James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

With all the recent SCOTUS decision in Cunningham v. Cornell University1, there has been a lot of discussion about Prohibited Transactions and Prohibited Transaction Exemptions (PTEs). That is understandable; however, it is important for plan sponsors not to overlook the traditional fiduciary duties of fiduciary prudence and loyalty.

As a fiduciary risk management counsel, I offer fiduciary audits and plan reviews. Unfortunately, I often find that plans are unknowingly exposed to unnecessary fiduciary liability due to legally insufficient fiduciary processes. The problems are typically due to a lack of understanding as to what fiduciary status requires and/or a lack of experience and/or knowledge about certain investments.

With our clients, we stress the importance of selecting cost-efficient investment options. To help them accomplish this goal, we teach them about the simplicity and benefits of cost-benefit analysis.

Companies around the world routinely use cost-benefit to evaluate proposed projects. However, my experience has been that the financial services industry and its agents typically do not use cost-benefit analysis in evaluating investment options. Why? Because, more often than not, cost-benefit analysis will reveal that actively managed mutual fund investments are not cost-efficient when compared to comparable passivley managed index funds.

For over twenty years, I served as a compliance professional for broker-dealers and insurance companies. As I got a better understanding of those businesses, I gained a greater understanding of their “tricks of the trade,” ” and how to properly deal with them.

Several years ago, I created a simple metric, the Active Management Value Ratio™ (AMVR). The AMVR is based on the research and concepts of investment icons such as Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton G. Malkiel. /quote

The best way to measure a manager’s performanceis to compare his or her return with that of a comparable passive investment.2

So, the incremental fees for an actively managed fund relative to its incremental returns shoud always be compared to the fees for a comaprable index fund relative to its returns. When you do this, you’ll quickly see that the incremental fees for active management are really, really high – on average, over 100 of incremental returns.3

Past performance is not helpful in predicting future returns. The two variables that do the best job in pedicting future performance [of mutual funds] are expense ratios and turnover.4

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that the incremental fees for active management are really, really high – on average, over 100% of incremental returns.

The AMVR is essentially a cost-benefit analysis using incremental cost and incremental returns, or versions thereof, in performing the analysis. Shown below are sample slides showing the basic AMVR analysis process.

Using purely nominal numbers, FCNKX’s incremental benefit does exceed its incremental costs. But a good ERISA plaintiff’s attorney will argue that a more accurate analysis of fiduciary prudence is provided by using the incremental return numbers obtained by applying Ross Miller’s Active Expense Ratio (AER), which factors in the correlation of returns between two mutual funds. Miller explains the value of his AER metric as follows:

Mutual funds appear to provide investment servicws for relatively low fees because they bundle passive and active funds together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active maangement while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have 90% of the variance in its returns explained by its benchmark index.5

So, essentially, the higher the correlation between an actively managed fund and a comparable index fund, the less likely the value of active management, if any, being provided by the actively managed fund.

Using the AER, an argument can be made that FSPGX is the much better choice in terms of fulfilling a plan sponsor’s fiduciary duties. The fact that FSPGX and FCNKX are offered by the same mutual fund company, Fidelity, and belong to the fund category, large cap growth, makes that analysis even more compelling. At the very least, an argument should be made that a plan sponsor should inquire into the availability of FSPGX for the plan rather than Fidelity Contrafund fund, which ironically is one of the most common mutual funds found in 401(k) plans. When I review plans, one of the first things I look for is whether Fidelity Contrafund is offered within the plan. Humble Arithmetic, as John Bogle was fond of saying.

So, if Fidelity refuses to offer FSPGX to a plan, what should the plan sponsor’s response be? A simple fiduciary risk management principle we teach our clients is that a fiduciary can never “settle.” “Settling” is the antithesis of a fiduciary’s “best interest” duty under the fiduciary duty of loyalty.

A prudent plan sponsor looking for cost-efficient options for a plan should always do an AMVR analysis using a comparable Vanguard index fund. I know various courts and judges dismiss Vanguard funds, some claiming you cannot compare “apples and oranges.”

That is absurd, simply a ruse to protect the cost-inefficient actively managed mutual fund industry. In fact, one of the primary benefits of using cost-benefit analysis in fiduciary prudence analysis is that it allows fiduciaries to compare investments based purely on an objective basis, cost-efficiency. Furthermore, Section 100 of the Restatement (Third) of Trusts recognizess the validity of comparing actively managed funds with comparable index funds.6 Judge Kayatta cited Section 100 of the Restatement in his opinion in Brotherton v. Putnam Investments LLC.7 As for Vanguard index funds specifically, Judge Sidney Stein, the well-respected district court judge for the Southern District of New Yor,k aka the Wall Street federal Court, has recognized the validity of using Vanguard index funds as comparators in forensic analysis.8

In the AMVR analysis shown for FCNKX and VIGAX (Vanguard Large Cap Growth Index Fund), based purely on the nominal, or publicly reported, numbers, VIGAX, is the more prudent option due to anpositive incremental risk-adjusted return (0.07) that is also less than the incremental cost between the two funds (0.51). If we base the comparison on the AER correlation-adjusted costs, the prudence of the VIGAX is even clearer (3.26 v 0.07).

In both of the comparisons shown, the correlation of returns between the two funds was 97. Surprisingly, such a high correlation of returns is not unusual today, as claims of “closet index” funds is a much-debated issue, not only in the U.S., but internationally as well. Canada and Australia have been the leaders in studying the existence and impact of closet index funds.

The AMVR itself, both the calculation and interpretation process, are very simple. Just divide the incremental cost between the funds by the incremental return between the funds. Since cost-efficiency is the goal, an AMVR score greater than 1.00 indicates that the actively managed fund is cost-inefficient relative to the comparator index fund. Actively managed funds that do not provide a positive incremental return should be automatically disqualified from consideration, since they will automatically be cost-inefficient and imprudent.

One of the “secret” benefits of using the AMVR metric is that it automatically reveals the unrewarded premium that a plan participant would be paying. That premium is common used by plaintiff’s attorneys in ERISA actions in calculating damages in a trial. An AMVR score of 1.25 would indicate a premium of 25% per share. Multiply the shares in the plan by the premium to determine the damages due to the inclusion of a particular fund within a plan.

The good news is that a plan sponsor can limit any potential fiduciary liability in connection with mutual funds and similar investment, e.g., TDFs, by using the AMVR to evaluate competing investment options for a pension plan. I used the AMVR in a case to compare the index-based version of Fidelity’s TDFs with the actively managed versions of the same TDFs.

ERISA plaintiff’s attorneys are well aware of the AMVR. Hopefully, your plan will never be involved in fiduciary litigation. However, if so, do not be surprised to see the familiar AMVR slide format at trial.

A prudent plan sponsor looking for cost-efficient options for a plan should always do an AMVR analysis using a comparable Vanguard index fund. I know various courts and judges dismiss Vanguard funds, some claiming you cannot compare “apples and oranges.”

That is an absurd assertion and a ruse to protect the cost-efficient actively managed mutual fund industry. In fact, one of the primary benefits of using cost-benefit analysis in fiduciary prudence analysis is that it allows fiduciaries to compare different kinds of investments with each other based purely on cost-efficiency. Furthermore, Section 100 of the Restatement (Third) of Trusts authorizes the validity of comparing actively managed funds with comparable index funds.9 Judge Kayatta cited Section 100 of the Restatement in his opinion in Brotherton v. Putnam Investments LLC.

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes).10

As for Vanguard index funds specifically, Judge Sidney Stein, the well-respected district court judge for the Southern District of New York aka the Wall Street Court, has supported the use of Vanguard index funds.11

In the AMVR analysis shown for FCNKX and VIGAX (Vanguard Large Cap Growth Index Fund), based purely on the nominal, or publicly reported numbers, VIGAX, is the more prudent option due to an incremental risk-adjusted return (0.07) that is less than the incremental cost between the two funds (0.51). If we base the comparison on the AER correlation adjusted costs, the prudency of the VIGAX is even clearer (3.26 v 0.07).

In both of the comparisons shown, the correlation of returns between the two funds was 97. Surprisingly, such a high correlation of returns is not unusual today, as claims of “closet index funds” is a much-debated issue, not only in the U.S., but internationally as well. Canada and Australia have been the leaders in studying the existence and impact of closet index funds.

The AMVR itself, both the calculation and interpretation are very simple. Just divide the incremental cost between the funds by the incremental return between the funds. Since cost-efficiency is the goal, an AMVR score greater than 1.00 indicates that the actively managed fund is cost-inefficient relative to the comparator index fund. Actively managed funds that do not provide a positive incremental return should be automatically disqualified from consideration, since they will automatically be cost-inefficient.

