Having read the CommonSpirit Health (CommonSpirit) decision1 and the related briefs several times, three key fiduciary risk management issues stand out to me with regard to plan sponsors

1. SCOTUS needs to expressly resolve this ongoing “apples and oranges” debate once and for all, to expressly rule on the propriety of using index funds for benchmarking purposes. I believe the Court may legitimately feel that they addressed and resolved the issue by refusing to grant certiorari in the Brotherston decision.2 The Sixth Circuit obviously feels differently, as it resurrected the “apples and oranges” argument in upholding the district court’s dismissal of the case.

In the CommonSpirit decision, neither the circuit court nor the Sixth Circuit acknowledged the First Circuit’s Brotherston decision and/or the court’s reliance on the Restatement (Third) of Trusts’3(Restatement) position on the propriety of using index funds for benchmarking purposes.

“So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100, cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes)”4

Neither court acknowledged SCOTUS’ denial of Putnam’s application for certiorari, which many would interpret as the court’s indication that both the First Circuit’s decision and underlying rationale were correct.

One circuit is not obligated to follow the decisions of another circuit, and laws are obviously open to differing opinions. However, the fact that neither court acknowledged Brotherston nor tried to distinguish the two cases is arguably noteworthy given the First Circuit’s reliance on the Restatement, a resource recognized by SCOTUS as a legitimate resource in resolving fiduciary questions in its Tibble decision.5

Hopefully, the Sixth Circuit’s decision will be appealed. The fact that the case involves the prudence of two competing products from the same mutual fund company makes the case even more appealing for review. As the Solicitor General’s amicus brief in Brotherston argued, the rights and protections guaranteed to employees by ERISA are too important to vary based upon in which jurisdiction employees may reside.

2. The whole “fiduciary disclaimer clause” issue needs to be addressed. More specifically, the question of whether a plan sponsor breaches his fiduciary duties of prudence and loyalty to the plan participants by agreeing to an advisory contract that contains a fiduciary disclaimer clause. Again, I think the CommonSpirit case brings this issue into focus since the case involved similar, yet competing, products offered by the plan adviser, Fidelity Investments.

I think several issues need to be explored and addressed with regard to the use of fiduciary disclaimer clauses in 401(k) plan advisory contracts. It can be argued that removing a plan adviser’s fiduciary obligations allows firms to argue that their advice and recommendations are to evaluated under Regulation Best Interest (Reg BI)6, not a true fiduciary standard.

The resulting quality of advice issues are obvious:

The fiduciary standard requires that an adviser consider the prudence of their actions/recommendations in terms of an “open architecture” platform, or the entire universe of investment options, to ensure that the best interests of the plan participants are genuinely protected.

Reg BI, and its “readily available alternatives” loophole, allows plan advisers to “carve out” a portion of the universe of investment options and essentially put the best interests of the broker-dealer and the plan adviser ahead of those of the plan and its participants.

This result is totally inconsistent with ERISA’s stated purpose and mission, to protect plan participants and retirement plans against any form of inequitable or abusive activity.

In analyzing cases involving fiduciary disclaimer clauses, my initial response is to ask (1) why a plan adviser would even request such a provision, and (2) why would a plan sponsor agree to such a provision.

Releasing a plan adviser from any fiduciary duties or obligations to a plan does not provide any benefits at all to plan participants. Not only does it allow a plan adviser to provide a lesser quality of advice and products pursuant to Reg BI, it also arguably allows them to avoid offering their company’s entire line of financial products to the plan participants, potentially denying the plan participants the opportunity to maximize their potential return by investing in cost-efficient investments. Therefore, agreeing to any plan advisory contract that contains a fiduciary disclaimer clause violates a plan sponsor’s fiduciary duties of loyalty and prudence.

I would argue that prior to agreeing to any fiduciary disclaimer clause, a plan sponsor should consider the fact that the financial services industry has historically opposed any attempt to impose a true fiduciary standard on its members. Could it be because the industry knows that their advice and products typically fall far short of complying with a true fiduciary standard, while Reg BI arguably protects them when providing imprudent advice and/or products?

Section 90, comment h(2), of the Restatement states that that due to the higher costs and risks associated with actively managed funds and active strategies, both are imprudent unless it can be objectively estimated that the funds and/or strategies will provide a commensurate return for the additional costs and risks incurred, i.e., are cost-efficient.7

The financial services industry does not like to discuss cost-efficiency, as studies have consistently shown that the overwhelming majority of actively managed mutual funds are cost-inefficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.8

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.9

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.10

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.11

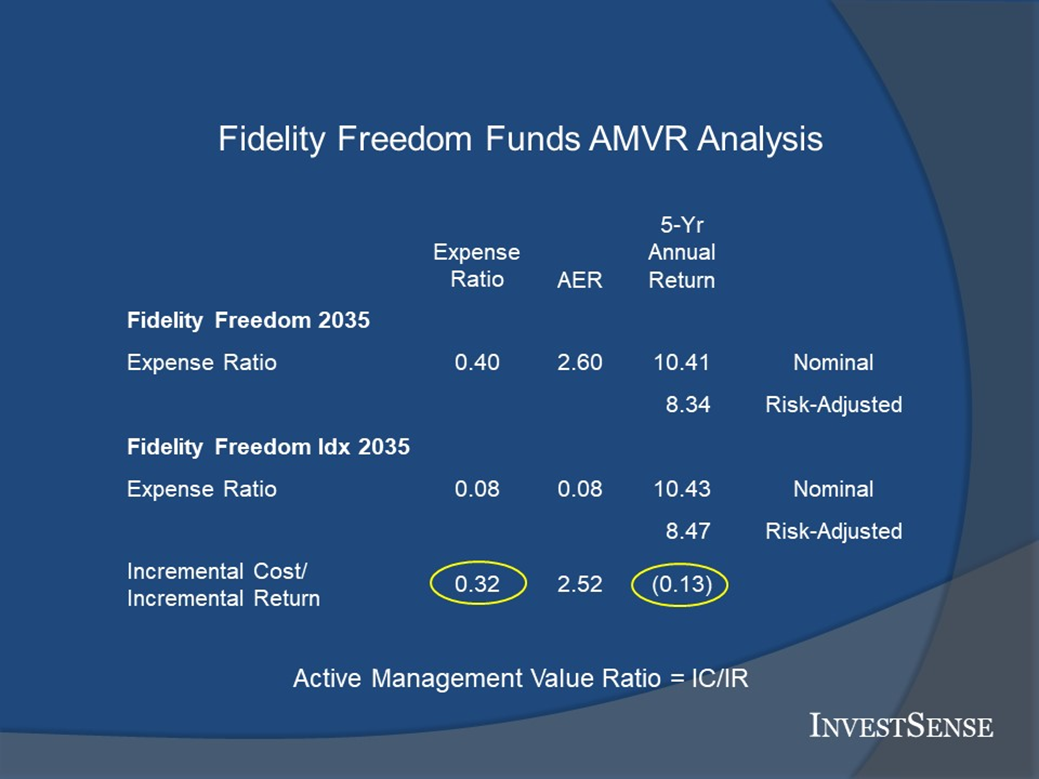

The CommonSpirit case presents a perfect example of this scenario in connection with the comparison between the Fidelity Freedom active suite of target-date funds and the Fidelity Freedom Index target date funds. A forensic analysis comparing the 2035 version of both funds using the Active Management Value Ratio™ clearly shows that the 2035 active version of the funds is cost-inefficient relative to the passive index version.

An AMVR analysis comparing the other Fidelity Freedom active/Freedom Index funds provided similar results

Had the CommonSpirit plan adviser remained subject to a fiduciary standard, it can be argued that the adviser would have been equally legally liable, along with the plan sponsor, for not recommending and selecting the cost-inefficient, i.e., imprudent, funds to the plan. The inability of the plan participants to include the plan adviser in any litigation could also impact their ability to achieve a full and complete recovery for any and damages suffered.

