Bradley Campbell of Faegre Drinker recently commented on the unusual strength of the language in the Fifth Circuit’s “Memorandum Opinion and Order” staying the DOL’s Retirement Security Rule.1 Given distristrict court Chief Judge Lynn’s earlier well-reasoned analysis and opinion in connection with the DOL’s initial Fiduciary Rule,2 as well as the fact that the Fifth Circuit’s Chief Judge cited the district court’s decision in his dissenting opinion in the 5th Circuit’s decision on the Rule,3 the Fifth’s Circuit’s statement that “[p]laintiffs are virtually certain to succeed on the merits,”4 arguably raises some legitimate questions, especially if, as expected, this case moves forward to SCOTUS..

As the court stated, in order to grant a stay or a preliminary injunction or stay, the movant must show (1) a substantial likelihood of success on the merits; (2) a substantial threat of irreparable harm; (3) that the balance of hardships weights in the movant’s favor; and (4) that issuance of a preliminary injunction will not disserve the public interest.5

As to the likelihood of success, I would point to the Judge Lynn’s well-reasoned district court decision, one which was persuasive enough to convince the Chief Judge of the Fifth Circuit’s to dissent from the majority’s decision. The Fifth Circuit stated that the DOL’s Rule was “arbitrary and capricious.”10 The Court also stated that it had weighed the equities between the parties. And yet, I would respectfully submit that common sense and “humble arithmetic” suggest otherwise.

Annuity advocates often argue that the DOL’s proposed Rule is unnecessary, that the NAIC oversees the insurance industry to ensure that the public’s “best interests” are protected, that conflicts of interest are properly addressed. However, as the Retirement Security Rule points out

[The NAIC’s] definition of ‘material conflict of interest] expressly carves out ‘cash compensation or non-cash compensation’ from treatment as sources of conflicts of interests. The NAIC model Regulation also provids that it does not apply to transactions involving contracts used to fund an employee pension or welfare plan covered by ERISA.6

The NAIC expressly disclaimed that its standard creates fiduciary obligations, and the obligations differ in significant respects from those applicable to broker-dealers in the SEC’s Regulation Best Interest..[The NAIC’s model] does not expessly incorporate the obligation not to put the producer’s or insurer’s interests before the customer’s interests, even though compliance with their terms is treated as meeting the ‘best interest’ standard.7

Additionally, the obligation to comply with the ‘best interest’ standard is limited to the indivual producer, as opposed to the insurer repsonsible for supervising the producer.8

Judge Lynn then provides support for the need for the DOL’s Retirement Security Rule by pointing out that

Further, the SEC’s Regulation Best Interest and the NAIC Model Regulations are each limited in important ways in terms of application to advice provided to ERISA plan fiduciaries although this is not the case with the Advisers Act fiducirry obligations….The NAIC Model Regulation does not apply to transactions involving conracts used to fund an employee pension or welfare plan covered by ERISA. The Department [of Labor] believes that retirement investors and the regulated community are best served by an ERIAS fiducairy standard that applies uniformly to all invstments that retirement investors may make with respect to their retirement accounts.9

And yet, the Fifth Circuit ignored the DOL’s accurate and logical arguments and analysis, choosing to protect the annuity industry over protecting plans and plan participants by issuing a stay of the DOL Rule based upon the Court’s opinion that the industry is virtually certain to succeed on the merits. It could legitimately be argued that Judge Lynn’s opinion more accurately reflects the current situations and concerns that caused the DOL to create the Retirement Security Rule in the first place..

One of the key targets of the Rule was fixed indexed annuities (FIAs). FIAs were origianlly marketed as equity indexed annuities (EIAs). I was a compliance director at the time EIAs were introduced. My immediate response when the annuity wholesaler introduced then during a weekly sales meeting was “no way,” as the product was misleading in suggesting market returns. However, the various artificial restrictions on returns made it clear that the product was structured more to ensure that the annuity issuer benefitted at the annuity owner’s expense.

My opinion on FIAs/EIAs remains the same. And apparently others in the industry agreed with my assessment, since many of the larger insurance companies avoided the product due to potential liability concerns when the EIAs were first introduced.

A vice president at Northwestenn Mutual stated that

These products are so complicated that I think it’s a stretch to believe that the agents, much less the clients, understand what they’ve got. The commissions are extreme. The surrender eriods are too long. The complexity is way too high.11

MassMutual Financial Group was so concerned that they prepared a study compaing how an FIA based on the S&P 500 would have performed over the 30-year period ending Dececmber 2003. The study concluded that the EIA would have delivered just 5.8% a year, compared to the 8.5% return on the S&P 500 (without dividends) and 12.2% return (with dividends reinvested). The study also found that investors in the EIA would have even done better invested in simple Treasury bills, which delivered 6.4% a year.12

In ” Can Annuities Offer Competitive Returns?,13“Dr. William Reichenstein, formerly a chaired professor of finance at Baylor University, came to the same conclusion about the imprudence of EIAs

By design, indexed annuities cannot add value. By design, (1) they do not attempt market timing, (2) they do not make sector/industry/style/size bets, and (3) they do not try to add value through security selection….So, I concluded that the risk-adjusted returns on indexed annities must trail the risk-adjusted returns available in marketable securities by the sum of their spread plus their transaction costs,14

Annuity issuers adamantly oppose disclosing the spreads that they assess against annuity owners. Spreads reduce the amount of interest credited to the annuity owner. Even when annuity disclose alleged spreads, they may not accurately reflect the actual impact in terms of reduced returns/loss incurred by an annuity owner. The graphic shown below shows how an alleged annual 2 percent spread (200 basis point) in connection with an FIA with a 10 percent cap effectively reduces an annuity owner’s annual return by 20 percent, not by the alleged 2 percent. And this does not even factor in the annual compounding effect of this excessive cost.

It is hard to believe that any court could/would try to ignore or justify such an inequitable practice, one which reduces an investor’s annual return by an outrageous 20 percent or more a year. Despite the Fifth Circuit’s “arbitrary and capricious “ allegation, these are facts based on ‘humble arithmetic,” not self-serving, speculative projections and “declarations”.

Yet, in staying the effectiveness of the DOL’s Rule, that is exactly what the Fifth Circuit has effectively done by virtue of issuing a stay of the Rule and allowing the annuity industry to continue to market these anti-consumer best interest products for who knows how long, with serious consequences for workers trying the prepare for “retirement readiness,” workers who may not have the time to make up for unnecessary losses resulting from the stay.

The Fifth Circuit also tried to justify the stay based on the annuity industry’s allegations of irreparable harm. The first words that came to mind when I read this was the “squandering plaintiff” ruse that the annuity industry used to try to convince the courts to require that structured settlements be required in actions involving significant damages. The annuity advocates claimed that the annuity industry had data and studies showing that 90 percent of injured plaintiffs receiving lump sum settlements instead of structured settlements and annuities dissipated such settlements within five years. And yet, when called on to produce such data studies, the annuity industry failed to do so.15

Jeremy Babener, a settlement expert, wrote several informative articles on this issue. Eventually, he cited an annuity advocate and industry in-house legal counsel who suggested that no such studies or findings ever existed, that they were simply made up/imaginary.16

So, against that backdrop of the annuity industry’s willingness and propensity to exaggerate and misrepresent the truth when it serves their purpose, I have to wonder to what extent the Fifth Circuit properly weighed the industry’s alleged irreparable claims, especially given the Court’s note that the alleged injury must also be complete, that “speculative injury is not sufficient.”17

Among the industry’s claims, based on personal self-serving “declarations”

(1) the Rule will cause more than half a billion dollars in compliance costs, and another $2.5 billion in costs over the next decade. Compliance costs are always in flux as new products are introduced. And yet, by their very nature, such forward looking projections are self-serving and speculative, and, thus, should not be a factor in any decision since they would be inadmissable under the federal rules of evidence;18

(2) 87% of independent insurance agents “estimate” that the Rule will increase their staffing and operational costs,19

(3) 93% of these independent agents anticipate rising professional liability insurance premiums,20

(4) Some agents fear they will be forced out of business, forced to restructure their business, or to retire. (speculative and hyperbole).21

Compliance costs are always a cost in both the securities and insurance industries. However, I remain sceptical of such claims given my compliance background. If one accepts these claims at face value, I would argue that it is tantamount to an admission against interest, an admission that an insurance/annuity company is selling these products without proper compliance programs and safeguards. These “woe is me” claims are reminiscent of the Aesop’s famous saying _ “A tyrant always has a pretext for his tyranny.”

