With the Supreme Court’s new term scheduled to begin in a few days, we move closer to the Court hearing the Northwestern University 403b case. I believe that this case has the potential to be a landmark case, not just regarding the future of 401(k) and 403(b) litigation, but also for fiduciary litigation in general.

For that reason, I cannot help but think of two relevant quotes:

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”1

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.2

The first quote is from the First Circuit’s 2018 Brotherston v. Putnam Investments, LLC decision. The second quote is from a 1976 article written by John H. Langbein and Richard A. Posner, published shortly after the release of the Restatement (Third) of Trusts. Langbein served as the Reporter on the Restatement committee.

These quotes will obviously gain greater importance if SCOTUS effectively shifts the burden of proof regarding causation to 401(k) and 403(b) plan sponsors, as well as investment fiduciaries in general.

On Investment Selection: Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs…. The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.”1 Nobel laureate Dr. William F. Sharpe

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.2 – Burton G. Malkiel

Your chances of selecting the top-performing funds of the future on the basis of their returns in the past are about as high as the odds that Bigfoot and the Abominable Snowman will both show up in pink ballet slippers at your next cocktail party. In other words, your chances are not zero—but they’re pretty close.3 Benjamin Graham

Most fund buyers look at past performance first, then at the manager’s reputation, then at the riskiness of the fund, and finally (if ever) at the fund’s expenses.8 The intelligent investor looks at those same things—but in the opposite order. Since a fund’s expenses are far more predictable than its future risk or return, you should make them your first filter.4 Benjamin Graham

Financial scholars have been studying mutual-fund performance for at least a half century, and they are virtually unanimous on several points: the average fund does not pick stocks well enough to overcome its costs of researching and trading them; the higher a fund’s expenses, the lower its returns; the more frequently a fund trades its stocks, the less it tends to earn; highly volatile funds, which bounce up and down more than average, are likely to stay volatile; funds with high past returns are unlikely to remain winners for long.5 Benjamin Graham On Cost-Efficiency and Overall Prudence: So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!6 Charles D. Ellis

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funs engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.7 Ross Miller

a large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by for fees for active management that they do not receive or receive only partially….Such funds are not just poor investments; they promise investors a service that they fail to provide.8 Martijn Cremers

Active vs. Passive Investing: “Prudent investment principles …allow the use of more active management strategies by trustees, “if the costs are ‘justified’ in comparison to ‘realistically evaluated return expectations’. 9 Restatement (Third) of Trusts, Section 90, cmt. h(2)

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.10 Laurent Barras, Olivier Scaillet and Russ Wermers

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.11 Charles D. Ellis

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.12 Philip Meyer-Braun,

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.13 Mark Carhart

Investment Litigation Risk Management: When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.14 John H. Langbein and Richard A. Posner

Note: This is exactly what the First Circuit Court of Appeals mentioned in its Brotherston v. Putnam Investments, LLC decision. As legendary ERISA attorney Fred Reish likes to say, “forewarned is forearmed.

And the one many judges love to cite: “[A] pure heart and an empty head are not enough” to defeat a breach of fiduciary duty claim.15

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

The financial adviser tells you that a fund has a five-year compound return of 20 percent.

The fund’s advertisement tells you that the fund has a five-year compound return of 20 percent.

Morningstar tells you that the fund has a five-year compound return of 20 percent.

So why would I possibly tell you not to buy the fund? Because the fund might not be cost efficient, its incremental costs may exceed its incremental returns. Any investment whose incremental costs exceed its incremental returns is never a prudent investment.

[A] large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by for fees for active management that they do not receive or receive only partially….

Closet indexing raises important legal issues. Such funds are not just poor investments; they promise investors a service that they fail to provide. As such, some closet index funds may also run afoul of federal securities laws.1

Closet indexing has become an international issue for the very reasons stated above. Closet indexing refers to a situation where a fund charges a high expense ratio, citing the benefits of the fund’s active management. However, the fund shows a high correlation of returns to a much less expensive, comparable index fund with the same, or better, returns.

Financial advisers and actively managed mutual funds do not like to talk about the costs associates with their funds. Research has consistently shown that the overwhelming majority of actively managed are not cost efficient.

99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.7

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.8

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.9

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.10

Correlations Matter Financial advisers and actively managed funds also do not like to discuss the relationship between a fund’s implicit expense ratio and its correlation of returns with comparable index funds.

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funds engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.2

This quote from Ross Miller, creator of the Active Expense Ratio metric (AER), is one of the three core foundations of my metric, the Active Management Value Ratio AMVR. Using only a fund’s r-squared/correlation data and the fund’s incremental costs relative to a comparable index fund, the AER provides investors and investment fiduciaries with both a fund’s percentage of active management and its implicit expense ratio.

This information is important given the recent trend of actively managed funds to show correlations of returns of 90 or above, many 95 or above, relative to comparable index funds. Many have theorized that the high correlation of return numbers reflects an attempt by actively managed funds to reduce the risk of underperforming comparable, less expensive index funds and possibly losing customers.

The bottom line is that actively managed mutual funds do not adjust their expense ratios in line with their correlation of returns numbers, even though the value of their active management is arguably less. For example, the effective, or implicit, expense ratio of a fund with an r-squared/correlation number of 95 is naturally higher since 95 percent of the fund’s return can be attributed to the market instead of the fund’s active management team.

Miller found that the correlation of return numbers do not reflect a one-to-one percentage of a fund’s active management weight. The AER provides a metric for calculating the percentage of active management provided by a fund, what Miller refers to as “active weight.” Miller then simply divides the incremental costs of an actively managed fund by its active weight number.

What Miller found is that an actively managed fund’s implicit expense ratio, its AER, is often 3-4 times higher, sometimes even higher, than its publicly advertised expense ratio. This obviously has potentially important implications for the cost-efficiency, and prudence, of an actively managed fund.

Putting It All Together

Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs…. The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!4

These two quotes, one from a Nobel laureate Dr. William F. Sharpe and the other from investment icon Charles D. Ellis, provide two of the core foundations for my metric, the Active Management Value Ratio (AMVR). The third core foundation for the AMVR is the AER and correlation-adjusted expense ratios. The AMVR provides investors and investment fiduciaries with a simple, but powerful, method of evaluating the cost-efficiency/prudence of an actively managed relative to a comparable index fund.

Cost-efficiency is a simple enough concept to understand. Do the projected costs of a project exceed the projected benefits of the project? In the case of the AMVR, the question is whether the investment’s incremental costs exceed the investment’s incremental returns. Even better, the AMVR only requires simple, basic math skills, what John Bogle referred to as “humble arithmetic.”:

This emphasis on cost consciousness and the cost-efficiency of investments is consistent with the fiduciary principles set out in the Restatement (Third) of Trusts. The importance of costs and cost-efficiency is also a core concept in the SEC’s Regulation Best Interest (Reg BI). In discussing Reg BI’s provisions regarding costs as a factor in recommending investments, former SEC Chairman Jay Clayton stated that

A rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.5

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.6

One comment about Reg BI by Clayton was particularly interesting regarding its applicability to the concept of InvestSense.