From a strategic standpoint, the inclusion of a claim based on the fiduciary disclaimer theory could also benefit ERISA plaintiff attorneys in preventing dismissal of their cases by creating a genuine and material issue of fact. On ruling on motions to dismiss, judges are required to accept plaintiff’s allegations of fact as true and to base their decisions involving such motions only on questions of law. A basic tenet of the law is that decisions of fact are to be made solely by a jury.

Furthermore, given the fact that the plaintiff will rarely have pre-trial access to the advisory contract between the plan and the adviser, the Leber v. Citigroup 401(k) Investment Committee decision12 should be cited as authority for granting plaintiff’s attorney restricted discovery on the issue of the advisory contract prior to the court deciding a motion to dismiss.

3. When I read the Sixth Circuit’s CommonSpirit decision, two other 401(k) decisions immediately came to mind, Brotherston and Hughes v. Northwestern University.13 The reasons these cases came to mind is that they support my advice to plan sponsors and other investment fiduciaries to follow the actual law, not the interpretations of the law by the courts.

My advice is not meant as disrespect for the courts. My advice is simply meant as a risk reduction reminder to plan sponsors and other investment fiduciaries that courts can, and sometimes do, legitimately interpret the application of the law differently due to a difference in the facts involved in a case.

Courts are also not infallible. As Justice Benjamin Carozo pointed out,

There is in each of us a stream of tendency, whether you choose to call it philosophy or not, which gives coherence and direction to thought and action. Judges cannot escape that current any more than other mortals.

The great tides and currents which engulf the rest of men do not turn aside in their course and pass the judges by.

The law, however, should remain constant. And in interpreting and applying the law, I agree with Justice Cardozo that in many cases, “[t]he risk to be perceived defines the duty to be obeyed.”

In the Northwestern University case, we saw SCOTUS reject the Seventh Circuit’s “menu of options” argument based solely on the wording of ERISA itself. In Brotherston, we saw the First Circuit reject the lower court’s “apples and oranges” argument solely on the wording of Section 100, comment b(1), of the Restatement (Third) of Trusts.

In the CommonSpirit case, we have two Courts of Appeal that have issued two diametrically opposed and irreconcilable decisions involving the same law and the same issue, the propriety of using index funds for benchmarking purposes in determining damages in 401(k) litigation cases.

Only time will tell what the eventual outcome of the case will be. In the meantime, I believe the case provides a valuable lesson as to why plan sponsors and other investment fiduciaries should always focus primarily on the actual laws, not judicial interpretations of such laws

As the Solicitor General pointed out in the amicus briefs filed with SCOTUS in both the Brotherston and Northwestern University cases, inconsistencies between the federal Courts of Appeal is simply one that cannot be allowed to stand, especially in ERISA cases where the financial security of employees and their families are involved.

Notes 1. Smith v. CommonSpirit Health, No. 21-5964, June 21, 2022 (6th Cir. 2022). (CommonSpirit) 2. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Circuit 2018). (Brotherston) 3. RESTATEMENT (THIRD) TRUSTS, (American Law Institute). (All rights reserved). 4. Brotherston, 39. 5. Tibble v. Edison International, 135 S. Ct 1823 (2015). 6. SEC Release 34-86031, Regulation Best Interest: The Broker-Dealer Standard of Conduct (Reg BI), 279. 7. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt h(2). (All rights reserved). 8. Laurent Barras, Oliver Scaillet, and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANE 179, 181 (2010). 9. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, https://www.ft.com/content/6b2d5490-d9bb-eb37a6aa8e 10. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE 57-58 (1997). 11. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Funds Advisors, L.P., August 2016. 12. Leber v. Citigroup 401(k) Plan Inv. Committee, 2014 WL 4851816. 13. Hughes v. Northwestern University, 142 S.Ct. 737 (2022).

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

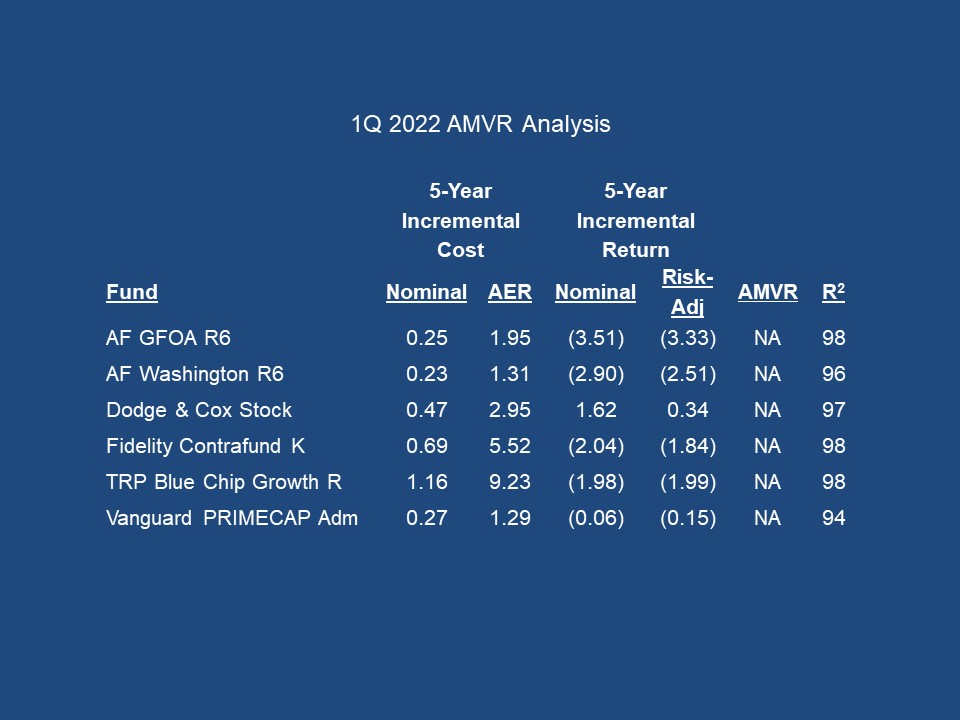

At the end of each calendar quarter, I perform a forensic AMVR fiduciary prudence analysis on the non-index mutual funds within the top 10 funds in U.S. defined contribution plans, as ranked by “Pensions & Investments.” InvestSense provides both a 5-year and a 10-year analysis, using both a fund’s incremental nominal costs/returns and a fund’s incremental AER/correlation-adjusted costs and incremental risk-adjusted returns.

Studies have consistently shown that the overwhelming majority of actively managed mutual funds are cost-inefficient. A cost-inefficient mutual funds is never in an investor’s “best interest.” Therefore, a fiduciary that selects cost-inefficient fund would violate his/her fiduciary duty of prudence.

Past AMVR analyses have generally confirmed the studies that have found the majority of actively managed funds to be cost-inefficient. InvestSense uses a fund’s incremental AER/correlation-adjusted costs and incremental risk-adjusted return in assessing a fund’s Fiduciary Prudence Rating.

None of the funds qualified as prudent using the 5-year analysis. The Dodge & Cox Stock fund’s nominal nominal numbers would have qualified as prudent. However, the fund failed to produce a positive incrmental return using the fund’s risk-adjusted return.

The 10-year analyses did produce one fund, the Vanguard PRIMECAP Fund (Admiral shares), that qualified as a prudent performance using the fund’s adjusted costs and returns.

The results of the analyses continue to show the harmful effects of a combination of high incremental costs and high r-squared correlation numbers. A prime example of this is the T. Rowe Price Blue Chip Growth fund, where the combination of high incremental nominal costs (1.17) and a high r-squared number (98) resulted in the fund’s incremental correlation adjusted cost increased to 9.31. Very few actively managed will ever provide incremetnsl returns to cover such a deficit.