These self-serving “declarations” should have absolutely no weight in whether to protect workers against imprudent investment products. Instead, the evidence suggests that once again the legal system is once again drinking the annuity industry’s self-serving misrepresentation Kool-aid without verification of same, just as with the industry’s “squandering plaintiff” ruse in connection with structured settlements and significant injuries, all to once again benefit the annuity industry at the public’s expense.

The insurance/annuity industry created and market these complex and misleading products to ensure that they profit at the public’s expense. They should now be tasked with cleaning up their own mess to ensure that their products are actually in the best interest of consumers, especially those saving for retirement.

I think that most people agree that this case will, and should, be heard by SCOTUS to ensure an equitable and consistent interpretation and enforcement of the rights and guarantees promised under ERISA. As for now, the courts need to “call” the annuity industry’s bluff in order to properly weight the equities and to preserve, protect and promote ERISA’s stated purpose and goals. The DOL should also petition for a reconsideration of the stay by the Fifth Circuit, en banc, and then petition SCOTUS, if necessary.

For more information on the inherent fiduciary liability issues with FIAs, variable annuities, and annuities in general, see my earlier post, “A Fiduciary’s Guide to Annuities: Why Go There?

Notes 1. American Council of Life Insurers v. United States Department of Labor, “Memorandum Opinion and Order,” Civil Action No. $:24-cv-00482-O 7-26-2024. (Memorandum) 2. Chamber of Commerce of the United States of America v. United States Department of Labor, 231 F. Supp.3d 152 (N.D. Tex 2017). (District Court) 3. Memorandum, 7. 4. Memorandum, 7.. 5. Memorandum, 7. 6. 29 CFR Part 2510.B.5 (Retirement Security Rule), State Legislative and Regulatory Developments 7. Retirement Security Rule, 100. 8. Retirement Security Rule, 101. 9. Retirement Security Rule, 101. 10. Memorandum, 7. 11. “Why Big Insurers Are Staying Away From This Year’s Hot Investment Product,” Wall Street Journal, D-12, December 14, 2005. (Staying Away) 12. Staying Away, D-1. 13. William Reichenstein, “Can Annuties Offer Competitive Returns?” Journal of Financial Planning, (August 2011), 36; William Reichenstein, “Financial Analysis of Equity-Indexed Annities,” Financial Services Review 18, 291-311. 14. Reichenstein, 36 15. Jeremy Babener, “Justifying the Structured Settlement Tax Subsidy: The Use of Lump Sum Settlement Monies,” NYU Journal of Law and Business Vol 6 (Fall 2009), 129. (Babener) 16. Babener. 129. 17. Memorandum, 10. 18. Memorandum, 11. 19. Memorandum, 11-12 20.. Memorandum, 11-12. 21. Memorandum, 12.

I recently posted my initial impressions on the 11th Circuit’s Decision in the Pizarro v. Home Depot 401(k) case:

It should be noted that the court granted HD summary judgment even though the court found that there were significant issues of material facts, which typically precludes summary judgment under Rule 56 of the federal rules of civil procedure. Hopefully, SCOTUS will have an opportunity to weigh in in order to resolve the split within the courts to ensure all employees’ rights guaranteed under ERISA are protected by the uniform and equitable interpretation and enforcement of ERISA in the courts, The 11th Circuit’s decision is also contra to the amicus brief filed by the Solicitor General with SCOTUS in the Brotherston case, hashtag#401k #hashtag #fiduciaryprudence

Having gone back and reviewed the district court’s original decision, the 11th Circuit’s decision and the the amicus brief that the DOL filed, I would like to share these additional observations and opinions, as this case will shape the future of both ERISA and ERISA litigation, and thus the rights and protections gauranteed to American workers.

Right now, ERISA can fairly be defined by the well-known acronym SNAFU due to the inconsistent interpretation and enforcment of ERISA within the federal courts. The courts are split on the issue as to which party has the burden of proof with regard to causation of damages in ERISA actions.

While there is currently a split within the federal courts, the majorituy of the courts adhere to the principle that plan sponsors have the burden of proof on causation, based on the basic principles set out in the common law of trusts. In Tibble v. Edison International,1 the Supreme Court (SCOTUS) endorsed the Restatement (Third) of Trusts (Restatement) as a legitimate resource in resolving trust and fiduciary disputes.

The Restatement’s position is generally that once plan participants show a fiduciary breach and resultinng loss, the burden of proof on the issue of causation shifts to the plan sponsor. This is different than the general rule in civil litigation, where the plaintiff is responsibleible for proving all aspects of his/her case. As the Solicitor General explained in an amicus brief filed with SCOTUS in the Putnam Investments, LLC v. Brotherston case, the change in ERISA litigation is due largely to the fact that plan sponsors often have access to relevant information, such as the rationale behind the internal plan decisions about why certain investment options were selected, that is known only to them.

When plan participants file an ERISA action against a plan sponsor, the plan sponsor typically responds quickly by filing a motion to dismiss and or a motion for summary judgment to quickly resolve the case and prevent discovery by the plan participants. This strategy creates a fundamental fairness/equity issue, as it may prevent the plan participants to obtain the critical information needed to prove their case, the information uniquely known only to the plan sposnsor.

The Solicitor General has addressed the current situation regarding shifting the burden of proof, stating that

In trust law, burden shifting rests on the view that ‘as between innocent beneficiaries and a defaulting fiduciary, the latter should bear the risk of uncertainty as to the consequences of its breach of duty. ERISA likewise seeks to ‘protect *** the interests of participants in employee benefit plans’ by imposing high standards of conduct on plan fiduciaries. Indeed, in some circumstances, ERISA reflects congressional intent to provide more protections than trust law. Applying trust law’s burden-shifting framework, which can serve to deter ERISA fiduciaries from engaging in wrongful conduct, thus advances ERISA’s protective purposes.3

More importantly, we have many decades of experience with the allocation of the burden of proof called for routinely by trust law, with no evidence of any particular difficulties, unfairness, or costs in applying that rule in the few cases in which it actually makes a difference.4 Solicitor General’s Brotherston amicus brief , 10 (Amicus brief) and 907 F.3d 39

The Sixth Circuit Court of Appeals recently acknowledged the equity issues in the current situation, stating

But at the pleading stage, it is too early to make these judgment calls. ‘In the absence of further development of the facts, we have no basis for crediting one set of reasonable inferences over the other. Because either assessment is plausible, the Rules of Civil Procedure entitle [the three employees] to pursue [their imprudence] claim (at least with respect to this theory) to the next stage….5

This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth ‘investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares’ because ‘the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….’ Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.6

In support of awarding Home Depot a summary judgment, both the district court and the 11th Circuit cited previous 11th Circuit decisions as controlling. However, as the DOL’s amicus brief pointed out, the cited cases do not support the argument against shifting the burden of proof on the issue of causation, but rather the decisions cited actually support the argument for shifting the burden of proof on causation.