One of the “secret” benefits of using the AMVR metric is that it automatically indicates the unrewarded premium that a plan participant would be paying. That premium is a plaintiff’s attorney would use in calculating damages in a trial. An AMVR score of 1.25 would indicate a premium of 25%, or 25 basis points on each share. Multiply the shares in the plan by the premium to determine the damage due to a particular fund.

The good news is that a plan sponsor can limit any potential fiduciary liability in connection with mutual funds and similar investments by using the AMVR to evaluate competing investment options for a pension plan. The AMVR can even be used to evaluate the prudence of individual elements of TDF funds.

ERISA plaintiff’s attorneys are well aware of the AMVR. Hopefully, your plan will never be involved in fiduciary litigation. However, if so,, do not be surprised to see the familiar AMVR slide format at trial.

Going Forward A basic understanding of the core principles set out in the Restatement (Third) of Trusts is an absolute necessity for prudent plan sponsors and other investment fiduciaries. In my opinion, three key comments in Section 90 of the Restatement, aka The Prudent Investor Rule, are shown in the box below.

We tell our clients that if they simply remember and apply these three concepts in their practices, they will greatly reduce the risk of unwanted fiduciary liability exposure. Time has proven that advice to be true.

When I think of fiduciary risk management, I think of a quote by the late General Norman Schwarzkopf. I always used this quote in my closing argument to the jury.

The truth of the matter is that you always know the right thing to do. The hard part is doing it.

Notes 1. Cunnigham v. Cornell University, Supreme Court Case No. 23-1007 (2024). 2. William F. Sharpe, “The Arithmetic of Active Investing,” available online t https://web.stanford.edu/~wfsharpe/art/active/active.htm. 3. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 4. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 5. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926. 6. Restatement (Third) of Trusts, Section 100, American Law Institute. All rights reserved. 7. Brotherston v. Putnam Investments, LLC, 907 F.3d 17, 31, 39 (2018). (Brotherston) 8. Leber v. Citigroup 401k Plan Investment Committee, 2014 WL 4851816. 9. Restatement (Third) of Trusts, Section 100, American Law Institute. All rights reserved. 10. Brotherston, 31, 39 11. Leber v. Citigroup 401k Plan Investment Committee, 2014 WL 4851816.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other qulified professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

During a recent deposition I asked the plan sponsor if he understood the requirement under the fiduciary duties of prudence and loyalty. His answers were your basic ERISA 404(a) language. When he finished describing the duty of loyalty, I clearly surprised him when I asked, “Anything else?”

I have recently posted a number of posts about my expectation of the coming increase in fiduciary litigation involving RIAs and annuities based on their breach of their fiduciary duty of loyalty. When I inform plan sponsors, RIAs, and other investment fiduciaries that the duty of loyalty includes a duty to disclose all material facts that they knew or should have known.1 The same “should have known” language shown in ERISA 404(a).

“Of course, the thoroughness of a fiduciary’s investigation is measured not only by the actions it took in performing it, but by the facts that an adequate evaluation would have uncovered.2 (Scalia, J., concurring in part and dissenting in part)

[T]he determination of whether an investment was objectively prudent is made on the basis of what the trustee knew or should have known; and the latter necessarily involves consideration of what facts would have come to his attention if he had fully complied with his duty to investigate and evaluate.” (emphasis in original)).3

blind reliance on a broker whose livelihood was derived from the commissions he was able to garner — is the antithesis of such independent investigation. 4

If a plan sponsor RIA, or other investment fiduciary is not even aware of the duty of disclosure required under ERISA the duty of loyalty, as set out in section 78(3), it is reasonable to assume that the required investigation and evaluation, as well as the required disclosure of material facts, was not performed as well. Given the annuity industry’s known opposition to transparency and disclosure, that assumption is more reasonable since it was unlikely that the annuity issuer did or would provide material information such as applicable spreads and other costs. or the risks involved with a particaular type of annuity.

So, what constitutes “material information” that must be disclosed under the fiduciary duty of loyalty, as set out in Section 78(3)?

Information is ‘material’ if there is a substantial likelihood that, the disclosue of the omitted fact would have been viewed by the reasoanble investor as having significantly altered the ‘total mix’ of information made available.5

I am a big fan of Stanford University’s new AI platform, STORM (storm.genie,stanford.edu. I especially like the fact that STORM includes extensive footnotes, which helps in further researching, as well as a BrainSTORMing section, which provides focused answers from various experts on issues relevant to the original topic

I submitted a “material information” query to STORM. I cannot improve on the answer it provided: /quote

“Under ERISA, the term “material” refers to any information that could affect a participant’s decision-making regarding their investments. This inlcudes details about the investment options available , the associated risks an returns, and any fees that might be incurred. The requirement emphasizes that participants mu be able to understand the risk and benefits of each option, allowing them to make choicds that align with their financial goals and risk tolerance.6

The Department of Labor (DOL) has issued guidelines specifying the type of information that must be disclosed, which encompasses investment performance data, fee structures, and the nature of the risks associated with each investment option. Effective communication of the information is crucial for ensuring that participants can exercise informed control over their accounts and make prudent investment choices. 7

Fiduciaries must carefully navigate the complexities of compliance with the sufficient information requirement. Failure to adequately disclose material information can expose them to legal challenges from participants, as it undermines the intended protective mechanisms of ERISA.8

[Restatement Section 78(3) and ERISA Section (404(a) emphasize] the fiduciary duty of plan administrators to provide necessary disclosures oin a manner that allows participants to make informed investment decisions.“9

The annuity indusry has been engaged in a campaign to convince RIAs and plan sponsors to increase their use of annuities. My concern is that in the annuity industry’s marketing materials on so-called “advisory annuities,” they have tended to focus on the compensation issue, suggesting that fiduciaries can use “advisory annuities” to increase income while avoiding legal hassles, since advisory annuities do not pay a commission. Fiduciaries cannot receive commissions or other financial compensation from third parties, as it would create conflict of interest issues. However, the compensation is far from being the only liability issues investment fiduciaries have to consider in connection with annuities.

For example, most of the annuity industry annuity marketing material to RIAs that I have seen seems to suggest that RIAs can recommend annuities to their clients, even if the client does not understand annuities, and then turn around and offer to manage the annuity for them, using management fees to make up for the loss of commissions. In the retail securities industry, this is known as “double dipping” and is prohibited. While I understand the managing variable annuities concept, no annuity advocate has explained the concept of managing FIAs, given the structure of the product and the fact that the FIA issuer typically reserves the right to unilaterally change key terms within the FIA annually to protect the issuer’s best interests

