James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

A common question I am receiving is “What are the fiduciary liability issues with in-plan annuities?”

A reccent LIMRA study found that plan sponsors are citing a desire to provide retirement income as the primary reason for some plan sponsors showing interest in retirement income inestment options.

Now, as the fiduciary prudence grinch, my initial response is always going to be “Is the specific investmeent and/or expressly required by ERISA?” If the answer is “no,” then my response will always be “Why go there?” Despite the fact that some annuity advocates say my position is cruel, the fact is that plan participants can always purchase an annuity outside of a retirement plan, thereby allowing a plan sponsor to avoid unnecessary fiduciary liability exposure. As my colleague, Nevin Adams, recently posted, simply framing the question in terms of the desirability of guaranteed retirement income is a canard, especially when fiduciary liability is involved.

I believe that the we are on the cusp of seeing plan sponsor fiduciary liability in connection with in-plan annuities develop into a significant fiduciary litigation issue. Judge Barbara Lynn addressed similar issues in her 2018 decision upholding the DOL’s Fiduciary Rule.1 (which the 5th Circuit overruled and then vacated the DOL’s Fiducairy Rule). My belief in the future growth of litigation involving in-plan annuities is even stronger given the fact that I recently participated in a program discussing a probable blueprint for successfully litigating in-plan annuity issues. I am also receiving an increaing number of inquiries from ERISA plaintiff attorneys on the same topic.

As a former plaintiff’s attorney, I am familiar with the insurance industry’s history of advocating for structured settlements whenever a case involves significant injuries and potentially significant damage awards. A structured settlement typically involves an upfront payment, with most of the damages being covered by an annuity.

From a plaintiff atttorney’s viewpoint, the challenge is to insure that any settlement offer results in a fair result, one that provides the plaintiff with a commensurate return for their injuries and related losses. For example, if the insurance company offers a settlement of $1,000, 000 dollars, with a requirement that the settlement involve a structured settlement, the plaintiff’s attorney must verify (1) that the cost of the annuity to the insurance company will actually be $1,000,000, and (2) that the annuity itself is in the client’s best interest, i.e., provide the client with commensurate return. Since attorneys owe their clients the fiduciary duties of loyalty and prudence, failure to verify the two referenced items can result in an attorney being sued for malpractice.

This is exacrly what happened for several years when insurance companies misled plaintiff attorneys and the court as to their costs in purchasing annuities for use in structured setlements. The insurance companies would misquote their costs, while actually purchasing the annuity from an affiliated insurance company, at a much lower cost.

As a result, prudent plaintiff attorneys either learned how to perform breakeven analyses of annuities or hired actuaries to provide and/or confirm, such analyses. While the actual process is relatively easy, my experience has been that very few plan sponsors perform such analyses in connection with deciding whether to offer in-plan annuities within their plan. As a result, I believe we are going to see an uptick in such litigation.