As the DOL pointed out,

The district court’s error infected its disposition of nearly every strand of Plaintiff’s claim.7

Willett did not even consider burden shifting, let alone reject it. If anything, the Eleventh Circuit precedent – including Willett itself – supports applying trust law’s burden shifting rule to ERISA fiduciary cases.8

However, the 11th Circuit’s decision not t o shift the burden on the issue of causation is questionable for more than just its reliance on its Willett decision. The 11th Circuit rejected prior rulings citing the informational edge held by plan sponsors. As the Supreme Court ruled in the Schaffer decision

the ordinary rule does not place the burden upon a litigant of establishing facts peculiarly within the knowledge of his adversary.9

This approach is aligned with the Supreme Court’s instruction to “look to the law of trusts ” for guidance in ERISA cases.10 Tibble The 11th Circuit’s decision is contrary to ERISA’s trust law roots , the weight of circuit authorty, and the 11th Circuit’s case law. amicus

In rejecting Plaintiff’s burden shifting argument, the 11th Circuit denied the existince of an “informational advantage” in favor of plan sponsors, stating that

ERISA imposes on fiduciaries a comprehensive scheme of mandatory disclosure and reporting, both to plan particiapnts and to the public at large. The statute itself thus enforces a suite of requirements mitigating the informational advantage imputed to the trustee at common law. These disclosures, combined with the ‘proper use of discovery tools,” men that ERISA fiduciaries lack the informational advanatge that would justify shifting the burden.11

I would argue that the Court’s argument is misleading. Furthemore, the facts in this case itself, and Home Depot itself , nullify the Court’s argument.

First, the disclosures required by ERISA, are primarily quantitative in nature, e.g., returns, and do not address the qualitative/fiduciary prudence aspects of a plan’s deliberative process.

In the immediate case, the very lack of meaningful minutes of the plans deliberative meetings deny the plan participants the information needed to properly prove their case, resulting in the very “informational advantage that the plan said would be needed to justify shifting the burden of proof.

The district noted the qualitative problems with the plan’s minutes, including (1) the lack of an explanation on why the court failed to remove a fund whose trailing three-year performance had underpermed its benchmark for fourteen consecutive quarters, and its five-year performance had underperformed its benchmark for ten consecutive quarters, yet removed another fund when it lagged its benchmark for only one quarter;

(2) The fact that the investment committee did not benchmark to the benchmarks specified in the plans investment policy statement (IPS), and in some cases relied on customized benchmarks, which are always suspect due to the potenial for self-serving manipulation. Failure to follow a plan’s IPS is evidence of a fiduciary breach that a plan did not engage in a prudent monitoring process;

(3) The minutes consistently failing to disclose the amount of time spent deliberating and the content of such discussions.

(4) the evidence indcates that Home Depot “neither invetigated nor discussed whether advisory fees of certain advisors were “reasonable relative to the service they provided, even thought the evidence clearly indicated that such fees were higher than rates offered by competitors for active account management. The evidence showed that the plan’s fees were also higher than those charged by competitors to comparably-sized plans.12

(5) Home Depot measured some funds against changing benchmarks, the rationale for which was never discussed in the Investment Committee meeting minutes.13

(6) The Investment Committee did not discuss the fact that the TS&W Fund, As of March 2017, had underperformed 99% of its peers on a three-year basis and 83% of its peers on a five-year basis.14 * 27

(7) The Inveastment Committee measured the Blackrock TDFs using a BlackRock custom benchmark, in violation of the terms of the IPS. The BlackRock TDFs underperformed from 2013-2015.15

The Home Depot’s response is both evidence of the plan’s attitude toward its fiduciary responsibilities and the fallacy in the the 7th Circuit’s “no informational advantage” theory:

Minutes are not verbatim transcripts of everything discussed at IC (investment committee) meetings so this evidence does not raise a material fact question about the prudence of their monitoring process.16 District Court @218

The district court obviously disagreed, ruling that the lack of information and explanation within Home Depot’s minutes did create a material fact questions. Under Rule 56, that alone should have precluded summary judgment in favor of Home Depot. Yet, the district court did grant Home Depot’s motion for summary judgments and the 11th Circuit has now upheld such action,

Home Depot’s nondisclosure position creates the “guessing” situation that the 1st Circuit warned against in their Brotherston decision:

It makes liittle sense to have the plaintiff hazard a guess as to what the fiduciary would have done had it not breached its duty in selecting investment vehicles, only to be told “guess again.”17 Brother @ 39

Using the 11th Circuit’s own announced standard, the 11th Circuit’s failure to shift the burden of proof on causation should be reviewed by SCOTUS. The ongoing refusal of some federal courts to adopt the majority position of shifting the burden of proof on causation is unjustifiable and continues to deprive a signficant portion of workers the protections and rights guaranteed to them under ERISA, simply due to the jurisdictions they live in.

The Solicitor General of the United States has already weighed in on this issues by virtue of the amicus brief it filed in connection with the Brotherston. While the Solicitor General ultimately recommended that the Court not grant certiorari in the case, his opinion was basednot on the merits, but on the fact that it was an interlocutory appeal from an ongoing case. Based on the merits of the case, he supported the shifting the burden of proof argument based on the principles established by the Restatement of Trusts and the Supreme Court’s support of the Restatement in resolving fiduciary issues.

ERISA is a comprehensive statute designed to promote the interests of employees and their beneficiaries. The statute promotes this interest by, among other things, imposing stringent trust law-derived duties on those who manage the plan and its assets.18 DOL amicus @1,

However, the current split between the federal courts on the issue of the burden of proof on causation has resulted in inconsistent and inequitable decisions, causing investors to suffer unnecessary financial loss over the six years since the Court denied certiorari in Brotherston. Hopefully, the plaintiffs in this case will appeal for certiorari so that SCOTUS has an opportuntity to establish a uniform standard on this issue in order to resolve the inconsistent interpresentation and enforcement of ERISA.

Notes 1. Tibble v. Edison Int’l, 575 U.S. 523 (2015) 2. Amicus Brief of the Solicitor Genral of the United States, Putnam Investments, LLC v. Brotherston, at 19. (Solicitor’s Brief) 3. Solicitor’s Brief, at 17. 4. Solicitor’s Brief, at 17 and Brotherston v. Putnam Invesments, LLC., 907 F.3d 17, 39 (1st Cir. . 5. Foreman v. TriHealth, Inc, 40 F.4th 443, 450 (6th Cir. 2022) (TriHealth) 6. TriHealth, 453. 7. DOL Amicus Brief in Pizarro v. Home Depot, at 24. (DOL brief) 8, Ibid., at 19, Useden v. Acker, 947 F.2d 1563 (11th Cir. 1991), Willett v. Blue Cross and Blue Shield of Alabama, 953 F.2d 1335 (11th Cir. 1992). 9. Schaffer v. Weast, 546 U.S. 49, 60. 10. Tibble v. Edison Int’l, 575 U.S. 523, 529 (2015). 11.Pizarro v. Home Depot, Inc., Case No. 22-13643 (11th Circuit 2024) 12. DOL Brief, at 4, 5, 8 13. Pizarro v. Home Depot, Inc.,2022 WL 4687096, at *7, *8,*16 and *21-22. (N.D. Ga. 14. DOL brief, 27 15. Pizarro v. Home Depot, 2022 WL 46709687096, at *8, *21-22. 16. Pizarro v. Home Depot, 2022 WL 46709687096, at *7, *8,*16 and *21-22. 17. Brotherston, 39 18. DOL brief, 1

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

The 11th Circuit recently released its much anticipated decision in Pizarro v. Home Depot. The case is significant since it involves the question of which party has the burden of proof on the issue of causation in ERISA litigation. There is currently a split within the federal circuit courts on this issue, resulting in an inconsistent and inequitable interpretation and enforcement of ERISA, which has resulted in plan participants effectively being denied the rights and protections guaranteed to them under ERISA.