Recently, the Sixth Circuit handed down its decision in the Smith v. CommonSpirit Health (“CommonSpirit) 401(k) action.1 My immediate reaction was “hello again SCOTUS,” as once again we have inconsistent and irreconcilable rulings between two circuits involving ERISA litigation

The decision raises a number of issues, including the Court’s suggestion that the alleged popularity of a fund has any relevance whatsoever in connection with the legal prudence of such fund. However I want to focus on what I consider to be the primary reason for the increase in 401(k) litigation and the simple solution that would provide a win-win situation for both plan sponsors and plan participants going forward, reducing litigation and its associated costs.

As the Solicitor General pointed out in the amicus brief it filed in connection with Brotherston v. Putnam Investments, LLC,2 (Brotherston) case, the rights and protections guaranteed under ERISA are simply too important to be determined on the basis of the jurisdiction in which a plan participant resides. And yet, just as in the Northwestern University 401(k) case3, that is exactly the situation we now face as a result of the CommonSpirit decision

SCOTUS denied Putnam’s request for certiorari, thereby arguably implicitly, if not expressly, agreeing with the First Circuit’s decision and the reasoning behind the decision. The Brotherston decision clearly discredited the lower court’s reliance on the “apples and oranges” defense, the suggestion that the use of index funds for benchmarking purposes is legally inappropriate due to inherent differences between active and index funds.

SCOTUS has made it clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected “Congress'[s] desire to offer employees enhanced protection for their benefits.”4

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes)”5

The First Circuit stated that while courts may determine questions of law, the lower court had effectively decided questions of fact, which is the exclusively the responsibility of a jury.

The Court then went on to suggest a way that 401(k) plans might avoid such litigation going forward:

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”6

In the CommonSpirit decision, the Sixth Circuit ignored both the Brotherston decision and the Restatement (Third) of Trusts, a resource that SCOTUS has acknowledged as a resource in resolving questions involving fiduciary prudence. The Sixth Circuit’s primary basis for dismissing the action was its position that index funds are not a “meaningful benchmark” for determining the fiduciary prudence of an actively managed mutual funds.

We accept that pointing to an alternative course of action, say another fund the plan might have invested in, will often be necessary to show a fund acted imprudently (and to prove damages). But that factual allegation is not by itself sufficient.7

That court explained that the two general investment options “have different aims, different risks, and different potential rewards that cater to different investors. Comparing apples and oranges is not a way to show that one is better or worse than the other.”8

That a fund’s underperformance, as compared to a “meaningful benchmark,” may offer a building block for a claim of imprudence is one thing. But it is quite another to say that it suffices alone, especially if the different performance rates between the funds may be explained by a “different investment strategy….”We would need significantly more serious signs of distress to allow an imprudence claim to proceed.9

The Sixth Circuit then went on to suggest that the alleged popularity of a fund and/or its Morningstar rating may be relevant in determining the prudence of a fund. This suggestion is clearly in conflict with other courts, which have consistently stated that the alleged popularity of a fund and/or third-party ratings are totally irrelevant in determining the fiduciary prudence of mutual funds.

The Court then stated that

publicly available performance information about an investment may show sufficiently dismal performance that this reality, when combined with “allegations about methods,” will successfully allege that a prudent fiduciary would have acted differently.10

The Court credited CommonSpirit with removing the AllianzGI Fund as an investment option in 2018, stating that is served as evidence “that CommonSpirit fulfilled its ‘continuing duty to monitor trust investments and remove imprudent ones’.11The Court apparently was unaware that the AllianzGI Fund was apparently closed in 2018, so it is possible that CommonSpirit had a choice in removing the fund from the plan’s menu of investment options

Building a Better, and Fairer, Mousetrap While most 401(k) decisions address costs and returns, I have never seen any court take the next, and to me the obvious, step of combining the two to address the cost-efficiency of an actively managed fund relative to a comparable index fund.

Interestingly enough, the Sixth Circuit referenced Charles D. Ellis’s classic book, “Winning the Loser’s Game.” Unfortunately, the Court failed to reference arguably Ellis’ most important contribution to wealth management:

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns.

When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!12

Add to that the contributions of both Nobel Laurerate Dr. William D. Sharpe and investment icon Burton L. Malkiel:

[T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.13

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.14

Based upon the Restatement and the studies of Ellis, Sharpe, and Malkiel, I created a simple metric, the Active Management Value Ratio™ (AMVR), that allows investors, investment fiduciaries and attorneys to quickly determine the cost-efficiency of an actively managed mutual fund relative to a comparable index fund. For more information about the AMVR, including the calculation process, click here (iainsight.wordpress.com).

Once the AMVR is calculated for an actively managed fund, the investor or investment fiduciary only needs to answer two simple questions:

(1) Does the actively managed mutual fund provide a positive incremental return relative to the benchmark being used? (2) If so, does the actively managed fund’s positive incremental return exceed the fund’s incremental costs relative to the benchmark?

If the answer to either of these questions is “no,” the actively managed fund is both cost-inefficient and unsuitable/imprudent according the the Restatement’s prudence standards, and should be avoided. The goal for an actively managed fund is an AMVR number greater than “0” (indicating that the fund did provide a positive incremental return), but equal or less than “1” (indicating that the fund’s incremental costs did not exceed the fund’s incremental return).

The AMVR metric provides extremely useful information regarding the cost-efficiency of an actively managed mutual fund using just a fund’s nominal, or publicly reported, costs and returns. However, a cost-efficiency analysis should not end there if one wants a truly accurate cost-efficiency analysis of an actively managed mutual fund.

Professor Ross Miller did a study on the impact of closet indexing, focusing primarily on the relationship between an actively managed mutual fund’s r-squared number, “closet index” status, and the resulting overall financial impact of the two. “Closet index” funds are actively managed funds whose returns are essentially the same as a comparable index fund, but who charge much higher fees than the index fund. The higher an actively managed fund’s r-squared number, the greater the likelihood that the actively managed fund can be classified as a closet index fund.

An r-squared rating of 98 would indicate that 98 percent of an actively managed mutual fund’s returns could be attributed to the performance of a comparable index fund, rather than the active fund’s management team.

There is no universally agreed upon level of r-squared that designates an actively managed mutual fund as a closet index fund. I use an r-squared correlation number of 90 as my threshold indicator for closet index status. Others, including Morningstar, use much lower r-squared numbers.

Miller’s findings were extremely interesting, namely that

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.15

As a result of his study, Ross Miller, created the Active Expense Ratio (AER) metric. What Miller discovered was that once a fund’s r-squared correlation number is factored in, an active fund’s AER, the fund’s implicit, or effective, expense ratio is significantly higher than the fund’s stated expense, often as much as 400-500 percent higher. Investors and investment fiduciaries should remember John Bogle’s advice on investment costs, “you get what you don’t pay for,” as well as the fact that simple mathematics proves that each one percent in fees and expenses reduces an investor’s or fiduciary’s end-return by approximately seventeen percent over a twenty-year time period.16

The AMVR and the CommonSpirit Health Decision The Plaintiffs in the CommonSpirit case did not include a cost-inefficiency argument in their complaint. While the AMVR has gained increasing recognition and support among investment fiduciaries and some plaintiff’s attorneys, many attorney still refuse to even consider the metric. Attorneys often cite the simplicity of the AMVR and the fact that many judges still dislike the use of index funds, particularly Vanguard index funds, as comparators due to their inherent advantages over comparable actively managed funds

First, I believe that the simplicity of the AMVR is one of its main advantages. The AMVR requires very little time to learn and use effectively. The calculations are based primarily on online data from free sites such as morningstar.com and yahoo.finance.com and marketwatch.com. Once one becomes familiar with the AMVR calculation process and downloads the relevant data, the calculations themselves usually take less than a minute or two.

