The fiduciary duty of loyalty, as delineated in Section 78(3) of the Restatement (Third) of Trusts, imposes a stringent standard on fiduciaries, including plan sponsors and investment fiduciaries. The language “knew or should have known” underscores the expectation that fiduciaries remain vigilant and informed about their decisions and the tools they employ, such as artificial intelligence (AI).

In the retirement plan context (e.g., ERISA fiduciaries, plan sponsors, investment committees), courts and regulators often look to the Restatement for interpretive guidance on duty of prudence, loyalty, and monitoring obligations.

Under section 79(3), fiduciaries face exposure if they:

Knew of a breach (actual knowledge), or

Should have known (constructive knowledge based on what a reasonably prudent fiduciary would have known under the circumstances).

The “should have known” standard is objective and evolves with available tools, practices, and information in the fiduciary community.

A prudent fiduciary response requires

1. Demonstrated awareness of AI-enabled capabilities,

2. Deliberate governance decisions about their use, and

3. Robust documentation of the rationale behind those decisio

📌 Key Fiduciary Duties Under Section 78(3)

Section 78(3) articulates that a fiduciary must act with the utmost loyalty, avoiding conflicts of interest and placing the beneficiaries’ interests above all else. The “knew or should have known” standard implies that fiduciaries are expected to be aware of potential risks and to act proactively to mitigate them.

The “knew or should have known” standard is also repeated in ERISA scetion 404(a). Plan sponsors cannot legitimately claim to be surprised by the standard In the retirement plan context (e.g., ERISA fiduciaries, plan sponsors, investment committees), courts and regulators often look to the Restatement for interpretive guidance on duty of prudence, loyalty, and monitoring obligations. This is in accordance with the the Supreme Court’s direction in the landmark Tibble1 decision – look to the Restatement of Trusts when fiduciary issues ar involved

The “knew or should have known” standard emphasizes the need for fiduciaries to be proactive and informed. While AI offers significant advantages in financial decision-making, fiduciaries must exercise caution, ensuring that their use of AI aligns with their duty of loyalty and care. By implementing due diligence, oversight, and expert consultation, fiduciaries can navigate the complexities of AI integration while upholding their fiduciary responsibilities.

The proliferation of AI-based research, analytics, and monitoring tools (e.g., for investment due diligence, ESG risk screening, fee benchmarking, and market anomaly detection) may raise the baseline of reasonable prudence.

A fiduciary who fails to use—or at least consider—the insights available from these technologies could be deemed to have constructive knowledge of risks or issues that AI tools would have revealed.

AI and the Evolving Standard of Care

The “knew or should have known” standard emphasizes the need for fiduciaries to be proactive and informed. While AI offers significant advantages in financial decision-making, fiduciaries must exercise caution, ensuring that their use of AI aligns with their duty of loyalty and care. By implementing due diligence, oversight, and expert consultation, fiduciaries can navigate the complexities of AI integration while upholding their fiduciary responsibilities.

Process Integration

Integrate AI outputs into existing oversight frameworks (e.g., quarterly committee meetings, monitoring reports)

Establishes a defensible process

Consultant Oversight

Require service providers to disclose their use of AI or data analytics in fiduciary support

Shifts part of monitoring duty and ensures informed oversight

Documentation and Governance

Keep records of deliberations on whether and how AI tools were evaluated, selected, or excluded

Creates a paper trail showing prudence and good faith

Key Implication:

As AI becomes a widely available tool, courts and regulators may infer that a prudent fiduciary should have known what a commercially reasonable AI system could have shown.

Under Section 78(3), fiduciaries can be liable not only for what they knew but also for what they should have known—as the standard of what they “should have known” evolves with technology.

The increasing accessibility and sophistication of AI-driven fiduciary tools raise the bar for prudence and oversight. Plan sponsors and fiduciaries who fail to integrate or reasonably evaluate such tools risk constructive knowledge liability and co-fiduciary exposure.

Courts and regulators are applying increasingly technologically informed standards of prudence. As fiduciary tools advance, the threshold for what a fiduciary “should have known” correspondingly increases. AI-enabled analytics are no longer experimental—they are rapidly becoming an industry norm.

Under Section 78(3), the constructive knowledge standard may expand as AI tools make previously opaque information discoverable. Fiduciaries can no longer credibly claim ignorance of risks that automated tools routinely identify in peer institutions.

Regulators (e.g., DOL, SEC) and plaintiffs’ counsel increasingly reference data analytics capabilities as part of fiduciary process evaluation. Fiduciaries who cannot demonstrate awareness of these tools face heightened litigation vulnerability and discovery risk.

The fiduciary duty of prudence is dynamic. As AI and data-driven research redefine what fiduciaries can reasonably know, Section 78(3) increases the risk that inaction or failure to adopt available tools will be seen as a breach of fiduciary duty.

The “should have known” standard is objective and evolves with available tools, practices, and information in the fiduciary community.

Going Forward The likelihood that the courts may adopt a AI-generated breakeven analysis of annuities going forward is as much a matter of simplicity as a seach for equiatable decisions. The introduction of AI into questions of fiduciary prudence and fiducairy litigation zllows for quick and simple analyses, where changes in input data can be easily made, allowing for easier targeting of causation factors.My own experience in using AI to prepare annuity breakeven analysis have produced excellent results, allowing for properly factoring in both present value and mortality risk in the fiduciary prudence analysis. The ease and cost-efficiency of AI-generated fiduciary prudence analytics makes the inclusion of same in a plan’s process a must. An example of a sample prompt that I have used with success is

Prepare a breakeven analysis, brokern into annual intervals, factoring in both present value and mortality risk, on a $$$$$$ immediatew annuity for a 65 year-old male/female retiring at age X, asuming a normal life expectancy.

ERISA plaintifff attorneys are already using AI to develop cases and to design trial strategies. Plan sponsors can also use AI to create screens and interview strategies for vendos and plan advisers.

Notes 1. Tibble v. Edison International, 135 S. Ct. 1823, 1828 (2015).

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

“Facts are stubborn things; and whatever may be our wishes, our inclinations, or the dictates of our passion, they cannot alter the state of facts and evidence.” – John Adams

[C]onsistent with fiduciaries’ obligations to choose economically superior investments….[P]lan fiduciaries should consider factors that potentially influence risk and return. – 29 CFR 2509.2015-01

He fell at last a victim of the relentless ruthless of humble arithmetic. Remember, O stranger: ‘Arithmetic is the first of the sciences and the mother of safety’- Justice Louis Brandeis

Mathematics is the light that reveals the nature of things.”- Justice Louis Brandeis

“May it please the court. At issue in this case is whether the plan sponsor breached its fiduciary duties of prudence and loyalty by including annuities within the company’s 401(k) plan.

The plan argues that its decision to include such annuities was done solely in the best interest of both the plan participants and their beneficiaries, as required under Section 404(a) of ERISA. The plan sponsor claims that the selection and inclusion of the in-plan annuity was done solely to provide plan participants with additional retirement income and added financial security for participants and their beneficiaries. However, the evidence clearly suggests otherwise

During the trial, we introduced testimony and numerous exhibits that clearly establish that annuities are typically structured to benefit the annuity issuer, not the annuity owner. This is exactly why annuity issuers pay such a high commission to those who can convince a plan to offer annuities within their plan. It is also why annuities are an inherent fiduciary traps for plan sponsors and other investment fiduciaries.

The facts and mathematics that introduced in this case clearly establish that the annuity offered within the plan not only was not only not in the best interest of the plans’ participants or their beneficiaries, but that had the plan sponsor performed the legally required independent and objective investigation and evaluation required by ERISA1, the resulting harm was easily foreseeable using basic mathematical skills, i.e., humble arithmetic.

