James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

When the DOL announced the relases of its new alternative investments rule, we quickly advised out fiduciary risk minimization clients to simply ignore it, as it failed our basic two-step fiduciary analysis process:

1. Does ERISA require the product/strategy to be offered within a plan?

2. If not, could/would the product/strategy potentially expose the plan to unnecessary fiduciary liability? Here, even the DOL warned plan sponsors of the potential liability.

The second reason we advised our fiducairy riask management to simply ignore the proposed rule altogether was that upon review of the rule, I concluded that thre is little chance of the proposed rule passing judicial scrutiny under the Administrative Procedure Act (APA), as the rule is “arbitrary and capricious” based on current APA judicial precedent.

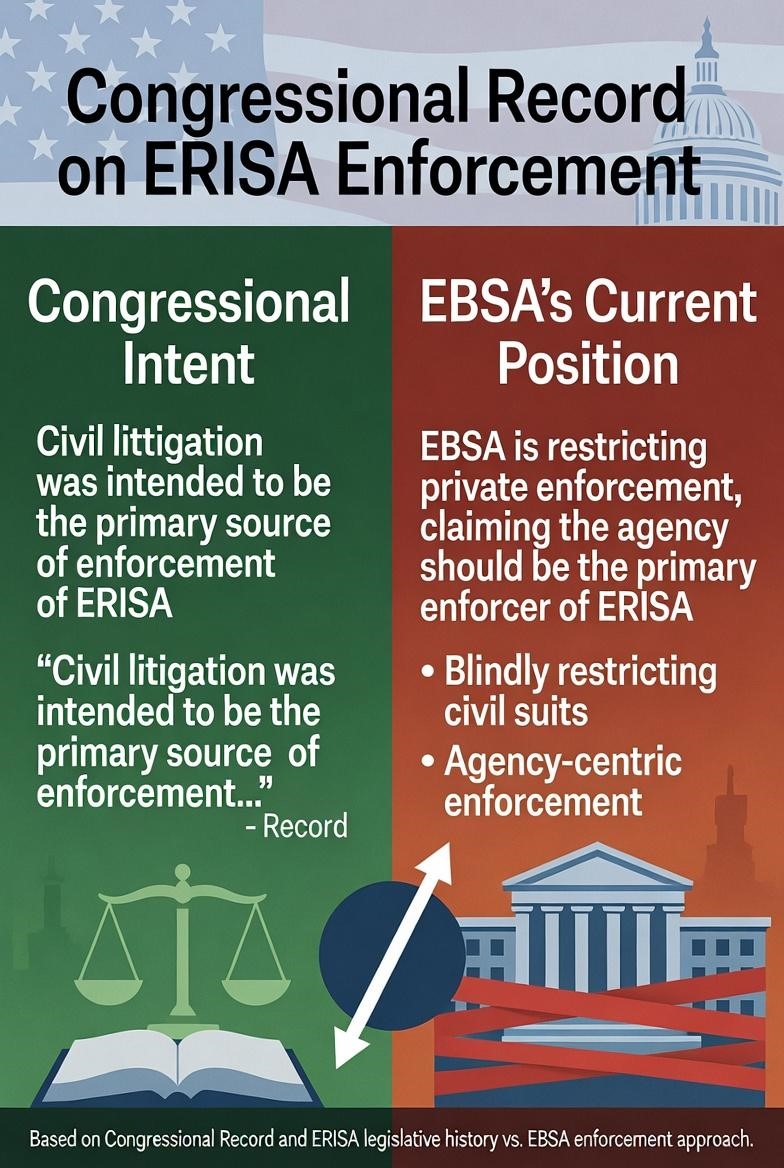

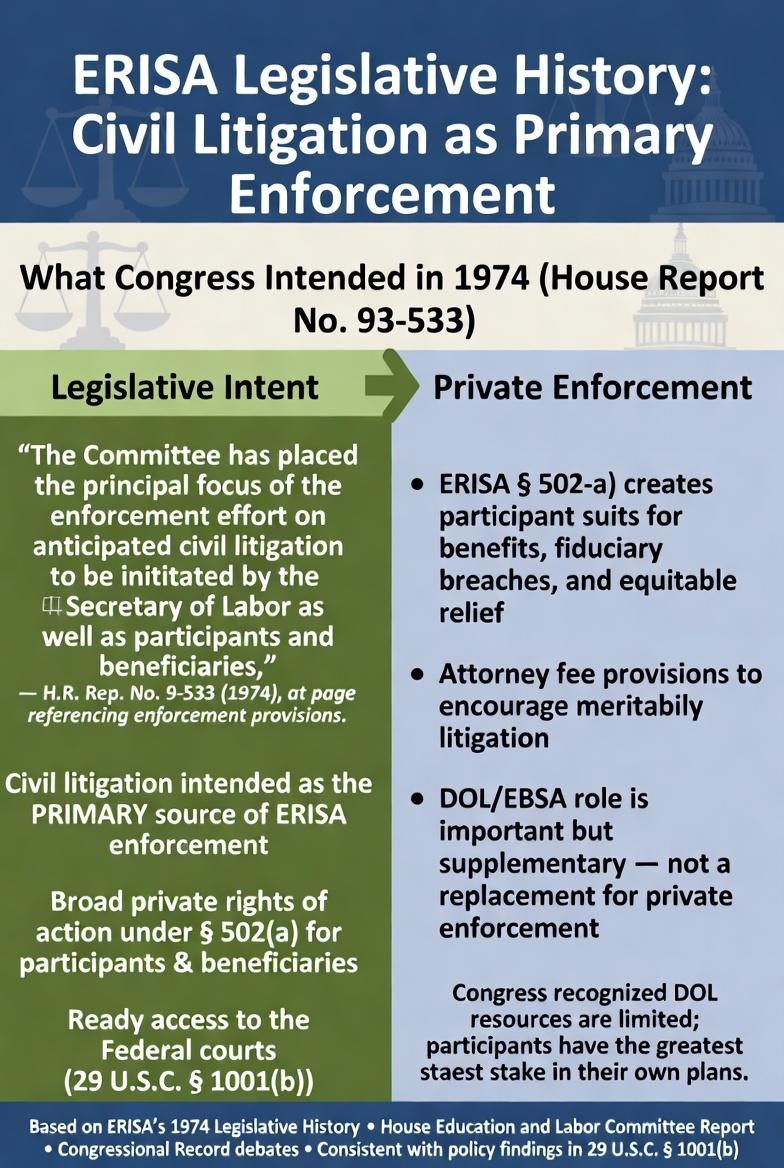

Upon close examination, despite being titled i nterms of “alternative investments,” I consider the release and proposed riule to be yet another continued attempt to illegally deny plan participants acccess to the courts, which is clearly inconsistent with Congessional intent, as evidenced by the legislative history of ERISA. Furhter evidence of this intent is supported by the fact that release used the term “litigation” over 105 times.

The Proposed Rule and EBSA’s Litigation Positions Violate the Administrative Procedure Act