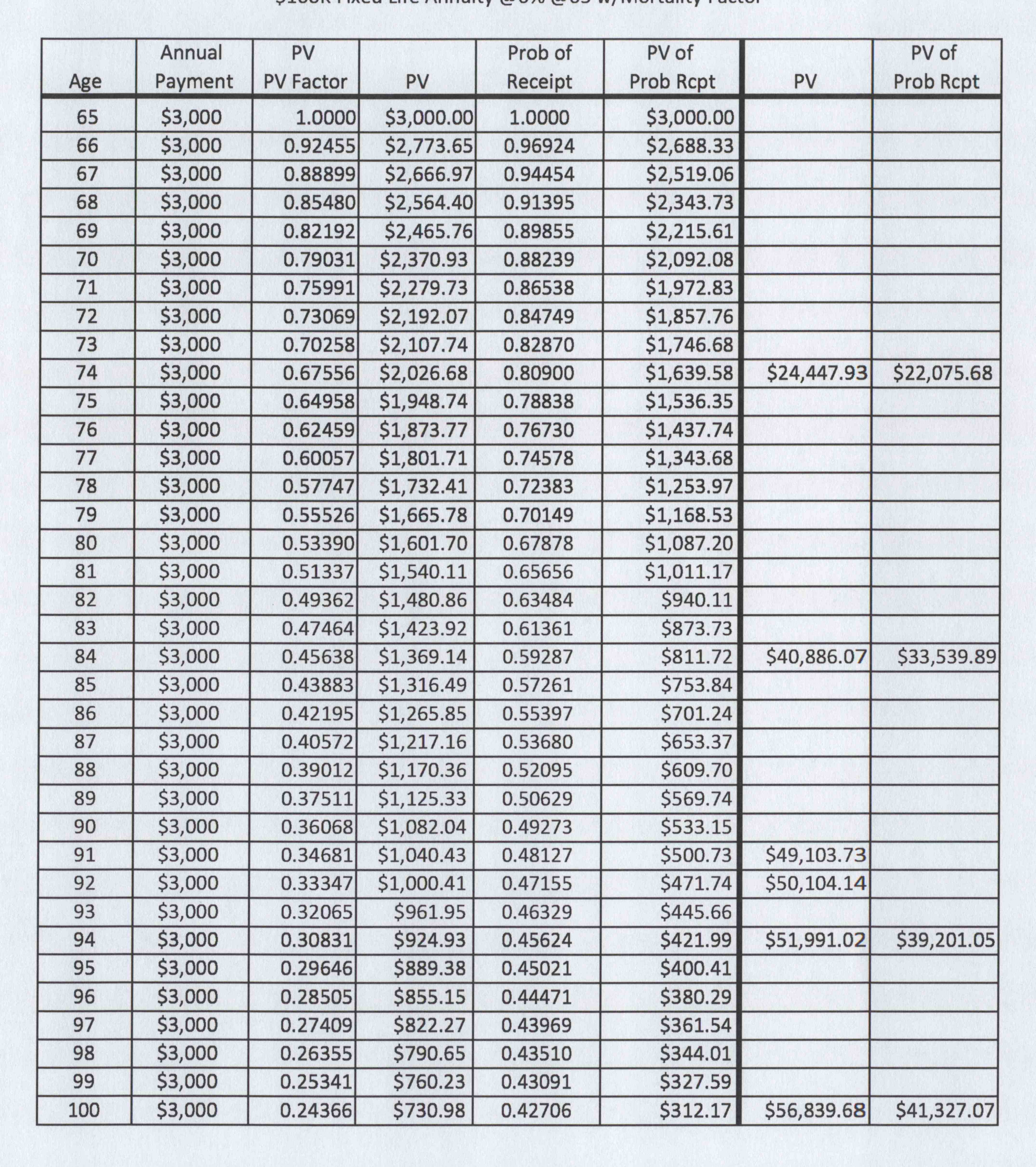

The graphic shown above is a forensic breakeven analysis on a $50,000 fixed annuity with an interest rate of 6 percent. The scenario assumes a plan participant retiring at age 65 and immediately annuitizing his annuity interest. To simplify the analysis, the example does not factor in annual charges/fees. However, plan sponsors and other investment fiducairies should always factor in the impact of such charges/fees, keeping in mind the GAO and DOL studies that found that each 1 percent in fees/charges reduces an investot’s end-return by approximately 17 percent over a twenty year period.2 Plan sponsors should also be alert to the fact that annuity advocates like to engage in semantics to try not to address the topic of costs/fees and other strategies that the annuity industry employs to avoid transparency of costs/fees and the impact of same on an investor’s end-return.

A properly prepared forensic breakeven analysis of an annuity should always factor in both present value and mortality risk. Present value is important not only in terms of factoring in the impact of inflation and the impact of the time value of money, but also because many annuity owners eventually sell their annuity because it is not providing them with the level of additional income needed. The party purchasing an annuity will typically base their offer on the present value of the annuity, not the original purchase price, as well as the present value of the annuity factoring in the mortality risk factor. in the example shown, note the significant difference in the present value calculations and the resulting commensurate return and fiduciary prudence issues.