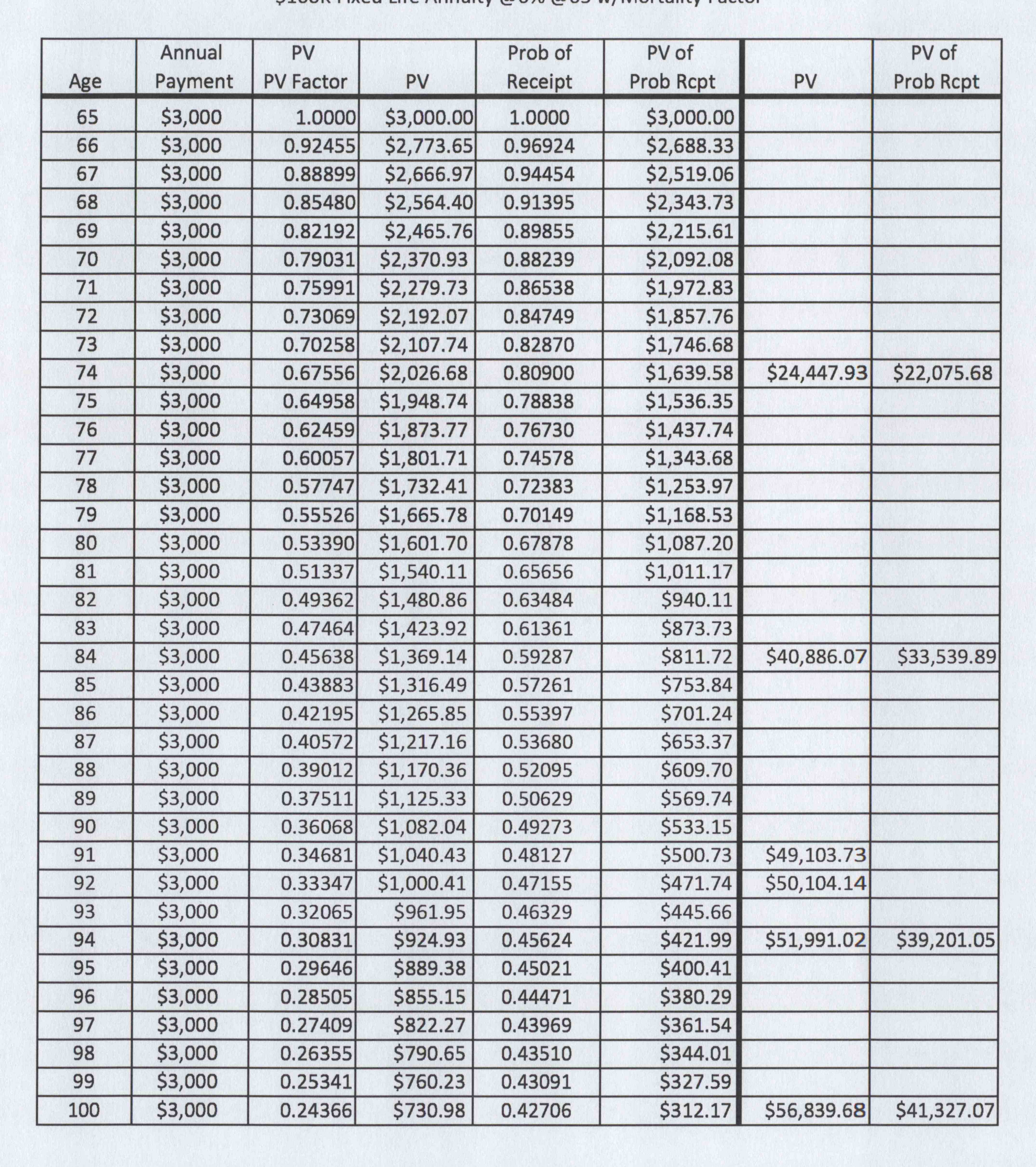

In a famous study by annuity expert, Moshe Milevsky, Milevsky determined that variable annuities were charging five to ten times the industry’s median M&E risk fee of 115 basis points (1.15%) a year, a fee five to ten the most optimistic estimate of the economic benefit of the death benefit guarantee.This raises obvious fiduciary breach issues.10 In my opinion, inverse pricing is a blatant breach of an investment fiduciary’s fiduciary duties.

Insurance/annuity executive John D. Johns wrote an article in which he suggested it was time for change, as inverse pricing was counterintuitive.

Another issue is that the cost of these protection features is generally not based on the protection provided by the feature at any given time, but rather linked to the VA’s account value. This means the cost of the feature will increase along with the account value. So over time, as equities appreciate, these asset-based benefit charges may offer declining protection at an increasing cost. This inverse pricing phenomenon seems illogical, and arguably, benefit features structured in this fashion aren’t the most efficient way to provide desired protection to long-term VA holders. When measured in basis points, such fees may not seem to matter much. But over the long term, these charges may have a meaningful impact on an annuity’s performance.11

As mentioned earlier, my concern is that the annuity industry’s marketing materials to RIAs on advisory annuities that I have seen could be deemed misleading and could expose RIAs to fiduciary liability unless they consider the other potential fiduciary liability issues, e.g., cost of death benefit, inverse pricing, and cost inefficiency of the subaccount offered by a variable annuity. Trying to discuss these issues with annuity advocates has proven to be extremely difficult in most cases, with such irresponsible statements such as “you cannot be a fiduciary unless you offer annuities.” Tell me you know nothing about fiduciary law without telling me that you know nothing about fiduciary law.

An example of inverse pricing would be where the annuity contract limits the death benefit to the annuity owner’s actual capital contribution. So, if the variable annuity (VA) owner’s actual contribution was only $100,000, his death benefit would be limited to $100,000. With inverse pricing, the annuity issuer typically uses the accumulated value of the VA instead of the contract’s terms. As a result, if the VA has grown to $200,000, under inverse pricing, the annuity issuer charges an annual fee based on the $200.000 accumulated value instread of the actual amount under the terms of the annuity contract. Counterintuitive indeed. Pay more to get less.

My experience has been that annuity brokers do not disclose if inverse pricing will be used in connection with the VA or explain the risdks and equitable issues involved with inverse pricing. This would appear to be a clear fiduciary breach under Restatement Section 78(3).

As for cost-efficiency of a VA’s subaccounts, I have never seen a case where the plan sponsor, RIA, or other investment fiduciary says that each subaccount was compared to a comparable index fund to determine the cost-efficiency of the VA subaccounts. I believe a case can be made that such information would consitute “material information” under 78(3) and the fiduciary duty to perform an independent investigation and evaluation of each investment option, as well as offering cost-inefficient subaccounts is clearly not in the best interests of a plan participant or RIA client.

During my time as a compliance director, first as an RIA compliance director, then as a general securities compliance director, the brokers all wanted to be approved to exercise discretion so they could offer to manage annuities for a fee, providing for a steady sourve of annual income rather than look for new customer s each year.

FIAs Why Go There At All In a recent opinion involving the Retirement Security Rule , Chief Judge Barbara M.G. Lynn summed up the fiduciary issues with FIAs, stating that /quote

The DOL described the complexity of FIAs (fixed indexed annuities) in its Regulatory Impact Analysis (“RIA”). The RIA explained that FIAs generally provide “crediting for interest based on changes in a market index,” but noted there are hundreds of indexed annuity products, thousands of index annuity strategies, and that “the selection of the crediting index or indices is an important and often complex decision.” Further, there are several methods for determining changes in the index, with different methods resulting in varying rates of return. Rates of return are also affected by “participation rates, cap rates, and the rules regarding interest compounding.” Because “insurers generally reserve rights to change participation rates, interest caps, and fees,” FIAs can “effectively transfer investment risks from insurers to investors.” The DOL found that FIAs may offer guaranteed living benefits, but such benefits “may come at an extra cost and, because of their variability and complexity, may not be fully understood by the consumer.” The DOL also cited the SEC, which recently stated, “[y]ou can lose money buying an indexed annuity … even with a specified minimum value from the insurance company, it can take several years for an investment in an indexed annuity to break even.1 (emphasis added)12

Purchasing an annuity, or any investment for that matter, that allows the issuer to annually change the interest rate to be credited and/or other key terms of the investment unilaterally, to effectively shift all investment risk to an investor, makes absolutely no sense. Talk about being counterintuitive.

As Judge Lynn pointed out, FIAs allow the FIA issuer to shift the total risk of loss to the annuity owner.This, on top of the fact that it is unlikely that the annuity issuer has disclosed the spreads that will be used to further reduce the annuity owner’s realized return, is a fiduciary breach action waiting to happen. Any argument suggesting that FIAs are in the best interest of the FIA owner is simply disingenuous and an attempt to justify a fiduciary breach. This is clearly information that would qualify as “material information, as it would definitely impact an investor’s decision in deciding on whether to invest in an FIA.

When it comes to FIAs, the question is why go there at all. Neither ERISA nor any other law requires plans to offer annuities of any type. Academic studies claim plan participants want the income that annuities provide. From a fiduciary risk managment perspective, the plan sponsor’s response should be “so what. ” An investment fiduciary in under no obligation to expose themselves to unnecessary fiduciary risk. Furthermore, plan participants interested in annuities can always purchase annuities outside of the plan, without exposing the plan sponsor to fiduciary risk.

The most obvious and effective risk management strategy is to totally avoid risk whenever possible. Toward that goal, I teach my fiduciary risk management clients a simple two-question process.

(1) Does ERISA or any other law explicitly require you to offer the investment option? ERISA does not explicitly reuuie a plan to offer specific type of investment. Therfore, under current law, the answer to question will always be “no.”

(2) If the answer to question number (1) is “no,” could offering the investment in question possibly expose the plan to unnecessary fiduciary liability?

Since we already know that the answer to the first question is “no,” we can focus purely on the fiduciary risk management issues presented by the second question, what I refer to a the “why go there” issues. Academic studies often argue the interest in annuities from plan participants and the alleged benefits of increased retirement income. From a fiduciary risk mangement perspective, since there is no legal requirement that fiduciaries expose themselves to unnecessary fiduciary risk, a decison to do so would clearly be imprudent. What the academics conveniently refuse to to addess is that a plan participant can easily purchase an annuity outside of the plan, without exposing the plan to unnecessary risk exposure. Why do academics and annuity advocates fail to address the annuity options out of the plan? My theory is that they do not discuss the availability of annuities outside of a plan for the same reason that the annuity industry has targeteted in-plan annuties.