The Department’s proposed rule cannot withstand scrutiny under the Administrative Procedure Act1 because it is internally inconsistent, departs from prior agency positions without adequate explanation, and rests on rationales that conflict with both statutory text and binding precedent.

I. The Rule Is Arbitrary and Capricious Because It Is Inconsistent with ERISA’s Trust Law Foundation

The Supreme Court has repeatedly held that Employee Retirement Income Security Act of 1974 fiduciary duties are derived from the common law of trusts. In Firestone Tire & Rubber Co. v. Bruch2, the Court made clear that “ERISA abounds with the language and terminology of trust law” and must be interpreted accordingly. Likewise, Varity Corp. v. Howe3 reaffirmed that courts should look to “the law of trusts” to define fiduciary obligations under ERISA.

More recently, in Fifth Third Bancorp v. Dudenhoeffer4, the Court again emphasized that ERISA’s fiduciary standards are rooted in trust law principles, rejecting attempts to create atextual modifications to those duties.

Those principles include the burden-shifting framework reflected in the Restatement (Second) of Trusts § 100, under which a fiduciary who has breached its duty bears the burden of proving that the breach did not cause the loss.

By adopting a rule that effectively avoids or undermines these trust law consequences, the Department is not interpreting ERISA—it is contradicting it. Under Motor Vehicle Manufacturers Association v. State Farm Mutual Automobile Insurance Co.5, agency action is arbitrary and capricious where it “runs counter to the evidence before the agency” or fails to align with governing law. That is precisely the defect here.

