James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

For years, the annuity industry has attempted to gain greater access to plan participants’ accounts within 401(k) and 403(b) retirement plans. The industry has tried to counter the fiduciary prohibition against the receipt of commissions with versions of annuities that do not pay commissions to fiduciaries. Furthermore, the industry recently lobbied Congress to provide plan sponsors further incentives to offer annuities within plans. The SECURE Act provides a potential safe harbor against fiduciary liability for plan sponsors offering annuities within their plans in the event that the annuity issuer is subsequently unable to honor its legal obligations to plan participants. Protection for the plan sponsors, but not for the plan participants.

What the annuity industry either does not know or knows but refuses to acknowledge, aka “willful ingnorance,” is that there are other significant potential liability issues with annuities that investment fiduciaries should be aware of, issues that, left unaddressed, effectively make most annuities potential fiduciary liability traps for plan sponsors and other investment fiduciaries.

I previously addressed a number of legal issues that potentially make annuities fiduciary liability traps for plan sponsors in an earlier post, The post generated, and continues to generate, inquiries from plan sponsors and other investment fiduciaries on both fiduciary risk management vis-a-vis annuities and the topic of fiduciary risk management in general.

What concerns me is that I see disturbing situations developing in the annuity industry’s campaign to offer more annuity products within pension plans. My experience has been that plan sponsors often do not truly understand their legal obligations as fiduciaries, what is and is not required of them. Given the financial services industry’s and the insurance/annuity industry’s adamant opposition to meaningful transparency, plan sponsors should have no expectation of same from such industries.

For example, both industries relentlessly publish studies and related articles stating that polls claim that plan participants are interested in products offering “guaranteed income” and promoting “retirement readiness,” “financial wellness,” or another buzzword. Such industry articles should have no influence on a prudent plan sponsor.

Neither ERISA, the Restatement of Trusts (Restatement), nor the common law of trusts requires that a plan sponsor, or any other investment fiducairy for that matter, offer a specified type of investment. The three sources cited only require that the plan sponsor only offer investment options that are legally prudent, investment products that are truly in the best interest of the plan participants.

And yet, most plan sponsors do not understand that fact since most have never read either ERISA and/or the Restatement or consulted with an ERISA attorney. As a result, they can be easily misled, whether intentionally or unintentionally, to engage in unnecessary activity that is not required of them and toward goals they cannot possibly achieve, activity that can actually result in unnecessary and unwanted fiduciary liability exposure.

As a fiduciary risk management counsel, my job is to explain the potential fiduciary liability pitfalls to plan sponsors in order to avoid unnecessary liability exposure. In my presensentations, I focus on three areas: (1) a plan sponsor’s duty to independently and objectively investigate and evaluate each investment option within a plan, (2) a plan sponsor’s actual fiduciary duties under ERISA Section 404(a) to know and factor in the the material facts discovered as a result of performing their legally required investigation and evaluation, and (3) ERISA Section 404(c)’s “adequate information to make an informed decision” requirement for Section 404(c)’s safe harbor protection.

The first thing I tell my fiduciary risk management clients is not to worry about getting sued. Anyone who can pay the necessary filing fees can sue anyone they want. My value proposition to my clients is the ability to review their plan in terms of legal compliance to ensure that their plan is properly designed and maintained so that if they do get sued, they should not lose the case. Those are the issues that investment fiduciaries should focus on.

I created the following diagram to help my fiduciary risk management clients understand the basic legal liability issues involved in fiduciary law.

Fiduciary law is essentially a combination of three types of law – trust law, agency law, and equity law. Trust law and agency law track each other in many ways since they deal with duties owed by a fiduciary representing the legal interests of their beneficiaries (trust law) and/or principals (agency law).