Second, with regard to judges’ resistance to the use of index funds as comparators, I believe that the Brotherston decision and the Restatement (Third) of Trusts clearly establish that index funds, including Vanguard index funds, are “meaningful benchmarks” under the law. The First Circuit and the U.S. District Court for the Southern District of New York17, aka Wall Street’s federal court, have recognized the propriety of benchmarking in connection with 401(k) actions. As a result, I have suggested to attorneys that they should always include a cost-inefficiency claim in their 401(k) actions cases, if for no other reason than to preserve the issue on appeal.

The CommonSpirit decision validates the AMVR and the processes and fiduciary principles upon which it is based. This opinion is based on the Court’s dacknowledgement of the importance of investment costs:

“One feature of the active/passive management debate deserves focus. It is easy for investors at a given time to preoccupy themselves with the present-day or year-to-year value of their portfolio—the part of a financial statement usually placed most squarely in view. But just as compounding can dramatically increase the value of a mutual-fund investment over time, so the costs of that investment can dramatically eat into that investment over time…. Over time, management fees, like taxes, are not trivial features of investment performance.”17

The Sixth Circuit’s acknowledgment of the importance of investment fees and others costs, including the fact that the impact of such fees, like returns, compound over time, cannot be overemphasized. The costs associated with underperformance are obvious and often discussed, both in terms of the financial loss and opportunity costs.

Costs and cost-efficiency generally do not receive the same amount of attention that returns receive. When the Securities and Exchange Commission (SEC) announced and implemented Regulation “Best Interest” (Reg BI), then SEC chairman Jay Clayton acknowledged the importance of cost-efficiency of investments:

rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.18

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.19

The financial services industry quickly announced its opposition to Reg BI. The financial services industry opposition was based largely on the regulation’s requirement that costs must be factored into any investment recommendation provided my brokers.

Section 90, comment h(2) of the Restatement states that that due to higher costs and risks associated with actively managed funds, actively managed funds are imprudent unless it can be objectively estimated that the funds will provide a commensurate return for the additional costs and risks incurred, i.e., are cost-efficient.20

The financial services industry does not like to discuss cost-efficiency, as studies have consistently shown that the overwhelming majority of actively managed mutual funds are cost-inefficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.21

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.22

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.23

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.24

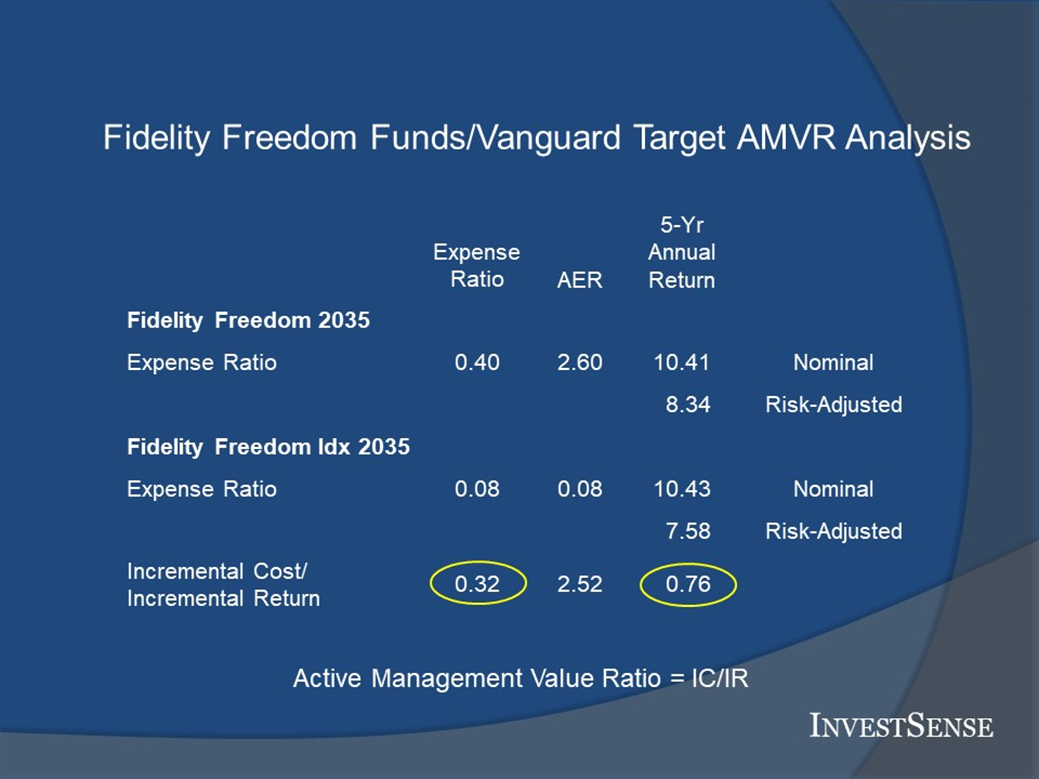

Critics of the AMVR often claim that it is simply a way to promote Vanguard funds. The CommonSpirit decision provided me with an opportunity to discredit that allegation by performing an AMVR forensic fiduciary prudence analysis comparing some of the the Fidelity Freedom active funds to comparable Fidelity Freedom Index funds.

I decided to also perform a similar AMVR fiduciary prudence analysis comparing some of the Fidelity Freedom active funds to comparable Vanguard TDF funds.

In the Fidelity Freedom active/inedx analysis, the active funds failed to provide a positive incremental return. So, arguably, the Fredom Active/Freedom Index AMVR analysis would have helped the plaintiff in the CommonSpirit case establish the cost-inefficiency of the active suite of funds, the “more” that courts keep demanding in meeting the required plausibility pleading standard. Conversely, the Fidelity Freedom active/Vanguard TDF AMVR analysis shows the importance of selecting the appropriate comparator index funds, as using Vanguard’s comparable index funds would have undermined the plaintiff’s case.

Going Forward I would argue that there are several issues with the Sixth Circuit’s CommonSpirit decision. However, I believe the bigger issue in connection with 401(k) litigation and fiduciary in general is the opportunity it provides to divert attention from the active/passive debate and place the attention to a much more meaningful issue, the value of cost-efficiency and the AMVR in assessing fiduciary prudence/ liability and determining damages and in 401(k)/fiduciary actions. The simplicity and straightforward nature of the AMVR, combined with the fact that it is consistent with the fiduciary standards established by the Restatement, suggest that it is a “meaningful benchmark” that so many courts require to meet the federal pleading standards.

The AMVR exposes the irrelevancy of the defenses courts and the financial services industry often cite in 401(k) actions in defense of active management, e.g., differences in strategies, methodolgy, goals. The AMVR counters such arguments and tangential issues, essentially saying “ I do not care HOW you allegedly provided me with a benefit, but whether you actually DID provide me with a benefit at all.”

Businesses use cost-benefit analysis every day. The AMVR is simply the cost/benefit equation using incremental cost and incremental returns as the imputs.

The Brotherston and Leber25 decisions, along with the Restatement effectively rebut any suggestions that index funds, including Vanguard index funds, are not “meaningful benchmarks.” The focus of the courts should be determining whether 401(k) plans provided plan participants with “meaningful choices” within their plans, cost-efficienct investment options that provided genuine benefits to the plan participants and their benefits as required by ERISA.