The Court’s decision presented a number of interesting and novel arguments, not the least of which was the court’s rejection of a common argument in these cases, the argument that the burden of proof on causation by necessity must belong to a plan sponsor given the fact that they alone know what policies and procedures were used in evaluating and selecting the plan’s investment options.

The 11th Circuit disputed that assumption:

ERISA imposes on fiduciaries a comprehensive scheme of mandatory disclosure and reporting, both to plan participants and to the public at large. The statute itself thus enforce a suite of requirements mitigating the informational advantage imputed to the trustee at common law. These disclosures, combined with the “proper use of discovery tools,” mean that ERISA fiduciaries lack the informational advantage that would justify shifting the burden of proof.

The 11th Circuit is surely aware that plan sponsors usually file motions to dismiss and/or Summary judgment motions quickly to prevent the type of meaningful discovery contemplated by the Court. In response to the 11th Circuit’s argument, I think the Sixth Circuit properly recognized and addressed the relevant issues in its decision in Foreman v. TriHealth, Inc. decision:

But at the pleading stage, it is too early to make these judgment calls. ‘In the absence of further development of the facts, we have no basis for crediting one set of reasonable inferences over the other. Because either assessment is plausible, the Rules of Civil Procedure entitle [the three employees] to pursue [their imprudence] claim (at least with respect to this theory) to the next stage….’2

This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth ‘investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares’ because ‘the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….’ Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.3

One could argue that the Sixth Circuit’s Chief Judge Jeffery Sutton does not agree that ERISA’s disclosure requirements provide sufficient information to overcome the inherent informational advantage that plan sponsors enjoy in carrying the burden of proof on the issue of causation. Judge Sutton also suggests that too many cases are summarily dismissed prematurely based on this issue of causation, without necessarily all the relevant and legally required facts.

Plan sponsors often seek quick dismissals of ERISA cases, allegedly to avoid the high costs of discovery. However, as Judge Sutton suggested, there are various methods of allowing discovery while controlling costs. “Controlled” discovery, limited to documents and minutes from a plan’s investment meetings, would probably suffice, assuming such documents and minutes actually exist.

The Solicitor General of the United States addressed the burden of proof on causation issue back in 2018 in connection with the Brotherston v. Putnam Investments, LLC4 case. While the Solicitor General supported shifting the burden of proof to plan sponsors, he advised SCOTUS against taking the case since it was before the Court as an interlocutory appeal. The Court followed the Solicitor General’s advice.

This case needs to be heard and the issues involved resolved once and for all without letting another 6 years pass and more plan participants suffer needless financial losses.

Given the significance of this decision and the impact of the burden of proof re causation in ensuring that 0lan participants are being treated equitably and that ERISA remains meaningful, hopefully the plan participants will seek certiorari from SCOTUS, who would presumably hear the case given the divide between the courts and the importance of ERISA and plan participants.

Stay tuned!

Notes 1. Pizarro v. Home Depot, Case No. 22-13643 (11th Cir. 2024) decided 8/2/2024 2. Forman v. TriHealth, Inc., 40 F.4th 443, 450 (6th Cir. 2022). (TriHealth) 3. TriHealth, 453. 4. Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (1st Cir. 2018).

Testimony of James W. Watkins, III, J.D., CFP Board Emeritus™, AWMA® re QDIAs and Annuities as QDIAs

In my practice, I often refer to as the “fiduciary responsibility trinity” (Trinity). The Trinity consists of the Tibble v. Edison International1 (Tibble I), Brotherston v. Putnam Investments, 2 (Brotherston), and Hughes/Northwestern3 decisions.

Tibble recognized the Restatement of Trusts (Restatement) as a legitimate resource in resolving fiduciary issues and ruled that a plan sponsor has an ongoing fiduciary duty to monitor plan investment options for prudence.

Brotherston ruled that comparable index funds can be used for benchmarking purposes, citing Section 100 b(1) of the Restatement.

Hughes/Northwestern ruled that a plan sponsor has a fiduciary duty to ensure that each investment option within a plan is prudent and to remove any that are not.

The question that I am constantly asked by plan sponsors and other investment fiduciaries, as well as attorneys, is “so how do I use all this to evaluate the fiduciary prudence of an investment option?” Since SCOTUS recognized the legitimacy of the common law of trusts in resolving fiduciary questions in its Tibble decision4, and since the Restatement of Trusts (Restatement) is essentially the codification of the common law of trust, I always suggest consulting the Restatement for guidance.

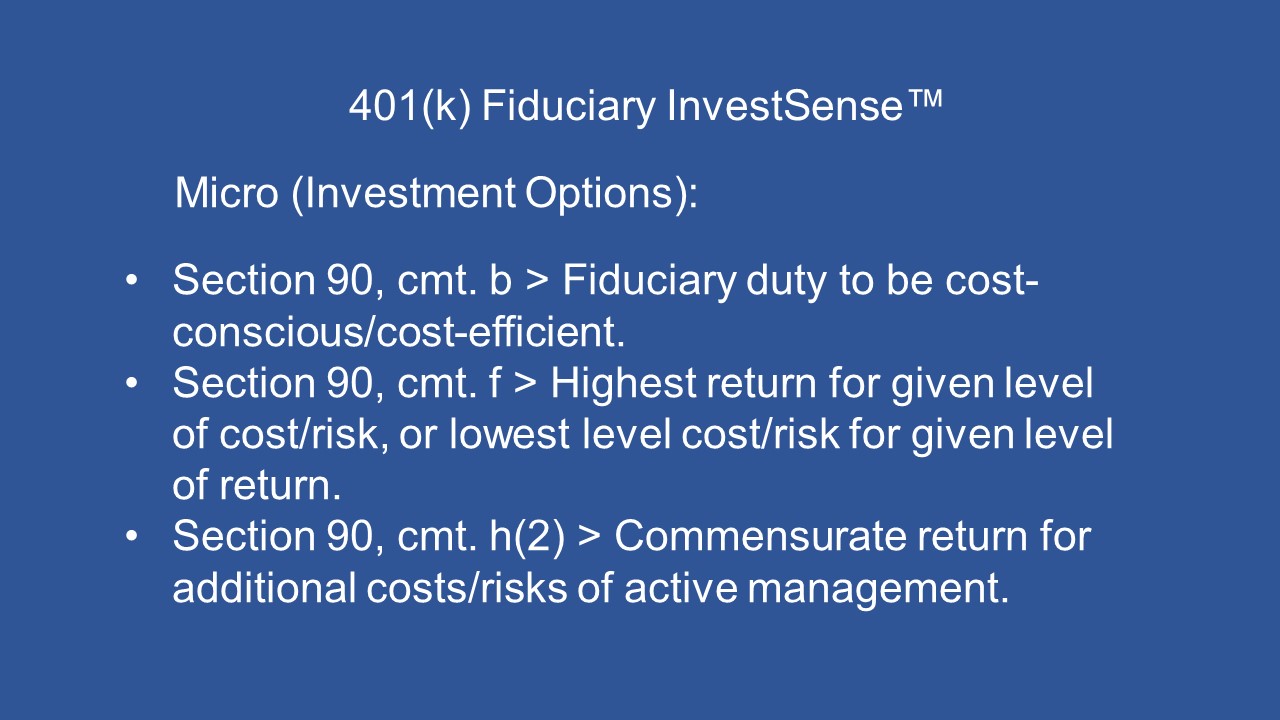

Three comments within Section 90 of the Restatement, commonly known as the “Prudent Investor Rule,” provide a simple blueprint for selecting prudent investment options for ERISA plans.