Two key fiduciary duties are the duties of prudence and loyalty. Borrowing from both the common law of trusts and the Restatement of Trusts, ERISA describes the duties of prudence and loyalty as follows:

[A] fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan; and with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.1

With regard to the consideration of an investment or investment course of action taken by a fiduciary of an employee benefit plan, the requirements of section 404(a)(1)(B) of the Act are satisfied if the fiduciary:

(i) Has given appropriate consideration to those facts and circumstances that, given the scope of such fiduciary’s investment duties, the fiduciary knows or should know are relevant to the particular investment or investment course of action involved, including the role the investment or investment course of action plays in that portion of the plan’s investment portfolio or menu with respect to which the fiduciary has investment duties; and

(ii) Has acted accordingly.2 (emphasis added)

(2) For purposes of paragraph (b)(1) of this section, “appropriate consideration” shall include, but is not necessarily limited to:

(i) A determination by the fiduciary that the particular investment or investment course of action is reasonably designed, as part of the portfolio (or, where applicable, that portion of the plan portfolio with respect to which the fiduciary has investment duties) or menu, to further the purposes of the plan, taking into consideration the risk of loss and the opportunity for gain (or other return) associated with the investment or investment course of action compared to the opportunity for gain (or other return) associated with reasonably available alternatives with similar risks;3 (emphasis added)

Fiduciary prudence focuses on the process used by a plan sponsor in investigating and evaluating the investment products chosen for a plan, not the eventual performance of the product. In assessing the process used by a plan sponsor, the courts evaluate prudence in terms of both procedural and substantive prudence.

Procedural prudence focuses on whether the fiduciary utilized appropriate methods to investigate and evaluate the merits of a particular investment. Substantive prudence focuses on whether the fiduciary took the information from the investigation and made the same decision that a prudent fiduciary would have made. Note the requirement is would have made, not could have made.

Fiduciary Duty to Conduct Independent Investigation and Evaluation

The courts have consistently held that plans have a fiduciay duty to conduct an independent and objective investigation and evaluation of the each investment included in a plan.

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.4

A fiduciary’s independent investigation of the merits of a particular investment is at the heart of the prudent person standard. (citing Donovan v. Cunningham, 716 F.2d 1455, 1467 (5th Cir. 1983); Donovan v. Bierwirth, 538 F.Supp. 463, 470 (E.D.N.Y.1981). The determination of whether an investment was objectively imprudent is made on the basis of what the trustee knew or should have known; and the latter necessarily involves consideration of what facts would have come to his attention if he had fully complied with his duty to investigate and evaluate.5 (emphasis added)

Further complicating the situation is that there is ample evidence that plan sponsors often blindly rely on their plan adviser’s recommendations rather than perfrom their legally required investigations, even though the courts have consistently ruled that such blind reliance is a breach of a plan sponsor’s fiduciary duties, especially when stockbrokers and commissioned salespeople are involved. The courts have taken the position that such compensation issues create an inherent conflict of interest, and that that conflict may prevent an expert from providing the independent and impartial advice needed to ensure that the plan participants best interests are being served.

Blind reliance on a broker whole livelihood was derived from the commissions he was able to garner is the antithesis [of a fiduciary’s duty to conduct an] independent investigation”6

[A] broker [is] not an impartial analyst. [A] broker [has an incentive to close deals], not to investigate which of several policies might serve the [plan] best. A [broker]…must consider both what plan it can convince the [plan] to accept and the size of the potential commission associated with each alternative.7

In conducting their investigations and evaluations, plan sponsors considering offering annuities within their plan should especially note the “knows or should know” language. I can, and have, argued that that language, combined with the language “solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries,” and the “sufficient information to make an informed decision” requirement under ERISA 404(c), are the potential Achilles’ heel of plan sponsors in litigation involving annuities.