[W]hen a broker-dealer recommends a more expensive security or investment strategy over another reasonably available alternative offered by the broker-dealer, the broker-dealer would need to have a reasonable basis to believe that the higher cost is justified (and thus nevertheless in the retail customer’s best interest) based on other factors….7

When people ask me about the AMVR, I tell them that the AMVR addresses the basic question every investor should ask about an actively managed mutual fund:

Does the actively managed fund provide a commensurate return for the additional costs and risks an investor is asked to assume?

This is a key provision in the Restatement in determining the prudence of actively manageed investments.8 To answer that question, an investor and/or investment fiduciary simply has to answer two simple questions:

Does the actively managed fund provide a positive incremental return relative to a comparable index fund?

If so, does the actively managed fund’s positive incremental return exceed the actively managed fund’s incremental costs?

If the answer to either of these questions is “no,” then the actively managed fund is not a prudent investment choice relative to the benchmark index fund. As far as the actual formula for the AMVR,

To illustrate the value and power of the AMVR in assessing cost-efficiency, let’s look at two well-known actively managed funds, American Funds’ Growth Fund of America retail shares (AGTHX) and Fidelity Contrafund retirement K shares (FCNKX

AGTHX is an actively managed fund that is classified as a Large Cap Growth fund. Like most actively managed mutual funds AGTHX charges investors a front-end load/commission. The front-end load is assessed at the time of each initial purchase, effectively reducing the investor’s actual purchase/investment.

The chart below shows the results of an AMVR forensic analysis of the annualized compound return of AGTHX, using the Vanguard Large Cap Growth Index fund (VIGRX) as the benchmark. Two points to note are (1) the fact that AGTHX fails to provide a positive incremental return, indicating that it is not cost-efficient relative to VIGRX, and (2) the impact of the front-end in reducing AGTHX’s 3-year annualized compound return.

The final point to note is the dramatic increase in AGTHX’s expense ratio (0.65) when the fund’s R-squared/correlation of returns number, in this case 98, is factored into the equation (5.44). The combination of high incremental costs and a high r-squared number basically ensures that a mutual fund will not be considered cost-efficient.

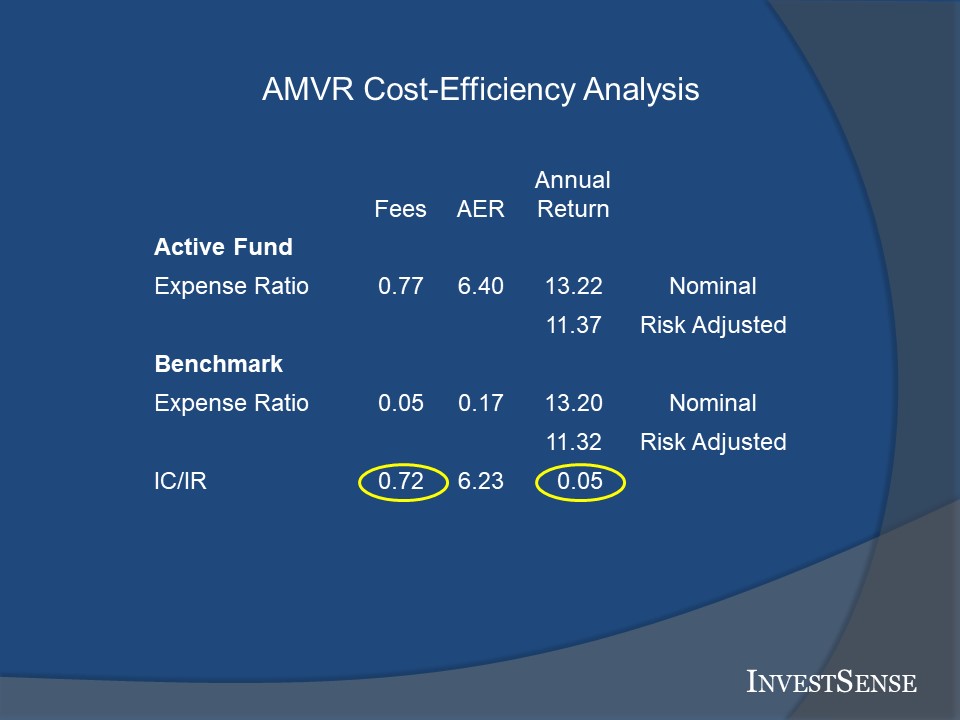

The chart below shows the results of an AMVR forensic analysis of the annualized compound return of Fidelity Contrafund’s retirement/K shares, FCNKX, using the Vanguard Large Cap Growth Index fund retirement shares (VIGAX) as the benchmark. Once again, FCNKX fails to provide a positive incremental return, indicating that it is not cost-efficient relative to VIGAX, and (2) the dramatic increase in FCNKX’s expense ratio, from, 0.77 to 6.40, when the fund’s r-squared/correlation of returns number, 98, is factored into the equation.

Going Forward

Facts do not cease to exist because they are ignored – Aldous Huxley

As noted earlier, financial advisers, plan sponsors, and the financial services industry in general like to talk about returns, but not about correlation of returns and/or cost-efficiency. The evidence presented in this post demonstrates why this is so, as well as why the financial services adamantly opposes any suggestion of a true fiducairy standard and increased transparency in connection with their products.

However, the plaintiff’s bar is going to continue to press plan sponsors, plan advisers, and financial adviser on these issues since, realistically, these parties essentially have no valid defense to challenges based on cost-inefficiency issues, especially when confronted with simple and straightforward AMVR analyses.

As I tell plan sponsors and investment fiduciaries, the best defense is to be proactive in analyzing, selecting, and monitoring the investment options within your plan or investment account portfolios. With the increase in reliance on pre-packaged model portfolios by plan sponsors, plan advisers and other investment fiduciaries, that advice becomes even more valuable.

I always give my consulting clients the following advice based on the Oracle of Omaha’s well-known adage:

Rule No. 1 – With regard to actively managed mutual funds, only invest in funds that provide a commensurate return for the additional costs and risks an investor in such finds is asked to assume. (Restatement (Third) of Trusts, Section 90, cmt. h(2)

Rule No. 2 – Calculate such additional cost and risks based upon a fund’s incremental risk-adjusted returns and incremental correlation-adjusted costs. (Ellis, Sharpe, and Miller)

Rule No. 3 – Never forget Rules No. 1 and No. 2.

Very few actively managed mutual funds will ever pass this test using the “humble arithmetic” of the AMVR, simply because most actively managed funds are not cost-efficient. As a result, investors and plan participants will be directed back toward the relative safety and financial security of index funds, and investment fiduciaries will avoid unnecessary and unwanted fiduciary liability exposure.

