James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Men occasionally stumble over the truth, but most of them pick themselves up and hurry off as if nothing has happened.

Winston Churchill

Some courts continue to attempt to justify premature dismissals of 401(k) and 403(b) actions (collectively, “401(k) cases”) based on a court’s refusal to recognize index funds as “meaningful benchmarks” in determining whether a plan sponsor breached their fiduciary duties.1 Other courts have readily recognized comparable index funds as acceptable benchmarks in 401(k) cases, in most cases citing SCOTUS’ recognition of the Restatement of Trusts (Restatement) as a legitimate authority in resolving fiduciary issues.2

In the Tibble decision3, SCOTUS recognized the value of the Restatement in resolving fiduciary questions. SCOTUS noted that the Restatement essentially restates the common law of trusts, a standard often used by the courts. The two dominant themes running throughout the Restatement are the dual fiduciary duties of cost-consciousness and diversification within investment portfolios, the latter to reduce investment risk.

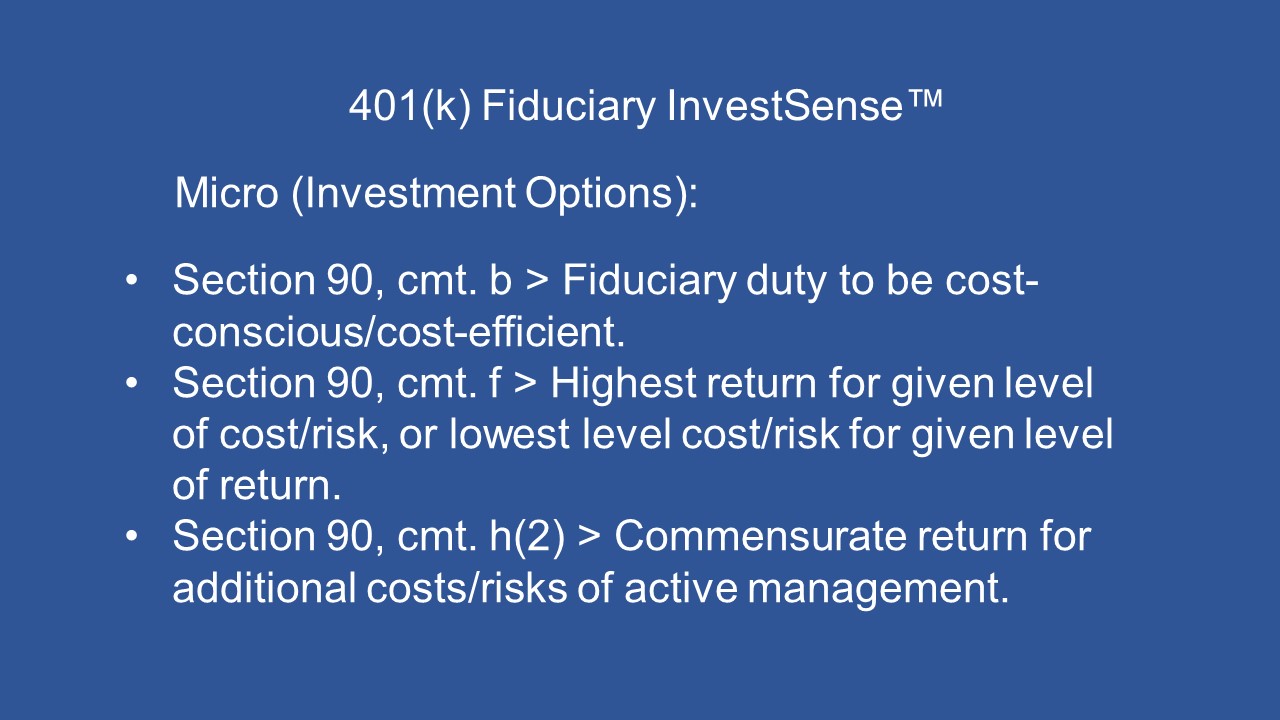

In my fiduciary risk management consulting practice, I rely heavily on five core principles from Section 90 of the Restatement to reduce fiduciary risk. Three of the five principles are cost-consciousness/cost-efficiency principles:

Comment h(2)’s commensurate return standard is a standard that I feel very few fiduciaries do, or can, meet if they include actively managed mutual funds in their plan. Actively managed funds start from behind in comparison to comparable passive/index funds due to the extra and higher expenses they incur from management fees and trading fees.

