James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Fiduciary Duty to Coduct Independent Investigation and Evaluation The courts have consistently held that plans have a fiduciary duty to conduct an independent and objective investigation and evaluation of the each investment included in a plan.

It is by now black-letter ERISA law that ‘the most basic of ERISA’s investment fiduciary duties [is] the duty to conduct an independent investigation into the merits of a particular investment.’ The failure to make any independent investigation and evaluation of a potential plan investment’ has repeatedly been held to constitute a breach of fiduciary obligations.1

A fiduciary’s independent investigation of the merits of a particular investment is at the heart of the prudent person standard.2 The determination of whether an investment was objectively imprudent is made on the basis of what the trustee knew or should have known; and the latter necessarily involves consideration of what facts would have come to his attention if he had fully complied with his duty to investigate and evaluate.3 (emphasis added)

Further complicating the situation is that there is ample evidence that plan sponsors often blindly rely on their plan adviser’s recommendations rather than perform their legally required investigations, even though the courts have consistently ruled that such blind reliance is a breach of a plan sponsor’s fiduciary duties, especially when stockbrokers and commissioned salespeople are involved. The courts have taken the position that such compensation issues create an inherent conflict of interest, and that that conflict may prevent an expert from providing the independent and impartial advice needed to ensure that the plan participants best interests are being served.

Blind reliance on a broker whole livelihood was derived from the commissions he was able to garner is the antithesis [of] a fiduciary’s duty to conduct an] independent investigation”4

[A] broker [is] not an impartial analyst. [A] broker [has an incentive to close deals], not to investigate which of several policies might serve the [plan] best. A [broker]…must consider both what plan it can convince the [plan] to accept and the size of the potential commission associated with each alternative.5

In conducting their investigations and evaluations, plan sponsors considering offering indexed annuities within their plan should especially note the “knows or should know” language within ERISA. I can, and have, argued that that language, combined with the language “solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries,” and the “sufficient information to make an informed decision” requirement under ERISA 404(c), are the potential Achilles’ heel of plan sponsors in future fiduciary litigation involving annuities.

In conducting their investigation and evaluation and making their final decisions, plan sponsors should consider the following quote from an executive with Northwestern Mutual with regard to indexed annuities:

These products are so complicated that I think it’s a stretch to believe that the agents, much less the clients, understand what they’ve got….The commissions are extreme. The surrender periods are too long. The complexity is way too high.6

MassMutual Financial Group shared similar concerns, so much so that it sent the results of a thirty-year study to its agents comparing the performance of an annuity based on the S&P 500 Index to an actual investment in the index itself. The study factored in the dividends an investor would have received as part of an actual investment in the index. The study also factored in the fact that indexed annuities do not receive the benefit of dividends paid by the annuity’s underlying index. The study assumed that the annuity had a 9.4 percent annual cap on returns.

The study found that over the relevant thirty years:

(1) Investors in the actual S&P 500 Index, with dividends reinvested, would have received an annual return of 12.2 percent. (2) Investors in the S&P 500 Index, without dividends, would have received an annual return of 8.5 percent. (3) Investors in the indexed annuity would have received an annual return of 5.8 percent.7

On a side note, the study also concluded that investors investing in simple Treasury bills would have actually fared better than those investing in the annuity, earning an annual return of 6.4 over the same thirty year period.

Caveat plan sponsors!

Fiduciary Duty to Disclose Material Information

[A] fiduciary is obligated to investigate all decisions that will affect the pension plan, and must act in the best interests of the beneficiaries.8”

The duty of loyalty requires a fiduciary to disclose any material information that could adversely affect a participant’s interests.”9

Information is material “if there is a substantial likelihood that it would mislead a reasonable employee in the process of making an adequately informed decision regarding benefits to which she might be entitled.”10

As the Restatement (Second) of Trusts states:

[The trustee] is under a duty to communicate to the beneficiary material facts affecting the interest of the beneficiary which he knows the beneficiary does not know and which the beneficiary needs to know for his protection in dealing with a third person.11

[The trustee] is under a duty to communicate to the beneficiary material facts affecting the interest of the beneficiary which he knows the beneficiary does not know and which the beneficiary needs to know for his protection in dealing with a third person.12