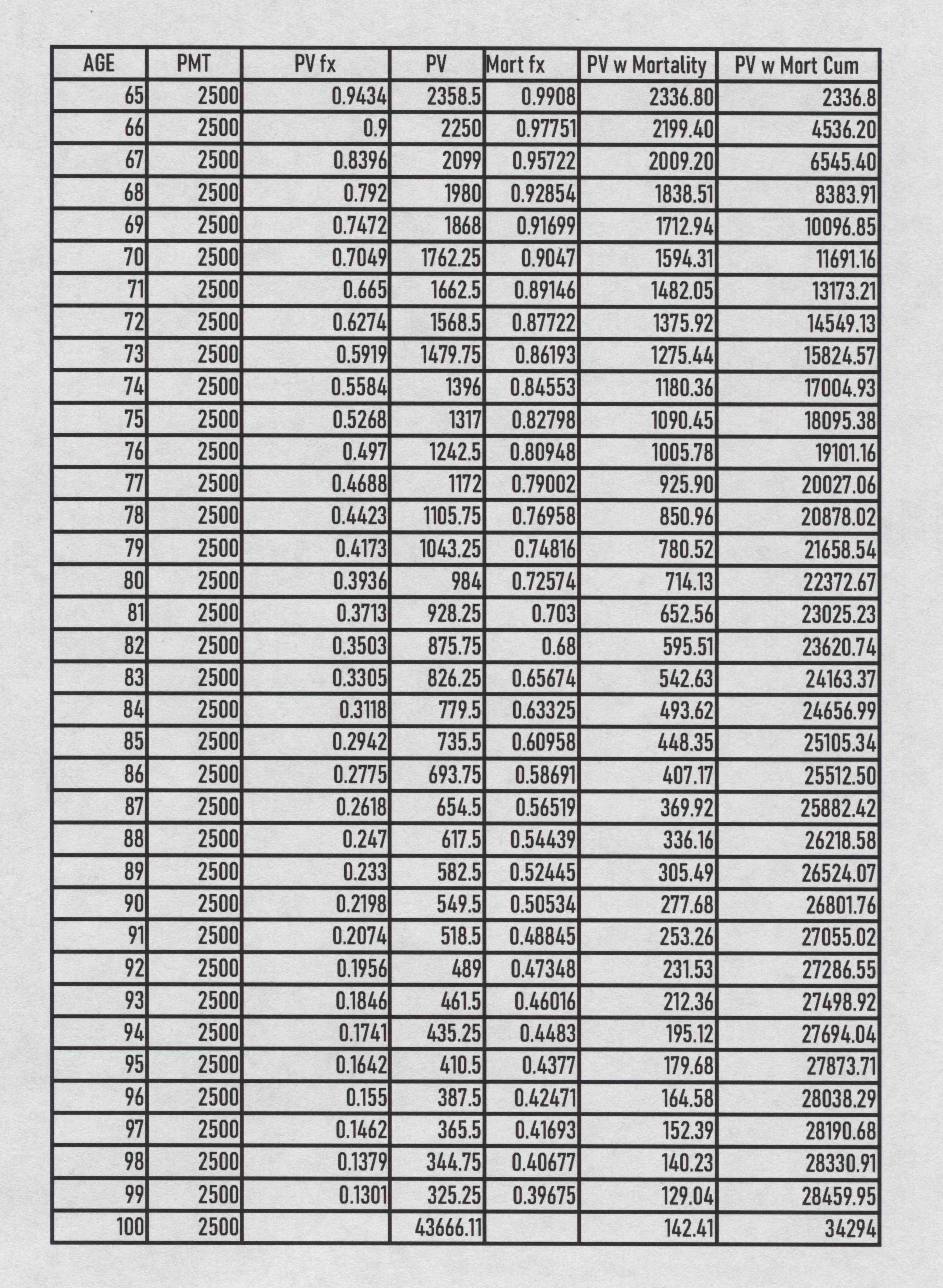

Reviewing Exhibit A, a basic Microsoft Excel breakeven analysis on an immediate $50,000 annuity, based solely on present value, paying 3% ($1,500) annually, for a 65 year old woman, with a normal lifetime expectancy (20.7 year). The data indicates that the odds of her reaching the age of 86, are 63%. Should that occur, at age 86, our Excel present value calculation predicted that the annuity owner would have only recovered approximately $18,076.80 , or 36% of her original value.

If we assume that the annuity owner chose a “life only” option in order to receive a higher annual distribution payment, that would result in a potential windfall of $31,923.20 for the annuity issuer. Multiply that by the potential number of owners of that particular annuity in the plan and you understand why the annuity industry is trying to make inroads into 401(k) plans and other ERISA pension plans.

The second part of the fiduciary breach equation in this case involves determining whether and when the annuity owner would actually break even by recovering the full amount of her $50,000 original investment. In this case, lets examine the situation if the 65 year old female participant lives to age 100. According to the Social Security Administration (SSA) Period Life Table:

A 65-year-old woman has about a 3.6% to 4% chance of living to age 100.

Assuming our annuity owner lives to age 100, our present value calculations project that at 100 she would only have recovered $19,000-$20,000 or 3.8-4% of her original investment, resulting in a windfall of $30,000- $31,000 for the annuity issuer.

In this case, our clients testified that the plan sponsor never disclosed such information, even though ERISA 404(c) requires that a plan sponsor provide plan participants with “sufficient information to make an informed decision.

Annuity advocates argue out that plan sponsors are not required to meet the “sufficient information” requirement unless they wish to qualify for the special protections offered under 404(c). However, since plan sponsors are legally fiduciaries, they are required to disclose “all material information” to plan participants.2

The courts have consistently defined “material information” as any information which an investor would deem helpful in deciding whether to invest in a product.3 I believe that a reasonable investor would consider the foregoing information, the heavy odds against simply breaking even, resulting in the annuity owner subsidizing the annuity issuer rather then the annuity owner’s heirs, “material.”

Exhibit B As bleak as that breakeven analysis is, a more accurate, and troubling, breakeven analysis is provided by factoring in both present value and mortality rate, the odds that the annuity owner will even be around to receive the annual distribution at a certain age. Going back to Exhibit A, we see that at age 86, the annuity owner would have recovered approximately $15,307, or 30% of her original investment. If we project out to age 100 (odds of 3.6-4%), the annuity owner would have recovered $17,218, or 34% of her original investment, leaving a nice windfall of $34,693 for the annuity issuer. Just as in Las Vegas, annuities are typically structured to ensure that the odds favor the “house.”

During your deliberations, ask yourself, would you consider such information “material” in making a decision as to whether to invest in the annuity. Then ask yourself whether the plan sponsor’s failure to ascertain these facts (a) as part of their legally required thorough and objective investigation and evaluation, and (b) the failure to disclose such information was “in the best interest of both the plan participants and their beneficiaries, or, rather, the third-party annuity issuer.

The plan sponsor admitted that they were not aware of such information and did not perform the necessary calculations themselves, that they blindly trusted the annuity broker’s advice and “expertise.” The courts have consistently warned plan sponsors or the dangers in such situations, especially when the reliance is on a commissioned salesperson:

Defendants relied on FPA, however, and FPA served as a broker, not an impartial analyst. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of “can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.5

As the judge will advise you, “a pure heart and an empty head are no defense in a case involving allegations of a breach of fiduciary duties.”6 In layman’s terms, there are no mulligans, no do-overs in fiduciary law, If a plan sponsor is unable to perform their legally required fiduciary duties, they have a duty to find someone who is qualified to do so objectively.7

Experience shows that too often plan sponsors simply choose to blindly follow the recommendations of product vendors and rely on the pure heart/empty head defense. As mentioned earlier, the dangers involved in adopting this practice were previously addressed in the Gregg decision.

Fortunately, plan sponsors can now use AI to perform a preliminary evaluation of an annuity recommendation. Note:An AI generated breakeven analysis should never be used as a replacement for the legally required investigation and evaluation, but rather as a “red flag’ for the need to obtain the services of a trained, experienced professional who is willing to serve in a fiduciary capacity and provide a written documentation of his breakeven analysis.