Advocates of active management often claim that active management provides an opportunity to overcome such cost issues. However, the evidence overwhelmingly indicates that very few do so, with most actively managed funds being unable to even cover their extra costs.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.4

Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.5

[T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.6

The First Circuit Court of Appeals has even suggested that plan sponsors wishing to avoid potential fiduciary liability for their selection of a plan’s investment options should consider comparable index funds as plan investment options.7

So, why are some courts continuing to ignore SCOTUS, the Restatement, and other federal circuit courts by refusing to accept comparable index funds as “meaningful benchmarks.” Why are some courts refusing to analyze 401(k) cases in terms of a more meaningful cost-efficiency approach instead of meritless arguments such as differing “strategies and goals” and/or the outdated active/passive debate, complete with the “apples-to-apples” argument?

Adopting a cost-efficiency approach, using a simple cost-benefit equation, will quickly and clearly indicate which available investment options are truly prudent, i.e., in the plan participants best interest. In adopting Reg BI, the SEC emphasized the inportance of recommending cost-efficient investment products and stratgies.8 Could it be that some courts, as well as the financial services industry, realize that the industries’ investment products are cost-inefficient and, in their present form, could never pass scrutiny under a cost-benefit analysis, much less a true fiduciary prudence standard?

How a legal action is framed is often a significant factor in the eventual outcome of the litigation. My argument in these cases has been that the primary focus in any ERISA action should always be consistency with the stated purposes of ERISA, namely protecting the rights guaranteed to employees under ERISA.

As mentioned earlier, the two dominant themes that run throughout ERISA are cost-consciousness/cost-efficiency and diversification.9 The legal system’s reliance on possible differences in strategies and goals is arguably nothing more than a “red herring” intended to avoid addressing the cost-efficiency issue.

Actively managed funds and index funds clearly employ different approaches in managing their funds. However, if the courts focus on the bottom line, namely which funds best serve a plan’s participants best interests in terms of cost-efficiency, the “apples-to-apples” argument has no merit. One benefit of adopting a basic cost/benefit analysis is that is can be use to compare various types of investments based on their relative costs and returns.

In the case of the active/passive debate, each category has the same opportunity to prove its managements strategies are superior to the other fund’s strategies. The fact that actively managed funds typically charge higher fees and incur higher transaction costs obviously favors the odds of the index fund posting better cost/benefit performance numbers. However, actively managed funds could easily revise their management style and/or fees to become more competitive. Which leads to an obvious question – just how much active management do “actively” managed funds actually provide, and how much benefit do plan participants actually derive from such active management?

Sunlight Is the Best Disinfectant

In a 2007 speech, then SEC General Counsel Brian G. Cartwright posed that very question. Cartwright asked his audience to think of an investment in an actively managed mutual fund as a combination of two investments: a position in an “virtual” index fund designed to track the S&P 500 at a very low cost, and a position in a “virtual” hedge fund, taking long and short positions in various stocks. Added, together, the two virtual funds would yield the mutual fund’s real holdings.

The presence of the virtual hedge fund is, of course, why you chose active management. If there were zero holdings in the virtual hedge fund — no overweightings or underweightings — then you would have only an index fund. Indications from the academic literature suggest in many cases the virtual hedge fund is far smaller than the virtual index fund. Which means…investors in some of these … are paying the costs of active management but getting instead something that looks a lot like an overpriced index fund. So don’t we need to be asking how to provide investors who choose active management with the information they need, in a form they can use, to determine whether or not they’re getting the desired bang for their buck?10

A simple metric that I created, The Actively Management Value Ratio (AMVR), allows investors, plan sponsors, trustees and other investment fiduciaries to do just that. The AMVR allows anyone to quickly compare the relative cost-efficienccy of two mutual funds.

