By James W. Watkins, III, J.D., CFP Board Emeritus™, AWMA®

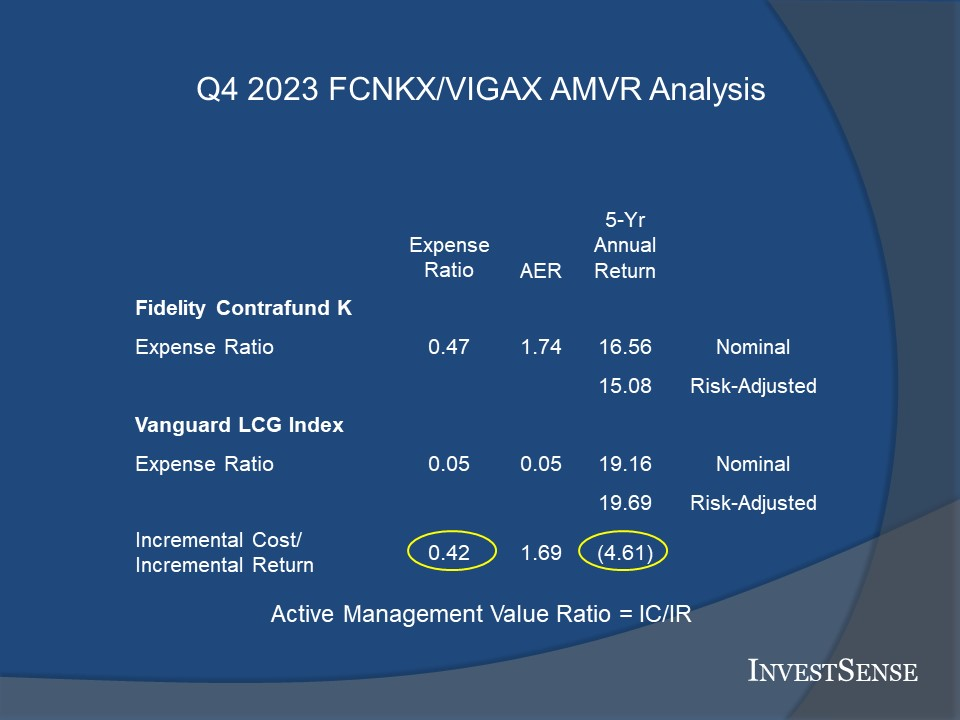

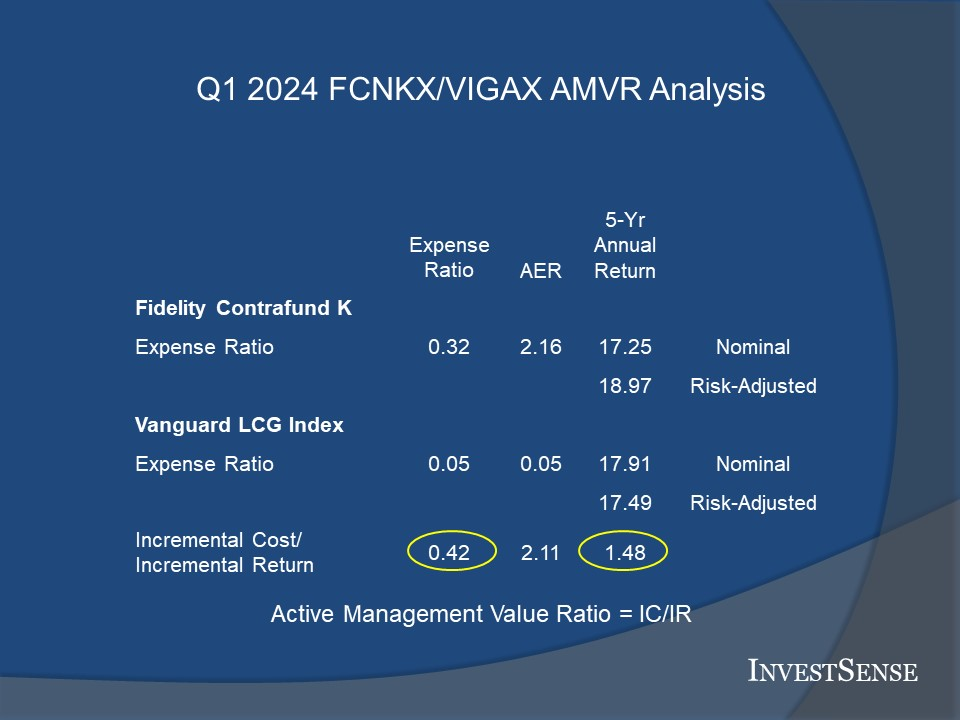

The first quarter of 2024 produced an interesting situation, resulting in an opportunity to demonstrate both the value of the Active Management Value Ratio (AMVR) and its nuances. The Fidelity Contrafund Fund K shares (FCNKX) reduced the fund’s expense ratio, from 47 basis points (0.47) to 32 basis points (0.32). A basis point equals 1/100th of one percent.