Copyright InvestSense, LLC 2020, 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

I thoroughly enjoy reading a well-reasoned legal brief or decision. For instance, the Enron1 decision, while lengthy, is an excellent treatise on ERISA. The First Circuit’s decision in Brotherston v. Putnam Investments, LLC2 is one of the best decisions I have ever read from a technical perspective.

The amicus brief filed by the Solicitor General (SG) in Hughes v. Northwestern University3 (Northwestern) is both well-written and well-reasoned. The Northwestern case is a highly anticipated case, as SCOTUS’s decision will change the entire landscape of the 401(k) industry, regardless of what SCOTUS ultimately decides

Anyone who has taken the time to read the amicus brief filed the Solicitor General (SG) in the Northwestern case know that the SG relied heavily on the Restatement (Third) of Trusts (Restatement), which states the common law of trusts. Some people have asked me why the SG did so. My answer:

“We have often noted that an ERISA fiduciary’s duty is ‘derived from the common law of trusts.’ In determining the contours of an ERISA fiduciary’s duty, courts often must look to the law of trusts”.4

ERISA is essentially the codification of the common law of trusts.

The Restatement (Third) of Trusts (Restatement) is a restatement of the common law of trusts.

Whether participants in a defined-contribution ERISA plan stated a plausible claim for relief against plan fiduciaries for breach of the duty of prudence by alleging that the fiduciaries caused the participants to pay investment-management or administrative fees higher than those available for other materially identical investment products or services.5

That is the question before SCOTUS in the Northwestern case. In reading the amicus brief, a couple of the SG’s comments particularly stood out to me, as they may offer an insight into key factors in SCOTUS’s decision. The actual question presented to SCOTUS for consideration is simple and direct.

So, the question before the Court involves what level of pleading is required in order for the plan participant’s case to survive a defendant’s motion to dismiss. This is a crucial question, as once a case survives a motion to dismiss, the case goes forward and the plaintiff is entitled to discovery, the ability to requests documents and other evidence from the defendants. Defendants desperately want to avoid discovery, as it may reveal unfavorable evidence against them and result in expensive settlements or decisions.

Civil Litigation and the “Notice” Pleading Requirement In civil litigation, the plaintiff is generally only required to provide “notice” pleading, sufficient information to inform the defendant of the general nature of the plaintiff’s claims. In many 401(k) cases, the defendants have argued that the plan participants needed to provide more specific information about their claims.

Unfortunately, in some cases the courts agreed and, in my opinion, prematurely dismissed the action. In other cases, the court granted the plan participants an opportunity to amend their complaints to provide such information.

However, the inequity in even requiring such specifics, in effect, to prove their case in its initial pleading without the benefit of discovery, was noted by the First Circuit’s in its decision in Brotherston, where the court stated that

More importantly, the Supreme Court has made clear that whatever the overall balance the common law might have struck between the protection of beneficiaries and the protection of fiduciaries, ERISA’s adoption reflected ‘Congress'[s] desire to offer employees enhanced protection for their benefits.’

In other words, Congress sought to offer beneficiaries, not fiduciaries, more protection than they had at common law, albeit while still paying heed to the counterproductive effects of complexity and litigation risk.

In short, when interpreting the application of ERISA in the absence of statutory guidance, the Supreme Court has usually opted for the common law approach except when rejection was necessary to provide enhanced beneficiary protections.6

That exception recognizes that the burden may be allocated to the defendant when he possesses more knowledge relevant to the element at issue. Schaffer, 546 U.S. at 60, 126 S.Ct. 528. Trust law has long embodied similar logic. See Restatement (Third) of Trusts, § 100 cmt. f (noting that the general rule placing on the plaintiff the burden of proving his claim “is moderated in order to take account of . . . the trustee’s superior (often, unique) access to information about the trust and its activities”

An ERISA fiduciary often — as in this case — has available many options from which to build a portfolio of investments available to beneficiaries. In such circumstances, it makes little sense to have the plaintiff hazard a guess as to what the fiduciary would have done had it not breached its duty in selecting investment vehicles, only to be told “guess again.” It makes much more sense for the fiduciary to say what it claims it would have done and for the plaintiff to then respond to that.7

Now the issue in Brotherston was who carried the burden of proof regarding causation, not pleading per se. The SG’s amicus brief ultimately argued in favor of placing the burden of proof on plans given the superiority of knowledge argument. However, the quotations are included here because many in the legal profession view Brotherston and Northwestern as companion cases for purposes of 401(k) litigation.

The Seventh Circuit Court of Appeals handed down the Northwestern decision currently under review by SCOTUS. One of the key issues before the Seventh Circuit was whether a plan sponsor was insulated from fiduciary liability if a plan included investment options that included both prudent and imprudent investments. In denying the plan participants’ appeal, the Seventh Circuit stated that

[P]lans participants had options to keep the expense ratios (and, therefore, recordkeeping expenses) low (by choosing to) invest in various low-cost index funds….[P]lans may generally offer a wide range of investment options and fees without breaching any fiduciary duty.8

Compare that with the following statement from the Seventh Circuit in an earlier case. Hecker v. Deere & Co., or more commonly known as “Hecker II.”9 In Hecker I, the Seventh Circuit decided the case based largely on statements similar to the ones just referenced. The uproar was immediate, causing the Seventh Circuit to issue a “clarification” of its earlier statements.

The Secretary also fears that our opinion could be read as a sweeping statement that any Plan fiduciary can insulate itself from liability by the simple expedient of including a very large number of investment alternatives in its portfolio and then shifting to the participants the responsibility for choosing among them. She is right to criticize such a strategy. It could result in the inclusion of many investment alternatives that a responsible fiduciary should exclude. It also would place an unreasonable burden on unsophisticated plan participants who do not have the resources to pre-screen investment alternatives. The panel’s opinion, however, was not intended to give a green light to such “obvious, even reckless, imprudence in the selection of investments”10

Many legal experts construed the court’s “clarification” as, in fact, a “reversal.” And yet, now SCOTUS is about to review a Seventh Circuit decision arguing the same faulty logic, logic which is clearly inconsistent with ERISA Section 404(a), which requires that the investment options within a plan be prudent, both individually and collectively. Equally disturbing is that the Seventh Circuit’s position is inconsistent with that of the majority of other federal appellate courts.

The Solicitor General effectively discredited the Seventh Circuit’s argument, commonly referred to as the “menu of options” argument, including numerous references to sections of the Restatement and common law.

The court’s reasoning was unsound. Under the law of trusts, which informs ERISA’s fiduciary standards, fiduciaries are not excused from their obligations not to offer imprudent investments with unreasonably high fees on the ground that they offered other prudent investments. See, e.g., Davis, 960 F.3d at 484 (“It is no defense to simply offer a ‘reasonable array’ of options that includes some good ones, and then ‘shift’ the responsibility to plan participants to find them.”) And the Court made clear that this duty applies to each of the trust’s investments….