Using ChatGPT and the previously discussed data, I generated a breakeven analysis using the following prompt:

Prepare a fiduciary breakeven analysis, in annual intervals, on a $50,000 immediate annuity paying $1,500 a year, factoring in both present value and mortality risk, for a 65 year old woman, assuming normal life expectancy

ChatGPT concluded that:

📌 Breakeven Points

1. Nominal Breakeven (Total Cash = $50,000)

Reached in: Year 34 (age 99)

This is when she would have received $50,000 in total cash payments (50,000 ÷ 1,500 = 33.3 years)

This “nominal” breakeven analysis is the typical misrepresentation that the annuity advocates argue and the typical deliberately flawed analysis used by online annuity breakeven calculators and their providers. Just divide the amount of the investment by the interest rate, willfully ignoring the concept of the time value of money.

However, as ChatGPT points out, the legally proper way of constructing a breakeven analysis on an annuity requires that both present value and mortality risk be factored in order to account for both the time value of money and the likelihood of the annuity owner actually being alive to receive the annual annuity payment.

2. Present Value Breakeven

Total PV of future payments equals $50,000 around year 25–26 (age ~90–91), without mortality, well beyond the annuity owner’s life expectancy.

But adjusting for mortality, the expected value (EV) of all future payments peaks below $50,000, around $14,600–15,000.

This suggests the “actuarial expected value” of the annuity for a typical 65-year-old woman is around $14,000–15,000, despite the upfront $50,000 cost. This also assumes that the annuity owner chose the “single life” distribution option to maximize the annuity’s distributions.

🎯 Key Takeaways

Metric

Value

Total nominal breakeven (no time discounting)

Age 99 (Year 34)

PV breakeven (no mortality)

Age 90–91

EV of annuity (with 3% discount & mortality)

~$14,600

Life expectancy (female, age 65)

~20 years

🧠 Interpretation

If she lives to 90+, the annuity becomes a good deal in real-dollar terms.

If she dies earlier, the insurer “wins” (keeps remainder of capital).

This is the trade-off of longevity insurance—it’s not about individual return maximization, but hedging the risk of outliving assets

So, the odds favor the “house” ultimately receiving the majority of the initial investment at the expense of the annuity owner and their beneficiaries, in blatant violation of ERISA 404(a)’s requirement that plan sponsors act in the best interest of both plan participants and their beneficiaries.

This type of estate asset erosion, loss of estate assets (here, approximately $35,400, or 72%, of the of the original investment, is exactly why estate planning attorneys often refer to annuities as estate planning “saboteurs,” depleting an estate of the assets needed to carry out the decedent’s last wishes. Remember, as fiduciaries, plan sponsors have a duty to disclose all material facts, or, as ERISA section 404(c) states “sufficient information to make an informed decision.” 8You heard the plaintiffs state that the plan sponsor never met either of these standards.

ERISA requires a plan sponsor to acts as a prudent person would handle their own affairs.9 Ask yourself, does a prudent person invest $50,000 knowing that the odds are stacked against them, that the likelihood is that they are going to lose $72% of their investment in favor of the annuity company, to essentially subsidize the annuity issuer at the expense of one’s intended heirs.

Equally egregious is the fact that the plan sponsor claims to have included the annuity in the plan to help plan participants receive retirement income, yet admitted that it did not take the time to determine whether the annuity was actually in the best interests of said parties by performing these simple calculations despite the ready availability of such tools. The plan sponsor’s indifference and failure to properly perform the required investigation and evaluation is a blatant breach of their fiduciary duty of loyalty, which requires a plan sponsor to always put the best interests of both the plan participant and their beneficiaries first and foremost, ahead of the best interests of both the plan sponsor and any third parties.10

In our example, the plan sponsor stand to receive 76% of the original investment compared to the plan participant’s 24%. I submit to you that such an inequitable result was both clearly foreseeable had the plan sponsor taken the time to properly perform the required investigation and evaluation of the annuity. The law clearly states that in determining whether a fiduciary breach occurred, the plan sponsor will be held liable for what they knew, or should have known, had they simply conducted the proper investigation and evaluation of the investment product.11

Ladies and gentleman, you will have the opportunity to review both the testimony offered in this case, and the charts of our forensic calculations in the jury room during your deliberations. We ask that unlike the plan sponsor, you understand the importance of this case and its consequences upon the financial security of the plaintiffs.

Today, you have more power than you will probably have at any other time in your life. This is the only chance that the plaintiffs have of receiving justice.

The late General Norman Schwartzkop once said

“The truth is that we always know the right thing to do. The hard part is doing it.”

Ladies and gentlemen, that is all the plaintiff is asking of you today. Objectively review and consider the testimony and the evidence in this case, and do the right thing.”

I am frequently asked about the most common fiduciary risk management mistake that i see investment fiduciaries make. By far, the most common mistake I see is the failure to understand what is and is not legally required. As a result, investment fiduciaries constantly expose themselves to unnecessary fiduciary liability.

Often, that is a result of misplaced trust, blindly following the recommendations and advice of parties that do not owe any fiduciary duty to the investment fiduciary. As I have previously posted, NAIC Rule 275, the applicable insurance rule covering fiduciary duties not only does not expressly cover annuities, it expressly exempts ERISA pension plans from requirements of the Rule.12 As a result an annuity broker can claim to be in compliance with Rule 275, even though the advice and product recommendations provided may actually result in a fiduciary breach for the plan sponsor. This reinforces the need for plan sponsors to heed the warning set out in the Gregg decision.

I believe that the situation that many plan sponsors unknowingly may find themselves in is accurately summarized in this snippet from the famous cartoon, “Pogo.”

There is nothing in ERISA or any other law or regulation that expressly requires a plan sponsor to address retirement income or to include annuities providing within a 401(k) or other type of ERISA plan. Furthermore, prudent plan sponsors will realize that such products are available outside the plan, without potentially exposing the plan to fiduciary liability.

As noted fiduciary attorney, Fred Reish, likes to say – “Forewarned is forearmed.” And as I advise InvestSense’s fiduciary risk management clients, “do the math or use AI to do the math!” Or, better yet, if approached by an annuity vendor, let them do the math for you.

When approached by an annuity vendor, insist that before you will even consider their annuity recommendation, they have to provide you with a written breakeven analysis, one that factors in both present value and mortality risk. The fact that you routinely requested a written analysis can be used, if necessary, as proof that the plan sponosr did have a prudent process in place. However,odds are that they are not going to do it, as it would expose the imprudence of the annuity. However, if the annuity broker does provide a written analysis, always have it reviewed for accuracy. Again, further proof of reasonable reliance and a prudent process.

As mentioned earlier, the days of blind reliance on conflicted advice from product vendors and claims of altruistic intent by a plan sponsor, aka the “pure heart, empty defense,” are over. Hopefully, the final nail in the coffin will occur once SCOTUS hear the Pizarro v. Home Depot case later in the Court’s current term. I am on record as stating that I believe the Court will adopt the standard set out in Section 100 of the Restatement (Third) of Trusts, that being that the burden of proof on the issue of causation shifts to the plan sponsor once the plan participants establish the fiduciary breach and a resulting financial loss.

Selah

Notes 1. Liss v. Smith, 991 F. Supp. 278 (S.D.N.Y. 1998); Fink v. National Savings Bank,, 772 F.2d 951 (D.C. Cir. 1985). 2. Bins v. Exxon Corp., U.S.A, 220 F.3d 1042 (9th Cir. 2000); Donovan v. Bierwirth, 680F.2d 263 (2d Cir. 1982. 3.Bins, supra: Varity Corp. v. Howe, 516 U.S. 489 (1996) 4. TSC Industries v. Northway, Inc. 426 U.S. 438 (1976) 5.Donovan v. Cunningham, 716 F.2d 1455, 1467 (S.D.Tex. 1983) 7. Gregg v. Transportation Workers of America Int’l, 343 F.3d. 833, 841. 8. ERISA Section 404(a) 9. Bierwirth,supra. 10. Bierwirth, supra 11. ERISA Section 404(a.) 12.NAIC Rule 275.