In closing, I think the validity and the value of the AMVR can be summed up in two relevant quotes. In a 2007 speech at the University of Pennsylvania Law School, Brian G. Cartwright, then general counsel of the SEC, asked his audience to think of an investment in a mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s real holdings. Cartwright told the students,

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund — no overweightings or underweightings — then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?26

The second quote is from John Langbein, who served as the Reporter on the committee that wrote the Restatement (Second) of Trusts over fifty years ago. Shortly after the release of the revised Restatement, Langbein wrote a law review article on the new Restatement. At the end of the article, he made a bold prediction:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.27

I would suggest that that day has arrived and that the AMVR will be an indispensable tool in making both speaker’s predictions become reality for the benefit of both investors and investment fiduciaries.

Notes 1. Smith v. CommonSpirit Health, No. 21-5964, June 21, 2022 (6th Cir. 2022).(CommonSpirit) 2. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Circuit 2018)(Brotherston) 3. Hughes v. Northwestern University, 142 S.Ct. 737 (2022) 4. Brotherston, 37 5. Brotherston, 34 6. Brotherston, 39 7. CommonSpirit, II.A 8. CommonSpirit, II.A 9. CommonSpirit, II.A 10. CommonSpirit, II.A 11. CommonSpirit, II.A 12. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online at https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 13. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm 14. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 15. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926 16. Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study”), http://www.gao.gov/new.item/d0721.pdf 17. CommonSpirit, I.A 18. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G.Cartwright).(SEC Speech) http://www.sec.gov/news/speech/2007/spch102407bgc.htm 19. SEC Speech 20. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt h(2). 21. Laurent Barras, Oliver Scaillet, and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANE 179, 181 (2010) 22. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, https://www.ft.com/content/6b2d5490-d9bb-eb37a6aa8e 23. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE 57-58 (1997) 24. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Funds Advisors, L.P., August 2016 25. Leber v. Citigroup 401(k) Plan Inv. Committee, 2014 WL 4851816 26. SEC Speech: The Future of Securities Regulation: Philadelphia, Pennsylvania: October 24, 2007 (Brian G. Cartwright). http://www.sec.gov/news/speech/2007/spch102407bgc.htm 27. John H. Langbein and Richard A. Posner, Measuring the True Cost of Active Management by Mutual Funds, Journal of Investment Management, Vol 5, No. 1, First Quarter 2007 http://digitalcommons.law.yale.edu/fss_papers/498

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

I am on record as saying that (a) ERISA plaintiff’s attorneys should never lose a properly vetted 401(k)/403(b) action, and (b) the amount of 401(k)/403(b) litigation is going to continue to increase. Those opinions are based on three trends within those industries.

1. Many plan sponsors do not even realize that they are fiduciaries. A J.P. Morgan survey found that 43% of plan sponsors surveyed were not aware that they are plan fiduciaries.1 Subsequent studies suggest that the problem still persists. It is highly unlikely that plan sponsors who do not even realize that they are fiduciaries realize what their fiduciary duties are in compliance with same.

1. Why do you offer so many investment options within the plan? 2. Why do you offer these specific investment options?

Far too often, the response is either “that’s what our plan adviser told us to do” or a simple shrug of the shoulders. My response – “What you are actually doing is unnecessarily exposing yourself to potential fiduciary liability. Simplicity is the new sophistication.”

Most plans try to qualify for ERISA 404(c) status in order to reduce their liability exposure. There are approximately 20-25 requirements that a plan must satisfy in order to qualify for 404(c) status. Fred Reish, one of the nation’s leading ERISA attorneys, has stated that many plans mistakenly believe that they have satisfied 404(c)’s requirements.

One thing has always fascinated me about the language in 404(c)’s requirements:

(3)Broad range of investment alternatives.

(i) A plan offers a broad range of investment alternatives only if the available investment alternatives are sufficient to provide the participant or beneficiary with a reasonable opportunity to:

(A) Materially affect the potential return on amounts in his individual account with respect to which he is permitted to exercise control and the degree of risk to which such amounts are subject;

(B)Choose from at least three investment alternatives:

(1) Each of which is diversified;

(2) Each of which has materially different risk and return characteristics;

(3) Which in the aggregate enable the participant or beneficiary by choosing among them to achieve a portfolio with aggregate risk and return characteristics at any point within the range normally appropriate for the participant or beneficiary; and

(4) Each of which when combined with investments in the other alternatives tends to minimize through diversification the overall risk of a participant’s or beneficiary’s portfolio…. (emphasis added)2

A valid argument can be made that a plan could comply with the three investment alternatives requirement simply with a plan consisting of a broad-based equity index fund, a broad-based fixed income index fund, and a money market fund. I would suggest that a plan at least add a broad-based international index fund to this three-investment plan, and possibly one or two other funds.

Many plan advisers have told me that this type of simplified plan is absurd and will expose plan sponsors to liability, that their 15-20 investment options plans are absolutely compliant and legally appropriate. To that, I respond with my friend Rick Ferri’s quote–“Complexity is just job security.”

When it comes to designing 401(k)/403(b) plans, the adage “less is more” definitely holds true as far as exposing plan sponsors to unnecessary liability. As the Supreme Court recently pointed out, each individual investment must be prudent.3 Consequently, the more investment options a plan offers, the greater the chances of a breach of the plan sponsor’s fiduciary duties.

Another issue I often see is plan sponsors mistakenly believing that they have a duty to ensure the ultimate performance of the investment options chosen for a plan. A plan sponsor’s fiduciary duties only involve the prudent selection of the plan’s investment options, not the eventual performance of such investments. Again, another example of plan sponsors making compliance with ERISA more difficult than it actually is, which provides a nice transition into my third point.

3. The Reg BI “reasonably available alternatives” vs. ERISA “fiduciary prudence” liability trap. 401(k) and 403(b) plans often hire third-parties to help them in administering the plan. These consultants are often what are known as 3(21) or 3(38) fiduciaries. While a lengthy discussion of the differences between the two is beyond the scope of this post, a simplified explanation is that a 3(21) adviser provides investment advice, while a 3(38) adviser provides investment management.

These consultants are often stockbrokers or dually registered stockbrokers/investment adviser representatives. Under Regulation “Best Interest”4 (Reg BI), the SEC’s new standard of conduct for stockbrokers, the stockbroker is required to always put a customer’s best interest first and to consider various factors, including the cost associated with any product recommendations.

In deciding on investment recommendations, a stockbroker is required to consider and compare “reasonably available alternatives.” However, as the saying goes, “the devil is in the details.”

In the Proposing Release, we provided guidance on what types of recommendations would or would not be in the best interest of a particular retail customer. In particular, the Proposing Release stated that where a broker-dealer is choosing among identical securities available to the broker-dealer, it would be inconsistent with the Care Obligation to recommend the more expensive alternative for the customer. Similarly, in the Proposing Release, we noted our belief that it would be inconsistent with the Care Obligation if the broker-dealer made a recommendation to a retail customer in order to: maximize the broker-dealer’s compensation, further the broker-dealer’s business relationships,…”5

We also stated that under the Care Obligation a broker-dealer generally should consider reasonable alternatives, if any, offered by the broker-dealer in determining whether it has a reasonable basis for making the recommendation….6

Further, the Proposing Release indicated that under the Care Obligation, when a broker-dealer recommends a more expensive security or investment strategy over another reasonably available alternative offered by the broker-dealer,….(emphasis added)7

And yet, I would argue that that is exactly what is happening by allowing plan advisers to artificially restrict their recommendations to the investment menu offered by their broker-dealer, to investments that benefit the plan adviser’s broker-dealer’s preferred providers.

“Open architecture” refers to an investment platform where a stockbroker can offer a wide variety of investment products, including no-load and index funds. Most of the major broker-dealers do not operate on an open architecture platform. Most broker-dealers usually restrict investment recommendations to the products offered by their “preferred providers,” mutual fund companies and other product vendors who have either paid for or arranged special deals for the privilege of accessing the broker-dealer’s stockbrokers.