The judgment and diligence required of a fiduciary in deciding to offer any particular investment fund must include consideration of costs, among other factors, because a trustee must “incur only costs that are reasonable in amount and appropriate to the investment responsibilities of the trusteeship.” Restatement (Third) of Trusts § 90(c)(3), at 293 (2007) (Third Restatement); see id. § 90 cmt. b, at 295 (“[C]ost-conscious management is fundamental to prudence in the investment function.”). “Trustees, like other prudent investors, prefer (and, as fiduciaries, ordinarily have a duty to seek) the lowest level of risk and cost for a particular level of expected return.” Id. § 90 cmt. f(1), at 308. For mutual funds specifically, trustees should pay “special attention” to “sales charges, compensation, and other costs” and should “make careful overall cost comparisons, particularly among similar products of a specific type being considered for a trust portfolio.” Id. § 90 cmt. m, at 33211

In short, “[w]asting beneficiaries’ money is imprudent.” Tibble v. Edison Int’l, 843 F.3d 1187, 1198 (9th Cir. 2016) (en banc)12

The Solicitor General’s Analysis of ERISA’s Pleading Standards

Petitioners’ Amended Complaint states at least two plausible claims for breach of ERISA’s duty of prudence, and the court of appeals’ decision reaching the opposite conclusion is incorrect in certain important respects. Taking petitioners’ factual allegations as true at the pleading stage, petitioners have shown that respondents caused the Plans’ participants to pay excess investment-management and administrative fees when respondents could have obtained the same investment opportunities or services at a lower cost.(emphasis added)13

If petitioners succeed in proving those allegations, then respondents breached ERISA’s duty of prudence by offering higher-cost investments to the Plans’ participants when respondents could have offered the same investment opportunities at a lower cost. (emphasis added)14

In Northwestern, the plan participants argued that there were lower cost institutional shares available. I would suggest that in cases where institutional shares are not available, the same argument could be made for using comparable, lower-cost index funds.

In language that I believe we may see incorporated into SCOTUS’ eventual decision, the SG stated that

Considering those allegations together and taking them as true at the pleading stage, the Amended Complaint plausibly states a claim that respondents acted imprudently….15

Petitioners did not merely present a conclusory assertion that the Plans’ recordkeeping fees were too high; they substantiated their claim with specific factual allegations about market conditions, prevailing practices, and strategies used by fiduciaries of comparable Section 403(b) plans.16

Last, the court of appeals stated that “plan participants had options to keep the expense ratios (and, therefore, recordkeeping expenses) low.” But that simply repeats the same error discussed above by wrongly suggesting that fiduciaries can avoid liability for offering imprudent investments with unreasonably high fees by also offering prudent investments with reasonable fee”17

“Taking petitioners’ factual allegations as true at the pleading stage” and “plausible claims.” Remember those two terms. The first states a basic rule of law in considering a motion to dismiss given the draconian nature of the motion itself, denying a plaintiff their day in court and the opportunity for discovery.

The second emphasizes the need to support a claim of fiduciary breach with some factual evidence of the harmful nature of the plan sponsors actions or failure to act. I have been advising some plaintiff’s attorneys that a simple way of satisfying that requirement would be to argue the cost-inefficiency of the actual investment options chosen.

A simple metric I created, the Active Management Value Ratio™4.0 (AMVR), allows investors and attorneys to quickly evaluate the cost-efficiency of an actively managed fund using low-cost index funds as benchmarks. While plan sponsors and the investment industry claim that using index funds as benchmarks is inappropriate, comparing “apples and oranges,” the First Circuit effectively discredited that argument in its Brotherston decision, referencing the Restatement and common law.

So to determine whether there was a loss, it is reasonable to compare the actual returns on that portfolio to the returns that would have been generated by a portfolio of benchmark funds or indexes comparable but for the fact that they do not claim to be able to pick winners and losers, or charge for doing so. Restatement (Third) of Trusts, § 100 cmt. b(1) (loss determinations can be based on returns of suitable index mutual funds or market indexes);

Going Forward

[I]f petitioners’ complaint had been filed in the Third or Eighth Circuit, [their complaint] would have survived respondents’ motion to dismiss.”18

That is the crux of the Northwestern case and why SCOTUS needed to hear the case. The rights and protections guaranteed to employees under ERISA are simply too important to be determined by the legal jurisdiction in which they reside. SCOTUS must establish one uniform standard applicable to all federal courts, both the U.S. Courts of Appeal and the lower federal courts.

I would also argue that the combination of the Northwestern and Brotherston decisions effectively discredit both the “apples and oranges” and the “menu of options” arguments that plan sponsors and others in the 401(k) industry have relied upon to convince courts to dismiss 401(k) actions.

While the SG’s Northwestern amicus brief cited the Restatement in support of its arguments, it failed to cite Section 90, comment h(2).19 The comment essentially states that before recommending or using a strategy that utilizes actively managed mutual funds, it must be objectively determined that the fund/strategy would provide an investor with a level of return commensurate for the additional cost and risk typically associated with such investments.

Research has consistently shown that very few actively managed mutual funds are cost-efficient. The AMVR metric provides a quick and simple means of determining cost-efficiency.

Regardless of what SCOTUS decides, the landscape of the 401(k) industry will be changed forever.

Notes 1. In Re Enron Corp. Securities, Derivatives and ERISA, 238 F.Supp.3d 799 (2017). 2. Brotherston v. Putnam Investments, LLC,, 907 F.3d 17, 39 (1st Cir. 2018). 3.. https://www.scotusblog.com/case-files/cases/hughes-v-northwestern-university/. 4. Tibble v. Edison Int’l, 843 F.3d 1187, 1198 (9th Cir. 2016) (en banc). 5. https://www.scotusblog.com/case-files/cases/hughes-v-northwestern-university/. 6. Amicus Brief of the Solicitor General (AB), 37 7. AB, 38. 8. Hughes v. Northwestern University, 953 F.3d 980 (2020). 9. Hecker v. Deere & Co., 569 F.3d 708 (2009) (Hecker II). 10. Hecker II, 711. 11. AB, 11-12. 12. AB, 13. 13. AB, 8. 14. AB, 9. 15. AB, 14. 16. AB, 14-15. 17. AB, 16. 18. AB, 20. 19. Restatement (Third) Trusts, Section 90, cmt. h(2). American Law Institute. All rights reserved.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

Right now, the DOL and the SEC are trying to define “prudence” and “best interest,” respectively. I am on record as saying that the simplest and most logical step would be one, universal standard of prudence, using the Investment Advisor’s Act of 1940 as the model.

Since I do not expect the warring factions to agree on something so simple and logical, I continue to advocate my metric, the Active Management Value Ratio™ 4.0 (AMVR), as a simple, yet powerful, way to evaluate the prudence of an actively managed mutual fund.

While some would argue that fiduciary prudence can be evaluated on an investment’s returns alone, the fiduciary standards set out in the Restatement (Third) of Trusts. (Restatement) “Prudent Investor Rule” would disagree. Section 90 of the Restatement, more commonly known as the “Prudent Investor Rule,” emphasizes the importance of cost-efficiency as a factor in the prudence of fiduciary investments. Bottom line – alpha without cost-efficiency is meaningless.