The duty of loyalty requires a fiduciary to disclose any material information that could adversely affect a participant’s interests. The duty to disclose material information is the core of a fiduciary’s responsibility, animating the common law of trusts long before the enactment of ERISA.13

Under ERISA, the term “material information” refers to any information that could affect a participant’s decision-making regarding their investments. This includes details about the investment options available and the risks and benefits of each option. allowing then to make choices that align with their financial goals and risk tolerance. 14

Sell the Sizzle, Not the Steak Based on my experience as a compliance director and fiduciary risk management consultant, the overwhelming majority of brokers and plan sponsors have no understanding of the methodology required to properly assess the prudence of annuities. More often than not, plan sponsors hear the mantra “guaranteed income for life” and they believe any annuity is prudent.

The mantra is an example of a common sales technique taught to brokers and agents – “Sell the sizzle, not the steak.” Talk up the allege benefits – guaranteed retirement income – and avoid discussing the negative, potential liability aspects of the product. We are seeing a perfect example of that now, as annuity advocates are playing up the benefits of extra income to plan sponsors without addressing the legitimate liability issues, that annuities present for investment fiduciaries, e.g., failure to provide commensurate return, required surrender of both the annuity contract and the accumulated value within the annuity without any corresponding guarantee of receiving a commensurate return, excessive fees. The late Peter Katt, a fee-only insurance adviser, taught me that with regards to insurance products always ask – “At what cost?”

Prior to entering the financial services as a compliance officer, I was a plaintiff’s personal injury attorney. In cases involving potentially significant injuries and monetary damage award, the defendant and their liability carrier will suggest a structured settlement. Structured settlements typically involve a small amoujnt of upfront cash, with the majority of the damages paid in the form of an annuity.

A plaintiff’s attorney has to ensure that the plaintiff actually receives the amount of money represented in the proposed settlement. After a long period of misrepresentations and other abusive practices by the annuity industry, the courts now require that the annuity carrier’s actual out of pocket expenses equal the amount of the proposed settlement.

For instance, annity issuers would often propose a settlement, but then purchase an annity at a substantially lower cost, often through a subsidiary. For example, if a plaintiff’s attorney convinces their client to accept a proposed settlement of one million dollars, only to find out that the liability carrier was able to purchase an annuity for only $250,000, the plaintiff’s atttorney will likely face a malpractice claim.

Therefore, it is absolutely essential that a plaintiff attorney either hire an expert or learn how to perform a forensic analysis of an annuity. I make the same recommendation to my fiducriary risk management clients. I also walk them through the proper process for evaluating annuities, a forensic actuarial breakeven analysis.