As the chart shows, based purely on the subject annuity’s calculated present value, this annuity owner would not breakeven until sometime between age 91 and 92. If you factor mortality risk, the annuity owner would have to live well beyond age 100 just to breakeven on their original investment, raising significant commensurate return and potential fiduciary breach issues. The calculated breakeven point in relation to an investor’s life expectancy is a critical consideration on the issue of the prudence of the decision to include any in-plan annuity in the plan at all. If the annuity contained a reverter clause in favor of the iannuity issuer, that would potentially present fiduciary issues in terms of the fiduciary duty of loyalty since the annuity issuer could potentially receive a windfall at the expense of the annuity owner.

So, from a potential litigation standpoint, the basic issue would be whether “guaranteed retirement income” justifies the fact that the plan sponsor chose to offer an annuity which was structured in such a way as to make it unlikely that the plan participant would ever break even on the investment. Even worse in terms of fiduciary loyalty and prudence, an argument could be made that as a result of the plan sponsor’s choice of the annuity, the product’s design increased the likelihood that a third part (the annuity issuer) would eventually benefit at the expense of the plan participant, which would violate the plan sponsor’s duty to act solely in the best interest of the plan’s participants.

Keep in mind that under ERISA, potential plan sponsor fiduciary breaches are evaluated in terms of what the plan sponsor “knew or should have known” as a result of their legally required independent investigation and evaluation of all plan investment options.3 In this case, while a plan sponsor can legitimately argue that no one can predict when a plan participant will die, an legitimate argument can be made that that uncertainty works against a plan sponsor including an in-plan annuity option with a plan, especially when the annuity owner would need to live well beyond the expected life expectancy at that time just to break even, with a resulting windfall in favor the annuity issuer, resulting in potential fiduciary breach of loyalty issues.

People often criticize me for my “Why go there” position. It’s never a sign of indifference. Rather, it’s based on a recognition of and an avoidance of potential fiduciary risk. In this case, that question is very appropriate, especially given the fact that a plan participant wanting to purchase a similar annuity could easily do so outside the plan. Aside from the potential commissions generated by such an annuity, why would a plan adviser ever recommend the purchase of such an in-plan annuity and the potential liability issues?

I see situations like this all the time. The plan sponsor acts out of a desire to help employees, but the plan sponsor does not understand the annuity product and ends up actually hurting their workers financially.

Plan sponsors often ask me what they can do to protect both themselves and their employees. There are no shortcuts to having a properly prepared forensic breakeven fiducairy prudence analysis performed, one that factors in both present value and mortality risk. As I tell my fiduciary risk management clients, the most effective risk management strategy is to avoid risk altogether, whenever possible. The InvestSense “KISS – Keep It Simple & Smart” “approach” is shown below.

Going Forward

While “guaranteed retirement income” is tempting, plan sponsors should also ask – “At what cost?” Under both ERISA and the fiduciary standards set out in Section 90 of the Restatement (Third) of Trusts, two key fiduciary prudence questions regarding a plan’s investments are cost-efficiency and commensurate return for the additional costs and risiks assumed by an investor. Additional fiduciary risk management questions plan sponsors should consider include, but are not limited to:

- (1) Will in-plan annuity investors be required to surrender control of the annuity and the accumulated value within the annuity as a condition of receiving the “guaranteed retirement income? If so, what assurances are given to the investors with regard to receiving commensurate return on such forfeitures? Are there additional costs involved in receiving a commensurate return? What are the realistic odds of an investor in the plan’s in-plan annuitities actually breaking even?

- (2) Does the plan’s in-plan annuity include a reverter clause? If so, to whom does the balance in an annity revert in the event a plan participant does not break even on their investment iin the annuity?

- (3) Prior to deciding to include an in-plan annuity within the plan, did the plan sponsor perform a forensic breakeven analysis involving several likely sceanrios to determine the likelihood of investors in the annuity breaking even on their investment?

Notes

1. Chamber of Commerce of the U.S. v. Hugler, 231 F. Supp. 3d 152 (N.D. Tex. 2017)

2. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study).

3. Fink v. National Savs.& Trust Co., 772 F.2d 951, 957 (D.C. Cir. 1985)

You must be logged in to post a comment.