“Facts are stubborn things; and whatever may be our wishes, our inclinations, or the dictates of our passion, they cannot alter the state of facts and evidence.” – John Adams

He fell at last a victim of the relentless ruless of humble arithmetic. Remember, O stranger: ‘Arithmetic is the first of the sciences and the mother of safety’- Justice Louis Brandeis

Mathematics is the light that reveals the nature of things.”- Justice Louis Brandeis

Closing Argument: Humble Arithmetic, Common Sense, and Fiduciary Prudence vs. In-Plan Annuities

“Facts are stubborn things; and whatever may be our wishes, our inclinations, or the dictates of our passion, they cannot alter the state of facts and evidence.” – John Adams

He fell at last a victim of the relentless ruthless of humble arithmetic. Remember, O stranger: ‘Arithmetic is the first of the sciences and the mother of safety’- Justice Louis Brandeis

Mathematics is the light that reveals the nature of things.”- Justice Louis Brandeis

“May it please the court. At issue in this case is whether the plan sponsor breached their fiduciary duties of prudence and loyalty by including annuities within the company’s 401(k) plan.

The plan argues that its decision to include such annuities was done solely in the best interest of both the plan participants and their beneficiaries, as required under Section 404(a) of ERISA. The plan sponsor claims that the selection and inclusion of the in-plan annuity was done solely to provide plan participants with additional retirement income and added financial security for participants and their beneficiaries. However, the evidence clearly suggests otherwise

During this trial, we have introduced testimony and numerous exhibits that clearly establish that annuities are typically structured to benefit the annuity issuer, not the annuity owner. This is exactly why annuity issuers pay such a high commission to those who can convince a plan to offer annuities within their plan.

The evidence and the mathematics that we have introduced in this case clearly establish that the annuity offered within the plan not only was not in the best interest of the plans’ participants or their beneficiaries, but also that had the plan sponsor performed the legally required independent and objective investigation and evaluation required by ERISA, the resulting harm was easily foreseeable using basic mathematical skills, i.e., humble arithmetic.

Reviewing Exhibit A, a basic Microsoft Excel breakeven analysis on an immediate $50,000 annuity, based solely on present value, paying 3% ($1,500) annually, for a 65 year old woman, with a normal lifetime expectancy (20.7 year). The data indicates that the odds of her reaching the age of 86, are 63%. Should that occur, at age 86, our Excel present value calculation predicts that the annuity owner would have only recovered approximately $18,076.80 , or 36% of her original value. If we assume that the annuity owner chose a “life only” option in order to receive a higher annual distribution payment, that would result in a potential windfall of $31,923.20 for the annuity issuer. Multiply that by the potential number of owners of that particular annuity in the plan and you understand why the annuity industry is trying to make inroads into 401(k) plans and other ERISA pension plans.

The second part of the fiduciary breach equation in this case involves determining whether and when the annuity owner would actually break even by recovering the full amount of her $50,000 original investment. In this case, lets examine the situation if the 65 year old female participant lives to age 100. According to the Social Security Administration (SSA) Period Life Table:

A 65-year-old woman has about a 3.6% to 4% chance of living to age 100.

Assuming our annuity owner lives to age 100, our present value calculations project that at 100 she would only have recovered $19,000-$20,000 or 3.8-4% of her original investment, resulting in a windfall of $30,000- $31,000 for the annuity issuer.

In this case, our clients have stated that the plan sponsor never disclosed such information, even though ERISA 404(c) requires that a plan sponsor provide plan participants with “sufficient information to make an informed decision.

Annuity advocates point out that plan sponsors are not required to meet the “sufficient information” requirement unless they wish to qualify for the special protections offered under 404(c). However, since plan sponsors are legally fiduciaries, they are required to disclose “all material information” to plan participants.

The courts have consistent defined “material information” as any information which an investor would deem helpful in deciding whether to invest in a product.# I believe that a reasonable investor would consider the foregoing information, the heavy odds against simply breaking even, resulting in the annuity owner subsidizing the annuity issuer rather then the annuity owner’s heirs, “material.”

Exhibit B As bleak as that breakeven analysis is, a more accurate, and troubling, breakeven analysis is provided by factoring in both present value and mortality rate, the odds that the annuity owner will even be around to receive the annual distribution at a certain age. Going back to Exhibit A, we see that at age 86, the annuity owner would have recovered approximately $15,307, or 30% of her original investment. If we project out to age 100 (odds of 3.6-4%), the annuity owner would have recovered $17,218, or 34% of her original investment, leaving a nice windfall of $34,693 for the annuity issuer. Just as in Las Vegas, annuities are typically structured to ensure that the odds favor the “house.”

During your deliberations, ask yourself, would you consider such information “material” in making a decision as to whether to invest in the annuity. Then ask yourself whether the plan sponsor’s failure to ascertain these facts (a) as part of their legally required thorough and objective investigation and evaluation, and (b) the failure to disclose such information was “in the best interest of both the plan participants and their beneficiaries, or, rather, the third party annuity issuer.

The plan sponsor has admitted that they were not aware of such information and did not perform the necessary calculations themselves, that they blindly trusted the annuity broker’s advice and “expertise.” The courts have consistently warned plan sponsors or the dangers in such situations, especially when the reliance is on a commissioned salesperson:

Defendants relied on FPA, however, and FPA served as a broker, not an impartial analyst. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of “can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.#

As the judge will advise you, “a pure heart and an empty head are no defense in a case involving allegations of a breach of fiduciary duties.”# In layman’s terms, there are no mulligans, no do-overs in fiduciary law, If a plan sponsor is unable to perform their legally required fiduciary duties, they have a duty to find someone who is qualified to do so objectively.

Experience shows that too often plan sponsors simply choose to blindly follow the recommendations of product vendors and rely on the pure heart/empty head defense. The dangers involved in adopting this practice were previously addressed in the Gregg decision, in which the court warned plan sponsors of the issues of relying on annuity brokers and other commissioned salespeople

Fortunately, plan sponsors can now use AI to perform a preliminary evaluation of an annuity recommendation. Note:An AI generated breakeven analysis should never be used as a replacement for the legally required investigation and evaluation, but rather as a “red flag’ for the need to obtain the services of a trained, experienced professional who is willing to serve in a fiduciary capacity and provide a written documentation of his breakeven analysis.

Using ChatGPT and the previously discussed data, I generated a breakeven analysis using the following prompt:

Prepare a fiduciary breakeven analysis, in annual intervals, on a $50,000 immediate annuity paying $1,500 a year, factoring in both present value and mortality risk, for a 65 year old woman, assuming normal life expectancy

ChatGPT concluded that:

📌 Breakeven Points

1. Nominal Breakeven (Total Cash = $50,000)

Reached in: Year 34 (age 99)

This is when she would have received $50,000 in total cash payments (50,000 ÷ 1,500 = 33.3 years)

This “nominal” breakeven analysis is the typical misrepresentation that the annuity advocates argue and the typical deliberately flawed analysis used by online annuity breakeven calculators and their providers. Just divide the amount of the investment by the interest rate, willfully ignoring the concept of the time value of money.

However, as ChatGPT points out, the legally proper way of constructing a breakeven analysis on an annuity requires that both present value and mortality risk be factored in order to account for both the time value of money and the likelihood of the annuity owner actually being alive to receive the annual annuity payment.

2. Present Value Breakeven

Total PV of future payments equals $50,000 around year 25–26 (age ~90–91), without mortality, well beyond the annuity owner’s life expectancy.

