modern 401(k) and 403(b) plans.

Cost-Inefficiency Within Plans

Plan sponsors are co-fiduciaries with any plan adviser the plan hires. However, in many cases, the plan adviser will insert a clause in their advisory contract with the plan disclaiming any fiduciary duties in connection with their services to the plan.

I maintain that by agreeing to an advisory contract with such a fiduciary disclaimer clause, the plan sponsor violates their fiduciary duties. My argument is based on the fact that by agreeing to release a plan adviser from their co-fiduciary status and duties, a plan sponsors arguably allows a plan adviser to legally provide a lower quality of advice under the SEC’s Regulation Best Interest (Reg BI) than the adviser would have been required to provide as a fiduciary.

While a true fiduciary standard requires an ERISA fiduciary to always act in the best interest of a plan’s plan participants and their beneficiaries, Reg BI provides advisers with a loophole, the “readily available alternatives” language, which effectively allows an adviser to put the best interest of their broker-dealer and themselves ahead of plan participants and their beneficiaries. This creates an obvious problem, especially when the evidence suggests that many plan sponsors blindly follow their plan adviser’s advice without performing their own legally required investigation and evaluation of a plan’s investment options.

Does a plan sponsor’s agreeing to a fiduciary disclaimer clause allow a plan adviser to recommend imprudent investments for a plan under Reg BI? Does a fiduciary disclaimer clause allow an adviser to deny a plan access to prudent investment alternatives that the adviser actually has available, but simply chooses not to offer to a plan for financial reasons?

Plan advisers typically recommend actively managed investment options because that is how they and their broker-dealers make money. Research has consistently shown that the overwhelming majority of actively maanged mutual funds are cost-inefficient when compared to comparable passively managed index funds.

- 99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.5

- [I]ncreasing numbers of clients will realize that in toe-to-toe competition versus near-equal competitors, most active managers will not and cannot recover the costs and fees they charge6

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.7

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.8

In an earlier post, I noted that when the Securities and Exchange Commission (SEC) announced and implemented Regulation “Best Interest” (Reg BI), then SEC chairman Jay Clayton acknowledged the importance of cost-efficiency of investments:

rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.9

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.10

And yet, as previously mentioned in my last post, the “readily available alternatives” language in Reg BI effectively allows brokers to ignore the cost efficiency issue and promote their own “best interests.”

SCOTUS has consistently recognized the Restatement (Third) of Trusts (Restatement) as a valuable resource in resolving fiduciary questions. The two dominant themes throughout the Restatement are cost-consciousness/cost-efficiency and risk-management through effective diversification.

Section 90 of the Restatement, more commonly known as the Prudent Investor Rule, is often cited in connection with the fiduciary duties of prudence and loyalty. Comment h(2) of Section 90 states that active management funds or strategies are only prudent when it can be objectively predicted that the fund/strategy will an investor with a commensurate return for the additional costs and risks typically associated with active management.

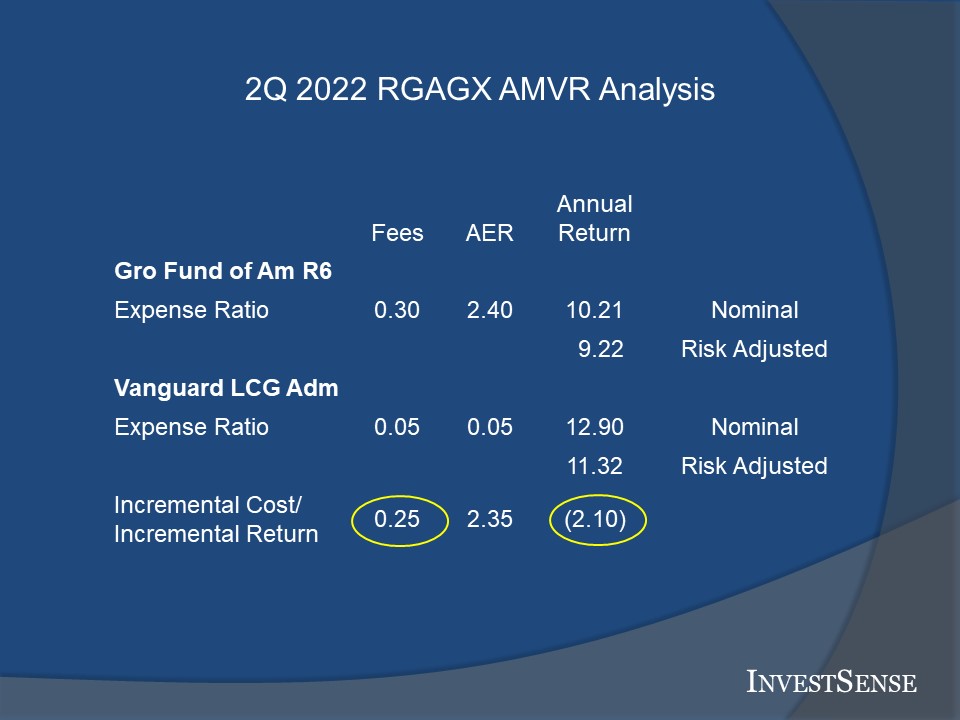

The obviousness and importance of cost-inefficiency within 401(k) plans can be illustrated with two forensic analyses using my Active Management Value Ratio™ (AMVR). The AMVR is based on the research of investment experts such as Charles D. Ellis, Burton L. Malkiel, Nobel Laureate Dr. William D. Sharpe and Ross Miller.