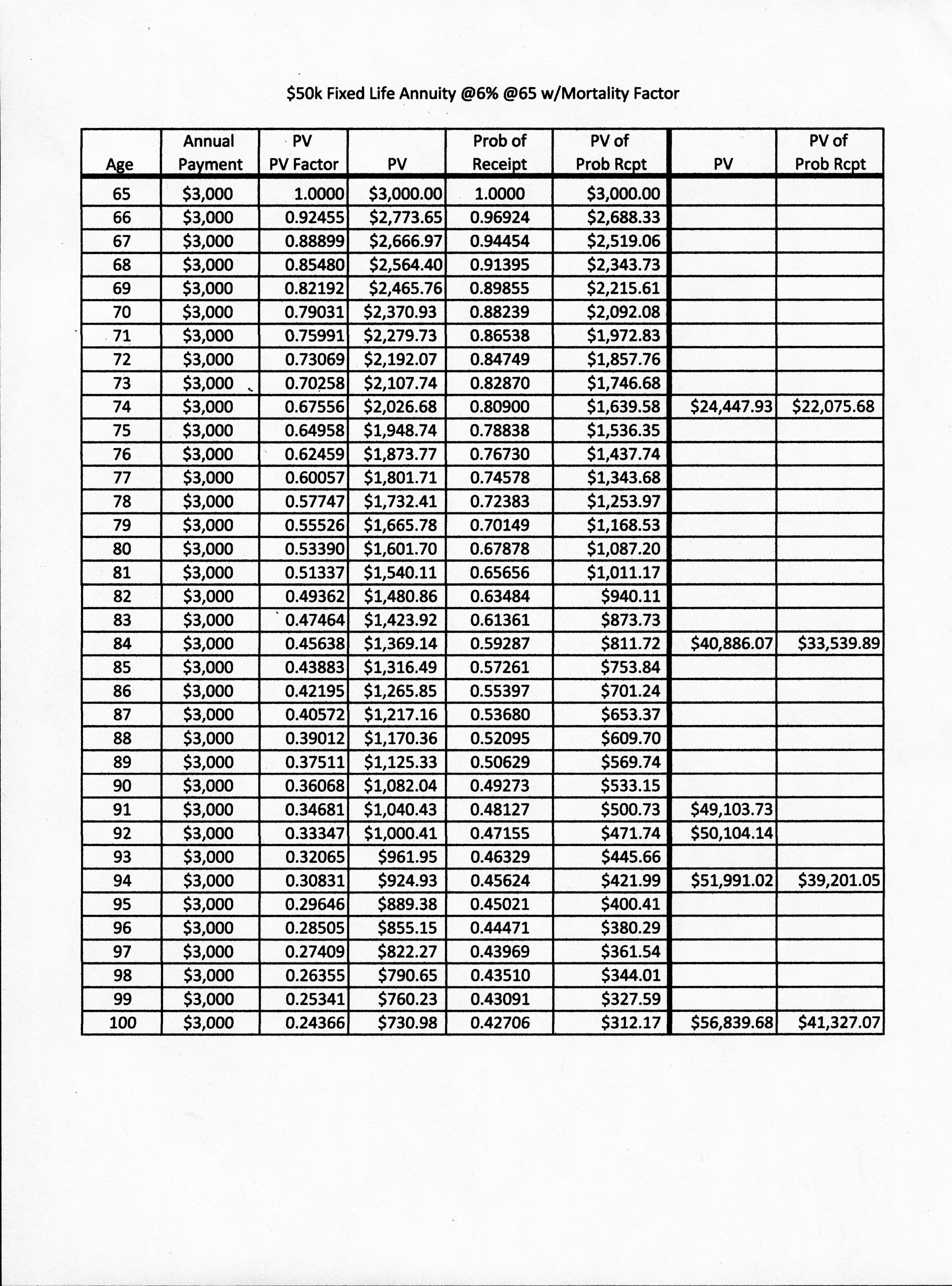

A common mistake in performing such an analysis is basing the analysis purely on present value (PV) calculations. PV calculations are important because they factor in the time value of money, that fact that payments to be made in the future are worth less than the same amount today. A sample breakeven analysis involving a $50,000 annuity on a man retiring at age 65 is shown below.

The breakeven analysis is valuable in indicating that based purely on PV calculations, the annuity owner would only have a 30 percent chance to breakeven on an investment in the asmple annuity, i.e., recover his intial capital investment, somewhere around age 92. So, just as in Las Vegas, the odds heqavily favor the “house,” the annuity issuer. As a result, one could legititmately argue that such information constitutes “material information” that a sponsor “should know” and consider in deciding on whether to offer the annity within a plan, since an objective analysis suggests that the odds were heavily against the annuity owner ever breaking even on his investment.

If the annuity provides that any balance remaining in the annuity reverts back to the annuity issuer.at the death of the annuity owner, this may result in a breach of the plan sponsor’s duty of loyalty, since the annuity issuer would thereby receive a windfall at the annuity owner expense. Section 5 of the Uniform Prudent Investor Act states that a fiduciary cannot make decisions that benefit the fiduciary or a third party at the beneficiary’s expense.15

In such situations, it can be argued that the plan sponsor violated their fiduciary duty of loyalty since the odds were in favor of the sannuity issuer realizing a benefit at the annuity owner’s expense, which the plan sponsor knew or should have known by reading the annuity prior to including the annuity within the plan sponsor’s plan. In legal terms, the harm was foreseeable, so fiduciary liability on the plan sponsor is both equitable and an appropriate remedy for the avoidable harm caused.

A prudent plan sponsor cannot fall for the “guaranteed income for life” spiel. As the late Peter Katt, a fee-only insurance adviser, always warned, when assessing insurance products, always include the question – “at what cost?” In this case, factoring in reasonable and objective input data, e.g., retiremeent at age, the odds were against the annuity owner ever breaking even at the time the plan sponsor made their decision, which is the appropriate standard for determining fiduciary prudence.