Comments b, f, h(2) and m of Section 90 are notable on this issue, particularly comment h(2). Comment h(2) states that a fiduciary should not recommended or select an actively managed fund unless it can fairly and objectively be expected that the active fund will provide a commensurate return for the additional costs and risks associated with such fund. Research has consistently shown that the overwhelming majority of actively managed funds are not, however, cost-efficient.

The AMVR evaluates the cost-efficiency of an actively managed fund relative to a comparable benchmark index fund. The AMVR is based primarily on the research and concepts of investment icon, Charles D. Ellis, who stated that

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!1

When people ask me about the AMVR, I tell them that the AMVR addresses the basic question every investor should ask about an actively managed mutual fund:

Does the actively managed fund provide a commensurate return for the additional costs and risks an investor is asked to assume?

To answer that question, an investor and/or investment fiduciary simply has to answer two simple questions:

Does the actively managed fund provide a positive incremental return relative to a comparable index fund?

If so, does the actively managed fund’s positive incremental return exceed the actively managed fund’s incremental costs?

If the answer to either of these questions is “no,” then the actively managed fund is not a prudent investment choice relative to the benchmark index fund.

An investor and/or investment fiduciary will have to pose those two questions in one of three scenarios. In the first scenario, the actively managed fund fails to produce a positive incremental return, i.e., has underperformed the benchmark index fund.

This is obviously an easy example of cost-inefficiency, as an investor in the actively managed fund would receive no commensurate return for the additional costs, let alone for any additional risk from the active fund.

In the second example, the actively managed fund does provide a positive incremental return. however the active fund’s positive incremental return is exceeded by the fund’s incremental costs. Once again, the active fund fails to provide a commensurate return relative to the benchmark index fund. The “New” Fiduciary Prudence Equation AMVR 4.0 introduces a new factor into the prudence debate, correlation of returns. The AMVR uses Ross Miller’s Active Expense Ratio (AER) in calculating an active fund’s correlation-adjusted expense rati

So why calculate an actively managed fund’s correlation-adjusted expense ratio? As Miller explains,

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funs engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.2

Martijn Cremers, creator of the Active Share metric, goes further, stating that actively managed mutual funds are arguably guilty of investment fraud.

[A] large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by for fees for active management that they do not receive or receive only partially….

Closet indexing raises important legal issues. Such funds are not just poor investments; they promise investors a service that they fail to provide. As such, some closet index funds may also run afoul of federal securities laws.3

At the end of each calendar quarter, I publish my AMVR “cheat sheet” on the non-index funds in “Pensions & Investments” annual list of the top mutual funds used in defined contribution plans, based on the amount of invested assets. The slide below shows the results for the 2Q 2021.

Using only an active fund’s incremental costs and its R-squared/correlation number, Miller’s research found that actively managed funds that combine high R-squared scores with high incremental costs often have implicit expense ratios that are 400-600 percent higher, in some cases even higher, than their publicly stated expense ratios. The AMVR forensic analysis slide below, involving a fund with an R-squared score of 97, provides an example of how correlation of returns can impact an active fund’s implicit cost-efficiency.

While some dismiss the importance of an active fund’s correlation of returns number, common sense indicates otherwise. For example, the active fund in this example had an R-squared/correlation number of 97. This suggests that an investor in the index fund could achieved 97 percent of the return of the active fund for less than 10 percent of the active fund’s cost, the essence of cost-efficiency.

At the same time, the high R-squared/correlation number indicates that either the active did not actually provide much active management or the active management provided was not very effective. Either way, the results support Cremers accusations.

Calculating AMVR Calculating an actively managed fund’s AMVR score is simple and straightforward, similar to the calculation process for the Sharpe Ratio. Whereas the Sharpe ratio divides return by standard deviation, the AMVR divides an actively managed funds incremental risk-adjusted return (RAR) by the fund’s incremental correlation-adjusted costs, i.e., the fund’s AER number.

The reasoning behind using correlation-adjusted costs has already been discussed. Ellis himself suggested using risk-adjusted returns because, the argument goes, an investment’s return is supposed to be a function of the risk assumed by an investor.

An active fund that fails to provide any positive incremental return automatically earns an AMVR score of zero. Otherwise, as mentioned earlier, an actively managed fund’s AMVR score is calculated by dividing the fund’s incremental risk-adjusted return by the fund’s incremental correlation adjusted costs. The higher a fund’s AMVR score, the greater the fiduciary prudence/cost-efficiency of the actively managed fund.

In our example, the active fund’s incremental correlation-adjusted costs greatly exceed the fund’s incremental risk-adjusted returns, earning the active fund an AMVR score of zero. Therefore, the actively managed fund would be deemed to be an imprudent investment choice relative to the benchmark index fund.

Going Forward Some ERISA plaintiff’s attorneys have already implemented the AMVR and AER metrics into their practices in calculating damages. Investment fiduciaries should consider the potential impact of the combination of the AMVR and AER metrics on their potentisl liability exposure, especially given the fact that SCOTUS could very easily impose the burden of proof regarding causation/fiduciary prudence on plan sponsors in 401(k)/403(b) litigation as a result of the Northwestern University 403(b) case currently pending before the Court.

Plan sponsors should perhaps heed the warning issued by John Langbein, who served as the reporter for the commission that drafted the revised Restatement (Third) over forty years ago:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.4

Or, as the First Circuit Court of Appeals recently commented,

Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”5

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

People that know me know how much I respect Charley Ellis. His classic, “Winning the Loser’s Game, ” changed my whole perspective on investing. My popular metric, the Active Management Value Ratio, is based primarily on WLG.

Robin Powell has championed the movement behind evidence-based investing. His recent Interview with Charley is available on Robin’s terrific blog, “The Evidence Based Investor.” Do yourself a favor and read the interview and improve your financial security .

At that point, many people, both investment professionals and ordinary investors, stop their AMVR analysis of the actively managed fund in question, unnecessarily exposing themselves to potential financial losses and/or legal liability. When InvestSense provides pension plans and attorneys with consulting services and forensic audits, we re-calculate a fund’s incremental returns using risk-adjusted returns and the fund’s incremental costs using the Active Expense Ratio (AER) metric.

Many people are unfamiliar with the AER. Created by Ross Miller, the AER factors in the implicit impact of a fund’s correlation of returns to the benchmark used in the AMVR analysis. The importance of this step in an AMVR analysis is that the higher the active fund’s correlation of returns to the applicable benchmark, the less contribution that the actively managed fund’s management is actually providing to the active fund’s overall performance. As Professor Miller explained,

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funs engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.1

The AER also helps identify and avoid so-called “closet index” funds. Closet index funds are, by definition, cost-inefficient, charging excessive fees for underperformance. As one noted expert explained,

a large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by for fees for active management that they do not receive or receive only partially. .