But adjusting for mortality, the expected value (EV) of all future payments peaks below $50,000, around $14,600–15,000.

This suggests the “actuarial expected value” of the annuity for a typical 65-year-old woman is around $14,000–15,000, despite the upfront $50,000 cost. This also assumes that the annuity owner chose the “single life” distribution option to maximize the annuity’s distributions.

🎯 Key Takeaways

Metric

Value

Total nominal breakeven (no time discounting)

Age 99 (Year 34)

PV breakeven (no mortality)

Age 90–91

EV of annuity (with 3% discount & mortality)

~$14,600

Life expectancy (female, age 65)

~20 years

🧠 Interpretation

If she lives to 90+, the annuity becomes a good deal in real-dollar terms.

If she dies earlier, the insurer “wins” (keeps remainder of capital).

This is the trade-off of longevity insurance—it’s not about individual return maximization, but hedging the risk of outliving assets

So, the odds favor the “house” ultimately receiving the majority of the initial investment at the expense of the annuity owner and their beneficiaries, in blatant violation of ERISA 404(a)’s requirement that plan sponsors act in the best interest of both plan participants and their beneficiaries.

This type of estate asset erosion, loss of estate assets (here, approximately $35,400, or 72%, of the of the original investment, is exactly why estate planning attorneys often refer to annuities as estate planning “saboteurs,” depleting an estate of the assets needed to carry out the decedent’s last wishes. Remember, as fiduciaries, plan sponsors have a duty to disclose all material facts, or, as ERISA section 404(c) states “sufficient information to make an informed decision.” You heard the plaintiffs state that the plan sponsor never met either of these standards.

ERISA requires a plan sponsor to acts as a prudent person would handle their own affairs. Ask yourself, does a prudent person invest $50,000 knowing that the odds are stacked against them, that the likelihood is that they are going to lose $72% of their investment in favor of the annuity company, to essentially subsidize the annuity issuer at the expense of one’s intended heirs.

Equally egregious is the fact that the plan sponsor claims to have included the annuity in the plan to help plan participants receive retirement income, yet admitted that it did not take the time to determine whether the annuity was actually in the best interests of said parties by performing these simple calculations despite the ready availability of such tools. The plan sponsor’s indifference and failure to properly perform the required investigation and evaluation is a blatant breach of their fiduciary duty of loyalty, which requires a plan sponsor to always put the best interests of both the plan participant and their beneficiaries first and foremost, ahead of the best interests of both the plan sponsor and any third parties.

In our example, the plan sponsor stand to receive 76% of the original investment compared to the plan participant’s 24%. I submit to you that such an inequitable result was both clearly foreseeable had the plan sponsor taken the time to properly perform the required investigation and evaluation of the annuity. The law clearly states that in determining whether a fiduciary breach occurred, the plan sponsor will be held liable for what they knew, or should have known, had they simply conducted the proper investigation and evaluation of the investment product.#

Ladies and gentleman, you will have the opportunity to review both the testimony offered in this case, and the charts of our forensic calculations in the jury room during your deliberations. We ask that unlike the plan sponsor, you understand the importance of this case and its consequences upon the financial security of the plaintiffs.

Today, you have more power than you will probably have at any other time in your life. This is the only chance that the plaintiffs have of receiving justice.

The late General Norman Schwartzkop once said

“The truth is that we always know the right thing to do. The hard part is doing it.”

Ladies and gentlemen, that is all the plaintiff is asking of you today. Objectively review and consider the testimony and the evidence in this case, and do the right thing.”

I am frequently asked about the most common fiduciary risk management mistake that i see investment fiduciaries make. By far, the most common mistake I see is the failure to understand what is and is not legally required. As a result, investment fiduciaries constantly expose themselves to unnecessary fiduciary liability.

Often, that is a result of misplaced trust, blindly following the recommendations and advice of parties that do not owe any fiduciary duty to the investment fiduciary. As I have previously posted, NAIC Rule 275, the applicable insurance rule covering fiduciary duties not only does not expressly cover annuities, it expressly exempts ERISA pension plans from requirements of the Rule. As a result an annuity broker can claim to be in compliance with Rule 275, even though the advice and product recommendations provided may actually result in a fiduciary breach for the plan sponsor. This reinforces the need for plan sponsors to heed the warning set out in the Gregg decision.

I believe that the situation that many plan sponsors unknowingly may find themselves in is accurately summarized in this snippet from the famous cartoon, “Pogo.”

There is nothing in ERISA or any other law or regulation that expressly requires a plan sponsor to address retirement income or to include annuities providing within a 401(k) or other type of ERISA plan. Furthermore, prudent plan sponsors will realize that such products are available outside the plan, without potentially exposing the plan to fiduciary liability.

As noted fiduciary attorney, Fred Reish, likes to say – “Forewarned is forearmed.” And as I advise InvestSense’s fiduciary risk management clients, “do the math!”

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

As a fiduciary risk management counsel, I read the DOL’s recent Advisory Opinion 2025-04A (Opinion) with great interest. As I read the opinion, I kept remembering my father’s advice – “The good Lord gave you a brain for a reason. Use it! Don’t be stupid.” In other words, always strive to make well-reasoned decisions.

Along those same lines, one of my main messages to our clients is to avoid unnecessary fiduciary risk exposure. To that end, InvestSense recommends that plan sponsors always use a simple two question analysis as a first step in evaluating potential investment options for their plan.

1. Does ERISA require a plan to offer the investment product or strategy in a plan? Hint: ERISA does not specifically require that any specific investment product or strategy be offered within a plan, only that each product offered within a plan be legally prudent.

2. If the product or strategy is not legally required to be offered within a plan, would/could offering the product or strategy expose the plan to unnecessary fiduciary risk? If so, why go there? Don’t go there! Don’t be stupid! Smart people do not valuntarily assume unnecessary risk. Thus, our directive for fiduciaries to Keep It Simple & Smart, or KISS.

Upon reading the Opinion, one particular sentence immediately stood out to me:

For participants who do not make a [SIP] allocation selection, the plan sponsor selects a default allocation percentage.” SIP refes to the annuity component in the investment at issue in the Opinion. Selecting investments for a plan is one thing. Any language calling for plan sponsors to become actively involving in making allocation decisions is a definite red flag, especially when the product itself is suspect as to fiduciary prudence.

While the Opinion seems to indicate that a plan participant can subsequently revise the percentage chosen by a plan sponsor, the complexity of the product itself and the likelihood of confusion of a plan participant raises numerous fiduciary litigation red flags as to potential litigation . The product fails the two question test.

With no legal obligation to offer the product, the prudent choice for a plan sponsor is not to do so at all, as plan participants interested in said product can do so outside of the plan, without exposing the plan to unnecessary and unwanted fiduciary liability.

Another reason for my position is the inconsistency between the standards set out in NAIC Rule 275 and ERISA 404(a). As I discussed the in an earlier post.1 The inconsistency clearly allows for the possibility that a broker’s recommendation may be compliant with Rule 275, while non-compliant with ERISA 404(a). As a result, the broker’s recommendation may actually result in a fiduciary breach by, and resulting liability for, the plan sponsor.

In managing fiduciary risk, InvestSense stresses the importance of two court decisions, one in connection with actively managed mutual funds, the other in connection with annuities. Both decisions are widely cited by courts across the country, The annuity case is Gregg v. International Transportation Workers of America, in which the court explained the need for pension plans to proceed in caution when considering recommendations involving annuity brokers:

Insurance brokers [like FPA] do not work for a pension plan; rather, insurance companies like Transamerica pay individual insurance broker a salary. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.”2

Because of the obvious conflict of interest issues created whenever commissions are involved, I would suggest that all investment fiduciaries heed the Gregg court’s warning. For investment fiduciaries, it is always best to avoid even the appearance of impropriety. As Judge Cardozo pointed out in the legendary fiduciary decision of Meinhard v. Salmon:

Many forms of conduct permissible in a workaday world for those acting at arm’s length, are forbidden to those bound by fiduciary ties. A trustee is held to something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most sensitive, is then the standard of behavior. As to this there has developed a tradition that is unbending and inveterate. Uncompromising rigidity has been the attitude of courts of equity when petitioned to undermine the rule of undivided loyalty by the “disintegrating erosion” of particular exceptions). Only thus has the level of conduct for fiduciaries been kept at a level higher than that trodden by the crowd.3 (citation omitted)

In other words, avoid even the appearance of impropriety.