The problem with this arrangement and Reg BI’s qualifying language, “reasonably available alternatives offered by the broker-dealer,” is that the investment products offered by preferred providers are often overpriced, consistently underperforming, i.e., cost-inefficient, products, the antithesis of both ERISA’s fiduciary prudence and loyalty requirements, as well as Reg BI’s goals.

Further complicating the situation is that plan sponsors often blindly rely on their plan adviser’s recommendations, even though the courts have consistently ruled that such blind reliance is a breach of a plan sponsor’s fiduciary duties, especially when commissioned salespeople are involved.

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.8

A determination whether a fiduciary’s reliance on an expert advisor is justified is informed by many factors, including the expert’s reputation and experience, the extensiveness and thoroughness of the expert’s investigation, whether the expert’s opinion is supported by relevant material, and whether the expert’s methods and assumptions are appropriate to the decision at hand. One extremely important factor is whether the expert advisor truly offers independent and impartial advice.9 Defendants relied on FPA, however, and FPA served as a broker, not an impartial analyst. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.10

A 3(21) adviser is technically a co-fiduciary with the plan sponsor. However, 3(21) advisers routinely insert fiduciary disclaimer clauses in their advisory contracts in attempt to avoid any fiduciary liability exposure, perhaps knowing the true quality of the advice they are going to provide to a plan.

Addressing the Reg BI/ERISA Fiduciary Duties “Trap” Perhaps the best advice on how plan sponsors should address the reasonably available alternatives/fiduciary prudence liability gap was offered by Judge Kayatta in the Brotherston decision.

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss incurred as a result.11

The Brotherston decision and the Solicitor General’s amicus brief in connection with Putnam Investment’s application for review by the Supreme Court provide an excellent overview of a plan sponsor’s fiduciary duties. I wrote a post on fiduciary prudence in a post-Brotherston 401(k) world.12

Further support for this position can be found in the studies which have consistently concluded that the overwhelming majority of actively managed funds are not cost-efficient.

99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.13

[I]ncreasing numbers of clients will realize that in toe-to-toe competition versus near-equal competitors, most active managers will not and cannot recover the costs and fees they charge.14

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.15

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.16

One of the key points in Reg BI was the requirement that stockbrokers would be required to factor in the costs associated with any investment product recommendations. The release announcing the adoption of Reg BI supported the importance of cost-efficiency, stating that

A rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest expected net benefit in light of the investor’s investment objective that maximizes expected utility.17

This simply reiterates comments on the importance of cost-efficiency from Section 90 of the Restatement. The Restatement establishes a number of fiduciary standards with regard to a fiduciary’s duty of prudence. Three of the key standards are

a fiduciary has a duty to be cost-conscientious in investing.18

a fiduciary has a duty to seek the highest return for a given level of cost and risk or, conversely, the lowest level of cost and risk for a given level of return.19

that due to higher costs and risks associated with actively managed funds, actively managed funds are imprudent unless it can be objectively estimated that the funds will provide a commensurate return for the additional costs and risks incurred, i.e., are cost-efficient.20

Nevertheless, the fact is that actively managed mutual funds still dominate 401(k) and 403(b), largely because, as the Gregg quote noted, those are the investment products stockbrokers recommend, primarily from their broker-dealer’s preferred provider list.

Fortunately, there are some simple steps that plan sponsors can take to protect themselves and their plan participants. First, do not sign any advisory contract that includes a fiduciary disclaimer clause. These clauses are often subtle and buried within an advisory contract. If a plan sponsor has any questions, they should consult with an experienced ERISA plaintiff’s attorney.

Second, the Active Management Value Ratio (AMVR) metric provides a free and simple tool that plan sponsors can use to detect cost-inefficient investment recommendations. Plan sponsors should assess the cost-efficiency of any recommended investment option using a universal “reasonably available alternatives” menu, not Reg BI’s unduly restricted “reasonably available alternatives” standard.

The AMVR is simple and straightforward, requiring only the ability to compare the data between an actively managed fund and a comparable index fund by simple subtraction. A plan sponsor, or any other investment fiduciary, then just has to answer two simple questions:

Did the actively managed fund provide a positive incremental return?

If so, did the actively managed fund’s incremental return exceed the fund’s incremental costs?

If the answer to either question is “no,” then the actively managed fund is cost-inefficient, i.e., imprudent, relative to the comparable index fund and should be avoided.

That has always been my advice to plan sponsors. However, a reader of our “The Prudent Investment Adviser Rules” blog and a member of his plan’s investment committee recently sent me an email asking me whether I thought a plan adviser should provide an AMVR analysis for every recommendation they make. I believe that would be a reasonable request to better protect the plan; but that it is highly unlikely that they would do so using the exact AMVR format, especially using the correlation-adjusted costs. The AMVR quickly exposes cost-inefficient investments.

In his case, the plan adviser actually did provide an AMVR analysis based on the nominal numbers, but substituted some strange analysis in lieu of a correlation-adjusted analysis based on the Active Expense Ratio. The AMVR, as constructed, is the investment industry’s worst nightmare, as it forces a plan adviser to provide greater transparency, which is the financial services’ kryptonite.

Going Forward As I mentioned at the start of this post, I am on record as saying that (a) ERISA plaintiff’s attorneys should never lose a properly vetted 401(k)/403(b) action, and (b) the amount of 401(k)/403(b) litigation is going to continue to increase. My job as a fiduciary risk management counsel is to alert my clients to such trends and teach them how to minimize their exposure to liability and litigation.

A key to accomplishing these goals is to make sure that plan sponsors truly understand what their fiduciary duties do, and do not, require. Fortunately, compliance with ERISA is just not that complicated if a proper system of policies and procedures is created and properly maintained.

Not much has been written about the fiduciary liability trap created by the disconnect between Reg BI’s “reasonably available alternatives offered by the broker-dealer” language and ERISA’s fiduciary prudence and loyalty requirements. The seriousness of this gap in compliance language and its potential consequences cannot be overstated, especially with the Department of Labor reportedly considering implementing its own fiduciary guidelines, including incorporating the provisions of Reg BI.

Far too often regulators have “dropped the ball” when it comes to protecting investors and employees against the very abuses that the securities regulations and ERISA were created to prevent. While many may have overlooked the potential implications of Reg BI’s cleverly drafted “reasonably available alternatives” language, it is imperative that plan sponsors recognize the issues discussed herein in order to protect both themselves and their plan participants.

Caveat fiduciarius

Notes 1. https://www.prnewswire.com/news-releases/jp-morgan-defined-contribution-survey-shows-plan-sponsors-aiming-to-strengthen-plans-finds-fiduciary-misperceptions-remain-300495423.html. 2. 29 CFR §2550.404c-1 – ERISA Section 404(c) Plans 3. Hughes v. Northwestern University, 4. SEC Release 34-86031, Regulation Best Interest: The Broker-Dealer Standard of Conduct (Reg BI), 278 5. Reg BI, 279. 6. Reg BI, 279. 7. Reg BI, 285. 8. Liss v. Smith, 991 F. Supp. 278, 291 (S.D.N.Y. 1988). 9. Gregg v. Transportation Workers of America Int’l, 343 F.3d 833, 841-42. (Gregg) 10. Gregg, 841-42. 11. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 39 (1st Cir. 2018) 12. “Plan Sponsor Special Report: 401(k) Fiduciary Liability Risk Management in a Post-Brotherston World” https://bit.ly/3Q3MEkK 13. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 14. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 15. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997). 16. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 17. Reg BI, 378. 18. RESTATEMENT (THIRD) TRUSTS, (American Law Institute),Section 90, cmt b. 19. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt f. 20. RESTATEMENT (THIRD) TRUSTS, (American Law Institute), Section 90, cmt h(2).

The financial services industry likes to use charts…a lot of charts. Attorneys do not like charts. Charts can be confusing and misleading, sometimes deliberately so. One judge told me that after I had argued the connection between charts and “weaseleze,” in a trial, he always grinned when an attorney tried to introduce a chart.