Closet indexing raises important legal issues. Such funds are not just poor investments; they promise investors a service that they fail to provide. As such, some closet index funds may also run afoul of federal securities laws.3

Over the last decade or so, there has been a definite trend of extremely high correlation of returns between U.S. domestic equity funds and comparable index funds. Professor Miller’s study found that the AER number for most U.S. domestic equity funds was often 400-500 percent higher than the fund’s publicly stated expense ratio, sometimes even higher.

Today, it is not uncommon to find that most U.S. domestic equity funds have high R-squared, or correlation, numbers of 90 percent of more. The higher a fund’s R-squared number and its incremental costs, the higher the fund’s AER number will be.

Charles D. Ellis, one of America’s most respected investment experts, stressed the importance of an actively managed fund’s correlations of returns numbers by pointing that on a fund that has an R-squared number of 95, that leaves the remaining 5 percent of the fund’s return having to try to justify the fund’s incremental costs. The odds of that happening are extremely unlikely, especially on a consistent basis, given the high correlation between the funds.

Active Management Value RatioTM 4.0

Active Management Value RatioTM (AMVR) 4.0 differs from AMVR 3.0 in the methodology used to calculate AMVR. In AMVR 3.0, we divided incremental cost by incremental return. Several legal colleagues and retired judges suggested that I “flip” the calculation to make it more similar to the Sharpe Ratio and, hopefully, make it easier to gain greater admissibility in the courts.

The main purpose of the AMVR is to establish whether a certain actively managed mutual fund is cost-efficient or not relative to a comparable, less expensive index fund. By establishing the cost-inefficiency of an actively managed mutual fund, the plaintiffs’ ERISA attorney creates a “material issue of fact,” which should prevent the court from dismissing the plan participants’ case.

Courts decide issues of law; juries decide questions of fact. While most 401(k)/403(b) actions are bench trials, I believe that may change in the near future, in part because of AMVR slides like the one shown here. I believe the AMVR would help juries answer the fundamental question- are an actively managed fund’s incremental costs greater than incremental returns?

When people ask me about the AMVR, I tell them that the AMVR addresses the basic question every investor should ask about an actively managed mutual fund:

Does the actively managed fund provide a commensurate return for the additional costs and risks an investor is asked to assume?

This come directly from the the “Prudent Investor Rule,” Section 90 of the Restatement (Third) of Trusts, comment h(2).

So what story does this AMVR “cheat sheet” slide tell us? This slide presents information on the six non-index funds from the top ten mutual funds used in U.S. defined contribution plan, based on invested assets, from “Pensions & Investments” annual survey. FIrst of all, the high R-squared correlation numbers should alert us to the possibility of “closet index” funds.

Next, 5 out of the 6 funds fail to provide a positive incremental return relative to a comparable Vanguard index fund based on nominal returns. Nominal returns are the simple return numbers you see on online services such as Morningstar. A fund obviously does not provide a commensurate return when it underperforms the benchmark fund.

To be cost-efficient, a fund’s AMVR has to be positive and greater than 1.00, showing that a fund’s nominal incremental returns are greater than the fund’s incremental costs. Here, Dodge and Cox Funds’s nominal AMVR score would be 8.93 (4.20./0.47).

However, ERISA plaintiff attorneys and others would argue that the use of nominal return numbers does not present an accurate picture of the situation. Many argue that investment performance figures are misleading unless they are adjusted for both risk and correlation of returns.

Here we see that adjusting for risk, using standard deviations, two funds produce positive annualized return, Dodge & Cox Stock Fund (2.69) and T. Rowe Price Blue Chip Growth (0.14). Those numbers are expressed in terms of basis points (bps). A basis point is one one-hundredth (0.01) of one percent. One hundred basis points equals one percent.

In our example Dodge and Cox had a higher standard deviation (19.14%) than the benchmark fund, Vanguard’s Large Cap Index Fund (VIGAX) (16.24). That explains Dodge & Cox Stock Fund’s lower risk-adjusted incremental return number.

The incremental costs numbers are calculated using the Active Expense Ratio (AER) mentioned earlier. The AER estimates a fund’s active weight/contribution, then determines the active’s fund’s inferred effective expense ratio. In essence, it indicates whether a fund’s incremental returns justify the fund’s incremental costs and, if not, the inferred additional costs.

High incremental costs combined with a high correlation of returns number significantly increase a fund’s AER number. Here, the combination of a high correlation number (97) combined with a moderately high incremental costs number (47 bps) resulted in an AER of 3.00, as compared to its nominal, or stated, expense ratio of 52 bps

As a result, Dodge & Cox Fund’s AMVR of 0.89 would technically classify it as cost-inefficient since its AMVR is less than 1.00. An investor should look for other options that provide a higher AMVR score.

As for the T. Rowe Price Blue Chip Growth Fund, the small positive risk-adjusted incremental return was completely overwhelmed by the fund’s high AER, the result of the combination of its high incremental costs (1.16 percent, or 116 bps) and high correlation of returns (98), resulting in an AER of 9..23. The fund’s AMVR would be its risk-adjusted incremental return (0.14) divided by its correlation-adjusted costs (9.23), 0.01, well-below the 1.00 required for cost-efficient status.

Going Forward To borrow from the Oracle of Omaha:

Rule No. 1 – With regard to actively managed mutual funds, only invest in funds that provide a commensurate return for the additional costs and risks an investor in such finds is asked to assume.

Rule No. 2 – Calculate such additional cost and risks based upon a fund’s risk-adjusted returns and correlation-adjusted costs.

Rule No. 3 – Never forget Rules No. 1 and No. 2.

Very few actively managed mutual funds will ever pass this test using the “humble arithmetic” of the AMVR, simply because most actively managed funds are not cost-efficient. As a result, investors and plan participants will be directed back toward the relative safety and financial security of index funds, and investment fiduciaries will avoid unnecessary and unwanted fiduciary liability exposure.

Notes 1. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-4. 2. Martijn Cremers and Quinn Curtis, Do Mutual Fund Investors Get What they Pay For?:The Legal Consequences of Closet Index Funds, https://papers.ssrn.com/sol/papers.cfm?abstract_id=2695133.

This article is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

The very essence of leadership is that you have to have a vision. You can’t blow an uncertain trumpet. – Father Theodore Hesburgh, University of Notre Dame

Over twenty years ago, I registered the domain name “investsense.com.” Since then, I have advocated what my concept of the term means and the potential benefits that can be derived by practicing investsense.

InvestSense – the art and science of combining sound, proven investment techniques and strategies with simple, common sense,

My vision is equally simple:

Plaintiff ERISA attorneys who incorporate CommonSense InvestSense principles into their practices should never lose a 401(k)/403(b) fiduciary breach case.

401(k) and 403(b) plan sponsors who properly incorporate CommonSense InvestSense principles into the plan’s investment selection process should never lose an action alleging a breach of their fiduciary duties.