This DOL Opinion has no impact on anyone other than the parties involved and does not compel any action on the part of other plan sponsors. As a result of the issues identified herein, we have advised our clients to ignore both this Opinon and the product involved.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

As a fiduciary risk management counsel, I’m often asked about my opinion as to the biggest risk management mistake plan sponsors make. To me, the answer is simple. The biggest and most common fiduciary risk management mistake that I see investment fiduciaries make, including plan sponsors, is not knowing and understanding what the law does, and does not, require of them in their fiduciary capacity.

I recently gave a presentation on the “next big thing” in ERISA fiduciary litigation. Overall, I expect healthcare fiduciary litigation to continue to increase. I believe there is going to be an increase in fiduciary litigation involving in-plan annuities and annuities, in any form, in plans in general, including TDFs with an embedded annuity element.

The litigation liability area that I think is most promising for ERISA plaintiff attorneys is the inconsistency in standards between ERISA 404(a)1 and NAIC Rule 275.2 There is simply no middle ground.i I have heard some annuity advocates claim that NAIC Rule 275 provides a safe harbor for plan sponsors who choose to include annuities in their plans, despite the fact that there is no evidence to support such claims. Furthermore, Rule 275 explicitly exempts ERISA plans from Rule 275 coverage…3

Other annuity advocates point to the SECURE Acts as providing safe harbor protection for plan sponsors choosing to include annuities in their plans. The SECURE Acts provide a safe harbor in connection with the selection of an annuity provider, not the selection ofan annuity product. The prudence of an annuity itself is still subject to ERISA’s prudence and loyalty requirements.

I think the Achilles’ heel that ERISA plaintiff attorneys should focus on is the obvious inconsistency of the standards between ERISA 404(a) and NAIC rule 275 and the potential fiduciary liability that exists, liability which is going to completely blindslide many plan sponsors, as there has been little discussion on the issue. The issue is that annuity salespeople can be in compliance with Rule 275 while leaving plan sponsors unknowingly in violation of ERISA 404(a) due to the inconsistencies in the two standards.

§ 2550.404a-1 Investment duties.

In general. Sections 404(a)(1)(A) and 404(a)(1)(B) of the Employee Retirement Income Security Act of 1974, as amended (ERISA or the Act) provide, in part, that a fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan; and with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.

Compare that language to the NAIC’s suitability requirements in connection with the sale of annuities:

Section 1. Purpose A. The purpose of this regulation is to require producers, as defined in this regulation, to act in the best interest of the consumer when making a recommendation of an annuity and to require insurers to establish and maintain a system to supervise recommendations so that the insurance needs and financial objectives of consumers at the time of the transaction are effectively addressed

Section 4. Exemptions Unless otherwise specifically included, this regulation shall not apply to transactions involving: A. Direct response solicitations where there is no recommendation based on information collected from the consumer pursuant to this regulation; B. Contracts used to fund: (1) An employee pension or welfare benefit plan that is covered by the Employee Retirement and Income Security Act (ERISA); (2) A plan described by Sections 401(a), 401(k), 403(b), 408(k) or 408(p) of the Internal Revenue Code (IRC), as amended, if established or maintained by an employer;

Section 6. Duties of Insurers and Producers A. Best Interest Obligations. A producer, when making a recommendation of an annuity, shall act in the best interest of the consumer under the circumstances known at the time the recommendation is made, without placing the producer’s or the insurer’s financial interest ahead of the consumer’s interest. A producer has acted in the best interest of the consumer if they have satisfied the following obligations regarding care, disclosure, conflict of interest and documentation:

Section 6 (1) (a) Care Obligation. The producer, in making a recommendation shall exercise reasonable diligence, care and skill to: (i) Know the consumer’s financial situation, insurance needs and financial objectives; (ii) Understand the available recommendation options after making a reasonable inquiry into options available to the producer; (iii) Have a reasonable basis to believe the recommended option effectively addresses the consumer’s financial situation, insurance needs and financial objectives over the life of the product, as evaluated in light of the consumer profile information;,

Not only does NAIC Rule 275 explicitly exempt ERISA plans from coverage under tthe Rule, it also does not require an annuity agent to factor in the best interests of the annuity owner’s beneficiaries when making recommendations involving annuities. It has been suggested to me that Rule 275 does not require consideration of the plan participant’s beneficiaries’ best interests because Rule 275 assumes that ERISA plans have access to experts who will ensure that the beneficiaries’ best interests have been considered. Experience has shown that such assumption is not supported by the evidence.

InvestSense, LLC, teaches our clients a simple two-step risk management process in analying potential investment options wihtina plan:

– Step One – Does ERISA or any other law/regulation expressly require that a plan offer the investment option be offered within a plan?

The answer is “no.” ERISA does not expressly require that any specific type of investment option be offered within a plan, only that all investment options offeredwithin a plan be legally prudent.

Step Two – Would/Could the investment option under consideration potentially expose the plan to unnecessary fiduciary liability?

If so, common sense should tell the plan to avoid the investment option. Plan participants interested in such products would still have the option of purchaing such investments outside of the plan, without potentially exposing the plan to unnecessary fiduciary risk.

With regard to annuities, we generally advise our clients to avoid them altogether, since plans have no legal obligation to provide such so-called “retirement income” products or strategies. Furthermore, most forensic techniques, such as breakeven analysis, prove that annuities are rarely in the best interests of either the plan participant or their benficiaries. As for annuity industry claims that plan participants “want’ such products, as a former securities compliance director, I always remember the annuity wholesalers stressing to our brokers that “annuities are sold, not bought.” As for self-serving annuity industry polls and surveys supporting such claims, plan sponsors have a legal obligation to comply with ERISA, not the alleged whims of some plan participants.

My experience has been that very few plan sponsors are aware of or have actually read ERISA 404(a) or NAIC Rule 275, choosing instead to blindly rely on the misrepresentations of annuity wholesalers and brokers, despite the warnings of the courts that such blind reliance on commissioned salespeople is not legally justified due to the obvious financial conflict of interest.

Defendants relied on FPA, however, and FPA served as a broker, not an impartial analyst. {Brokers} are not independent analysts. FPA does not work for the plan; rather, insurance companies like Transamerica pay [a broker’s salary.] As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.4

See also: Bussian v. RJR Nabisco, Inc., 223 F.3d 286, 301(5th Cir. 2000) (fiduciaries may not “rely blindly” on advice); In re Unisys.,74 F.3d 420, 435-36 (3d. Cir. 1996).

Fortunately, plan sponsors can independently evaluate the prudence of an annuity by performing an annuity breakeven analysis using Microsoft Excel. While a properly prepared breakeven should factor in both present value and mortality risk, a simple present value breakeven analysis using Excel often indicates the legal imprudence of an annuity based on present value considerations alone.