In conducting their investigation and evaluation and making their final decisions, plan sponsors should consider the following quote from an executive with Northwestern Mutual with regard to indexed annuities:

These products are so complicated that I think it’s a stretch to believe that the agents, much less the clients, understand what they’ve got….The commissions are extreme. The surrender periods are too long. The complexity is way too high.8

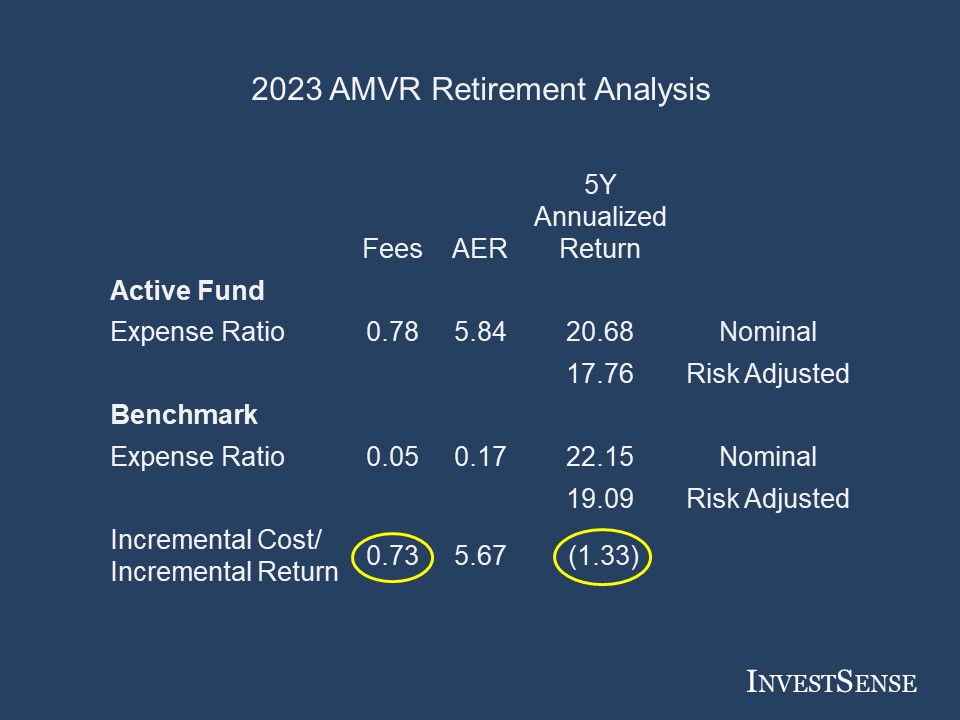

MassMutual Financial Group shared similar concerns, so much so that it sent the results of a thirty-year study to its agents comparing the performance of an annuity based on the S&P 500 Index to an actual investment in the index itself. The study factored in the dividends an investor would have received as part of an actual investment in the index. The study also factored in the fact that indexed annuities do not receive the benefit of dividends paid by the annuity’s underlying index. The study assumed that the annuity had a 9.4 percent annual cap on returns.

The study found that over the relevant thirty years:

(1) Investors in the actual S&P 500 Index, with dividends reinvested, would have received an annual return of 12.2 percent.

(2) Investors in the S&P 500 Index, without dividends, would have received an annual return of 8.5 percent.

(3) Investors in the indexed annuity would have received an annual return of 5.8 percent.9

On a side note, the study also concluded that investors investing in simple Treasury bills would have actually fared better than those investing in the annuity, earning an annual return of 6.4 over the same thrity year period.

Equity and Fiduciary Law

The cornerstone of equity law is fair dealing/fundamental fairness. A well-known tenet of equity law is that “equity abhors a windfall,” a situation where one party derives an unfair benefit at the expense of another.

I believe that the windfall issues with annuities has not received enough attention with regard to potential fiduciary liability exposure. My opinion is based on the fact that annuities are generally designed to increase the odds that annuity issuers ultimately receive a windfall in most cases, a windfall that they can use help them cover legal liabilities owed to other annuity owners via a so-called “mortality pool.”.