The AMVR is most often used to compare an actively managed mutual fund to a comparable index funds. The AMVR is based on the research of three investment experts. The initial version of the AMVR was based on the postions of two investment icons, Nobel laureate Dr, William F, Sharpe and Charles D, Ellis.

T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.11

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns.12

In version 3.0 of the AMVR, I added the concept of the Active Expense Ratio (AER). Professor Ross Miller essentially reiterated Cartwright’s concept of viewing actively managed mutual funds as consisting of two “virtual” funds. Miller explained the importance of the AER as follows:

Mutual funds appear to provide investment services for relatively low fees because they bundle passive and active funds management together in a way that understates the true cost of active management. In particular, funds engaging in ‘closet’ or ‘shadow’ indexing charge their investors for active management while providing them with little more than an indexed investment. Even the average mutual fund, which ostensibly provides only active management, will have over 90% of the variance in its returns explained by its benchmark index.13

I have written numerous posts examining the basic elements of the AMVR. You can easily find these posts by using the seach box provided on the right side of the web site.

In this post, I want to address the possible impact of combining the AMVR and the AER in 401(k) litigation going forward. I believe that SCOTUS may soon have an opportunity to decide whether the plan or the plan participants have the burden of proof on the issue of causation in such actions.

There is currently a split within the federal courts on that very issue. Those arguing that the plan participants bear the burden of proof point to the general rule that a plaintiff has to prove all elements of their case.14 Those arguing that the burden belongs to the plan sponsors point to the fact that the general rule has exceptions, one being in cases involving fiduciary relationships and the higher duties imposed on fiduciaries under the law.15

SCOTUS had an opportunity to decide this issue back in 2018 in connection with the Brotherston decision. The First Circuit Court of Appeals had ruled that a plan sponsor bears the burden of proof on causation, the burden of showing that any damages sustained by plan participants were not caused by the plan.16

SCOTUS invited the Solicitor General to file an amicus brief with the Court addressing the issue. The Solicitor General’s amicus brief stated that the burden of proof on causation in 401(k) litigation belongs to the plan sponsors.17 The Solicitor General based his opinion on (1) the fiduciary relationship between a plan sponsor and the plan participants, and (2) the fact that only the plan sponsor knows why they made the decisions they did and the processes they used. However, the Solicitor General ultimately recommended that the Court not grant certiorari to review the case since the action was still ongoing.

Combining the AMVR and the AER – Getting Down to the Nitty-Gritty

The AMVR is essentially the same cost-benefit technique taught in introductory economics classes. The simple question is whether the projected costs of the project exceed the project’s projected benefits. Most 401(k) cases are decided solely by a judge, the argument being that the cases are too complicated for the genral public to understand. In many cases, I beleive that argument is yet another “red herring” to avoid jury awards. Based on my experience with the AMVR, John and Jane Q. Public understand the simplicity of the AMVR, that investments whose projected costs exceed their projected benefits/return are not a prudent investment choice, and thus a breach of anmy fiduciary duties