The annuity industry desperately wants greater access to the significant sums in 401(k) plans and other retirement accounts. However, the fact is that annuities, especially guaranteed lifetime income annuities, in their presenrt form, are the antithesis of both fiduciary prudence and fiduciary loyalty. Unless and until the annuity industry acknowledges and properly addesses the legitimate fiduciary liability issues with annuities, in their current form, investment fiduciaries should ignore annuities altogether, especially guaranteed lifetime income annuities.

As for FIAs, simple common sense indicates that FIAs are not a prudent fidiciary investment choice for a number of reasons. First, explain the prudence of investing in a product where the issuer reserves the right to unilaterally change the annuity interest rate and other key terms annually, to effectively shift the entire burden of risk from the insurer to the investor. This simply ensures that the annuity issuer can protect their best interest instead of the annuity owners, a clear breach of fiduciary duties. Secondly, as Judge Lynn pointed out, it allows the annuity issuer to shift all of the risk from the insurer to to the FIA owner. But I’m sure the annuity issuer disclosed all of those risk consideration when they made the required disclosures pursuant to their fiduciary duty of loyalty under 78(3).

An even more basic question is whether FIAs are an inherent breach of a plan’s fiduciary duty of prudence. There is ample evidence that suggests that the structure of FIAs prevents FIAs from being a prudent investment choice. William Reichenstein, a chaired finance professor at Baylor University, has done extensive research on the fiduciary issues associated with FIAs..His conclusion

Because of their design, managers of indexed annuities cannot add value through security selection, they buy Treasury securities and index options, but do not engage in in indovidual security selection….By design, the IA wil produce returns that trail benchmark portfolio by the average spread. 13

For the indexed annuities, the question is whether they offer competitive risk-adjusted returns. On average, their returns must trail those of the risk-appropriate benchmark portfolio of Treasurys and index funds[s} by their annual expense. Since by design, indexed annuities cannot add value through security selection, all indexed annuities must produce risk-adjusted returns that trail those avaialble on the risk-appropriate portfolio. Their structure ensures this outcome.14

Further support for this conclusion is provided by a Mass Mutual study when EIAs, nka FIAs, were first introduced. Mass Mutual’s findings –

“over a 30 year period ending December 2003. the equity-indexed annuity would have delivered just 5.8 percent a year, far below the 8.5 perent for the S&P 500 without dividends and 12.2 percent for the S&P 500 with dividends, reinvested. Indeed, annuity investors would have been better of in super-safe Treasury bills,which delivered 6.4 percent a year.15

When one considers the various costs and return restrictions imposed by FIAs, a common sentiment among objective observers seems to be expressed by an article entitled “Equity Indexed Annuities: Downside Protection, But at What Cost?”

Each EIA (equity-indexed annuity) has so many moving parts that are under the discretion of the issuing insurer that it is difficult to determine whether company A’s EIA strucure is better or worse than company B’s.16

As a plaintiff’s attorney, my concern is that such issues and risks will not be disclosed to plan participants, as required by the fiduciary duty of disclosure and loyalty. Disclosure and transparency are the annuity industry’s kryptonite, as it would expose the serious fiduciary issues such as arbitrary and excessive costs and the true impact of caps and other articial and self-serving restrictions on an investor’s end returns. Collectively, these issues are why I constantly remind my fiduciary clients to pause and ask themselves – “Why go there?”, which, in the case of annuities, especially guaranteed life income annuities, ultimately leads to a decision of “Don’t go there!”_

My advice on navigating the 78(3) disclosure requirements and the inherent breach of fiduciary duty of loyalty traps – Don’t even try. Without the spread information for an annuity, plan sponsors and other investment fiduciaries set themselves up for a per se fiduciary breach since they cannot properly perform the required independent investigation and evaluation or the disclosure of material information required by ERISA and 78(3). Better to just avoid annuities and FIAs altogether, since not legally required. To quote Jack Welch, “Don’t make the process harder than it is.” If something is neither required by ERISA or some other law or regulation – “Don’t go there!” As I tell my clients, Keep it simple and smart”

Update: After I published this post, I had numerous responses asking me where to find the Restatement, Third, Trusts and/or to publish the exact languauge from Section 78(3). The American Law Institute (ALI) is the publisher of the Restatement, which is protected by copyright law. I had submitted a request to publish the exact language and the ALI has graciously granted permission for me to do so. Section78 (3) states as follows: /quote

(3) Whether acting in a fiduciary or personal capacity, a trustee has a duty in dealing with a beneficiary to deal fairly and to communiacte to the beneficiary all material facts the trustee knows or should know in connection with the matter. (emphasis added)

Pretty powerful little provision in terms of fiduciary risk management. And yet, based on my experience, very few investment fiduciaries have ever read Sections 77, 78, 90 (aka The Prudent Investor Rule), or 100 of the Restatement. So, further support for following my three-prong annuity investigation/evaluation approach before considering or adding any annuity to a plan.

The courts have consistently stated that costs qualify as “material information.” As mentioned in the post, per the DOL and GAO, over a twenty year period, each additional 1 percent in fees, cost or anything thst reduces an investor’s end return, e.g., spreads, reduces an investor’s end return by approximately 17 percent. A common 2 percent spread would project to a 34 percent loss, more than one-third , of the value of the investor’s account. Still think it’s not important to make the annuity salesman provide written information on spreads and cumulative costs?

Plan sponsors, share this post with your plan’s investment commitee. As leading ERISA attorney, Fred Reish, likes to say, “forewarned is forearmed.”

Notes 1. Restatement Third, Trusts Section 78(3). 2. Fink v. Nat’l Bank and Trust, 772 F.2d 962 3. In re Unisys Sav. Plan Litigation, 74 F.3d 420, 436 (3d. Cir. 1996) 4. Liss v. Smith, 991 F. Supp. 278, 299 (S.D.N.Y. 1998). (Liss), In re Enron Corp. Securities, Derivatives, and ERISA Litigation, 284 F. Supp. 2d 511, 546 (N.D. Tex 2003) 2. Donovan v. Cunningham, 716 F.2d 1455, 1467 (5th Cir. 1983 5. Basic v. Levinson, 108 S. Ct. 978, 983 (1988) 6. STORM IA analysis (STORM) 8. STORM 9. STORM 10. Moshe Milevsky and Steven E. Posner, “The Titanic Option: Valuation of the Guaranteed Death Benefit in Variable Annuities and Mutual Fund,” Journal of Risk Management and Inssurancce, Vol. 68, No. 1, (2009), 91-126, 92. 11.John D. Johns,”The Case for Change,” Financial Planning, 158-168, 158 (September 2004) (Johns) 12. Chamber of Commerce of the United States, et. al. v Hugler, 231 F. Supp. 3d 152 (N.D. Tex. 2017) (Lynn decision), 187 13. Reichenstein, W. (2009), “Financial Analysis of Equity Indexed Annuities,” Financial Services Review, 18, 291-311, 303 (Reichenstein) 14. Reichenstein, 303 15. Jonathan Clements, “Big Insurers Avoid Equity-Indexed Annuities, Wall Street Journal, (as published in Pittsburgh Post Gazette), January 14, 2006. 16. Collins, P.J., Lam, H., & Stampfi, J. (2009) “Equity indexed annuities: Downside protection, But at What Cost? Journal of Financial Planning,” 22, 48-57.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Lori Chavez-DeFemer has been approved as the new Secretary of Labor. With time still remaining on the 60-day period that the Fifth Circuit granted the DOL to decide on whether the DOL would appeal the stays granted by two Texas district courts. some decisions will need to be made in order to protect the future of the Retirement Security Rule (Rule).

Fortunately, I believe Head Judge of the Northern District of Texas, Judge Barbara Lynn, and Head Judge of the Fifth Circuit, Judge Carl E. Stewart, have seemingly made the DOL’s decision a no-brainer as a result of the judges’ decisions. Both Judge Lynn and Judge Stewart have come out in support of the Rule. While it is doubtful that the Fifth Circuit will similarly rule in the DOL’s favor, that is to expected since the financial services and annuity industries always run to the Fifth Circuit for protection against proposed laws holding their industries to a higher standard of care and greater investor protection.

However, at this point, I believe that the DOL has to look at the bigger picture, the potential for having the courts, specifically SCOTUS, decide the case. The fact that two well-respected federal judge have submitted excellent, well-reasoned opinions supporting the DOL’s process in creating and submitting the Rule cannot be overlooked in projecting the potential outcome before SCOTUS.