I tend to use the terms “weasel words” and “weaseleze” a lot. The terms come from Scott Adams’ book, “Dilbert and the Way of the Weasel.” Adams defines weaseleze as

Words that make perfect sense when individually, but when artfully arranged, they become misleading or impenetrable. Weaseleze is often used in advertising, legal work, employee performance reviews, and dating.1

One of the services I provide is fiduciary oversight services. Part of those services includes a forensic fiduciary audit. I tend to see a lot of weaseleze during such audits, often in connection with charts and diagrams. Lee Munson, author of “Rigged Money,” best described the use of weaseleze in connection with charts and diagrams with his phrase “the lie of the pie,”2

During a recent fiduciary audit of a 401(k) plan, the chairman of the investment committee politely questioned my findings, stating that they had followed the recommendations of their plan adviser.

I asked to see the documentation that the plan adviser had provided to the plan. I immediately recognized an ad that the adviser had provided in support of his recommendations. The ad is one used by a major mutual fund company claiming that their funds have beaten S&P 500 Index funds over an extended period of time.

I reminded the investment committee that they have a fiduciary duty to conduct their own objective investigation and evaluation of the funds chosen for their plan. Then I explained why mutual fund companies choose ads comparing their funds to market indices, rather than comparable index funds, knowing that they are arguably misleading.

First, the S&P 500 Index is technically classified as a large cap blend index. Prior to the Hughes v. Northwestern University (Northwestern) decision, the 401(k) industry, the investment industry, and even some courts objected to any comparison between actively managed funds and index funds, claiming that such comparisons were improperly comparing “apples and oranges.”

The Northwestern finally discredited such arguments. However, the use of the S&P 500 Index, or any other market index, to benchmark funds that are inconsistent with a fund’s classification is obviously comparing “apples and oranges.” This often results in misleading comparisons and potential liability exposure for plan sponsors and other investment fiduciaries.

Second, I have seen ads where the mutual fund company’s ads compare their funds to the S&P 500 Index’s returns without including the reinvestment of the Index’s dividends. Historically, over 40 percent of the Index’s returns can be attributed to the reinvestment of its dividends.

Excluding dividends in performance illustrations obviously creates misleading comparisons.

Over the ten-year period 2012-2021, the total return of the S&P 500 Index without the reinvestment of dividends was 251.67 percent (13.40 percent annualized) versus 325.33 percent with reinvestment of dividends (15.57 percent annualized).

Over the twenty-year period 2002-2021, the total return of the S&P 500 Index without the reinvestment of dividends was 301.13 percent (7.193 percent annualized) versus 488.87 percent with reinvestment of dividends (9.27 percent)

One mutual fund company is known for consistently engaging in this practice. Fortunately, their charts immediately raise red flags for attorneys and fiduciaries to investigate.

Finally, the decision to benchmark against market indices rather than comparable market indices suggests that the fund company is trying to prevent plan sponsors and other investment fiduciaries from performing a cost-efficiency evaluation of their funds.

Section 90 of the Restatement sets out several relevant cost-efficiency standards in determining whether a fiduciary has fulfilled its fiduciary duty of prudence, including

A fiduciary has a duty to be cost-conscious.3

In selecting investments, a fiduciary has a duty to seek either the highest level of a return for a given level of cost and risk or, inversely, the lowest level of cost and risk for a given level of return.4

Due to the impact of costs on returns, fiduciaries must carefully compare funds’ costs, especially between similar products.5

Due to the higher costs and risks typically associated with actively managed mutual funds, a fiduciary’s selection of such funds is imprudent unless it can be shown that the fund is cost-efficient.6

The fact that mutual fund companies and plan advisers would attempt to avoid cost-efficiency comparisons is not surprising. Studies have consistently concluded that the overwhelming majority of actively managed mutual funds are not cost-efficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.7

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.8

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.9

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.10

What is troubling from a legal standpoint is that a plan adviser would knowingly try to expose their client, the plan, to unnecessary fiduciary liability exposure. While they typically feign surprise when they are confronted with this evidence, they known exactly what they are doing.

More often than not, their advisory contract with the plan also includes a fiduciary disclaimer clause. Fortunately for plans, the Supreme Court has ruled that such clauses do not prevent plans from suing plan advisers.

The Active Management Value Ratio™3.0 For all the foregoing reasons, I advise my fiduciary compliance clients to simply ignore any and all mutual fund ads and perform their own fiduciary compliance analyses using the Active Management Value Ratio (AMVR).

Based upon the Restatement and the studies of investment icons such as Nobel laureate Dr. William F. Sharpe and Charles D. Ellis, I created a simple metric, the Active Management Value Ratio™ (AMVR), that allows investors, investment fiduciaries and attorneys to quickly determine the cost-efficiency of an actively managed mutual fund.

In analyzing an investment option, Nobel laureate William F. Sharpe has noted that

[t]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.11

Building on Sharpe’s theory, investment icon Charles D. Ellis has provided further advice on the process used in evaluating the cost-efficiency of an actively managed mutual fund.

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns.

When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!12

The AMVR metric provides extremely useful information regarding the cost-efficiency of an actively managed mutual fund using just a fund’s nominal, or publicly reported, costs and returns. However, an investor’s analysis should not end there if they want a truly accurate cost-efficiency analysis of an actively managed mutual fund.

There is a direct, negative relationship between a fund’s r-squared correlation number, a fund’s incremental costs, and the fund’s cost-efficiency. Morningstar states that “r-squared reflects the percentage of a fund’s movements that are explained by movements in its benchmark index, [rather than any contribution by the fund’s management team.]”13

Professor Ross Miller did a study on the impact of closet indexing, focusing primarily on the relationship between an actively managed mutual fund’s R-squared number, “closet index” status, and the resulting overall financial impact of the two. “Closet index” funds are actively managed funds whose returns are essentially the same as a comparable index fund, but who charge much higher fees than the index fund. The higher an actively managed fund’s r-squared number, the greater the likelihood that the actively managed fund can be classified as a closet index fund.

An r-squared rating of 98 would indicate that 98 percent of an actively managed mutual fund’s returns could be attributed to the performance of a comparable index fund rather than the active fund’s management team.

In fairness, Professor Miller has noted that there is not a one-to-one correlation between an actively managed fund’s r-squared number and the percentage of the active management provided.

There is no universally agreed upon level of r-squared that designates an actively managed mutual fund as a closet index fund. I use an R-squared correlation number of 90 as my threshold indicator for closet index status.

Miller’s findings were extremely interesting, namely that

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.11

As a result of his study, Ross Miller, created the Active Expense Ratio (AER) metric. A fund’s AER number is based on a fund’s r-squared number.

Since many investors are unfamiliar with the AER metric, a frequent question I receive is why even calculate an AER-adjusted AMVR. One of the benefits of calculating an actively managed fund’s AER number is that the calculation process results in calculating the actual percentage of active management provided by the actively managed fund in question. Miller refers to this measurement as a fund’s “active weight.14

Deriving a fund’s “active weight” number provides valuable insight into the amount of active management provided by a fund purporting to provide active management, especially since such funds higher fees are based on the purported benefits of active management. However, Miller claims the primary benefit of calculating a fund’s AER number is that the AER provides investors with a quantitative analysis of the implicit cost of the fund’s active management component. The AER accomplishes this by simply dividing an actively managed fund’s incremental cost by the fund’s active weight number.

In many cases, once a fund’s r-squared correlation number is factored in, the fund’s AER is significantly higher than the fund’s stated expense, often as much as 400-500 percent higher. Investors and investment fiduciaries should remember John Bogle’s advice on investment costs, “you get what you don’t pay for,” as well as the fact that simple mathematics proves that each one percent in fees and expenses reduces an investor’s or fiduciary’s end-return by approximately seventeen percent over a twenty-year time period.

