James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

In Tibble v. Edison International,1 SCOTUS noted the reliance of courts on the common law of trusts in resolving fiduciary matters, stating that

We have often noted that an ERISA fiduciary’s duty is ‘derived from the common law of trusts.’ In determining the contours of an ERISA fiduciary’s duty, courts often must look to the law of trusts.2 (citations omitted)

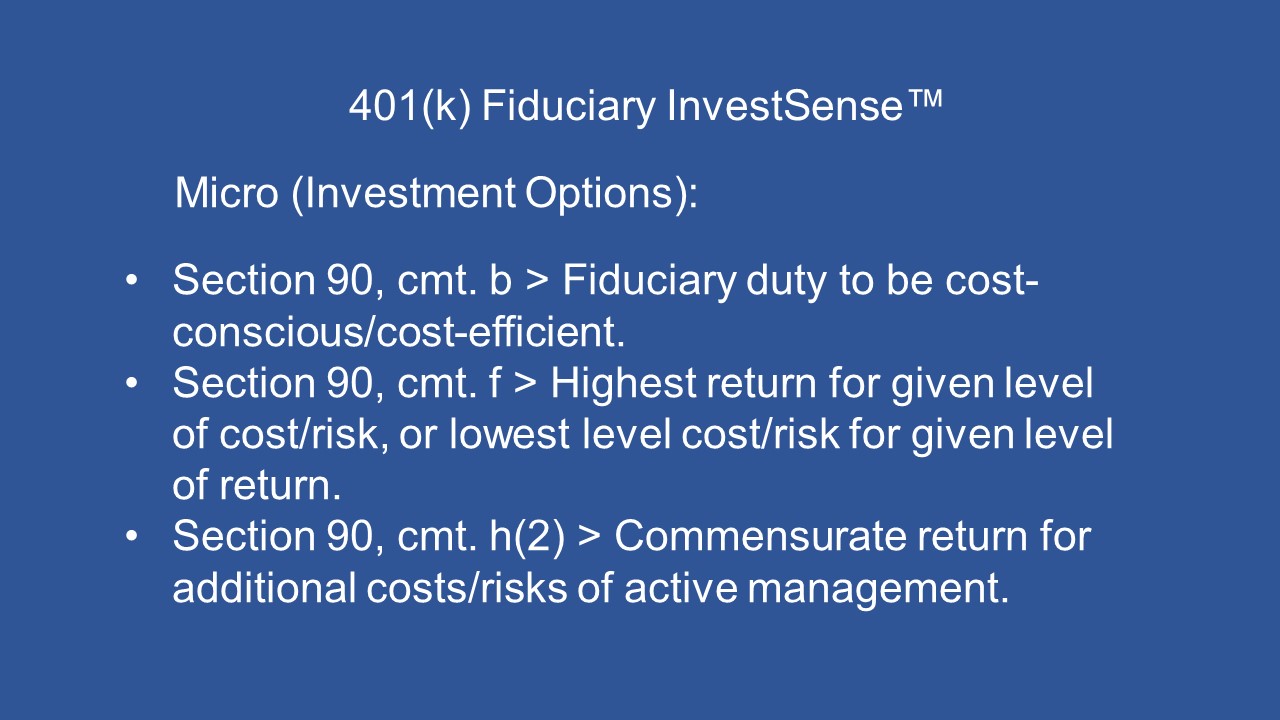

With SCOTUS’ endorsement in place, the next step is to determine what the the Restatement (Third) of Trusts (Restatement) says regarding fiduciary prudence. The Restatement sets out the common law of trusts. Section 90 of the Restatement is commonly known as the “Prudent Investor Rule.” Three key components of the Prudent Investor Rule are set out in comments b, f and h(2) of the Rule.

In 2015, the DOL issued Interpretive Bulletin 15-013 (IB 15-01). IB 15-01 reinstated earlier language from Interpretive Bulletin 94-14, specifically the following:

Consistent with fiduciaries’ obligations to choose economically superior investments….[P]lan fiduciaries should consider factors that potentially influence risk and return.5 (emphasis added)

[B]ecause every investment necessarily causes a plan to forgo other investment opportunities, an investment will not be prudent if it would provide a plan with a lower expected rate of return than available alternative investments with commensurate degrees of risk or is riskier than alternative available investments with commensurate rates of return.6

Sure sounds a lot like comment f from Section 90 of the Restatement. Sure sounds like further support for the use of cost-benefit analysis in evaluating the fiduciary prudence of the decisions of plan sponsors and other investment fiduciaries. Sure sounds like further support for the Active Management Value Ratio metric, which measures the cost-efficiency of an actively managed mutual fund relative to a comparable index fund.

JMO

Notes

1. Tibble v. Edison International, 135 S. Ct 1823 (2015). (Tibble)

2. Tibble, Ibid.

3. 29 CFR 2509.2015-01.

4. 29 CFR 2509.2015-01.

5. 29 CFR 2509.1994-01.

6. 29 CFR 2509.2015-01.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.