Going Forward The key point to consider is that an adviser recommending an in-plan or another form of an annuity as an investment option in a plan may be in compliance with NAIC Rule 275, but may nevertheless place a plan sponsor in violation of ERISA 404(a) due to the inconsistency in standards. The fact that annuities often require the annuity owner to annuitize the annuity, i.e., surrender the annuity contract and the amount of their investment, in order to receive the alleged benefit of the annuity, the stream of retirement, with absolutely no guarantee of a commensurate rerturn means that the annuity issuer stands to receive a windall at the annuity owner’s expense. Courts dislike such inequitable situations, citing that equity law, a basic component of fiduciary law, abhors a windfall. Upon annuitization, the annuity issuer becomes the legal owner of the value within the annuity. So, there is typically nothing available for the annuity owner’s beneficiaries, a result that the plan sponsor “knew or should have known”, a foreseeable result that is an obvious violation of ERISA 404(a)’s requirement to act in the beneficiaries’ best interests and should have factored in deciding whether toan annuity within the plan..

Annuity advocates will typically mention the availability of various “rider”s to address these issues. Unless they offer such riders for free (they don’t), there is the issue of the additional cost and the findings of both the General Accountability Office (GAO) and the Department of Labor (DOL) on the impact of cumulative fees and the compounding of same. Both the DOL and GAO determined that over a twenty-year period, each additional 1% in fees reduces an investor’s end-return by approximately 17%.

Therfore, plan sponsors considering annuities need to keep “3%” in mind, since 3 times 17 would result in plan participants and their beneficiaries losing 51 percent of their end-return. So, while annuity advocates may mention various riders, they often “forget” to mention the cumulative/compounding cost issue of the basic cost and fees of annuities. Adding the cost of riders would be expected to easily exceed the “3%” cumulative fees threshold, benefitting the annuity issuer at the annuity owner’s expense, a clear breach of the fiduciary duty of loyalty..

One last piece of advice. Investment fiduciaries who receive a recommendation to include an annuity, any type of annuity, should always require the annuity salesperson to provide a written, properly prepared breakeven analysis on the annuity being recommended. A written analysis can be introduced into evidence, if necessary. Trial attorneys will tell you that you never want a case to become a “he said,” she said” situation. If the annuity salesperson refuses request to provide a written breakeven analysis showing the process they used (they will, they know the truth about their product. They just hope you don’t.) The the prudent plan sponsor will simply walk away.Fiduciary risk management often requires proactive strategies and measures by an investment fiduciary.

One last reminder for plan sponsors considering annuities, there is no such thing as “mulligans’ in fiduciary law! Heed the sound advice of former CEO Jack Welch – “Don’t make the process harder than it is.”

Notes 1. 29 U.S.C.A. Section 1104(a). 2. NAIC Rule 275 – Suitability in Annuity Transactions Model Regulation (Rule 275) 3. Rule 275, Section 4, “Exemptions,” B(2). 4. Gregg v. Transportation Workers of Am. Intern, 343 F.3d 833, 841 (6th Cir. 2003). 5. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study).

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

President recently released an excutive order requesting that the DOL and other relevant regulatory bodies create guidelines and other measures, including safe harbors, that would allow plans to offer unnecessarily risk investments, such as private equity and crypto, inside 401k plans.

1. As a fiduciary risk management counsel, one of the most noticeable aspects is that ERISA does not mandate that any specific types of investment be offered within an ERISA plan.

The key requirements of Section 404 of ERISA are:

a fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan;

with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.

With regard to the consideration of an investment or investment course of action taken by a fiduciary of an employee benefit plan pursuant to the fiduciary’s investment duties, the requirements of section 404(a)(1)(B) of the Act set forth in paragraph (a) of this section are satisfied if the fiduciary:

(i) Has given appropriate consideration to those facts and circumstances that, given the scope of such fiduciary’s investment duties, the fiduciary knows or should know are relevant to the particular investment or investment course of action involved, including the role the investment or investment course of action plays in that portion of the plan’s investment portfolio or menu with respect to which the fiduciary has investment duties; and

(ii) Has acted accordingly.

For purposes of paragraph (b)(1) of this section, “appropriate consideration” shall include, but is not necessarily limited to:(i) A determination by the fiduciary that the particular investment or investment course of action is reasonably designed, as part of the portfolio (or, where applicable, that portion of the plan portfolio with respect to which the fiduciary has investment duties) or menu, to further the purposes of the plan, taking into consideration the risk of loss and the opportunity for gain (or other return) associated with the investment or investment course of action compared to the opportunity for gain (or other return) associated with reasonably available alternatives with similar risks;

The arguments can be, and have been, made that the alternative investments set out in the executive order are not only unnecessary, but are too risky and inconsistent with both the spirit and letter of ERISA’s provisions with the prudence process described under ERISA.

Prudent plan sponsors would be best served by totally ignoring the Presient’s executive order and just continue to monitor their plan’s existing internal process to ensure that their plan is ERISA compliant. 2. “”it is by now black-letter ERISA law that “the most basic of ERISA’s investment duties [is] the duty to conduct an independent an independent investigation into the merits of a particular investment….’The failure to make any independent invstigation and evaluation of a potential plan investment” has repeatedly been held to constitute a breach of fiduciary olgigations.” Liss v. Smith, 991 F. Supp. 278. 297 (S.D.N.Y. 1989), citing In re Unisys Savings PlanLitigation, 74 F.3d 420, 435 (3d Cir 1996), and Whitfield v. Cohen, 682 F. Supp. 188, 195 (S.D.N.Y 1988).

In In re Citigroup ERISA Litigation, 112 F. Supp 3d 156 (S.D.N.Y. 2015) (2017), the federal court for the Southern District of New York emphasized that a plan sponsor acting as a fiduciary under ERISA has a duty to independently and thoroughly investigate and evaluate each investment option offered within a 401(k) plan.

The court stated that fiduciaries cannot simply rely on the mere presence of an investment option or general market reputation but must conduct a careful, ongoing review to ensure the option is prudent and aligns with the plan participants’ best interests. This includes analyzing fees, risks, performance, and any other relevant factors that affect the value and suitability of the investments.

The ruling underscored that fiduciaries must:

Perform an independent due diligence process rather than blindly following advice or defaulting to common offerings.

Continuously monitor the investments, removing imprudent ones if necessary.

Ensure investment decisions are thorough, deliberate, and documented to meet ERISA’s standard of prudence.

Failure to meet these fiduciary duties can lead to liability for losses to plan participants.

Given the lack of transparency associated with the alternate investments set out in the executive order, is it even possible for a plan sponsor to comply with the independent investigation and evaluation requirement? The lack of transparency typically associated with alternative inevsments would clearly require a plan sponsor to rely on the information and value estimations of these conflicted and legally unreliable vendors. Gregg v. Intern’l Trasportation Workers of America, (reliance on commissioned salespeople is never legally justifiable}.

Since neither ERISA not any any laws/regulations require a plan to offer such potentially liability ridden investments, the obvious question from a fiduciary risk management standpoint – “Why go there?

3. We teach our fiduciary risk management clients that the best risk management strategy is to avoid risk altogether whenever possible. The Executive Order suggested that the DOL and other agencies create safe harbors for plan sponsors recommending alternative investments.

Why is it that whenever Congress or the President support unecessarily risky investments that could undermine the financial wellness and retirement security of American workers, they always seek to include a safe harbor to protect plan sponsors, but totally frustrate the very focus of ERISA, protecting the American workers? The financial services industry needs a helping hand, so we’re going to recommend these risky investments…and to Hell with American workers.

Think that’s unduly harsh? Ask an annuity peddler to provide a properly prepared written breakeven analysis, factoring in both present value and mortality risk. I am often asked to sit in on a plan’s investment committee meeting where an annuity peddler is scheduled to make a presentation. Ask the annuity wholesaler to provide a written breakeven analysis. Typicall response is that they are not legally required to do so. I quickly offer to provide such a breakeven analysis after the meeting.

In my opinion, a refusal to provide such a properly prepared, written breakeven is the equivalent to what the legal profession refers to as an admission against interest and/or an example of the what the law refers to as res ipsa loquitor (the facts speak for themselves). That should be the red flag to end the meeting.