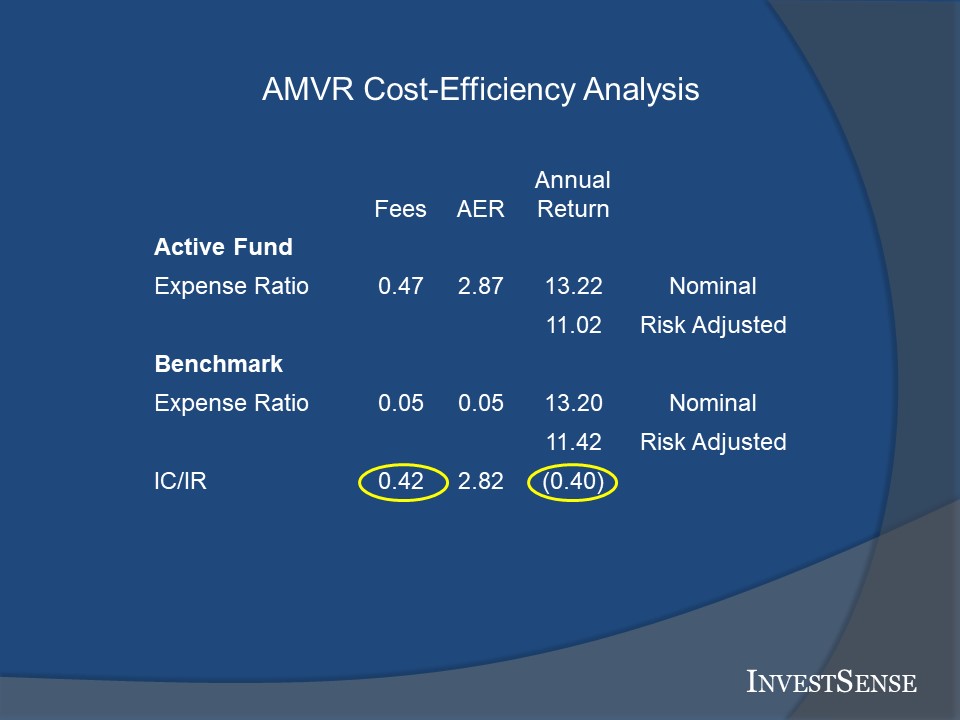

Using the two “virtual” funds concept suggested by both Cartwright and Miller, the AMVR calculations show that I could receive a more cost-efficient risk-adjusted return of 11.42 percent from the index fund alone. In this case, the actively managed fund was a total waste of money, as it provided absolutely no benefit whatsoever. As the Uniform Prudent Investor Act states, wasting plan participants’ money is never prudent.18

The AER calculates both the implicit percent of active management provided by an actively managed fund, as well as the implicit cost of same using the r-squared score of the actively managed fund The first step in Miller’s metric is to calculates the Active Weight (AW) of the actively manged fund, the percentage of active management provided by the actively managed fund.

The r-squared of the actively managed fund shown in our example is 97. Miller uses the following equation to calculate an actively managed fund’s AW:

AW = SQRT(1 – r-squared)/[SQRT(1 – r-squared) + (SQRT (R-squared)]

Here, AW would equal .1487, or 14.87% (1.723/11.580)

To calculate an actively managed fund’s AER, you divide the incremental cost number from the AMVR calculations by the actively managed fund’s AW. In our example, the actively managed fund’s AER, its implicit expense ratio, would be calcuated by dividing the fund’s incremental cost (0.42) by its AW (0.1487), resulting in an implicit expense ratio of 2.82, as opposed to the fund’s stated expense ratio, .

Since we are using the two “virtual” funds approach in analyzing the actively managed fund, we need to add back the index fund’s stated expense ratio (.05), resulting in an AER of 2.87. approximately 5 times higher than the fund’s stated expense ratio. Remember, wasting plan participants’ money is never prudent.

There are various methods of interpreting the AMVR results. The AMVR slide shown above shows how the prudence/imprudence of an actively managed fund can quickly be determined by simply answering two questions.

(1) Does the actively managed mutual fund provide a positive incremental risk-adjusted return relative to the benchmark index fund being used?

(2) If so, does the actively managed fund’s positive incremental risk-adjusted return exceed the fund’s incremental r-squared-adjusted costs relative to the benchmark index fund?

If the answer to either of these questions is “no,” the actively managed fund is cost-inefficient and, thus, imprudent according to the Restatement’s prudence standards. The actively managed fund shown above should be quickly rejected.