Now, I cannot guarantee those outcomes because, as we have seen, the courts have made some “interesting” decisions based on arguments that seem contrary to both ERISA’s stated purpose and the common law of trusts, from which fiduciary law is largely derived. As I write this post, SCOTUS is considering whether to rectify some questionable rulings involving a plan sponsor’s burden of proof in 401(k)/403(b) litigation

The basic rule of pleading is that the plaintiff is only required to provide the defendant with sufficient information to put the defendant “on notice” of what the plaintiff’s general allegations, or “notice pleading.” The reason for this rule is that the specific information involved in the alleged wrongdoing is, in most cases, exclusively within the possession of the defendant in the early stages of litigation and until the plaintiff has had the opportunity to conduct discovery. Therefore, it would be, and is, inherently inequitable to require greater specificity in the plaintiff’s initial pleadings.

Yet, some courts have done just that, dismissing 401(k) and 403(b) fiduciary breach actions based not on the merits of the case, but rather on concepts such as “comparing apples and oranges” and “menu of options.” The arguments against such questionable standards is that not only are they inconsistent with ERISA’s provisions, but they also ignore ERISA’s stated purpose, the protection of pension plan participants. Too often, recent ERISA court decisions have seemed to go out of their way to protect plans at the expense of the plan’s participans.

In two separate cases, Putnam Investments, LLC v. Brotherston and now Hughes v. Northwestern University, the Solicitor General has submitted an amicus brief to SCOTUS arguing that the burden of proof on the issue of causation, i.e., whether the plan sponsor was prudent in the selection of the plan’s investment options, should fall on the plan sponsor once the plan participants have provided sufficient notice pleading. The Solicitor Generals have pointed out that such a duty would be consistent with both the common law of trusts and rulings of other U. S. appellate courts.

SCOTUS has not indicated whether it will hear the Northwestern case. With the term of the current term almost over, it appears that the earliest the Court would consider the case will be the next term, which begins in October.

In the meantime, plan sponsors and plaintiff ERISA attorneys should consider the potential benefits of incorporating CommonSense InvestSense principles, as they would apply regardless of the outcome in the Northwestern case. The basic foundation for the InvestSense concept is the studies of investment icons Nobel laureate Dr. William D. Sharpe, Charles D. Ellis and Burton Malkiel.

Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs….The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.”1

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!2

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.3

This emphasis on cost consciousness and the cost-efficiency of investments is consistent with the fiduciary principles set out in the Restatement (Third) of Trusts. The importance of costs and cost-efficiency is also a core concept in the SEC’s new Regulation Best Interest (Reg BI). In discussing Reg BI’s provisions regarding costs as a factor in recommending investments, former SEC Chairman Jay Clayton stated that

A rational investor seeks out investment strategies that are efficient in the sense that they provide the investor with the highest possible expected net benefit, in light of the investor’s investment objective that maximizes utility.4

[A]n efficient investment strategy may depend on the investor’s utility from consumption, including…(4) the cost to the investor of implementing the strategy.5

One comment was particularly interesting with regard to its applicability to the concept of InvestSense.

[W]hen a broker-dealer recommends a more expensive security or investment strategy over another reasonably available alternative offered by the broker-dealer, the broker-dealer would need to have a reasonable basis to believe that the higher cost is justified (and thus nevertheless in the retail customer’s best interest) based on other factors….6

So cost matter. John Bogle said it. Ellis, Sharpe and Malkiel said it. And now former SEC Chairman Clayton is on record as saying it. I cannot wait to hear how plan sponsors are going to argue that cost-inefficient investment options are justified/prudent. So how does that translate into 401(k)/403(b) litigation and the potential benefits to ERISA plaintiff attorneys and plan sponsors of incorporating the core principles of InvestSense into their worlds?

A couple of years ago I created a metric, the Active Management Value RatioTM (AMVR), that allows investors, fiduciaries and attorneys to simply and quickly determine the cost-efficiency, and thus prudence, of actively managed mutual funds. Additional information about the AMVR is available on this blog, or click here.

Again, if SCOTUS does rule that plan sponsors have the burden of proof on the issue of causation, then plan sponsors will face the same cost-efficiency issues addressed by Clayton, the need to show a reasonable basis for the selection of higher cost investment options for their plan. That may prove to be a formidable task, given that studied have consistently shown that the overwhelming majority of actively managed funds are cost-inefficient relative to comparable passive, or index funds.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.7

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.8

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.9

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.10

These findings have resulted in recommendations that investment fiduciaries such as plan sponsors seriously consider selecting index funds instead of actively managed mutual funds. John Langbein, who served as the Reporter for the committee that wrote the Restatement (Thrid) of Trusts offered the following advice:

When market index funds have become available in sufficient variety and their experience bears out their prospects, courts may one day conclude that it is imprudent for trustees to fail to use such accounts. Their advantages seem decisive: at any given risk/return level, diversification is maximized and investment costs minimized. A trustee who declines to procure such advantage for the beneficiaries of his trust may in the future find his conduct difficult to justify.11

And the First Circuit Court of Appeals took the unusual step of offering the following advice to those who might object to its Brotherston decision:

In so ruling, we stress that nothing in our opinion places on ERISA fiduciaries any burdens or risks not faced routinely by financial fiduciaries. While Putnam warns of putative ERISA plans forgone for fear of litigation risk, it points to no evidence that employers in, for example, the Fourth, Fifth, and Eighth Circuits, are less likely to adopt ERISA plans. Moreover, any fiduciary of a plan such as the Plan in this case can easily insulate itself by selecting well-established, low-fee and diversified market index funds. And any fiduciary that decides it can find funds that beat the market will be immune to liability unless a district court finds it imprudent in its method of selecting such funds, and finds that a loss occurred as a result. In short, these are not matters concerning which ERISA fiduciaries need cry “wolf.”12

For my part, I offer the following AMVR fiduciary analysis comparing a very common investment option in 401(k) and 403(b) plans, the Fidelity Contrafund Fund (FCNKX), to the Fidelity Large Cap Growth Index Fund (FSPGX). As the slide clearly shows, Contrafund is cost-inefficient, and thus imprudent, relative to Fidelity’s own large cap growth index fund.

This is not to slight Contrafund’s legendary manager, Will Danoff. Working against Contrafund is its high expense ratio (77 basis points) and high R-squared correlation number (97) relative to the large cap growth index fund. The disparity is even more alarming if the analysis is done using Ross Miller’s Active Expense Ratio, which factors a fund’s R-squared correlation number even more heavily.

Trust me, there are plenty of other examples documenting the cost-inefficiency of popular 401(k)/403(b) actively managed mutual funds. The fact is that “true” actively managed mutual funds will always have higher expense ratios (Ellis) and higher trading costs (Malkiel).

Advocates of actively managed funds often argue that active management can offset such higher costs with better performance. Theoretically, yes. However, remember the quotes from the earlier studies. History does not support that optimism.