Comment b states that “cost-conscious management is fundamental to prudence in the investment function.”5

Comment f states that ”A fiduciary has a duty to select mutual funds that offer the highest return for a given level of cost and risk; or, conversely, funds that offer the lowest level of costs and risk for a given level of return.”6

Comment h(2) essentially says that actively managed mutual funds that are not cost-efficient, that cannot objectively be projected to provide a commensurate return for the additional costs and risks associated with active management, are imprudent.7

Taken together, these three comments stress the importance of a properly conducted cost-benefit analysis in selecting prudent investment options. Cost-benefit analysis is routinely used in business to evaluate the viability of projects. Yet, the investment industry typically avoids a cost-benefit analysis, as it knows what the results would show. Academic studies have consistently concluded that actively managed funds are typically cost-inefficient, most even failing to cover their costs:

99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.8

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.9

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.10

It should be noted that when the SEC announced Regulation Best Interest, Chairman Jay Clayton also stressed the importance of cost-efficiency relative to acting in the best interest of customers:

rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.11

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.12

In 2015, the DOL issued Interpretive Bulletin 15-01 (IB 15-01).13 IB 15-01 reinstated earlier language from Interpretative Bulletin 94-114, language that supports the previously mentioned Restatement comments and the potential importance of cost-benefit analysis in evaluating the fiduciary prudence of plan investments:

Consistent with fiduciaries’ obligations to choose economically superior investments….[Plan fiduciaries should consider factors that potentially influence risk and return. 15

[B]ecause every investment necessarily causes a plan to forgo other investment opportunities, an investment will not be prudent if it would provide a plan with a lower expected rate of return than available alternative investments with commensurable degrees of risk or is riskier that alternative available investments with commensurate rates of return.16

The Active Management Value Ratio As a fiduciary risk management consultant, I created a simple metric, the “Active Management Value Ratio,” (AMVR) that allows investors, investment fiduciaries, and attorneys to quickly perform cost-benefit analyses of actively managed investments. My favorite comment about the AMVR has been “it’s simply third grade math…but very persuasive third grade math.” The attached sample AMVR slide shows how easy the AMVR calculations are using “Humble Arithmetic” – subtraction and division. The actual AMVR formula is the actively managed fund’s incremental correlation-adjusted costs divided by the actively managed fund’s incremental risk-adjusted returns.

Interpreting the AMVR is equally easy, consisting of answering two questions:

Did the actively managed fund provide a positive incremental return?

If so, did the actively managed fund’s positive incremental return exceed the fund’s incremental costs?

If the answer to either question is “no,” then the actively managed fund is neither cost-efficient nor prudent under the Restatement’s guidelines.

The AMVR is based on the research findings and concepts of investment icons Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel:

The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.17– Dr. William F. Sharpe

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that the incremental fees for active management are really, really high – on average, over 100% of incremental returns.18– Charles D. Ellis

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover. 19– Burton G. Malkiel

Selecting prudent investments is just that simple. Cost-benefit analysis is consistent with applicable legal standards. Using an objective analysis metric, can an investment be projected to provide a commensurate return to an investor for the additional costs and risks associated with the investment in question?

“Black Box” Target Date Funds and Qualified Designated Investment Alternatives (QDIAs) Studies have consistently suggested that the majority of the public is financially illiterate when it comes to personal finances and investing. Target Date Funds (TDFs) were designed to simplify the investment process for investors, including plan participants, by creating professionally designed asset allocation plans designed to prudently reduce investment risk as an investor got older, while still providing a prudent return in anticipation of retirement.

Nice in theory, but actual results are still questionable given the disparity in risk among TDFs once the TDF owner reaches their “target” retirement date. In many cases, the asset allocation errors have been attributed the use of “black box” portfolio optimizers/asset allocation computer applications, many of which utilize Markowitz’s “Mean Variance Optimization” (MVO) theory. The issues involved with the use of MVO by such “black box” computer applications are well-known and were summed up perfectly by Michaud:

Although Markowitz efficiency is a convenient and useful theoretical framework for defining portfolio optimality, in practice it is an error-prone procedure that often results in “error-maximized” and “investment irrelevant” portfolios.20

In practice, the most important limitations of MV optimization are instability and ambiguity. Small changes in input assumptions often imply large changes in the optimized portfolio….21

In other words, molehills of erroneous assumptions result in mountains of erroneous projections out. Plan participants deserve better and ERISA demands better.

Notes 1.Tibble v. Edison International, Inc., 135 S. Ct. 1823, 1828 (2015) (Tibble). 2. Brotherston v. Putnam Investments, 907 F.3d 17 (1st Cir. 2018). 3. Hughes v. Northwestern University, 595 U.S. ___ (2022). 4. Tibble 5. Restatement (Third) of Trusts, Section 90, cmt. b. American Law Institute, All rights reserved. 6. Restatement (Third) of Trusts, Section 90, cmt. f. American Law Institute, All rights reserved. 7. Restatement (Third) of Trusts, Section 90, cmt. h(2). American Law Institute, All rights reserved. 8. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 9. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 10. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 11. SEC Release 34-86031, “Regulation Best Interest: The Broker-Dealer Standard of Conduct (Reg BI), 279. 12. Reg BI, 279. 13. DOL Interpretative Bulletin 15-01, 29 CFR.2015-01. 14. DOL Interpretative Bulletin 94-01, 29 CFR.1994-015. 15. DOL Interpretative Bulletin 15-01, 29 CFR.2015-01. 16. DOL Interpretative Bulletin 15-01, 29 CFR.2015-01. 17. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm. 16. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 17. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 18. Michaud at XIV 19. Michaud, 2.

“Don’t make the process harder than it is.” – Jack Welch, former GE CEO

When I meet with a prospective client, this is what I always tell them. Then I show them how their current plan is exposing them to unnecessary fiduciary liability exposure.

I continue to see posts and comments about how plan participants want annuities and guaranteed income products. When a plan member brings that issue up, my response is “who cares what plan participants want. You shouldn’t.” A plan sponsor’s fiduciary reality is defined by ERISA and the Restatement of Trusts, not by what plan participants allegedly want or what plan advisers and/or consultants may recommend. nor by the transitory and possibly uneducated wishes of plan participants.

Nowhere in ERISA does it mention any duty to provide investment alternatives that plan participants want. Annuity advocates respond with “that’s horrible” and make unfounded claims about moral and ethical duties to offer their imprudent investment products. Note, this is the same industry that deliberately mislead courts for years with claims that they had reports indicating that 95 percent of injured plaintiffs dissipated their injury awards within five years, also known as the annuity industry’s “squandering plaintiff” ruse. All this was done to try to get courts to require that injured victims accept structured settlements involving annuities, even as the annuity industry was misrepresenting the actual value of such settlements.1

The goal of the annuity industry’s fraud was to convince courts to require that any monetary award given to an injured victim be in the form of a structured settlement involving an annuity. Fortunately, most courts saw through this ruse, especially when the annuity industry was unable to produce the alleged studies supporting their “squandering plaintiff” claims.2

My fear is that we are seeing a repeat performance of these misrepresentations with relation to the annuity industry’s push for inclusion of annuities and “guaranteed income” products in 401(k) and other ERISA pension plans. One of the services that I provide as part of my fiduciary risk management consultant practice is fiduciary oversight services. Whenever income annuities are involved, I prepare a breakeven analysis like I did during my days as a plaintiff’s personal injury attorney facing the defense’s “squandering plaintiff” argument.

Shown below is a breakeven analysis based on a 65 year-old male purchasing an income annuity. A proper annuity breakeven analysis should factor in both present value, to account for the time value of money, and mortality risk, to factor in the odds that the annuity annuity may not survive long enough to recover the principal originally paid to purchase the annuity. My experience has been that most investors agree with Mark Twain’s famous quote – “I am more concerned with the return OF my money than I am the return ON my money.