II. The Department Fails to Provide a Reasoned Explanation for Departing from Prior Positions

An agency must provide a reasoned explanation when it changes course. In FCC v. Fox Television Stations, Inc.6, the Court held that while agencies may revise their policies, they must “display awareness that it is changing position” and show that the new policy is permissible and justified.

Here, the Employee Benefits Security Administration has, in prior amicus briefs, emphasized ERISA’s grounding in trust law and the importance of fiduciary accountability consistent with those principles. The proposed rule adopts a materially different approach—one that minimizes or avoids the implications of trust law, including burden shifting.

Yet the Department offers no acknowledgment of this shift, let alone a reasoned explanation. Under Fox, that failure alone renders the rule unlawful.

III. The Department’s Reliance on “Frivolous Litigation” Is Pretextual and Contrary to ERISA’s Legislative Design

The Department’s asserted concern about “frivolous litigation” is both legally insufficient and internally contradictory.

As an initial matter, ERISA’s enforcement scheme reflects Congress’s deliberate choice to rely on private litigation. In Massachusetts Mutual Life Insurance Co. v. Russell7, the Court recognized that ERISA’s civil enforcement provisions were “carefully integrated” to provide participants with meaningful remedies. Similarly, LaRue v. DeWolff, Boberg & Associates8, Inc. reaffirmed the central role of participant lawsuits in enforcing fiduciary duties.

An agency may not invoke concerns about litigation to undermine a statutory scheme that expressly depends on it.

Moreover, under State Farm, an agency acts arbitrarily when it offers an explanation that is implausible or inconsistent with the record. Here, the Department’s litigation rationale conflicts with its own prior positions. In amicus briefs, the EBSA has repeatedly defended robust private enforcement as essential to ERISA’s function. Its current reliance on litigation as a justification for weakening fiduciary accountability is therefore pretextual.

IV. The Rule Reflects Impermissible Outcome-Oriented Reasoning

The APA prohibits agencies from adopting rules driven by desired outcomes rather than reasoned analysis. In Department of Commerce v. New York9, the Court rejected agency action where the stated rationale was pretextual and did not reflect the agency’s true reasoning.

Here, the structure of the rule reveals an effort to avoid the consequences of applying trust law principles—particularly the burden placed on fiduciaries to disprove causation following a breach. The Department is aware that this burden would expose widespread fiduciary vulnerability, especially in connection with complex financial products such as annuities.

But avoiding statutory consequences is not a permissible basis for regulation. As the Court emphasized in State Farm, agencies must engage in reasoned decision-making grounded in the statute—not in policy preferences about economic impact.

V. The Rule’s Internal Contradictions Undermine Its Reasonableness

Finally, the rule is independently invalid because it is internally inconsistent. It purports to clarify fiduciary duties while simultaneously adopting standards that dilute them. It invokes ERISA’s protective purpose while advancing interpretations that weaken enforcement.

Such contradictions violate the APA’s requirement of reasoned decision-making. As State Farm makes clear, an agency must articulate a “rational connection between the facts found and the choice made.” The Department has failed to do so.

VI. The Proposed Rule Is Not Entitled to Deference Under Chevron or Loper Bright

The Department cannot rely on judicial deference to salvage the proposed rule. Whether analyzed under the traditional framework of Chevron U.S.A. Inc. v. Natural Resources Defense Council, Inc.10 or the Supreme Court’s more recent decision in Loper Bright Enterprises v. Raimondo11, the rule fails.

A. Even Under Chevron, the Rule Is Unlawful

Under Chevron, an agency interpretation receives deference only if (1) the statute is ambiguous and (2) the agency’s interpretation is reasonable.

Neither condition is satisfied here.

At Step One, ERISA is not ambiguous as to the source of its fiduciary standards. The Supreme Court has repeatedly held that Employee Retirement Income Security Act of 1974 incorporates the common law of trusts. See, e.g., Firestone Tire & Rubber Co. v. Bruch; Varity Corp. v. Howe; Fifth Third Bancorp v. Dudenhoeffer. That interpretive directive leaves no gap for the agency to fill with a conflicting framework.

At Step Two, even if ambiguity existed, the Department’s interpretation would still fail because it is not reasonable. An interpretation that effectively discards core trust law principles—such as the burden-shifting framework reflected in the Restatement (Second) of Trusts § 100—cannot be reconciled with the statute’s structure or purpose.

Chevron deference does not permit an agency to adopt an interpretation that contradicts the very body of law Congress incorporated.