Furthermore, Contrafund’s high R-squared correlation number (97), is reflective of a definite trend of more than a decade of U.S. domestic equity funds having correlation numbers of 90 and above, many higher than 95, relative to comparable index funds. Bottom line-odds of a fiduciary breach being found are extremely high when actively managed funds are compared to comparable index funds.

Going Forward At the beginning of this post, I set out two of my visions about CommonSense InvestSense

ERISA plaintiff attorneys who incorporate CommonSense InvestSense principles into their practice should never lose a 401(k)/403(b) fiduciary breach action.

410(k) and 403(b) plan sponsors who properly incorporate CommonSense InvestSense principles into the plan’s investment selection process should never lose an action alleging a breach of their fiduciary duties

As I have explained the importance of the Northwestern case and the potential ramifications of a SCOTUS decision to plan sponsors, I usually get a question as to why there are no potential adverse implications from the case for plan advisers since, in most cases, the plan sponsors were simply following the plan adviser’s recommendations and advice. There

There are definitely potential adverse implications for plan advisers as a result of a SCOTUS decision in the Northwestern case. However, those implications will most likely be determined by plan sponsors reaction to the Court’s decision rather than as a result of the decision itself.

Notes 1. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm. 2. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online athttps://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c 3. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460. 4. “Regulation Best Interest: The Broker-Dealer Standard of Conduct,” Release No. 34-86031; File No. S7-07-18, https://www.sec.gov/rules/final/2019/34-86031.pdf, 378 5. Ibid., 378 6. Ibid., 279 7. . Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 8.. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 9. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 10. Mark Carhart, On Persistence in Mutual Fund Performance, Journal of Finance, Vol. 52, No. 1, 57-8 (1997). 11. Brotherston v. Putnam Investments, LLC,, 907 F.3d 17, 39 (1st Cir. 2018) 12. John H. Langbein and Richard A. Posner, Measuring the True Cost of Active Management by Mutual Funds, Journal of Investment Management, Vol 5, No. 1, First Quarter 2007 http://digitalcommons.law.yale.edu/fss_papers/498.

This article is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.implications

“Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs….The best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.”1

Ask a plan sponsor, trustee or other investment fiduciary about their investment selection process, and they will probably quote you annualized return, nothing more, because they do not bother to properly select and monitor investments. Probably because in too many cases they do not know how to properly select and monitor investments.

This may seem harsh, but the evidence supports my theory. Take Dr. Sharpe’s quote for example. How many fiduciary investors bother to compare potential actively managed fund choices with a comparable index fund? How many fiduciary investors simply blindly follow whatever advice their adviser recommends, again because they do not know to properly evaluate the funds themselves?

SCOTUS has recognized the legitimacy of the Restatement of Trusts as a resource in addressing fiduciary questions. Section 90 of the Restatement, commonly known as the Prudent Investor Rule, stresses two consistent themes, cost-efficiency and risk-management through diversification. With regard to cost-efficiency, the Restatement states that

Active strategies, however, entail investigation and analysis expenses and tend to increase general transaction costs,…If the extra costs and risks of an investment program are substantial, those added costs and risks must be justified by realistically evaluated return expectations. Accordingly, a decision to proceed with such a program involves judgments by the [fiduciary] that: (a) gains from the course of action in question can reasonably be expected to compensate for its additional costs and risks;…2 – Restatement (Third) Trusts [Section 90 cmt h(2)]

Because the differences in the totality of the costs…can be significant, it is important for the [fiduciary] to make careful overall cost comparisons, particularly among similar products of a specific type being considered for a [plan’s] portfolio.3

Investment icon Charles D. Ellis has contributed immeasurably to the wealth management industry over the years, especially in the area of prudent and cost-efficient investing. One of Ellis’ greatest contributions has been the recommendation that

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!4

With that in mind, it should come as no surprise that studies have consistently found that the overwhelming majority of act5ively managed mutual funds are not cost-efficient.

“99% of actively managed funds do not beat their index fund alternatives over the long-term net of fees.”5

“[I]ncreasing numbers of clients will realize that in toe-to-toe competition versus near-equal competitors, most active managers will not and cannot recover the costs and fees they charge.6

“[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.”7

“[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.”8

Several years ago I created a metric, the Actively Managed Value RatioTM (AMVR), based upon Ellis’ research and findings. The metric is simple, yet powerful. I use it in both my forensic investment analysis and my 401(k)/403(b) compliance consulting practices.

To further demonstrate the power of the AMVR, I often present the AMVR as an analogy to passing in football. When a football team throws a pass,, three things can happen, two of which are bad – a completion, an incompletion, or an interception.

The same soft of analogy can be used with regard to investing in actively managed mutual funds. Using the AMVR and Ellis’ incremental cost/incremental return technique for illustration purpose, investing in actively managed mutual funds results in one of four results – incremental returns greater than incremental costs (cost-efficient investing), or one of three scenarios in which incremental costs exceed incremental returns (cost-inefficient investing), what I call the AMVR Triple Option

In AMVR Analysis Triple Option #1, the actively managed fund simply underperforms the comparable benchmark index fund. Other than computing damages, there is no reason to even factor in the fund’s incremental costs in determining prudence given the active fund’s underperformance.

In AMVR Analysis Triple Option #2, the actively managed fund manages to produce a positive return. However, the fund’s incremental costs clearly exceed the fund’s incremental return by well over 100 percent. As a result, the active fund would still be an imprudent investment choice.

AMVR Analysis Triple Option #3 is the one that the plaintiff’s bar is increasingly using to argue a breach of fiduciary duties by investment fiduciaries. This option involves a metric, Ross Miller’s Active Expense Ratio, which factors in the R-squared, or correlations of returns number, between an actively managed fund and a comparable benchmark index fund.

Why factor in an active fund’s correlation of returns number? Miller explains that

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active fund management together in a way that understates the true cost of active management. In particular, funds engaging in closet or shadow indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.9

Over the past ten to fifteen years, there has been a definite trend of increasing correlation of returns between U.S. domestic equity funds. As a result, there has been a an increasing correlation of returns between U.S. domestic equity funds and index funds.

In some cases, the high correlation of returns may have been due to a deliberate attempt by actively managed funds trying to avoid large differences in performance so as not to potentially lose investors to index funds. Funds that engage in such practices have come to be known as “closet index” funds and “index huggers.”

In this example, the correlation of returns between the active fund and the index fund was 97. As the graphic shows, active funds that have high incremental costs and/or a high correlation of returns number will see a dramatic increase in their effective expense ratio, as well a dramatic decrease in their AMVR/cost-efficiency score.

A fund’s R-squared, aka correlation of returns, number also plays a factor in the Restatement’s other consistent theme, risk management through effective diversification. The key to effective diversification is to create an investment portfolio consisting of investments that are not highly correlated, investments that counter balance each other during varying market and/or economic conditions, the hope being the avoidance of large financial losses. So while most investors ,including fiduciary investors, believer that investing is an active, offensive process that focuses on returns, Ellis has long maintained that