As the analysis below shows, even if the 65 year-old purchaser in this example beat the odds and lived to be 100, the owner still would not break even. If mortality risk is factored in, the annuity owner would fall woefully short of breaking even, over $30,000 short!

Fortunately, the reports are that most plan sponsors are not falling for the annuity industry’s annuity and “guaranteed income” marketing push. I am always reminded of what the late Peter Katt, a fee-only insurance adviser, used to say about evaluating insurance products – “At what cost?” For additional information about the inherent fiduciary liability issues with annuities and “guaranteed income” products, read my recent post.

Cost-Benefit Analysis Cost-benefit analysis is commonly used in the business world to assess the viability of a project. Despite the simplicity of cost-benefit analysis, far too many investment fiduciaries, including plan sponsors, do not employ the strategy, especially given the consistent finding of studies finding that the overwhelming majority of actively managed mutual funds are cost-inefficient, with many not even able to cover their costs2

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.3

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.4

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.5

Do costs exceed benefits? How much simpler could fiduciary prudence be for investment fiduciaries. Since studies show that humans are visually oriented, I created a visual metric, the Active Management Value Ratio (AMVR). I teach my clients, as well as investment fiduciaries, attorneys, and investors, how to use the AMVR to quickly calculate the cost-efficiency and fiducairy prudence of an actively managed mutual fund relative to a comparable index fund. The AMVR is based on the research of investment icons, including Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel.

The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.6

So, the incremental fees for an actively managed mutual fund realtive to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that the incremental fees for active management are really, really high – on average, over 100% of incremental returns.7

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.8

There are actually two forms of the AMVR, one that uses just a fund’s nominal, or publicly reported performance data, and a second version, which incorporates Miller’s Active Expense Ratio, which allows an attorney or investment fiduciary to detect both a fiduciary breach and the projected resulting monetary damages, using Miller’s Active Expense Ratio. Miller explained the importance of the AER as follows:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark indexs.9

The two-column version is based on the funds’ nominal performance data. In this example, a plan sponsor can easily see that the actively managed fund is cost-inefficient, thus imprudent relative to the comparable index fund, since the active fund provides no benefit for the additional/incremental costs. Since studies have shown that most actively managed funds are cost-inefficient relative to comparable index funds, the two-column AMVR is a quick way to evaluate actively managed funds with minimal data requirements.

When questions of potential legal liability are involved, the three-column AMVR is the preferred option since it allows a fiduciary to determine both potential liability exposure and the projected cost of damages from such breach of fiduciary dutiesby incorporating Miller’s AER. In this example, treating the underperformance of the actively managed fund as an opportunity cost, the projected cost would be 4.83 per share (1.95 + 2.88).

Based on the research of both the GAO and the DOL, showing that each additional one percent of costs/fees reduces an investor’s return by approximately 17 percent over 20 year period, the investor would suffer a projected loss of 82 percent of their end-return from the cost-inefficient actively managed fund.10

Fortunately, the AMVR provides a quick and easy way for a plan sponsor to proactively detect such potential fiduciary breaches using “humble arithmetic,” and to protect their plan participants by ensuring that the investment options offered within the plan are cost-efficient, thus prudent. Fiduciary risk management literally can, and should be that simple.

Going Foward While there are some other proprietary techniques and strategies that we use to reduce potential fiduciary liability exposure, the strategies discussed here are key parts in our process simplification model which we refer to as our KISS model – Keep It Simple and Smart!

Smart people do not assume unnecessary risk. Going back to the issue of annuities within plans, plan participants desiring annuities or “guaranteed income” products still have the opportunity to purchase those products outside of the plan, allowing the plan sponsor to avoid any liability issues.

Fiduciary liability is all about employing prudent processes in managing ERISA plans. So don’t make the fiduciary process harder than it is.

That said, we always suggest to our clients to insist that their plan adviser provide then with written AMVR analyses on funds and breakeven analyses on annuities using the exact methods shown here. It will make a plan sponsor’s life easier and, if an adviser refuses (and most do), this will let a plan sponsor know to keep looking for a better adviser candidate.

Notes 1. Jeremy Babener, “Justifying the Structured Settlement Tax Subsidy: The Use of Lump Sum Settlement Monies,” NYU Journal of Law & Business (Fall 2009), 36 (Babener); Laura Koenig, “Lies, Damned Lies, and Statistics: Structured Settlements, Factoring, and the Federal Government,” Indiana Law Journal, Vol. 82, Issue 3, Article 6, available at https:www.repository.law.indiana.edu/ilj/vol82/iss3/ 6. (Koenig). 2. Babener, Koenig. 3. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 4. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 5. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 6. William F. Sharpe, “The Arithmetic of Active Investing,” available online t https://web.stanford.edu/~wfsharpe/art/active/active.htm. 7. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 8. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 9. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926. 10. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study).

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

A [fiduciary] is held to something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most sensitive, is the standard of behavior….1

Consistent with fiduciaries’ obligations to choose economically superior investments,.. [P]lan fiduciaries should consider factors that potentially influence risk and return.2

Fiduciary law is a combination of three types of law–trust, agency and equity. The basic concept of fiduciary law is fundamental fairness.

SCOTUS has consistently recognized the fiduciary principles set out in the Restatement (Third) of Trusts (Restatement) as guidelines for fiduciary responsibility, especially for plan sponsors.

ERISA is essentially a codification of the Restatement (Third) of Trusts (Restatement). SCOTUS has recognized that the Restatement is a legitimate resource for the courts in resolving fiduciary questions, especially those involving ERISA.2

Under the Restatement, loyalty and prudence are two of the primary duties of a fiduciary. A fiduciary’s duty of loyalty requires that a plan sponsor act solely in the best interests of the plan participants and their beneficiaries. A fiduciary’s duty of prudence requires that a plan sponsor exercise reasonable care, skill, and caution in managing a plan, specifically with regard to controlling unnecessary costs and risks.

The key question in evaluating annuities, or any other investment, should always be “at what cost?” With annuities, you generally have annual costs as well as additional optional costs for various “bells and whistles.” While costs vary, a basic average annual cost for immediate annuities seems to be 0.7 percent. The average costs for various additional options with all annuities seems to be an additional 1.0 percent. However, it is a plan sponsor’s duty to always ascertain the exact costs.

Plan sponsors need to always remember this mantra – “Costs matter.” Costs do matter, a lot. The General Accounting Office has stated that each additional 1 percent in costs/fees reduces an investor’s end-return by approximately 17 percent over a twenty year period. 3

Against that backdrop, plan sponsors are now confronted with the potential issues of including annuities and within a 401(k) plan, even thought these is no legal, moral, or other type of requirement to do so. I believe that annuities are inappropriate for 401(k) and 403(b) plan sponsors, as well as other investment fiduciaries such as registered investment advisers and trustees and are potential fiduciary liability traps, as they are structured to best serve the annuity issuer’s “best interests,” not those of an annuity owner. The following example of a typical income annuity shows a breakeven analysis for a 65-year old purchasing a garden-variety income annuity

Annuities An exhaustive analysis of annuities is beyond the scope of this post. I simply want to address three of the most common types of annuities and some of the fiduciary issues associated with each. One of the fiduciary issues involved with annuities is their complexity. The analyses herein will be based on the simple, garden variety of each of the three annuities.

1. Immediate Annuities (aka Income Annuities} These annuities are often recommended to provide supplemental income in retirement. In most cases, immediate annuities can be used to provide income for life or for a certain period of time, e.g., 5, 10, 15 or 20 years.

Peter Katt was an honest and objective insurance adviser. During my compliance career, he was my trusted go-to resource. While he passed away in 2015, the lessons I learned from him will always be invaluable. I strongly recommend to investors and investment fiduciaries that they Google his name and read his articles, especially those he wrote for the AAII Journal.