However, a prudent forensic fiduciary analysis of our sample annuity provides even more support for arguing that the plan spomsor’s decision to offer the annuity within the plan was imprudent. A proper forensic analysis of an annuity factors in mortality rate, the potential that the annuity owner will even receive a commensurate return, i.e., full return of the principal amount originally invested.

Factoring in mortality rate has a dramatic impact on the possibilities of the annuity owner breaking even. In our example, even if the annuity owner lives to be 100 years old, the annuity owner would be approximately $59,000 short of achieving a commensurate return, of beraking even. Mark Twain expressed the sentiment of many investors when he said “I am not so much concernd about the return ON my mooney as I am the return OF my money.”

My experience has been that most people do not work all their lives for the purpose of subsidizing the annuity industry. When an annuity owner annuitizes an annuity, the annuity owner loses ownership and control of both the annuity contract and the balance within the annity. Upon annuitization, the annuity issuer assumes ownership and controasl of both the annuity and the balance within the annuity, subject to the contractual provisions, namely the obligation to make the required payments as set out in the annuity contract.

Factoring in the applicable mortality rate significantly reduces the probability of both the fiduciary prudence of including annuities in pension plans, as well as the likelihood that an annuity owner will not receive a commensurate return. Evaluating the fiduciary prudence of including an annuity within a 401(k) plan or other type of defined contribution plan, based solely on PV, is legally imprudent.

While evaluating the prudence of an annuity purely on the basis of present value calculations is a fiduciary liability trap, present value can be useful to both plan participants and plan sponsors. If an annuity owner decides to sell their annuity, as many do, in most cases the buyer’s offer will be based on the annuity’s present value, not the original price the annuity owner paid. As the sample forensic breakeven analysis shows, the annuity owner can expect to suffer a significant loss from the owner’s intial investment.

Another use of present value is a well-known 30 second Excel “hack” using Microsoft Excel’s Present Value formula (shown under Formulas > Financial) to alert fiduciaries to potential “red flags” of fiduciary imprudence. Using our sample annuity analysis and Excel’s Present Value (PV) function, the input data would be “Rate” (0.06), “Nperiods” (I usually start at 25 and create additional iterations until the PV is equal to or greater than the annuity owner’s initial investment), and “Pmt” to owner, here based on an annual payment of -$3,000 ($50,000 times 6%).

The PV appears underneath the last column. in this case, after 25 years, the PV of the annuity would only be approximately $43,494, well below the original principal contributed. Using this Excel hack, the annuity owner would have to live well past 100 in order to receive a commensurate return on their original investment. Given the odds against anyone living to that age, and the fact that the odds against receiving a commensurate return would be even greater once the mortality risk factor is added, a plan sponsor would be hard pressed to justify the inclusion of the sample annuity in a plan, especially since ERISA does not explicitly require that a plan offer annuities and plan participants could always purchase annuities outside of a plan.

Plan Sponsors and the Art of Cross-Examination The fact that plan sponsors can easily evaluate annuities using a simple PV table and a mortality risk table supports the argument that this is information that a plan sponsor “knew or should have known” as a result of a properly conducted investigation and evaluation, “material information” that a plan sponsor would need to know in order to make an “prudent “decision, as required under ERISA Section 404(c)16

People often ask me to recommend books to teach them how to properly analyze and evaluate annuities. The two books I recommend are Paul Lesti’s “Structured Settlements,” and “Structuring Settlements” by James R. Eck and Jeffrey L. Ungerer. Both are excellent in describing and explaining structured settlements. I prefer the Eck and Ungerer book because of the simple step-by-step worksheets they provide. I use these same worksheets to teach my fiduciary clients. Both books are usually found in law school libraries.

Plan sponsors often ask me what they can do to protect both themselves and their employees. There are no alternatives to having a properly prepared forensic breakeven fiduciary prudence analysis performed, one that factors in both present value and mortality risk. As I tell my fiduciary risk management clients, the most effective risk management strategy is to avoid risk altogether, whenever possible. The InvestSense “KISS – Keep It Simple & Smart” “approach” is shown below.

We provide our clients with a few simple rules regarding the consideration of annuities in their plans:

Don’t consider annuities at all since they are not required to be offered in plans, so total avoidance is the “best practice” for plan sponsors and other investment fiduciaries. What plan participants do or do not want is irrelevant. ERISA only requires that a plan sponsor offer at leaast three well diversified and legally prudent investment options.