Once AMVR is calculated for an actively managed fund, the investor or fiduciary only needs to answer two simple questions:

(1) Does the actively managed mutual fund provide a positive incremental return relative to the benchmark being used?

(2) If so, does the actively managed fund’s positive incremental return exceed the fund’s incremental costs relative to the benchmark?

If the answer to either of these questions is “no,” the actively managed fund is both cost-inefficient and unsuitable/imprudent according the the Restatement’s prudence standards and should be avoided. The goal for an actively managed fund is an AMVR number greater than “0” (indicating that the fund did provide a positive incremental return), but equal or less than “1” (indicating that the fund’s incremental costs did not exceed the fund’s incremental return).

Prudent plan sponsors and other investment fiduciaries do not knowingly waste money by offering and/or investing in cost-inefficient investments. It may require a little more work, but by using the AMVR metric, alone or in combination with Miller’s AER metric, investors can better protect their financial security and investment fiduciaries can hopefully avoid unnecessary personal liability exposure.

Going Forward

Facts do not cease to exist because they are ignored. Aldoux Huxley

As one commentator noted in 1976 after the Restatement (Second) Trusts was released made the following observation:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.15

Over forty years later, the First Circuit echoed such sentiments in the Brotherston decision, when it offered the following advice:

Moreover, any fiduciary of a plan such as the plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”16

One of the rewarding things about my posts is receiving constructive feedback from readers. A member of a plan investment committee recently wrote me a very nice email, including the following questions and comment:

In your opinion, should our advisor provide [AMVR] calculations as part of their service?

[The AMVR] should be THE comparison that every investor uses to evaluate a fund.

My response as to requiring plan advisors to provide AMVR analyses on their recommendations has, and always be, yes. Why would any plan adviser refuse to provide such simple analyses unless they are not committed to putting a client’s best interests first?

However, insist that they follow the AMVR format used by InvestSense, including risk-adjusted returns and correlation-adjusted costs, using the Active Expense Ratio. In most cases they will provide the calculations based on nominal returns and costs, but they refuse to provide the adjusted data.

As for the AMVR being THE leading metric for complying with one’s fiduciary prudence duty, let’s just say I’m obviously biased. For what it is worth, more fiduciaries and attorneys are reportedly using the metric.

Copyright InvestSense, LLC 2022. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

The legal requirement for prudence, as defined in ERISA Section 404(a)(1)(B), is for a fiduciary to discharge his or her duties with:

“the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”

But what does that really mean?

[R]ather than explicitly enumerating all of the powers and duties of trustees and other fiduciaries, Congress invoked the common law of trusts to define the general scope of their authority and responsibility.”1

Thus, a federal common law based on the traditional common law of has developed and is applied to define the powers and duties of ERISA plan fiduciaries….2

OK, getting closer.

The two consistent themes throughout the Restatement are cost-consciousness/cost-efficiency and risk management through effective diversification. Section 90 of the Restatement, more commonly known as the Prudent Investor Rule, contains three comments that could, and should, define prudence in future ERISA excessive fees/breach of fiduciary duty actions.

A fiduciary has a duty to be cost-conscious. (Introductory Section to Section 90)

A fiduciary has a duty to select mutual funds that offer the highest return for a given level of cost and risk; or, conversely, funds that offer the lowest level of costs and risk for a given level of return. (cmt. f)

Actively managed mutual funds that are not cost-efficient, that cannot objectively be projected to provide a commensurate return for the additional costs and risks associated with active management, are imprudent. (cmt. h(2)).

I collectively refer to these three comments as the “fiduciary prudence trinity.”

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.3

Nobel laureate Dr. William Sharpe has offered the following advice for analyzing the prudence of mutual funds:

Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs…. The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative”4

Noted wealth management expert, Charles D. Ellis, goes further, stating that

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!5

Cumulatively, I submit that these comments and quotes suggest that the best way to prove compliance with one’s fiduciary duties is to quantify such duties. The Active Management Value Ratio™ (AMVR) metric provides a simple way of proving compliance with these fiduciary prudence standards.

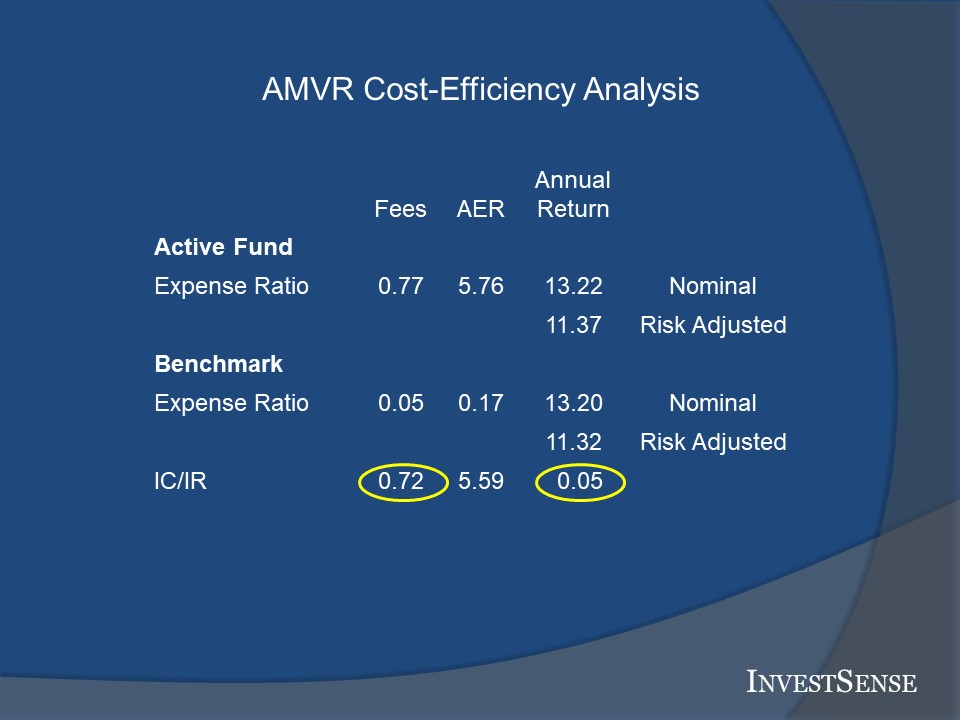

The AMVR analysis shows that the actively managed fund produced a positive incremental return of five basis points at an incremental cost of 72 basis points. As we all learned in our basis economics classes, any situation where costs exceed benefits is not a prudent is not a prudent choice.

I am often asked why the AMVR uses adjusted returns. As the Restatement pointed out, an actively managed fund or a strategy that employs active management is only prudent if an investor receives a commensurate return for the additional risks and costs typically associated with active management.

Another questions I often receive is what is the purpose of the “AER” column. AER stands for Active Expense Ratio, the metric created by Ross Miller. The AER factors the correlation of returns between an actively managed fund and a comparable index fund to determine the effective expense ratio of an actively managed fund.

So why calculate an actively managed fund’s correlation-adjusted expense ratio? As Miller explains,

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funds engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.6

While the calculation methodology for the AER can be intimidating, the AER essentially divides an actively managed fund’s incremental costs by its “active weight.” The active weight is a metric created by Miller to determine the true amount of active management provided by an allegedly actively managed fund.

Based upon my experience, formerly as a securities/RIA compliance officer and now as a securities/ERISA attorney and fiduciary compliance consultant, financial advisers and plan advisers rarely discuss or provide AER numbers in connection with their recommendations. That is exactly why InvestSense includes AER data in its forensic fiduciary analyses, to help fiduciaries aware of potential fiduciary liability issues and the need for additional risk management.