Since the AMVR is essentially a cost/benefit analysis, the goal for an actively managed fund is an AMVR number greater than “0” (indicating that the fund did provide a positive incremental adjusted return), but equal or less than “1” (indicating that the fund’s incremental adjusted costs did not exceed the fund’s incremental adjusted return).

As more plan sponsors, trustees, and other investment fiduciaries have adopted the AMVR metric as their fiduciary prudence standard, the one question that I have consistently received is why I added the AER at all. My response is always the same – trust me, there is definitely a method in the madness.

[A] large number of funds that purport to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by paying fees for active management that they do not receive or receive only partially….19

“Closet indexing” is a documented problem world-wide, Closet indexing raises important legal issues. Such funds are not just poor investments; they promise investors a service that they fail to provide. As such, some closet index funds may also run afoul of federal securities laws.20

While there is no universally agreed upon parameters for determing what constitutes closet indexing, the higher the level of correlation of returns, the stronger the argument for designation as a closet index fund. I personally believe that a correlation of 90 or above qualifies an actively managed fund as a closet index fund, especially when any incremental costs are considered. My postion is simply consistent with my position on the importance of cost-efficiency. Other groups use lower levels of correlation, even as low as 70.

Since research has shown that the overwhelming majority of actively managed mutual funds are cost-inefficient, unable to even cover their costs, the AER helps to expose possible closet index funds and avoid unnecessary fiduciary liability. For what it’s worth, ERISA plaintiff attorneys are increasingly incorporating the AER in their damages calculation in ERISA litigation.

Going Forward

2024 could prove to be a watershed year for both the 401(k)/403(b) industries and 401(k)/403(b) litigation. I believe that the odds are good that SCOTUS, if given the opportunity, will grant certiorari to review the Matney and/or the Home Depot 401(k) cases. My prediction is based primarily on the current split in the federal courts on the burden of proof in ERISA fiduciary cases, a split that is effectively denying employees in some sections of the country their rights and protections guaranteed under ERISA. Given the Court’s prior rulings in the Tibble21 and Northwestern22 cases, I believe that the Court would agree with the opinions of the Solicitor General, the DOL, several federal circuits, and the Restatement of Trusts and rule that the burden of proof as to causation in ERISA litigation properly belongs to the plan sponsor.

I believe that would result in increased 401(k)/403(b) litigation, not only between plan participants and plans, but also between plans and plan advisors. Plan sponsors often ask me what they can do to limit such liability and litigation exposure.

Unfortunately, I often have to advise them that due to the six-years statute of limitations that typically applies in 401(k) and 403(b) litigation, they can, and should, conduct a fiduciary prudence audit and immediately make any needed changes uncovered during the audit. While a prudence audit cannot retroactively limit any existing fiduciary liability exposure, it can proactively protect against such issues going forward.

What I am looking forward to seeing is how the financial service industry, both the securities and annuity sectors, address these issues. To date, the financial services industry has used a “preservation of choices” mantra. However, a cost-inefficient investment is not now, nor has ever been, a legitimate “choice.”

Yet another “red herring.” The AMVR can be used to provide the evidence to support such position. The AMVR can also provide a simple way to establish the monetary damages resulting from any breach of one’s fiduciary duties as a result of the inclusion of cost-inefficient actively managed funds within the plan.

As for the courts, hopefully the ERISA plaintiffs’ bar will address the continued unjustified and inequitable use of the “meaningful benchmarks” arguments to prematurely and inequitably dismiss meritorious 401(k) and 403(b) cases. While ERISA23 and other cases, most notably the First Circuit’s Brotherston decision, and various amicus briefs filed by the DOL24 and the Solicitor General25 have clearly established the validity of comparable index funds as legitimate comparators in ERISA litigation, the courts continue to ignore such arguments and authority.