Judge Lynn’s detailed analysis clearly indicated she knew that the Fifth Circuit would not look favorably upon her decision. As a result, she did a masterful job of addressing the possible arguments that the Fifth Circuit would raise relative to the Chevron decision. While the Fifth Circuit continues to refuse to rule on the actual merits of her decision, opting to simply issue a stay of her decision, they essentially said she exceeded her authority and that her decision was “arbitrary and capricious,” essentially with no legal basis and/or support. I have provided a link to Judge Lynn’s order at the end of this post so the reader can decide for themselves who has the better argument, Judge Lynn or the Fifth Circuit.

Some of they key points raised by Judge Lynn in her opinion include

The DOL described the complexity of FIAs (fixed indexed annuities) in its Regulatory Impact Analysis (“RIA”). The RIA explained that FIAs generally provide “crediting for interest based on changes in a market index,” but noted there are hundreds of indexed annuity products, thousands of index annuity strategies, and that “the selection of the crediting index or indices is an important and often complex decision.” Further, there are several methods for determining changes in the index, with different methods resulting in varying rates of return. Rates of return are also affected by “participation rates, cap rates, and the rules regarding interest compounding.” Because “insurers generally reserve rights to change participation rates, interest caps, and fees,” FIAs can “effectively transfer investment risks from insurers to investors.” The DOL found that FIAs may offer guaranteed living benefits, but such benefits “may come at an extra cost and, because of their variability and complexity, may not be fully understood by the consumer.” The DOL also cited the SEC, which recently stated, “[y]ou can lose money buying an indexed annuity … even with a specified minimum value from the insurance company, it can take several years for an investment in an indexed annuity to break even.1 (emphasis added)

The DOL found the annuity market to be influenced by contingent commissions, which “align the insurance agent or broker’s incentive with the insurance company, not the consumer,” that existing protections do not “limit or mitigate potentially harmful adviser conflicts,” and that “notwithstanding existing [regulatory] protections, there is convincing evidence that advice conflicts are inflicting losses on IRA investors.” The DOL found the conflicts would cost investors “at least tens and probably hundreds of billions of dollars over the next 10 years … despite existing consumer protections,” and that “the material market changes in the marketplace since 1975 have rendered [prior regulation] obsolete and ineffective.”2

The extensive changes in the retirement plan landscape and the associated investment market in recent decades undermine the continued adequacy of the original approach in PTE 84–24. In the years since the exemption was originally granted in 1977, the growth of 401(k) plans and IRAs has increasingly placed responsibility for critical investment decisions on individual investors rather than professional plan asset managers. Moreover, at the same time as individual investors have increasingly become responsible for managing their own investments, the complexity of investment products and range of conflicted compensation structures have likewise increased. As a result, it is appropriate to revisit and revise the exemption to better reflect the realities of the current marketplace.3

Judeg Stewart left no doubt as to his opinion on both the propriety of the DOL’s proposal of the Rule and Judge Lynn decision. Judge Stewart apparently felt so strongly that he felt the need to call out his brethren for what he termed their “strained” decision..

Over the last forty years, the retirement-investment market has experienced a dramatic shift toward individually controlled retirement plans and accounts. Whereas retirement assets were previously held primarily in pension plans controlled by large employers and professional money managers, today, individual retirement accounts (“IRAs”) and participant-directed plans, such as 401(k)s, have supplemented pensions as the retirement vehicles of choice, resulting in individual investors having greater responsibility for their own retirement savings. This sea change within the retirement-investment market also created monetary incentives for investment advisers to offer conflicted advice, a potentiality the controlling regulatory framework was not enacted to address. In response to these changes, and pursuant to its statutory mandate to establish nationwide “standards . . . assuring the equitable character” and “financial soundness” of retirement-benefit plans, 29 U.S.C. § 1001, the Department of Labor (“DOL”) recalibrated and replaced its previous regulatory framework. To better regulate conflicted transactions as concerns IRAs and participant-directed retirement plans, the DOL promulgated a broader, more inclusive regulatory definition of investment-advice fiduciary under the Employee Retirement Income Security Act of 1974 (“ERISA”) and the Internal Revenue Code (“the Code”). Despite the relevant context of time and evolving marketplace events, Appellants and the panel majority skew valid agency action that demonstrates an expansive-but-permissible shift in DOL policy as falling outside the statutory bounds of regulatory authority set by Congress in ERISA and the Code. Notwithstanding their qualms with these regulatory changes and the effect the DOL’s exercise of its regulatory authority might have on certain sectors of the financial services industry, the DOL’s exercise was nonetheless lawful and consistent with the Congressional directive to “prescribe such regulations as [the DOL] finds necessary or appropriate to carry out [ERISA’s provisions].”4

In the decades following the passage of ERISA, the use of participant directed IRA plans has mushroomed as a vehicle for retirement savings. Additionally, as members of the baby-boom generation retire, their ERISA plan accounts will roll over into IRAs. Yet individual investors, according to DOL, lack the sophistication and understanding of the financial marketplace possessed by investment professionals who manage ERISA employersponsored plans. Further, individuals may be persuaded to engage in transactions not in their best interests because advisers like brokers and dealers and insurance professionals, who sell products to them, have “conflicts of interest.” DOL concluded that the regulation of those providing investment options and services to IRA holders is insufficient.5

The panel’s majority conclusion that the DOL exceeded its regulatory authority by implementing the regulatory package that included a new definition of investment-advice fiduciary and both modified and created new exemptions to prohibited transactions is based on an erroneous interpretation of the grant of authority given by Congress under ERISA and the Code.6

Despite the relevant context of time and evolving marketplace events, Appellants and the panel majority skew valid agency action that demonstrates an expansive-but-permissible shift in DOL policy as falling outside the statutory bounds of regulatory authority set by Congress in ERISA and the Code. Notwithstanding their qualms with these regulatory changes and the effect the DOL’s exercise of its regulatory authority might have on certain sectors of the financial services industry, the DOL’s exercise was nonetheless lawful and consistent with the Congressional directive to ‘prescribe suchregulations as [the DOL] finds necessary or appropriate to carry out [ERISA’sprovisions.7

For 41 years, the DOL employed a five-part test to determine whether a person is an investment-advice fiduciary under ERISA and the Code, and that test limited the reach of the statutes’ prohibited transaction rules to those who rendered advice “on a regular basis,” and to instances where such advice “serve[d] as a primary basis for investment decisions with respect to plan assets.” See 29 C.F.R. § 2510.3–21(c)(1) (2015). This regulation “was adopted prior to the existence of participant-directed 401(k) plans, the widespread use of IRAs, and the now commonplace rollover of plan assets” from Title I plans to IRAs, thus leaving out of ERISA’s regulatory reach many investment professionals, consultants, and advisers who play a critical role in guiding plans and IRA investments. Fiduciary Rule, 81 Fed. Reg. 20,946.8

In 1975, DOL promulgated a five-part conjunctive test for determining who is a fiduciary under the investment-advice subsection. Under that test, an investment-advice fiduciary is a person who (1) “renders advice…or makes recommendation[s] as to the advisability of investing in, purchasing, or selling securities or other property;” (2) “on a regular basis;” (3) “pursuant to a mutual agreement…between such person and the plan;” and the advice (4) “serve[s] as a primary basis for investment decisions with respect to plan assets;” and (5) is “individualized . . . based on the particular needs of the plan.”9

The rule challenged on appeal addresses these and other changes in the retirement investment advice market by, inter alia, abandoning the five-part test in favor of a definition of fiduciary that includes “recommendation[s] as to the advisability of acquiring . . . investment property that is rendered pursuant to [an] . . . understanding that the advice is based on the particular investment needs of the advice recipient.10

The DOL’s interpretation of “renders investment advice” is reasonably and thoroughly explained. The new interpretation fits comfortably with thepurpose of ERISA, which was enacted with “broadly protective purposes” and which “commodiously imposed fiduciary standards on persons whose actionsaffect the amount of benefits retirement plan participants will receive”. In light of changes in the retirementinvestment advice market since 1975, mentioned above, the DOL reasonably concluded that limiting fiduciary status to those who render investment advice to a plan or IRA “on a regular basis” risked leaving retirement investors inadequately protected. This is especially so given that “one-time transactions like rollovers will involve trillions of dollars over the next five years and can be among the most significant financial decisions investors will ever make.”11

Notwithstanding the DOL’s reasoned explanation for the new regulations, the panel majority maintains that the DOL acted unreasonably and arbitrarily when it promulgated the new fiduciary rule and, in a strained attempt to justify this conclusion, the panel majority disregards the requirement of showing judicial deference under Chevron by highlighting purported issues with other provisions of the regulation. Each of the panel majority’s positions fails.12(emphasis added)