Katt’s thought on immediate annuities include:

The immediate annuity is for people who want the absolute security that they can’t outlive their nest egg. The problem is that there is nothing left over for your heirs.4

While annuities often offer options to address this issue, such options often result in reduced monthly payments and/or additional costs.

Katt always said to get the annuity salesmen to provide a written analysis providing the breakeven analysis for an annuity, the estimated time that would be required for an annuity owner to recover their original investment in the annuity. He told me that breakeven periods of twenty years or more are common, making it unlikely that the annuity owner will ever recover their original investment. And remember, with a life-only immediate annuity, once the annuity owner dies, the balance in the annuity goes to the annuity issuer, not the annuity owner’s heirs.

The sample breakeven analysis shown below shows the odds a 65 year old purchasing a simple income annuity paying 5 percent annually would face of not even breaking even, even if they lived to be 100. The example shows why it is importance to factor in both present value and mortality risk in evaluating the prudence of a garden-variety annuity.

If at some point, the annuity owner realizes that they made a mistake and wants to get out of the annuity by selling it, the purchaser, at best, is going to base the offering price on the annuity’s present value, not the original face value. In some cases, the purchaser will discount the offering price even further, using the mortality risk-based value.

This is why I often refer to the annuity industry’s attempt to make courts order that cases involving significant amounts of money include “structured settlements” that include annuities, what I refer to as “victimizing the victim.” For years, the annuity industry mislead the courts in an effort to persuade courts to require settlements to include annuities by claiming to have research showing that over 90 percent of plaintiffs receiving large sums outright squandered the money within 5 years. When finally pressed to produce such research, the annuity industry admitted that there was no such research.5

Katt also said to always ask the annuity salesman for the APR that was used in calculating the breakeven point. The APR is the interest rate that annuity issuers typically use in determining an annuity’s payments. In the example above, the applicable APR is 5 percent.

One of the drawbacks with immediate annuities is that once an interest rate is set, that will be the applicable interest rate for the period of the annuity. Again, some annuities may offer options to avoid this inflexibility…at an additional cost.

The inflexibility of an annuity’s interest rate results in purchasing power risk for an annuity owner. This risk increases as the period of the annuity increases. Purchasing power risk refers to the risk that the annuity’s payments will lose their buying power over the years due to inflation. Some annuities provide for “step-ups” in rates…at an additional cost.

Katt’s advice-anyone considering an immediate annuity should first build a balanced portfolio consisting of stocks and bonds to ensure flexibility, and then invest augment that portfolio with a reasonable am0unt in the immediate annuity. While some annuity salesmen will argue for an “all or nothing” approach in order to maximize their commission. Prudent investors will follow Katt’s advice.

Perhaps the strongest argument against including immediate annuities in 401(k) and other pension plans comes from a study by three well-respected experts on the subject. In analyzing when a Single Premium Immediate Annuity (SPIA), probably the most popular type of immediate annuity, would make sense, the three experts stated that

Results suggest that only when the possibility of outliving 70 percent or more of a cohort exists, and then only at elderly ages. For ages younger than 80, assets are best kept within the family, because both inflation and possible future market returns have time to do better than SPIA lifetime sums.6

Based upon my experience, very few 401(k) plans have plan participants aged 80 or older. I predict that plan sponsors who decide to offer immediate annuities, in any form, in their plans can expect to see that quote again, especially cases involving litigation.

2. Fixed Indexed Annuities (aka Equity Indexed Annuities) Target date funds (TDFs) are controversial investments that attempt to create investment portfolios that are appropriate based on the investor’s estimated retirement, or target, date. Target date funds have typically designed portfolios consisting of equity and fixed income investments.

There have been reports suggesting that the annuity industry may be trying to include some form of equity indexed annuities (EIAs) as an element in TDFs in 401(k) and 403(b) plans. So, what would be wrong with that? Dr. William Reichenstein, finance professor emeritus at Baylor University sums up the primary issue perfectly.

The designs of equity index annuities (EIAs) and bond indexed annuities ensure that they must offer below-market risk-adjusted returns compared with those available on portfolios of Treasurys and index funds. Therefore, this research implies that indexed annuity salesmen have not satisfied and cannot satisfy SEC requirements that they perform due diligence to ensure that the indexed annuity provides competitive returns before selling them to any client.6

While EIAs/FIAs are technically insurance products, not securities, Dr. Reichenstein’s analysis is still applicable with regard to a fiduciary’s duties of loyalty and prudence. If the design of these products ensures that they cannot offer competitive returns to those of alternative investments, then how does a plan sponsor, or any fiduciary for that matter, plan to meet their fiduciary duty of loyalty and prudence? Would the inclusion of EIAs in either TDFs, or in 401(k) plans in general. potentially create unnecessary fiduciary liability exposure for plan sponsors or other investment fiduciaries,

As regulators emphasize, before an insurance agent can sell an annuity, he or she must perform due diligence to ensure that the investment offered ex ante competitive returns. Therefore, it is appropriate to compare the net returns available in an equity-indexed annuity to those available on similar-risk investments held outside an annuity.7

[By] design, [equity]indexed annuities cannot add value through security selection ….[T]he hedging strategies [used by equity-indexed annuities] ensure that the individuals buying equity-indexed annuities will bear essentially all the risks. Consequently, all indexed annuities must (ital) produce risk-adjusted returns that trail those offered by readily available marketable securities by their spread, that is, by their expenses including transaction costs.8

Furthermore, by design, indexed annuities typically impose restrictions on the amount of return that an investor can actually receive. Therefore, the combination of the design of these products and the restrictions on returns typically imposed by EIAs/FIAs ensure a fiduciary breach.

So, even though the annuity industry markets these equity indexed annuities by emphasizing stock market returns, the majority of fixed indexed annuity owners are guaranteed to never receive the actual returns of the stock market. While some annuity firms are marketing so-called “uncapped” equity indexed annuities, they may still impose restrictions, and such “uncapped” returns…come with additional costs.

The restrictions and conditions that equity indexed annuities naturally vary. For example, during my time as a compliance director, the equity indexed annuities I saw typically imposed a 8-10 percent cap and a participation rate of 80 percent. What that meant was that regardless of the returns of the applicable market index, with a cap of 10 percent, the most the annuity owner could receive was 10 percent of the index’s return.

As if that was not unfair enough, that 10 percent return was then further reduced by the annuity’s participation rate. So, with a participation rate of 80 percent, the maximum return an investor could receive in our example was 8 percent.

More recently, the point has been made that while a fixed indexed annuity may claim to only impose a certain amount of spread, for instance a 2 percent “spread” that would only reduce the annuity owner’s realized return by 2 percent on a capped return of 10 percent, “humble arithmetic” indicates that the impact of the 2 percent “spread” a capped 10 percent return would be a 20 percent reduction in return (A basis point equals 1/100th of 1 percent, so 100 basis points equals 1 percent. 200 basis points divided by 1000 basis points equals 20 percent).

Reichenstein points out even more inequities, noting that

Because interest rates and options’ implied volatilities change, the insurance firm almost always retains the right to set at its discretion at least one of the following: participation rate, spread, and cap rate.9

And finally, a simple explanation of how equity indexed annuity companies aka indexed fixed annuities further manipulate returns to ensure that they protect their interests first.

From AmerUS Group financial statements, ‘Product spread is a key driver of our business as it measures the difference between the income earned on our invested assets and the rate which we credit to policy owners, with the difference reflected as segment operating income. We actively manage product spreads in response to changes in our investment portfolio yields by adjusting liability crediting rates while considering our competitive strategies….’ This spread ensures that the annuity will offers noncompetitive risk-adjusted returns.10

I could go on to discuss additional issues such as single entity credit risk and illiquidity risk, but I think investment fiduciaries get the picture. The evidence against equity index annuities establishes that they are a fiduciary breach simply waiting to happen. I strongly recommend that plan sponsors and other investment fiduciaries read Reichenstein’s analysis before deciding to offer fixed indexed annuities, in any shape or form, in their plans or to clients. With no legal obligation to offer annuities of any type, the obvious risk management question is – “why go there?”