The written breakeven analysis is also prudent in that it demonstrates due diligence on the part of the plan sponsor. Fiduciaries have a duty to disclose all “material facts” to plan participants.

Quite often a properly prepared breakeven will indicate that the odds of benefitting from an annuity heavily favor the annuty issuer rather than the plan participants. With regard to investments, the law described a “material information” as any fact or information that an investor would find beneficial in making an investment decision. I’m guessing that most investors would consider information suggesting that they are unlikelly to break even on a certain annuity, that the odds favor the annuity issuer at the investor’s expense, would influence the investor’s investment decision.

I’m also guessing that few plan sponsors have the skill or knowlege to properly create their own annuity breakeven analysis. I’m also guessing that few plan sponors have the experience or skill to properly investigate and/or evaluate alternative investments.

Going Forward Fortunately, there is no obligation under ERISA or any other law to offer any specific type of investments in an ERISA plan. Nothing about the Executive Order changes that fact.

President Trump suggested safe harbors for plan sponsors who decide to offer alternative investments within a plan. I have read the executive order several times and still cannot find a provision addressing the best interests and financial wellness of the plan participants. Until such such concerns are properly addressed, prudent plan sponsors and their plan participants would be well advised to ignore the Excutive Order and follow the sage advice of jack Welch – “Don’t make the process harder than it is.”

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

ERISA Section 404a-1 provides as follows:

2550.404a-1 Investment duties.

(a) In general. Sections 404(a)(1)(A) and 404(a)(1)(B) of the Employee Retirement Income Security Act of 1974, as amended (ERISA or the Act) provide, in part, that a fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan; and with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.

Based on my experience, too many plan sponsors who are considering or have included in-plan annuities as an investment option within their plan have either overlooked or have not properly assessed the potential fiduciary liability risks presented by the inclusion of the “and their beneficiaries” language.

The most obvious concern for a plan sponsor should be with the possibility of an in-plan annuity resulting in an erosion of estate assets. Annuity advocates frequently point to available options such as annuity riders to protect against estate asset protection. Unless the annuity issuer iss providing such riders for free (they don’t), then the additional costs further reduce returns and estate assets. As SCOTUS pointed out in Hughes v. Northwestern University#, each investment option within a plan must be individually prudent, must stand on its own.

That would presumably rule out the added costs of the “bells and whistles suggested by the annuity industry. After all, as both the DOL and GAO studies# pointed out, over a twenty year period, each additional 1 percent in fees and costs reduces an investor’s end-return by approximately 17 percent. It does not take much for cumulative costs on annuities to exceed 3 percent annually, at which point the annuity becomes a better investment for the annuity issuer than the plan participant, and a fiduciary breach for the plan sponsor.

The annuity industry loves to use head games to sell their product. They used the “squandering plaintiff” ruse in an attempt to convince courts to require structured settlements in cases involving significant damage payments. Attorney Jeremy Babener exposed that ruse by pointing out that there was no verifiable evidence of the evidence cited by the industry, with the general counsel essentially admitting that the “evidence” cited by the industry were simply made up to help promote the industry.#

Currently we have some annuity advocates attempting to manipulate plan sponsors and other investment fiduciaries by reportedly suggesting that they have a legal obligation to offer annuities within a plan. Other questionable annuity marketing strategies involving plan sposnors include recommending annuities for decumulation purposes. Let’s set the record straight:

There is no legal foundation for the suggestion that ERISA or any other law requires a plan to offer annuities within plan.

There is no legal foundation for the suggestion that ERISA or any other law requires a plan to offer any specific type of investment. ERISA simply requires that each investment offered within a plan be legally prudent.

There is no legal foundation for the suggestion that plan sponsors have any legal obligation with regard to assisting in the decumulation of a plan account, whether by providing products or advice. In fact, providing advice and/or assistance can be grounds for holding that an otherwise non-fiduciary has crossed the line and is legally recognized as a fiduciary.

Annuity advocates claim that my positions are cruel and insensitive. My response – my advice is legally prudent and reflects prudent fiduciary risk management strategies. Furthermore, the alleged “humanitarian” argument coming from the annuity industry is extremely ironic coming from an industry marketing a product that is intentionally designed to produce a windfall for the annuity issuer at the expense of both the plan participant and their beneficiaries.

Ironic coming from an industry that consistently opposes any type of a meaningful fiduciary standard that would simply require that the industry always act in the best interests of the public. Ironic coming from an industry that, as Judge Barbara Lynn pointed out, markets products that reserve the right for the annuity issuer to unilaterally change key terms of the annuity, after the fact, so as to shift the risk of the investment from the annuity issuer to the annuity owner.

Plan sponsors, plan participants and their beneficiaries would be better served by heeding the advice of Jack Welch, former CEO of GE – “Don’t make the process harder than it is.” Yet, far too many plan sponsors do just that, resulting in unnecessary fiduciary liability exposure.

Another marketing strategy currently being used by the annuity industry is to suggest that plan sponsors have a duty to offer annuities within a plan because plan participants supposedly “want” to buy them. As soon as I hear the “participants want them” argument, I immediately think “tell me that you know nothing about fiduciary law without telling me that you know nothing about fiduciary law.” I even had a well-known annuity advocate tell me that someone cannot be a fiduciary without offering annuities. That simply is not true.

I sometimes receive requests to sit in on plan investment committee meeting to offer fiduciary risk management advice. Whenever an annuity wholesaler is going to make a presentation, I “woodshed” plan’s investment committee so they know how to evaluate the wholesaler and their sales pitch. In following Steve Job’s advice to always include a “Holy S**t” moment, I always tell the committee to ask the wholesaler if they are willing to submit a written breakeven analysis of any recommended annuities.

The wholesaler will immediately object, “that’s not required by law,” or offer to provide a verbal breakeven analysis. Always insist on a written breakeven analysis, as it should be admissible in court, if necessary. Amazing how facts often change under stress.

To summarize, plan sponsors should always remember Jack Welch’s advice. I have a saying for my clients – KISS – Keep It Simple and Smart. Simple refers to the fact that the more investment option a plan offers, the greater the likelihood of a breach. ERISA only mentions a required number of investment options once, as in a minimum of three broadly diversified investment options are required for plans looking for the protection offered under 404(c). For a long time, the federal government’s highly successful Federal Thrift Plan (FTP) only offered five, diversified index-type investment options. As a result, they offered federal employees an easily understandable and effective plan, while protecting against “paralysis by analysis.” Today, the FTP boasts a number of millionaires.

As for the “smart” part of the equation, I recommend evaluating investment options with simple cost-benefit analysis {CBA}. Obviously, I prefer the Active Management Value Ratio (AMVR) metric I created for my fiduciary risk management consulting firm, InvestSense, LLC. The AMVR is essentially a cost-benefit analysis using incremental risk-adjusted returns and incremental correlation-adjusted costs as the input data. Based on the investment concepts investment icons such as Nobel laureate Dr. William F. Sharpe and Charles D. Ellis, the metric is fundamentally sound and simple to use. Further information on the AMVR and sample analyses can be found at fiduciaryinvestsense.com.

In concluding, lets return to the “and their beneficiaries” language of ERISA Section 404a. I submitted the following query on ChatGPT:

Using cost-benefit analysis, prepare a fiduciary prudence analysis of a $50,000 immediate annuity, paying 5% annually, on a 65 year old woman, assuming normal life expectancy, factoring in commensurate return, breakeven analysis, estate asset erosion, present value and mortality risk concerns, as well the best interest of the plan participants and their beneficiaries.

I am not going to post the chat GPT generated report here due to its length. However, with one notable exception, the report’s findings, conclusions, and recommendations agreed with mine. The exception involved the report’s use of a “nomina”l breakeven point, which is nothing more than diving the cost of the annuity by its interest rate. Here, the reported reported a nominal breakeven point of 10 years, Most courts would not such a deliberatively misleading analysis into evidence.