The number of 401(k)/403(b) cases continues to grow. And it will continue to do so unless and until plan sponsors take the time to truly understand their legal responsibilities and adjust their plans accordingly.

I am on record as saying that plan participants should never lose a 401(k)/403(b) breach of fiduciary action if their attorneys properly plead their action. After the recent SCOTUS decision in Hughes v. Northwestern University (Northwestern), that opinion has only grown stronger.

First, the Northwestern, decision is the final piece of what I have termed the “fiduciary responsibility trinity” (Trinity). Together with the earlier decisions in Tibble v. Edison International and Brotherston v. Putnam Investments, LLC, the Northwestern decision provides a simple blueprint for both effectively litigating 401(k)/403(b) actions and for preventing such actions.

Second, the fiduciary breach actions continue to demonstrate that plan sponsors simply do not understand what their fiduciary responsibilities truly are and how easy it is to comply with same to avoid unnecessary and unwanted fiduciary liability exposure.

In college, my minor was psychology. My thesis was on heuristics, cognitive biases and the decision-making process. I have always been fascinated by the way the mind works.

As I monitor the ongoing legal developments regarding fiduciary liability, I am amazed at the failure, or refusal, of fiduciaries to simplify their responsibilities by focusing on creating “win-win” plans, plans which are in the plan participants’ best interests while protecting the plan sponsor from legal liability.

Nobel Laureate Daniel Kahneman’s best seller, “Thinking Fast and Slow,” offers a valuable insight into why the fiduciary liability crisis exists and how it can be avoided. Click here to view a 2-minute analysis of Kahneman’s thoughts.

When I created the Active Management Value Ratio™ (AMVR) metric, it was based on these same principles and how the metric could help both fiduciaries and attorneys address the current fiduciary responsibility disconnect.

Heuristics and Cognitive Biases

Let me begin by saying that what I am about to write is neither intended to, nor does, provide a detailed discussion. For those desiring to learn more about the subject, especially in connection with investing, simply search online using the search term, “heuristics and investment decision-making.” There are plenty of interesting articles addressing the issue.

Heuristics are essentially mental shortcuts that we take in making decisions. The bat/paddle and ball analogy is an excellent example of how we use heuristics to simplify the decision-making process, the intuitive or “fact thinking” process.

The problem that a decision-maker must consider is that heuristics can often result in errors due to the influence of cognitive biases that may influence a decision-maker’s judgment. Common cognitive biases that influence decisions include

- Confirmation bias – the tendency to give greater weight to information that confirms our existing beliefs.

- Anchoring bias – the tendency to put greater emphasis on and credibility to the first piece of information that we hear.

- “Halo effect” – the tendency for an initial impression of a person to influence the overall and ongoing opinion we have of them.

Based upon my experience, these three cognitive biases often come into play in the fiduciary decision-making process. The most notable example of this is the refusal of plan sponsors to listen to anyone other than their existing plan advisers and their refusal to consider alternative options.

Heuristics and the Active Management Value Ratio™

As I mentioned, heuristics and cognitive biases were a primary consideration when I created the AMVR metric. As the video points out, the impact/influence of large numbers is a well-known cognitive bias.

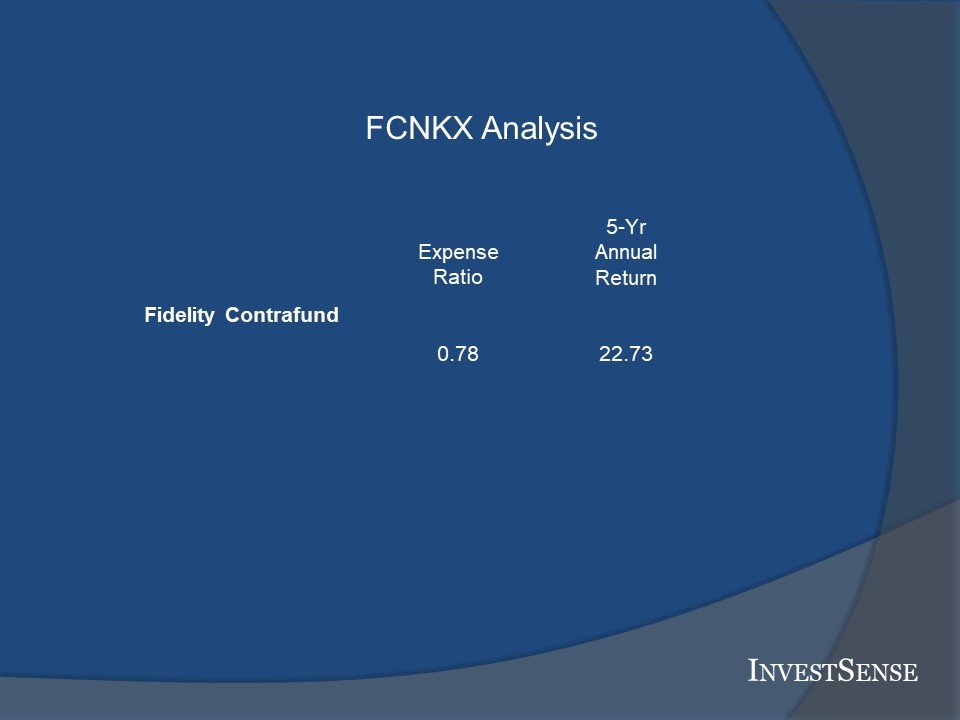

What would be your initial reaction if I were to recommend this investment option for your 401(k)/403(b) plan?

22.73 percent return with an expense ratio of 78 basis points. 22.73 vs. 0.78. The immediate, intuitive reaction would most likely be very positive.

Now, what would be your reaction if you were presented with the following AMVR forensic analysis slide?

Hopefully, a plan sponsor’s rational, “slow thinking” decision-making side would quickly convince them that Fidelity Contrafund is not the optimum choice for their plan relative to the comparable index fund. Again, an optimum choice would be one which advances the best interests of plan participants and protects a plan sponsor against unnecessary and unwanted fiduciary liability exposure.

Unfortunately, the continuing increase in 401(k) /403(b) actions and multi-million-dollar settlements suggests that too many plan sponsors are using an intuitive, “fast thinking approach to fiduciary decision-making instead of a rational, “slow thinking” approach, resulting in greater liability exposure.

Going Forward

I recently gave a presentation of my new concept, “The 401(k) Fiduciary Responsibility Blueprint™” to several investment fiduciaries. The concept combines my “fiduciary responsibility trinity” and “fiduciary prudence trinity” concepts with the impact of heuristics and cognitive biases on the fiduciary decision-making process.

To be honest, I was somewhat surprised, but encouraged, by the overwhelmingly positive response, with several attendees asking for follow-up sessions. While 401(k)/403(b) litigation continues to receive the most attention, the issues discussed herein apply to all investment fiduciaries. Unless and until investment fiduciaries acknowledge and address these decision-making shortfalls, they will continue to be targets for fiduciary litigation actions.

You must be logged in to post a comment.