To document a prudent process was used in evaluating a annuity for inclusion within a plan, plan sponsors should always insist on a written beakeven analysis factoring in both PV and mortality risk, in case you need exhibits in future litigation.

Plan investment committees should learn how to personally perform a forensic actuarial analysis in order not to be “duped” by the annuity industry’s “sell the sizzle, not the steak” marketing ruse and to demonstrate that a prudent process was followed.

Avoid the guaranted income mantra and consider other viable guaranteed income alternatives, e.g.,bonds, CD’s, and dividends, which can be used to produce a slifetime stream of income without requiring an investor to surrender the asset and effectively subsidize the annuity industry. I have never met a plan participant whose goal was to work and save for the purpose of subsidizing the insurance and annuity industry.

Going Forward In addition to serving as a fiduciary risk management consultant, I also provide estate planning and wealth preservation advice. Annuities are essentially bets, with the annuity issuer betting that the annuity owner dos not live long enough to totally recover their original investment. As the sample analysis shows, the odds usually heavily favor the annuity issuer, resulting in a windfall for the annuity issuer.

Bayesian theory states that the probability of making a correct decision improves with each additional piece of relevant information. Using the sample forensic analysis provided herein and viewing the annity as a bet, we know the following information:

The odds are always heavily in favor of the annuity issuer, not the plan particiapnt, with arguably little chance of the annuity owner receiving a commensuarte return on their original investment.

Annuities are known for assessing excessive fees, further reducing the profitability of annuities.

In order to receive the alleged benefit, a guaranteed stream of income for life, an annuity owner must deplete available estate assets, potentially destroying any estate planning strategies for those wishing to provide for heirs.

Annuties are complex and confusing. Annuities are also for their lack of transparency/disclosure.

In “Thinking in Bets: Making Smaerter Decisions When You Don’t Have All the Facts,”16 Annie Duke suggests that decisions are often evaluated in terms of ultimate results. Duke argues that the prudence of decisions should be evaluated based upon the information avaialble and used at the time the decision is made, which is consistent with the standard used under ERISA. Even at the outset, the odds are heavily in favor of the annuity issuer, not the plan participant, benefiting from the annuity. Such a situation would violate the plan sponsor’s duties of prudence and loyalty. The duty of loyalty requires a plan sponsor to acr solely in the best interest of the plan participants and their beneficiaries.

The annuity industry’s basic pitch is typically along the lines of

How would you like to earn guaranteed retirement income for life. An annuity will guarantee that you will never run out of money. In order to receive this guaranteed stream of income, you will, however, be required to surrender ownership and control of both the annuity contract and the balancce remaining within the annuity, with no guarantee that you will ever receive a commensurate return on your original investment.

I am Scotch-Irish, so the deal offered above would be counterintuitive given the popular Scottish proverb

Get what you can, and keep what you have, that’s the way to get rich.

So, annuities are counterintuitive for us Scots, and should be so for plan sponsors and plan particiapnts/ due to the surrender of an estate asset without a guarantee of a commensurate return. Among estate planning attorney, annuities are also counterintiutive investments. Among estate planning attorneys, annuities are typically referred to as “estate planning saboteurs” since the success of estate plans generally depends on having sufficient assets in the estate to carry out the decedent’s last wishes. Annuities reduce available estate assets, with no guarantee of a commensurate return to replace such estate assets. Annuties are associated with excessive fees, further reducing estate assets.

ERISA provides that in selecting a plan’s investment options and in otherwise managing a plan,

a fiduciary shall discharge his duties …with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.17

The obvious issue is that a prudent man does not voluntarily surrendeer a substantial asset without an expectation of receiving a commensurate return. Annuities do not provide that assurance, at least not without charging yet another excessive fee via a “return of principal” rider, which in itself would violates the fiduciary duty to avoid unnecessary fees. In such situations, prudent people would insist on a commensurate return.

Bottom line – ERISA does not require that a plan offer annuities and annuies, which by their structure, inherently expose plan sponsors to unnecessary liability risk. Since plan participants are free to purchase annuities outside of a plan, the question plan sponsors should always ask before offering any annuity within a 401(k) plan or any other type of defined contribution plan is – “Why go there” The answer – “Don’t go there!”

