by James W. Watkins, III, J.D., CFP®, AWMA®

The legal requirement for prudence, as defined in ERISA Section 404(a)(1)(B), is for a fiduciary to discharge his or her duties with:

“the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”

But what does that really mean?

[R]ather than explicitly enumerating all of the powers and duties of trustees and other fiduciaries, Congress invoked the common law of trusts to define the general scope of their authority and responsibility.”1

Thus, a federal common law based on the traditional common law of has developed and is applied to define the powers and duties of ERISA plan fiduciaries….2

OK, getting closer.

The two consistent themes throughout the Restatement are cost-consciousness/cost-efficiency and risk management through effective diversification. Section 90 of the Restatement, more commonly known as the Prudent Investor Rule, contains three comments that could, and should, define prudence in future ERISA excessive fees/breach of fiduciary duty actions.

- A fiduciary has a duty to be cost-conscious. (Introductory Section to Section 90)

- A fiduciary has a duty to select mutual funds that offer the highest return for a given level of cost and risk; or, conversely, funds that offer the lowest level of costs and risk for a given level of return. (cmt. f)

- Actively managed mutual funds that are not cost-efficient, that cannot objectively be projected to provide a commensurate return for the additional costs and risks associated with active management, are imprudent. (cmt. h(2)).

I collectively refer to these three comments as the “fiduciary prudence trinity.”

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.3

Nobel laureate Dr. William Sharpe has offered the following advice for analyzing the prudence of mutual funds:

Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs…. The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative”4

Noted wealth management expert, Charles D. Ellis, goes further, stating that

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!5

Cumulatively, I submit that these comments and quotes suggest that the best way to prove compliance with one’s fiduciary duties is to quantify such duties. The Active Management Value Ratio™ (AMVR) metric provides a simple way of proving compliance with these fiduciary prudence standards.

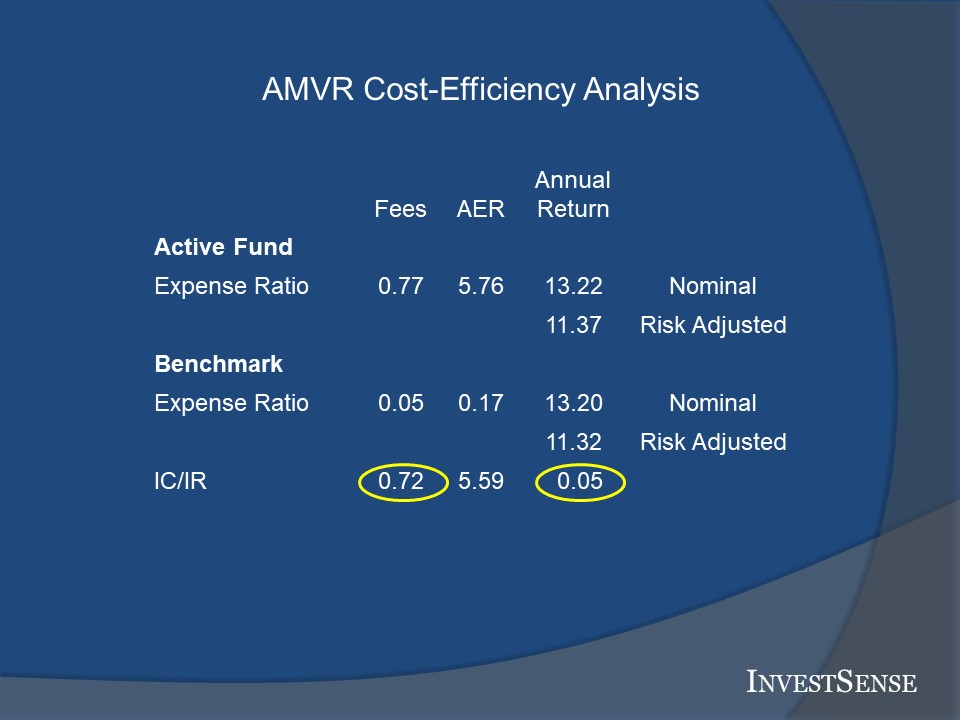

The AMVR analysis shows that the actively managed fund produced a positive incremental return of five basis points at an incremental cost of 72 basis points. As we all learned in our basis economics classes, any situation where costs exceed benefits is not a prudent is not a prudent choice.

I am often asked why the AMVR uses adjusted returns. As the Restatement pointed out, an actively managed fund or a strategy that employs active management is only prudent if an investor receives a commensurate return for the additional risks and costs typically associated with active management.

Another questions I often receive is what is the purpose of the “AER” column. AER stands for Active Expense Ratio, the metric created by Ross Miller. The AER factors the correlation of returns between an actively managed fund and a comparable index fund to determine the effective expense ratio of an actively managed fund.

So why calculate an actively managed fund’s correlation-adjusted expense ratio? As Miller explains,

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funds engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.6

While the calculation methodology for the AER can be intimidating, the AER essentially divides an actively managed fund’s incremental costs by its “active weight.” The active weight is a metric created by Miller to determine the true amount of active management provided by an allegedly actively managed fund.

Based upon my experience, formerly as a securities/RIA compliance officer and now as a securities/ERISA attorney and fiduciary compliance consultant, financial advisers and plan advisers rarely discuss or provide AER numbers in connection with their recommendations. That is exactly why InvestSense includes AER data in its forensic fiduciary analyses, to help fiduciaries aware of potential fiduciary liability issues and the need for additional risk management.

In this example, the r-squared, or correlation of returns, number was 98, which translates into an AW of 0.1250, or 12.50 percent of active management within the actively managed fund. The AER is therefore 5.76 (0.72/.1250), resulting in an incremental CAC (correlation-adjusted cost) of 5.59, which makes the actively managed fund’s cost-efficiency even worse.

Going Forward

I believe that the combination of the “fiduciary responsibility trinity,” (Tibble v. Edison International, Brotherston v. Putnam Investments, LLC, and Hughes v. Northwestern University), and the “fiduciary prudence trinity,” will combine to increase the level of fiduciary litigation and eventual settlements, Investment fiduciaries can use the AMVR metric to proactively manage such liability risk exposure by identifying potential liability issues and adopting the necessary changes to bring their plans/accounts into compliance with ERISA and the Restatement.

Notes

1. In re Enron Corp. Securities, Derivatives, and ERISA Litigation, 284 F. Supp. 2d 511, 546 (N.D. Tex 2003)

2. Ibid.

3. Liss v. Smith, 991, F. Supp. 278, 297 (S.D.N.Y. 1988)3

4. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm.

5. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online at https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c.Sharpe

6. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-4.

© Copyright 2022 InvestSense, LLC. All rights reserved.

“InvestSense,” the “InvestSense” logo, “Active Management Value Ratio. and the “Active Management Value Ratio” logo ” are trademarks of InvestSense, LLC.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.