The basic premise is to assess the cost-efficiency of an actively managed mutual fund by comparing the fund’s incremental costs and incremental returns relative to a comparable index fund. Index funds, rather than market indices, are used for comparison purposes since market indices do not allow for cost-efficiency comparisons.

Each year, the retirement shares of Fidelity’s Contrafund Fund (FCNKX) and American Fund’s Growth Fund of America (RGAGX) are rated as within the top funds used in U.S. defined contribution plans. AMVR forensic analysis of both funds is shown below (based on the 5-year period ending on June 30, 2022).

When I perform an AMVR analysis, I report two sets of numbers, one set being based on the funds’ nominal, or publicly reported numbers, the other set being being based on the funds’ correlation-adjusted costs and risk-adjusted returns. Experience has shown that the investment and 401(k) industries typically prefer the nominal numbers, while ERISA plaintiff attorneys prefer the adjusted numbers.

The AMVR slides speak for themselves. Situations where an investment’s incremental costs exceed its incremental returns is never a desirable, or prudent, investment scenario. Cost-inefficient investment alternatives within a 401(k) plan are not legally valid “choices.” Additional details on the calculation and interpretation are available on this website.

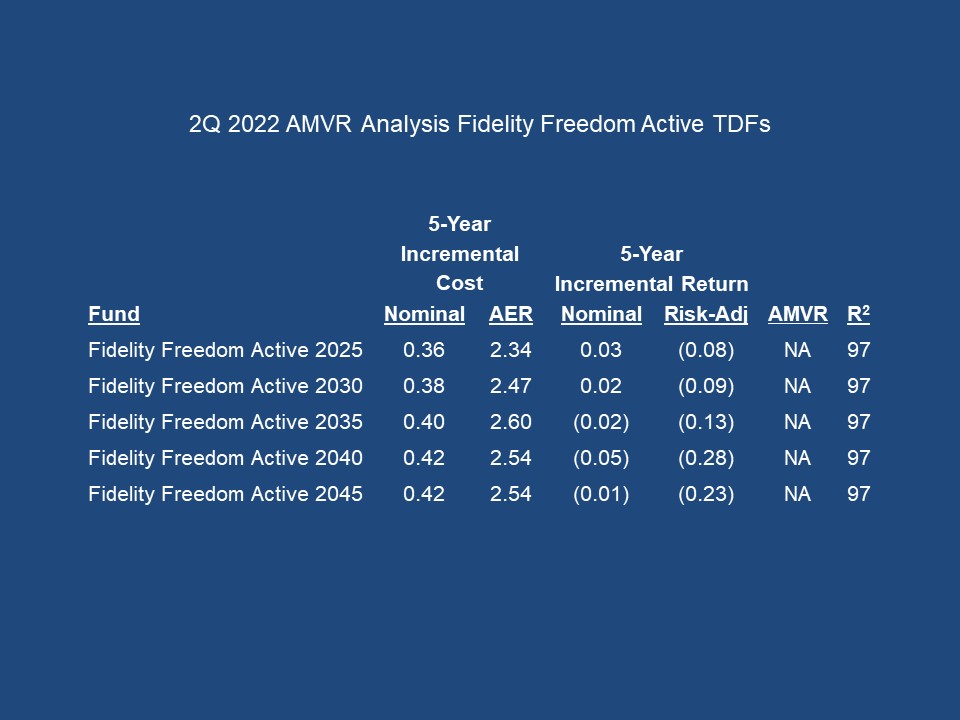

The CommonSpirit case provided users of the AMVR with a unique opportunity – the opportunity to compare the cost-efficiency and respective prudence of two competing products offered by the same fund company, in this case Fidelity Investments. The products in this case involved the Fidelity Freedom suite of actively managed target date funds (TDFs) and the Fidelity Freedom Index TDFs.

The AMVR analysis slide comparing the two Fidelity 2035 TDFs is shown below.

Each quarter InvestSense prepares a “cheat sheet” on some of the top non-index funds within U.S defined contribution plans. The “cheat sheet” comparing the remaining Fidelity Freedom active and Index funds is shown below.

In an earlier AMVR analysis, Fidelity Contrafund K shares were compared to Vanguard Large Cap Growth Index shares. An AMVR forensic analysis comparing Contrafund to Fidelity’s Large Cap Growth Index shares is shown below.