3. Variable Annuities Any fiduciary that sells, uses, or recommends a variable annuity (VA) has probably breached their fiduciary duty…period. Annuity expert Moshe Milevsky summed it up perfectly with the following observations and opinions in his classic article, :The Titanic Option”:

Exhibit A Benefit – VAs provide a death benefit to limit a VA owner’s downside risk.

[T]he fee [for the death benefit] is included in the so-called Mortality and Expense (M&E) risk charge. The M&E risk charge is a perpetual fee that is deducted from the underlying assets in the VA, above and beyond any fund expenses that would normally be paid for the services of managed money.11

[T]he authors conclude that a simple return of premium death benefit is worth between one to ten basis points, depending on purchase age. In contrast to this number, the insurance industry is charging a median Mortality and Expense risk charge of 115 basis points, although the numbers do vary widely for different companies and policies.12

The authors conclude that a typical 50-year-old male (female) who purchases a variable annuity—with a simple return of premium guaranty—should be charged no more than 3.5 (2.0) basis points per year in exchange for this stochastic-maturity put option. In the event of a 5 percent rising-floor guaranty, the fair premium rises to 20 (11) basis points. However, Morningstar indicates that the insurance industry is charging a median M&E risk fee of 115 basis points per year, which is approximately five to ten times the most optimistic estimate of the economic value of the guaranty.13 (emphasis added)

Excessive and unnecessary costs violate the fiduciary duty of prudence, especially when they produce a windfall for an annuity issuer at the expense of the annuity owner. The value of a VA’s death benefit is even more questionable given the historic performance of the stock market. As a result, it is unlikely that a VA owner would ever need the death benefit. These two points have resulted in some critics of VAs to claim that a “VA owner needs the death benefit like a duck needs a paddle.”

Exhibit B Benefit – VAs provide a death benefit to limit a VA owner’s downside risk.

At what cost? VAs often calculate a VAs annual M&E charge/death benefit based on the accumulated value within the VA, even though contractually most VAs limit their legal liability under the death benefit to the VA owner’s actual investment in the VA.

This method of calculating the annual M&E, known as inverse pricing, results in a VA issuer receiving a windfall equal to the difference in the fee collected and the VA issuer’s actual costs of covering their legal liability under the death benefit guarantee.

As mentioned earlier, fiduciary law is a combination of trust, agency and equity law. A basic principle of fiduciary law is that “equity abhors a windfall.” The fact that VA issuers knowingly use the inequitable inverse pricing method to benefit themselves at the VA owner’s expense would presumably result in a fiduciary breach for fiduciaries who recommend, sell or use VAs in their practices or in their pension plans.

The industry is well aware of this inequitable situation. John D. Johns, a CEO of an insurance company, addressed these issues in an article entitled “The Case for Change.”

Another issue is that the cost of these protection features is generally not based on the protection provided by the feature at any given time, but rather linked to the VA’s account value. This means the cost of the feature will increase along with the account value. So over time, as equities appreciate, these asset-based benefit charges may offer declining protection at an increasing cost. This inverse pricing phenomenon seems illogical, and arguably, benefit features structured in this fashion aren’t the most efficient way to provide desired protection to long-term VA holders. When measured in basis points, such fees may not seem to matter much. But over the long term, these charges may have a meaningful impact on an annuity’s performance.14

In other words, inverse pricing is always a breach of a fiduciary’s duties of both loyalty and prudence, as it results in a windfall for the annuity issuer at the annuity owner’s expense, a cost without any commensurate return, which would presumably violate Section 205 of the Restatement of Contracts.

Exhibit C Benefit – VAs allow their owners the opportunity to invest in the stock market and increase their returns.

VAs offer their owners an opportunity to invest in equity-based subaccounts. Subaccounts are essentially mutual funds, usually similar to the same mutual funds that investors can purchase from mutual fund companies in the retail market.

While there has been a trend for VAs to offer cost-efficient index funds as investment options, many VA subaccounts are essentially same overpriced, consistently underperforming, i.e., cost-inefficient, actively managed mutual funds offered in the retail market. As a result, VA owners’ investment returns are typically significantly lower than they would have been when compared to returns of comparable index funds.

Exhibit D Benefit – VAs provide tax-deferral for owners.

So do IRAs. So do any brokerage account as long as the account is not actively traded. However, dividends and/or capital gain distributions are taxed when they occur.

The key point here is that IRAs and brokerage accounts usually do not impose the high costs and fees associated with annuities. This is especially true of VAs, where annual fees of 3 percent or more are common, even higher when riders and/or other options are added.

Remember the earlier 1/17 note? Multiply 3 by 17 to see the obvious fiduciary issues regarding the fiduciary duties of loyalty and prudence.

Although not an issue for plan sponsors, another “at what cost” fiduciary issue for other investment fiduciaries has to do with the adverse tax implications of investing in non-qualified variable annuities (NQVA). Non-qualified variable annuities are essentially those that are not purchased within a tax-deferred account, e.g., a 401(k)/403(b) account, an IRA account.

When investors invest in equity investments, they typically are not taxed on the capital appreciation until such gains are actually realized, such as when they sell the investment or, in the case of mutual funds, when the fund makes a capital gains distribution.

In many cases, investors can reduce any tax liability by taking advantage of the special reduced tax rate for capital gains. However, withdrawals from a NQVA do not qualify for the lower capital gains tax. All withdrawals from a NQVA are considered ordinary income, and thus taxed at a higher rate than capital gains. An investment that increases its owner’s tax liability by converting capital gains into ordinary income is hardly prudent or in an investor’s “best interest.”

Bottom line – there are other less costly investment alternatives available that provide the benefit of tax deferral. While they may not offer the same guaranteed income, they provide other significant benefits, while avoiding some of the fiduciary liability risks associated with VAs, e.g., reduced flexibility, purchasing power risk, higher taxes.

Exhibit E Benefit: Annuity owners do not pay a sales charge, so more of their money goes to work for them.

The statement that variable annuity owners pay no sales charges, while technically correct, is misleading. Variable annuity salesmen do receive a commission for each variable annuity they sell. Commissions paid on VA sales are typically among the highest paid in the financial services industry.

While a purchaser of a variable annuity is not directly assessed a front-end sales charge or a brokerage commission, the variable annuity owner does reimburse the insurance company for the commission that was paid. The primary source of such reimbursement is through a variable annuity’s various fees and charges.

To ensure that the cost of commissions paid is recovered, the annuity issuer typically imposes surrender charges on a variable annuity owner who tries to cash out of the variable annuity before the expiration of a certain period of time. The terms of these surrender charges vary, but a typical surrender charge schedule might provide for a specific initial surrender charge during the first year, then decreasing 1 percent each year thereafter until the eighth year, when the surrender charges would end. There are some surrender charge schedules that charge a flat rate over the entire surrender charge period.

Going Forward I have been asked by clients and the media for my opinion on what I see for fiduciary law and 401(k) litigation going forward. My answer-a significant increase in litigation.

What too many plan sponsors fail to recognize and appreciate is the fact that those recommending the inclusion of annuities in plans generally are not doing so in a fiduciary capacity and therefore arguably have no potential fiduciary liability. Plan sponsors, trustees and other investment fiduciaries that follow such advice will typically have unlimited personal liability exposure based on the issues discussed herein.

Plan sponsors and other investment fiduciaries have a duty to independently investigate, evaluate, select and monitor the investment options they select or recommend.