Courts in 401(k)/403(b) litigations often dismiss breach of loyalty claims on the grounds that the plan sponsor did not directly benefit from the investment options chosen for a plan. The annuity industry often makes similar claims. However, it can be argued that a breach of loyalty under fiduciary law also includes any situation where the plan sponsor’s decision benefits a third party at the expense of a plan participant who invests in an annuity offered within the plan.

The “Comments” section under Section 5 of the Uniform Investor Act10, “Loyalty,” states as follows:

The duty of loyalty is perhaps the most characteristic rule of trust law, requiring the trustee to act exclusively for the beneficiaries, as opposed to acting for the trustee’s own interest or that of third parties.11

A fiduciary cannot be prudent in the conduct of investment functions if the fiduciary is sacrificing the interests of the beneficiaries.12

The duty of loyalty is not limited to settings entailing self-dealing or conflict of interest in which the trustee would benefit personally from the trust.13

The trustee is under a duty to the beneficiary in administering the trust no to be guided by the interest of any third person.14

In my legal cases and in presentations to investment fiduciaries, I often use the following example:

Would you be interested in a product that can offer you guaranteed income for life? The only requirement to receive that lifetime stream of income is that you will have to surrender both control of the product and the accumulated value within the product to the company offering the product, with the issuer being allowed to unilaterally change the interest rate on the annuity at any time, with no guarantee that annuity owner will receive a commensurate return in exchange for surrendering both the value and control of the annuity, and with the understanding that the issuer, not your heirs, will receive any residual value in your account when you die.

Annuity advocates will often point out that annuities often offer so-called “riders” that do guarantee a return of the annuity owner’s principal to the annuity owner’s heirs…for an additional price. With annual fees within an annuity often running two percent or more, the additional fee for “riders” serves to further reduce an annuity owner’s payments under the annuity.

As both the Department of Labor and the federal General Accountability Office have pointed out, each additional one percent in fees and expenses reduces an investor’s end-return by approximately 17 percent over a twenty-year period.15 Riders often cost an additional one percent or more of the annuity’s accumulated value. When combined with an annuity’s other annual costs, it is easy to see how over half of an annuity owner’s end-return can be lost in an annuity’s annual fees (3 times 17).

When people ask me to define fiduciary law in 5 words or less, my answer is simple – fundamental fairness. Looking at the sample disclosure above, a prudent investment fiduciary should quickly determine that the annuity is heavily weighted in favor of the annuity issuer, not the anuity owner. That is why I argue that annuities are imprudent under applicable fiduciary principles/laws and are, ipso facto, fiduciary liability traps. (Sorry, someone dared me to use the term in exchange for a donation to St. Jude Children’s Hospital.)

In part two of this post, we will discuss ERISA section 404(c)’s “sufficient information to make an informed decision” issues relative to annuities and sufficient fiduciary disclosures, as well as a possible model that plan sponsors can use to decide whether annuities belong in their 401(k)/403(b) plan at all.

Notes

1. 29 U.S.C.A. Section 404a

2. 29 C.F.R Section 2550.404a-1(a), (b)(i) and (b)(ii)

3. 29 C.F.R Section 2550.404a-1(a), (b)(i) and (b)(ii)

4. Liss v. Smith, 991 F. Supp. 278, 291 (S.D.N.Y. 1998) (Liss)

5. Fink v. National Savs.& Trust Co., 772 F.2d 951, 957 (D.C. Cir. 1985)

6. Liss, 299

7. Gregg v. Transportation Workers of America Int’l, 343 F.3d 833, 841-42. (Gregg)

8. Jonathan Clements, “Why Big Issuers Are Staying Away From This Year’s Hottest Investment Products,” Wall Street Journal, December 14, 2005, D1 (Clements)

9. Clements

10. Uniform Prudent Investor Act, https://www.uniformlaws.org/viewdocument/final-act-108?CommunityKey=58f87d0a-3617-4635-a2af-9a4d02d119c9 (UPIA)

11. UPIA

12. UPIA

13. UPIA

14. UPIA

15. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study).

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.