So, the AMVR forensic analysis clearly shows that the Fidelity Large Cap Growth Index Fund shares are a more prudent investment option for a 401(k) plan. However, Fidelity does not offer the Large Cap Growth Index Fund to 401(k) plans. Contrafund is obviously more financially lucrative to Fidelity.

Unless Fidelity is in a fiduciary relationship with a plan sponsor, it has no legal obligation to offer their entire product line to 401(k) plans. If Fidelity is in a fiduciary relationship with a plan, an argument can be made that they do have a fiduciary obligation to offer their most prudent investment alternatives to a 401(k) plan.

At the same time, the Contrafund/Large Cap Growth Index fund AMVR analysis puts a plan sponsor in a predicament given the significantly better performance and cost-efficiency of the index fund. Simply because Fidelity refuses to make the better investment alternative available to a plan does not legally justify selecting the inferior investment alternative and causing the plan participants unnecessary losses. That would obviously constitute a breach of the plan sponsor’s fiduciary duties.

Closet Indexing

[A] large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by paying fees for active management that they do not receive or receive only partially….11

Closet indexing raises important legal issues. Such funds are not just poor investments; they promise investors a service that they fail to provide. As such, some closet index funds may also run afoul of federal securities laws.12

Closet indexing is an international issue. As set out above, the issue is simple – are investors in actively managed mutual funds getting what they were promised, active management, or simply overpaying for the same performance they could receive from less costly index funds.

Professor Ross Miller did a study on the impact of closet indexing, focusing primarily on the relationship between an actively managed mutual fund’s r-squared number, “closet index” status, and the resulting overall financial impact of the two. “Closet index” funds are actively managed funds whose returns are essentially the same as a comparable index fund, but who charge much higher fees than the index fund. The higher an actively managed fund’s r-squared number, the greater the likelihood that the actively managed fund can be classified as a closet index fund.

An r-squared rating of 98 would indicate that 98 percent of an actively managed mutual fund’s returns could be attributed to the performance of a comparable index fund, rather than the active fund’s management team.

There is no universally agreed upon level of r-squared that designates an actively managed mutual fund as a closet index fund. I use an r-squared correlation number of 90 as my threshold indicator for closet index status. Others, including Morningstar, use much lower r-squared numbers.

Miller’s findings were extremely interesting.

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.13

As the AMVR and “cheat sheet” slides provided herein show, once correlations of returns is factored into the cost-efficiency equation, the effective expense ratios investors pay increase substantially, resulting in significantly lower overall cost-efficiency.

Going Forward

As a risk management consultant, I advise plan sponsors and other investment fiduciaries on compliance and “best practices” issues. I constantly stress to them the importance of exposing and eliminating cost-inefficiency and closet indexing within a 401(k) plan.

I often explain the relationship between cost-efficiency and fiduciary prudence/risk management with the following illustration.

As plan sponsors and investment fiduciaries increase the cost-efficiency within their plan, the level of fiduciary prudence increases, reducing their potential fiduciary liability exposure.

I believe that the CommonSpirit decision will eventually be vacated for exactly the reasons that the First Circuit set out in the Brotherston decision – SCOTUS’ advice regarding using the Restatement to resolve fiduciary disputes. The Restatement endorses the use of index funds as acceptable and “meaningful” benchmarks in calculating losses and addressing fiduciary breach questions. “Facts do not cease to exist because they are ignored.”

The Active Management Value Ratio™ provides plan sponsors and other investment fiduciaries with a fundamentally sound and simple means of accomplishing these goals using index funds. In so doing, plan sponsors can create and maintain a win-win plan, one that provides genuine benefits for plan participants and protects plan sponsors against unnecessary and unwanted exposure to fiduciary liability.

Notes

1. Smith v. CommonSpirit Health, No. 21-5964, June 21, 2022 (6th Cir. 2022). (CommonSpirit)

2. Hughes v. Northwestern University, 142 S.Ct. 737 (2022).

3. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Circuit 2018). (Brotherston)

4. Brotherston, 39.

5. Laurent Barras, Oliver Scaillet, and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

6. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, https://www.ft.com/content/6b2d5490-d9bb-eb37a6aa8e

7. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE 57-58 (1997).

8. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Funds Advisors, L.P., August 2016.

9. SEC Release 34-86031, Regulation Best Interest: The Broker-Dealer Standard of Conduct (Reg BI), 279.

10. Reg BI, 279.

11. Martijn Cremers and Quinn Curtis, Do Mutual Fund Investors Get What they Pay For?:The Legal Consequences of Closet Index Funds, https://papers.ssrn.com/sol/papers.cfm?abstract_id=2695133 (Cremers), 5, 42.

12. Cremers, 5, 42.

13. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-4.

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

Pingback: The Conversation Every 401(k) and 403(b) Plan Needs to Have: The Plan Sponsor Liability Circle™ | The CommonSense 401k Project

Pingback: The Conversation Every 401(k) and 403(b) Plan Needs to Have: The Plan Sponsor Liability Circle™ | The Prudent Investment Fiduciary Rules