Annuities are the antithesis of a plan spsonsor’s ERISA fiduciary duties of prudence and loyalty. Many annuity advocates react strongly when I make that statement. When I present the type of objective information contained herein, plan sponsors generally realize the truth in my position.

Annuities are essentially bets…bad bets!

I have previously stated my position with regard to annuities in ERISA plans:

To the extent that an annuity requires the annuity owner to surrender ownership of the annuity contract and conrol of the accumulated value of the annuity to receive the alleged benefit promised by the annuity, with no guarantee of the annuity owner even breaking even/receiving a commensurate return, and the terms of the annuity contract written in such a way as to essentially ensure that the annuity issuer and/or other third parties will reap a windfall at the annuity owners expense, such an annuity is a breach of an investment fiduciary’s duties of loyalty and prudence.

As for all the annuity industry studies and papers referencing what plaintiff’s want as part of plans, just remember this advice I always provide to my fiduciary risk management clients:

A plan sponsor’s fiduciary legal reality is defined by ERISA and the Restatement of Trusts, not by what plan participants supposedly want or what plan advisers and/or consultants may recommend.

Notes 1. Liss v. Smith, 991 F. Supp. 278, 299 (S.D.N.Y. 1998). (Liss), In re Enron Corp. Securities, Derivatives, and ERISA Litigation, 284 F. Supp. 2d 511, 546 (N.D. Tex 2003) 2. Donovan v. Cunningham, 716 F.2d 1455, 1467 (5th Cir. 1983); Donovan v. Bierwirth, 538 F.Supp. 463, 470 (E.D.N.Y.1981). 3. 29 U.S.C.A. Section 1104(c) 4. Liss 5. Gregg v. Transportation Workers of Am. Intern, 343 F.3d 833, 841-842 (6th Cir. 2003). (Gregg) 6. “Why Big Insurers Are Staying Away From This Year’s Hot Investment Product,” Wall Street Journal, D-12, December 14, 2005. (Staying Away) 7. Staying Away 8. Braden v. Wal-Mart Stores, Inc., 590 F. Supp. 2d 1159, 1167 (W.D. Mo. 2008) (Braden) 9. Braden, 1167-68 10. Braden, 1167-68 (W.D. Mo. 2008) 11. Eddy v. Colonial Life Ins. Co. of America, 919 F.2d 747, 750 (D.C. Cir. 1990) (Eddy), In re Enron Corp. Securities, Derivatives, and ERISA Litigation, 284 F. Supp. 2d 511, 546. 556 (N.D. Tex 2003). 12. Eddy, 750 13. Shea v. Esensten, 107 F.3d 625, 628; Eddy v. Colonial Life Ins. Co. of America, 919 F.2d 747, 750 (D.C. Cir.1990). 14. In re Dynergy ERISA Litigation, 309 F. Supp. 2d 861, 884-85 (S.D. Tex 2004), Restatement (Second of Trusts, Section 173, cmt d, (1959) American Law Institute. All rights reserved. 15. Uniform Prudent Investor Act, Section 5. 16. Annie Duke, “Thinking in Bets: Making Smart Decisions When you Don’t have all the Information,” Penguin Publishing Group (2019) 17. 29 U.S.C.A. Section 1104(a).

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

I am a securities and ERISA attorney. I hold CFP Board Emeritus™ status and I am an Accredited Wealth Management Advisor™. I provide fiduciary risk management consulting to 401k/430b plans, trustees, RIAs and other investment fiduciaries.

I am a 1977 graduate of Georgia State University and a 1981 graduate of the University of Notre Dame Law School. I am the author of "CommonSense InvestSense: The Power of the Informed Investor" and "The 401(k)/403(b) Investment Manual: What Plan Sponsors and Plan Participants REALLY Need To Know" I write two blogs, "CommonSense InvestSense, investsense.com, and "The Prudent Investment Fiduciary Rules, fiduciaryinvestsense.com.

As a former compliance director, I have extensive experience in evaluating the legal prudence of various types of investments, including mutual funds and annuities. My goal is to combine my legal and compliance experience in order to help educate investors and investment fiduciaries on sound, proven investment strategies that will help them protect their financial security and/or avoid unnecessary fiduciary liability exposure.

You must be logged in to post a comment.