In light of changes in the retirement investment advice market since 1975,…, the DOL reasonably concluded that limiting fiduciary status to those who render investment advice to a plan or an IRA “on a regualr basis” risked leaving retirement investors inadequately protected. This is especailly so given that “one-time transactions like rollovers will involve trillions of dollars over the next five years and can be among the most significant financial decisions investors will ever make.13

The panel majority’s conclusion that the DOL exceeded its regulatory authority by implementing the regulatory package that included a new definition of investment-advice fiduciary and both modified and created new exemptions to prohibited transactions is premised on an erroneous interpretation of the grant of authority given by Congress under ERISA and the Code. I would hold that the DOL acted well within its regulatory authority—as outlined by ERISA and the Code—in expanding the regulatory definition of investment-advice fiduciary to the limits contemplated by the statute, and would uphold the DOL’s implementation of the new rules.14

Congress was concerned to protect all retail inbvestment clients, and there is no evidence that Congress expected DOL to more restrictively regulate a trillion dollar portion of the market when it delegated the general question to the SEC (for broker-dealers and registered investment advisers) and conditionallly deferred to state insurance practices.15

Armed with these two excellent opinions from two highly respected federal judges, one could argue that a decision by the DOL not to pursue the appeals, as well as pursue this case all the way to SCOTUS, if necessary, would constitute a betrayal of both American workers and the spirit of ERISA.

Non-attorneys might consider that an extreme statement. But I believe that trial attorneys would back me up, given the strength of having two well-respected federal judges unconditionally supporting the propriety of and need for the DOL’s proposed Retirement Security Rule.

The DOL Knew that the Rule would face serious obstacles, including the fact that the financial services and annuity industries would run to seek the Fifth Circuit’s protection. But when Judge Lynn issued a spot on and masterful opinion upholding the Rule, the Fifth Circuit’s “strained ” opinion attempting to “dismiss” Judge Lynn by calling her opinion “arbitrary and capricious”, Judge Stewart seemingly felt compelled to call his brethern on Fifth Circuit out and set the record straight.

Both Judge Lynn and Judge Stewart displayed an incredible amount of courage for stepping forward and issuing opinions that they no doubt knew would draw criticism from the financial services and annuity industries. They should be commended for doing the right thing and trying to protect American workers and preserving the spirit of ERISA.

Whenever I see someone display such courage and conviction, I am reminded of three quotes that I pften used in my closing argument to challenge jurors:

Facts are stubborn things; and whatever may be our inclinations , or the distates of our passions, they cannot alter the state of facts and evidence. – John Adams

The truth is we always know the right thing to do. The hard part is doing it. – General Norman Schwartzkopf

Knowing the right thing to do, and not doing it, is the worst kind of cowardice. – Confucius

Hopefully, the DOL will decide to take advantage of the situation it has been dealt with Judge Lynn and Judge Stewart’s support. While I believe it may require the help of SCOTUS to resolve this case, I like the DOL’s chances before SCOTUS.

One final thought. ERISA attorney Bonnie Treichel, arguably offered the best observation on this whole case: “Arguably the most impacted perties then are the investors these individuals serve that aren’t provided service as an ERISA fiduciary16

For fellow legal nerds, Judge Lynn’s opinion and Judge Stewart’s dissenting opinion can be found at the following links:

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Listening to the recent oral arguments before SCOTUS in the Cunningham v. Cornell University case, I was both disappointed and encouraged by the questions and comments of some of the Justices. After all, the justices are supposedly among the best and the brightest attorneys in the legal profession.

And yet, I found some of the comments disingenuous and further evidence of what appears to be an ongoing financial services-courts complex, one that. IMHO, too often seems to disregard the reasons that ERISA was deemed necessary and protect employers and the financial services industry at the expense of plan participants. I could not help but notice that the lawyers and several justices referenced the asymmetry of important information between plan participants and plan sponsors.

Several justices cited the plans’ red herring of “expensive discovery” as a compelling factor in favor these 401k br3ach cases. Justice Kavanaugh is arguably the most knowledgeable of the current Supreme Court justices when it comes to ERISA. He cited the number of cases filed by Jerry Schlichter, suggesting the need to address the number of cases based on the alleged “expensive discovery” involved with such cases, without mentioning the relative merits of such cases.

Fortunately, Justice Jackson countered by suggesting that there were other viable options to address such concerns, notably limited and/or “controlled discovery” rather than unnecessarily denying employees the rights and protections guaranteed to them under ERISA, including the access to the courts to enforce such rights and protections. I maintain that allowing “controlled discovery,: including discovery of a plan’s advisory contract and the minutes from the plan’s meetings would be in furtherance with the overall purpose and goals of ERISA, without being onerous to a plan.

The main issue in Cunningham v. Cornell University has to do with what constitutes sufficient pleading in ERISA actions, the specificity required in the employees’ complaint. The Federal Rules of Civil Procedure (F.R.C.generally adopt a “notice pleading” standard that simply requires that a plaintiff provide sufficient information to let the defendant know to nature of the complaint, the alleged wrongdoing. This simple requirement acknowledges the fact that, in many cases, the defendants have greater knowledge of the relevant facts.

As the Solicitor General pointed out in the oral arguments, in ERISA actions, the plan sponsor is typically the only one who actually knows what the plan did and why they did it. And yet some courts continue to prematurely dismiss legitimate fiduciary breach actions based on the inability of the employees to plead the specifics of the plan’s actions, in effect, the employees’ inability to read the plan sponsor’s mind. This would appear to violate Rule 9 of the FRCP, which states that plaintiffs are not required to plead a defendant’s state of mind.

Interestingly, some jurists have stepped up and recognized the asymmetry issue in ERISA actions, most notably Sixth Circuit Chief Judge Sutton. In his TriHealth decision, Judge Sutton offered this observation

But at the pleading stage, it is too early to make these judgment calls. ‘In the absence of further development of the facts, we have no basis for crediting one set of reasonable inferences over the other. Because either assessment is plausible, the Rules of Civil Procedure entitle [the three employees] to pursue [their imprudence] claim (at least with respect to this theory) to the next stage.1

This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth ‘investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares’ because ‘the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….’ Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.2

As Judge Sutton referenced, the court has a number of options available to control the costs of discovery. Judge Sutton was presumably talking about options such as limited and/or “controlled” discovery, where a judge can limit discovery to only such facts and documents relative to the case at hand. Presumably, the costs of such discovery could involve nothing more than copying costs, with perhaps some follow-up discovery and a few depositions. In some cases, follow-up requests for admissions and/or production may provide the needed discovery information.

One interesting aspect of the Cornell case is the fact that it comes from the Second Circuit. The Second Circuit is the Circuit that addressed a burden of proof issue in Sacerdote v. New York University,3 correctly citing the Restatement and ruling that the burden of proof on causation properly belongs with the plan sponsor, but adding that

If a plaintiff succeeds in showing that “no prudent fiduciary” would have taken the challenged action, they have conclusively established loss causation, and there is no burden left to “shift” to the fiduciary defendant.4

I believe the Second Circuit is spot on. However, with Cunningham, the issue is what is required from the employees/plaintiffs to prove the breach and loss. I believe the Solicitor General’s amicus brief correctly presented the question and the solution.

When a plaintiff brings suit against a [plan sponsor]for breach of trust, the plaintiff generally bears the burden of proof . The general rule, however, is moderated in order to take account of the [plan sponsor’s]duties of disclosure …as well as the [plan sponsor’s] (often, unique access to information about the [plan] and its activities, and also to encourage the plan sponsor’s compliance with applicable fiduciary duties.5

Courts should generally not depart from the usual practice under [the Federal Rules of Civil Procedure](F.R.C.P) on the basis of perceived policy concerns. In any event, a district court has various tools to screen out implausible claims. To survive a motion to dismiss under F.R.CP. 12(b)(6), a compliant must plead “enough facts to state a claim for relief that is plausible on its face. (citing Bell Atl. Corp v. Twombly, 550 U.S. 544, 570 (2007); Ashcroft v. Iqbal, 556 U.S. 662, 678 (2009)…[A]n inference pressed by the plaintiff is not plausible if the facts he points to are precisely the result one would expect from lawful conduct in which the defendant is known to have engaged.6

As a practical matter, moreover, it is not clear what additional facts petitioners could have alleged that would have satisfied the court of appeals, without the benefit of discovery….[P]articipants would likely require discovery into additional facts in the fiduciaries’ possession-such as the terms of of the contract, the range of contracted services, and performance metrics that justify the fees charged-to ascertain the quality and full extent of the services provided.7

As Justice Jackson pointed out, there are cost-efficient methods of controlling the costs associated with ERISA litigation. I would argue that the Court should follow its own advice in Tibble

We have often noted that an ERISA fiduciary’s duty is ‘derived from the common law of trusts.’ In determining the contours of an ERISA fiduciary’s duty, courts often must look to the law of trusts.(citations omitted) 8

In the Cunningham case, perhaps the Court should look to Section100, comment f, of the Restatement (Third) of Trusts and accordingly shift the burden of proof on causation to plan sponsors, especially given the fact that several justices’ acknowledged the asymmetrical possession of relevant info in these cases.