Various reasons have been suggested for the refusal of some courts to recognize the fiduciary standards established by the Restatement and common law. Whatever those reasons may be, they do not justify either the denial of employees’ ERISA rights and the resulting, and possibly irreversible, harm being caused by the ongoing willful blindness of such courts.

One of my favorite sayings is from Aesop – “The tyrant will always find a pretext for his tyranny.” I have made several references to what I believe are pretexts that some courts are using to deny all employees a fair and equitable interpretation and protection of their rights under ERISA. ERISA is too important in helping employees work toward “retirement readiness” and their financial security to allow the current trend of dismissals of meritorious ERISA actions based on such pretexts.

The DOL’s recent amicus brief in the Home Depot 401(k) case made an interesting observation regarding some courts continuing reliance on the burden of proof on the causation issue to dismiss 401(k) and 403(b) actions. Citing the Second Circuit’s decision in the Sacerdote26 case, the DOL stated that

If a plaintiff succeeds in showing that “no prudent fiduciary” would have taken the challenged action, they have conclusively established loss causation, and there is no burden left to “shift” to the fiduciary defendant.27

It is just that simple. Can anyone truthfully argue that a prudent fiduciary would select cost-inefficient mutual funds when more cost-efficient investment options are available? Hopefully, 2024 will be the year that SCOTUS finally has an opportunity to address that question and, in so doing, make ERISA meaningful for all employees.

Notes

1. See, e.g., Meiners v. Wells Fargo & Co., 898 F.3d 820, 823 (8th Cir. 2018)

Matney v, Barrick Gold of North America, No. 22-4045, September 6, 2023 (10th Circuit Court of Appeals. (Matney)

2. See, e.g., Brotherston v. Putnam Investments, LLC, 907 F.3d 17 (2018). (Brotherston)

3. Tibble v. Edison International, 135 S. Ct 1823 (2015). (Tibble)

4. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

5. Charles D. Ellis, The Death of Active Investing, Financial Times, January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

6. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

7. Brotherston, Ibid.

8. Regulation Best Interest, Exchange Act Release 34-86031, 378, 380, 383-84 (2019).

9. 29 U.S.C.A. Section 404a; 29 C.F.R Section 2550.404a-1(a), (b)(i) and (b)(ii).

10. Martijn Cremers and Quinn Curtis, Do Mutual Fund Investors Get What They Pay For?:The Legal Consequences of Closet Index Funds.” https://papers.ssrn.com/sol/papers.cfm?abstract_id=2695133 (Cremers), 5, 42.

11. William F. Sharpe, “The Arithmetic of Active Investing.” https://web.stanford.edu/~wfsharpe/art/active/active.htm.

12. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines.” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c

13. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926.

14. Matney, Ibid.

15. Brotherston, Ibid.

16. Brotherston, Ibid.

17. Amicus Brief of Solicitor General Noel Francisco in Brotherston v. Putnam Investments, LLC .(hereinafter “Brotherston Amicus Brief”), available at https://bit.ly/2Yp00xt

18. Uniform Prudent Investor Act, https://www.uniformlaws.org/viewdocument/final-act-108?CommunityKey=58f87d0a-3617-4635-a2af-9a4d02d119c9 (UPIA)

19. Cremers, Ibid.

20. Cremers, Ibid.

21. Tibble, Ibid.

22. Hughes v. Northwestern University, 595 U.S. 170 (2022).

23. RESTATEMENT (THIRD) TRUSTS, Section 100, comment b(1). American Law Institute. All rights reserved.

24. Amicus Brief of the Department of Labor in Pizarro v. Home Depot, Inc., No. 22-13643 (11th Cir. 2022). (DOL Amicus Brief) http://www.dol.gov/sites/dolgov/files/SOL/briefs/2023/HomeDepot_2023-02-10.pdf

25. Brotherston Amicus Brief, Ibid.

26. Sacerdote v. New York University, 9 F.4th 95 (2d Cir. 2021)

27. DOL Amicus Brief, 26.

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.