B. Under Loper Bright, the Court Owes No Deference to the Agency’s Interpretation

Any reliance on Chevron is, in any event, misplaced. In Loper Bright Enterprises v. Raimondo, the Supreme Court made clear that courts must exercise independent judgment in interpreting statutes and may not defer to agency interpretations merely because a statute is ambiguous.

Under Loper Bright, the question is not whether the Department’s interpretation is permissible, but whether it is correct.

It is not.

Applying independent judicial judgment, the Court must interpret ERISA in accordance with its text, structure, and historical context—all of which point to trust law as the governing framework. As discussed, that framework includes established principles governing fiduciary liability and burden allocation.

The Department’s rule, which attempts to avoid those principles, cannot survive de novo review.

C. The Major Questions Doctrine Further Confirms That Deference Is Inappropriate

Even if ambiguity could be manufactured, this case implicates questions of vast economic and legal significance. The rule effectively reshapes fiduciary liability exposure across the retirement system, with substantial downstream effects on plan sponsors, financial institutions, and fiduciary liability insurers.

Under West Virginia v. Environmental Protection Agency12, courts require clear congressional authorization before permitting agencies to exercise such sweeping authority.

No such authorization exists here. ERISA does not grant the Department power to redefine fiduciary liability in a manner that departs from its trust law foundation. To the contrary, the statute presumes adherence to those principles.

Conclusion

Because the proposed rule conflicts with Supreme Court precedent interpreting ERISA, departs from prior agency positions without explanation, relies on pretextual reasoning, and fails the standards articulated in Motor Vehicle Manufacturers Association v. State Farm Mutual Automobile Insurance Co. and FCC v. Fox Television Stations, Inc., it violates the Administrative Procedure Act.

Furthermore, because the proposed rule fails under both Chevron U.S.A. Inc. v. Natural Resources Defense Council, Inc. and Loper Bright Enterprises v. Raimondo, and raises serious concerns under West Virginia v. Environmental Protection Agency, it is not entitled to judicial deference.

The Court should interpret ERISA independently and should rule that the rule is ulawful and set the rule aside.

Notes

1. Admininstrative Procedure Act, 5 U.S.C.A. Sections 551 -559.

2. Firestone Tire & Rubber Co. v. Bruch, 489 U.S. 101 (1989).

3. Varity v. Howe, 516 U.S. 489 (1996).

4. Fifth Third Bancorp v. Dudednhoeffer, 573 U.S. 409 (2014).

5. Motor Vehicle Mfg. Assn. v. State Farm Ins. Co., 463 U.S. 29 (1983).

6. FCC v. Fox Television Stations, 556 U.S. ____ (2009).

7. Mass Mutual Life Ins. Co. v. Russell, 473 U.S. 134 (1985).

8. LaRue v. DeWolff, Boberg, & Associates, 553 U.S. 248 (2008).

9. Dept. of Commerce v. New York, 558 U.S. ____ (2019).

10. Checron USAInc. v. NAtural Resources Defense Council, Inc., 467 U.S.837 (1984).

11. Loper Bright Enterprises v. Raimondo, 200 U.S. 321 (2024).

12. West Virginia v. EPA, 597 U.S. 697 (2022).

© Copyright 2026 InvestSense, LLC. All rights reserved

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

About jwatkins

I am a securities and ERISA attorney. I hold CFP Board Emeritus™ status and I am an Accredited Wealth Management Advisor™. I provide fiduciary risk management consulting to 401k/430b plans, trustees, RIAs and other investment fiduciaries. I am a 1977 graduate of Georgia State University and a 1981 graduate of the University of Notre Dame Law School. I am the author of “CommonSense InvestSense: The Power of the Informed Investor” and “The 401(k)/403(b) Investment Manual: What Plan Sponsors and Plan Participants REALLY Need To Know” I write two blogs, “CommonSense InvestSense, investsense.com, and “The Prudent Investment Fiduciary Rules, fiduciaryinvestsense.com. As a former compliance director, I have extensive experience in evaluating the legal prudence of various types of investments, including mutual funds and annuities. My goal is to combine my legal and compliance experience in order to help educate investors and investment fiduciaries on sound, proven investment strategies that will help them protect their financial security and/or avoid unnecessary fiduciary liability exposure.

You must be logged in to post a comment.