Requiring employee/ plaintiffs to plead greater specificity, without allowing the discovery necessary to allow them to do so would make a mockery of ERISA’s goals and purposes and unnecessarily and inequitably deny employees their much needed access to the courts to protect their rights and guarantees under ERISA, which are needed given the current number and complexity of investment options offered within most plans.

[T]he Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection and beneficiaries, ERISA’s adoption reflected ‘Congress'[s] desire to offer employees enhanced protection for their benefits….In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection that they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.9

The fiduciary is in the best position to provide information about how it would have made investment decisions in light of the objectives of a particular plan and the characteristics of plan participants. Indeed, this Court recognized in Schaffer that ii is appropriate in some circumstances to shift the burden to establish ‘facts particularly within the knowledge’ of one party.10

Notes 1. Forman v. TriHealth, Inc., 40 F.4th 443, 450. (TriHealth) 2. TriHealth, 450. 3. Sacerdote v. New York University, 9 F.4th 95. (Sacerdote) 4. Sacerdote, 113 5. Solicitor General’s Amicus Brief in Brotherston v. Putnam Investments, LLC, https://www.justice.gov/usdoj-media/osg/media/1035476/dl?inline. (Brotherston amicus), 8 6. Solicitor General amicus brief, Cunningham v. Cornell University, https://www.supremecourt.gov/DocketPDF/23/23-1007/333121/20241202200914652_23-1007tsacUnitedStates.pdf.(Cunningham amicus), 29. 8.Tibble v. Edison International, Inc, 135 S. Ct. 1823, 1828 (2015) (Tibble) 9. Brotherston amicus, 37. 10. Brotherston amicus, 11.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Looking at the ERISA litigation landscape for 2025, I think there are three clear-cut cases that may shape the future of ERISA litigation and ERISA itself: the ongoing litigation in the Fifth Circuit over the DOL’s Retirement Security Rule (Rule)1, the Sixth Circuit’s Parker-Hannifin case (Hannifin)2, and the Cunningham v. Cornell University (Cornell)3 case, which is scheduled for oral arguments before SCOTUS on January 22, 2025. I believe SCOTUS’ decision in the Cornell case will likely impact the ultimate disposition of both of the other two cases.

I have already posted my opinion on the 5th Circuit’s actions in connection with the Retirement Security Rule. I believe District Court Judge Barbara Lynn’s decision upholding and her supporting rationale was spot on. The dissenting opinion filed by Fifth Circuit Chief Judge Stewart in connection with the Court’s decision to stay the effectiveness of the Rule was equally on point.4

There has been no movement in the case since the stay was issued in July, effectively leaving plan participants vulnerable to the annuity industry’s abusive marketing tactics that necessitated the creation of the Rule in the first place. As Judge Lynn pointed out in her decision5upholding the Rule, FIAs involve investor/consumer interest issues that clearly work to the benefit of the FIA issuer at the expense of the annuity owner.

[I]nsurers generally reserve the right to change participation rates, interest caps, and fees, FIAs can effectively transfer investment risks from insurers to investors….You can lose money buying indexed annuities….even with a specified minimum value from the insurance company, it can take several years for an investment in an indexed annuity to breakeven.6

Such uncertainty also effectively prevents plan sponsors, from complying with ERISA’s requirement that they conduct independent and objective fiduciary prudence investigations and evaluations on each investment offered within a plan.

As for the Parker-Hannifin case, there are several ERISA related issues involved in the case, including pleading issues, including who has the burden of proof on the issue of causation of damages. The importance of the case and its issues is reflected in the number of amicus briefs that have already been filed, most notably the amicus brief of the U.S. Solicitor General.

As a fiduciary risk management counsel, one of my services is to help plan sponsors understand the importance of developing a sound, legally compliant fiduciary process for a plan to follow in selecting and monitoring a plan’s investment options. To make the technical complexities of ERISA and fiduciary compliance simpler to understand I created what I call the Fiduciary Prudence CircleTM (Circle). In my practice, I recommend that my clients use the Circle as the foundation for developing a sound fiduciary prudence process that will withstand judicial scrutiny.

Tibble v. Edison International7 is a cornerstone decision in developing a prudent fiduciary process. Courts often cite Tibble for the fact that the Supreme Court (SCOTUS) officially recognized the Restatement of Trusts (Restatement) as a legitimate resource in resolving questions about fiduciary prudence. The Restatement of Trusts is essentially a codification of the common law of trusts. As SCOTUS noted

We have often noted that an ERISA fiduciary’s duty is ‘derived from the common law of trusts.’ In determining the contours of an ERISA fiduciary’s duty, courts often must look to the law of trusts.(citations omitted)8

So, the obvious question would appear to be – “What standards does the Restatement establish with regards to fiduciary Prudence?”

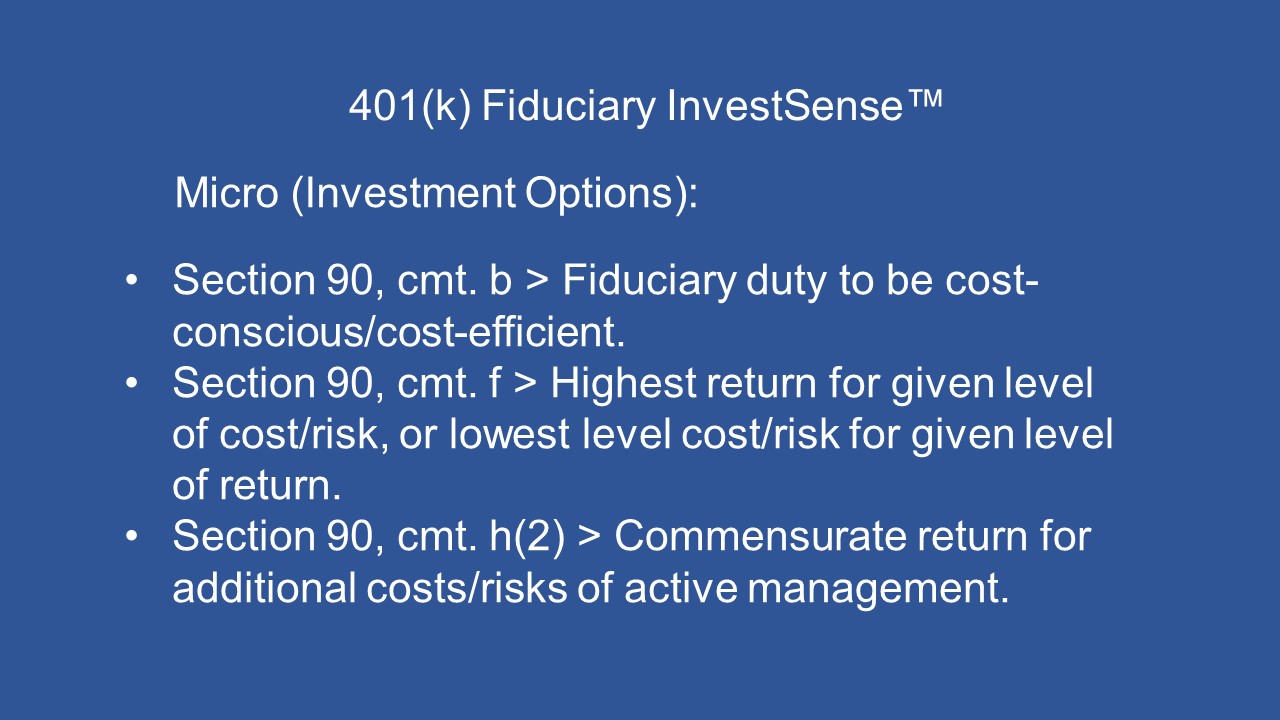

I believe that that three comments in Section 90, aka the Prudent Investor Rule, merit special attention for plan sponsors and other investment fiduciaries – comments b, f, and h(2).