The AMVR slide below shows the results of an AMVR analysis between FCNKX and a comparable index fund, the Vanguard Large Cap Growth Index Fund Admiral shares (VIGAX), for the 5-year period ending on December 31, 2023. Shown below the Q4 2023 analysis is a 5-year AMVR analysis of the same funds, for the same five-year period ending on March 31, 2024.

My fiduciary clients immediately called and emailed me asking how to evaluate the AMVR results resulting from FCNKX’s significant reduction in its expense ratio. While such a significant reduction in a fund’s expense ratio is uncommon, the AMVR makes a new cost-efficiency analysis relatively simple.

The 2023 AMVR analysis resulted in FCNKX failing to provide a positive incremental risk-adjusted return, resulting in FCNKX failing to qualify for an AMVR score. Using Contrafund’s risk-adjusted 1Q 2024 returns resulted in FCNKX providing a positive incremental risk-adjusted return (1.48) relative to the benchmark Vanguard fund, resulting in an AMVR score of 0.18. Under the AMVR metric, a low AMVR score indicates a higher cost-efficiency rating.

However, if we recalculate those AMVR scores using Miller’s Active Expense Ratio1 (AER) and factoring in the correlation of returns between the two funds in each scenario, FCNKX would be considered cost-inefficient/imprudent relative to the benchmark Vanguard fund in both analyses.

While some investment professionals ignore the correlation, or r-squared, factor, fiduciaries who do so risk being deemed to have breached their fiduciary duties for not properly carrying out their required independent, thorough, and objective investigation and evaluation. When the returns of funds are highly correlated, an argument can be made that the actively managed fund is a “closet index” or “mirror” fund, charging higher fees based on the claim of providing active management. The higher an actively managed fund’s r-squared number, the higher the implicit expense ratio of such fund, making it less likely that the fund will pass the AMVR’s cost-efficiency standards.

In both of the scenarios provided, the correlation of returns was at or above 90 percent. As a result, the AER estimated that the actively managed fund only provided approximately 25.00 percent of active management. A strong argument can be made that a fund providing only 25.00 percent of active management hardly qualifies as an actively managed fund.

The Case for Risk-Adjusted Returns

I am often asked why the AMVR uses a fund’s risk-adjusted returns. The investment industry often objects to risk-adjusted returns, parroting the industry line of “you can’t eat risk-adjusted returns.” My response is that the investment industry has no qualms about using Morningastar’s star system in advertising its products, even though Morningstar clearly states that they use risk-adjusted returns in determining their star system scores.

The Q1 2024 AMVR slide provides a perfect example of why the AMVR uses risk-adjusted returns. Risk and return are inextricably woven together. A key component in the prudence of any investment is whether the investment provides a commensurate return for the level of risk and cost assumed by an investor. In this case, using Contrafund’s risk-adjusted returns resulted in higher returns and a very favorable AMVR rating based on Contrafund’s nominal cost numbers. However, as mentioned earlier, the fund’s AMVR rating became cost-inefficient/imprudent when the fund’s correlation-adjusted costs were used in the calcuations.

Remember, when using the AMVR, the goal is a score between zero and 100. The lower the AMVR score, the higher the cost-efficiency. We also recommend that the user always prepare both a five and ten-year AMVR analysis, if possible, to evaluate possible prudence trends and/or inconsistencies.

Going Forward

The two AMVR slides demonstrate the need to properly re-examine each investment in a plan on a regular basis. While the reduction in FCNKX’s expense ratio may increase the likelihood of additional positive AMVR evaluations, one period is not a sufficient period to deem a previously consistently cost-inefficient/imprudent fund under the AMVR metric suddenly a cost-efficient/prudent. The fund should be monitored interms of future performance.

While arguments can be made about the validity of the AER being factored in as part of the AMVR analysis, the key fact is that it creates a legitimate question of fact in terms of prudence and the question of “closet indexing.” As a result, it should prevent a court from dismissing the case and allow the plan participants the opportunity to have discovery to determine what process, if any, the plan sponsor used in conducting their investigation and evaluation. While the issue of “closet indexing” has not received as much attention in the U.S. as it has in other countries, the issue and the potential harm is real, as evidenced by studies such as those conducted in Canada and Australia.

Others have argued that high correlations of return, often referred to as a fund’s r-squared number, could be considered as fraud since the amount of active management an investor receives is significantly less than an investor has a right to expect from a fund holding itself as being actively managed and charging higher fees accordingly. Again, this creates a question of fact that is not proper for adjudication at the motion to dismiss stage.

These questions become even more important given the likelihood that SCOTUS may soon have the opportunity to decide which party has the burden of proof in 401(k) and 403(b) litigation. If SCOTUS decides that plan sponsors have the burden of proving that their actions did not cause the plan participants to suffer financial losses, the issues of cost-inefficiency and closet indexing could make the plan sponsor’s burden that much harder.

Notes

1. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

You must be logged in to post a comment.