Comments b and f focus on cost-efficiency. In 2015, the DOL issued Interpretive Bulletin 15-019(IB 15-01). IB 15-01 reinstated earlier language from Interpretive Bulletin 94-14, specifically the following:

Consistent with fiduciaries’ obligations to choose economically superior investments….[P]lan fiduciaries should consider factors that potentially influence risk and return.5 (emphasis added)10

[B]ecause every investment necessarily causes a plan to forgo other investment opportunities, an investment will not be prudent if it would provide a plan with a lower expected rate of return than available alternative investments with commensurate degrees of risk or is riskier than alternative available investments with commensurate rates of return.11

Sure sounds a lot like comment f from Section 90 of the Restatement. Sure sounds like further support for the use of cost-benefit analysis in evaluating the fiduciary prudence of the decisions of plan sponsors and other investment fiduciaries. Sure sounds like further support for the Active Management Value Ratio metric, which measures the cost-efficiency of an actively managed mutual fund relative to a comparable index fund.

Comment h(2)12focuses on the concept of commensurate return, or return relative to the additional risk and cost incurred by an investor. This is further support for simple cost-benefit analysis as part of any fiduciary prudence process. Cost-benefit analysis is a common practice in the business world in evaluating the viability of a project. However, the financial services industry and the annuity industry have essentially rejected the use of cost-benefit analysis. I would suggest that there is a good reason for such rejection.

That reason may become even more significant if SCOTUS rules that plan sponsors carry the burden of proof on the issue of causation, which I believe is exactly how SCOTUS will rule in Cunningham v. Cornell, based on not only the Solicitor General’s most recent amicus brief to the court, but also on the amicus brief that the Solicitor General filed in connection with the Brotherston case.13 I belleve that earlier amicus brief, combined with the First Circuit ‘s Brotherston decision and the Solicitor General’s amicus brief provided an outstanding analysis of why the plan sponsor, both logically and by necessity, must be the party responsible for carrying the burden of proof on the issue of causation.

Both the First Circuit and the Solicitor General referenced Section 100 of the Restatement in their arguments. Section 100, comment (b) endorses the use of index funds as comparators in assessing the prudence of actively managed funds in plans, while Section 100 comment (f) addresses the allocation of the burden of proof.

When a plaintiff brings suit against a [plan sponsor]for breach of trust, the plaintiff generally bears the burden of proof . The general rule, however, is moderated in order to take account of the [plan sponsor’s]duties of disclosure …as well as the [plan sponsor’s] (often, unique access to information about the [plan] and its activities, and also to encourage the plan sponsor’s compliance with applicable fiduciary duties.15

That is what is so puzzling about the reluctance of some courts to follow the Restatement and shift the burden of proof to the party with the necessary information once the plaintiff has met its duty to plausibly plead its claims and establish a resulting loss from such fiduciary breaches. Since SCOTUS has already legitimized the Restatement as a resource in cases involving fiduciary cases, it would seem justifiable that the Court will reference Section f in ruling that the burden of proof as to causation once the plaintiff plausibly pleads a breach of fiduciary duty and provides evidence of the resulting loss. Common sense and common law.

In Brotherston, the First Circuit recognized the importance of Section 100 by stating that

[T]he Restatement specifically identifies as an appropriate comparator for loss calculation purpose ‘return rates of one or more …suitable index mutual funds or market indexes (with such adjustments as may be appropriate.16 (citing Section 100, comment b(1)

ERISA itself is not so specific. Rather it states that a breaching fiduciary shall be liable to the plan for ‘any losses to the plan resulting from each such breach. Certainly the text is broad enough to accommodate the total return recognized in the Restatement. Behind the text, too, stands Congress’ clear intent ‘to provide the courts with broad remedies for redressing the interests of participants and beneficiaries when they have been adversely affected by breaches of fiduciary duty.17

[T]he Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection and beneficiaries, ERISA’s adoption reflected ‘Congress'[s] desire to offer employees enhanced protection for their benefits….In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection that they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.18

The Solicitor General also filed an amicus brief in connection with SCOTUS’ consideration on whether to grant certiorari and hear Putnam LLC’s appeal of the First Circuit’s Brotherston decision. While SCOTUS ultimately decided not to review the First Circuit’s, due largely to the fact that it was an interlocutory appeal, as the trial was technically still ongoing, the Solicitor General cited Section 100, comment f, on the burden of proof issue, stating that

Under trust law, ‘when a beneficiary has succeeded in proving that the trustee has committed a breach of trust and that a related loss has occurred, the burden of proof shifts to the [fiduciary] to prove that the loss would have occurred in the absence of the breach.19

I would, and have, argued, that the concept of incorporating the simple arithmetic of cost-benefit analysis, in the form of the Active Management Value Ratio metric, accomplishes the stated goal while complying with any counterproductive effects other than establishing a fiduciary’s breach of duty. Furthermore, cost-benefit analysis and, in the case of annuities, breakeven analysis, factoring in both present value and mortality risk, will more often than not prevent a plan sponsor from carrying their burden of proof on the issue of causation, assuming the plan participants carry their preliminary burden of both breach and resulting loss.

The Supreme Court has time and again adopted ordinary trust law principles to construe ERISA in the absence of explicit textual direction.20

The First Circuit also noted many of the same issues and concerns addressed in the Solicitor General’s amicus brief, including “Congress’ indicated desire to ‘offer employees enhanced protection of their benefits,” and “Congress’ intent to offer [plan participants], not plan sponsors, more protection than they had a common law.

The Supreme Court has time and again adopted ordinary trust law principles to construe ERISA in the absence of explicit textual direction.21

The Solicitor General filed an excellent amicus brief with the SCOTUS, also referencing Section 100, stating that

[A] beneficiary has the burden of showing only ” a prima facie case,’ at which point ‘the burden of contradicting it or showing a defense will shift to the [plan sponsor.’22

Applying trust law’s burden shifting framework to ERISA fiduciary -breach claims also furthers ERISA’s purposes. In trust law, burden shifting rests on the view that ‘as between innocent [plan participants] and a defaulting [plan sponsor], the latter should bear the risk of uncertainty as to the consequences of its breach of duty.23

ERISA reflects congressional intent to provide more protections than trust law. Applying trust law’s burden shifting framework, which can serve to deter ERISA fiduciaries from engaging in wrongful conduct, thus advances ERISA’s protective purposes. By contrast, declining to apply trust-law’s burden-shifting framework could create significant barriers to recovery for conceded fiduciary breaches.24

The fiduciary is in the best position to provide information about how it would have made investment decisions in light of the objectives of a particular plan and the characteristics of plan participants. Indeed, this Court recognized in Schaffer that ii is appropriate in some circumstances to shift the burden to establish ‘facts particularly within the knowledge’ of one party.25

[T]he ‘common sense concern’ underscoring a burden-shifting regime is that ‘it makes little sense to have the plaintiff hazard a guess as to what the [plan sponsor would have done had it not breached its duty.26

The First Circuit’s Brotherston opinion set out many of the same concerns ands rationales as the Solicitor General’s amicus brief.

This from the Solicitor General’s 2024 amicus brief:

Courts should generally not depart from the usual practice under [the Federal Rules of Civil Procedure](F.R.C.P) on the basis of perceived policy concerns. In any event, a district court has various tools to screen out implausible claims. To survive a motion to dismiss under F.R.CP. 12(b)(6), a compliant must plead “enough facts to state a claim for relief that is plausible on its face. (citing Bell Atl. Corp v. Twombly, 550 U.S. 544, 570 (2007); Ashcroft v. Iqbal, 556 U.S. 662, 678 (2009)(emphasis added)27…[A]n inference pressed by the plaintiff is not plausible if the facts he points to are precisely the result one would expect from lawful conduct in which the defendant is known to have engaged.27

The Federal Rules of Civil Procedure establish the rules of pleading in the federal (and generally all) courts. Under F.R.C.P. 8,28 plaintiffs are generally held to “notice pleading, simply providing enough information to apprise the defendant of the nature of the plaintiff’s claims. However F.R.C.P Rule 9, “Pleading Special Matters,” Subsection (b), “Fraud or Mistake, Conditions of the Mind,” states that “Malice, intent knowledge and other conditions of a person’s mind may be alleged generally.29 I maintain that since plan participants are generally not aware of the deliberative process used by a plan’s investment committee, courts demanding specific allegations as to an investment committee’s processes, if any, are trying to force plan participants to do more than they are required to do under the F.R.C.P,

The Solicitor General addressed such concerns as well:

[P]etitioners’s factual allegations sufficed to plausibly allege that the challenged transactions for recordkeeping services were not obviously reasonable.30