James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

InvestSense, LLC

I. Introduction

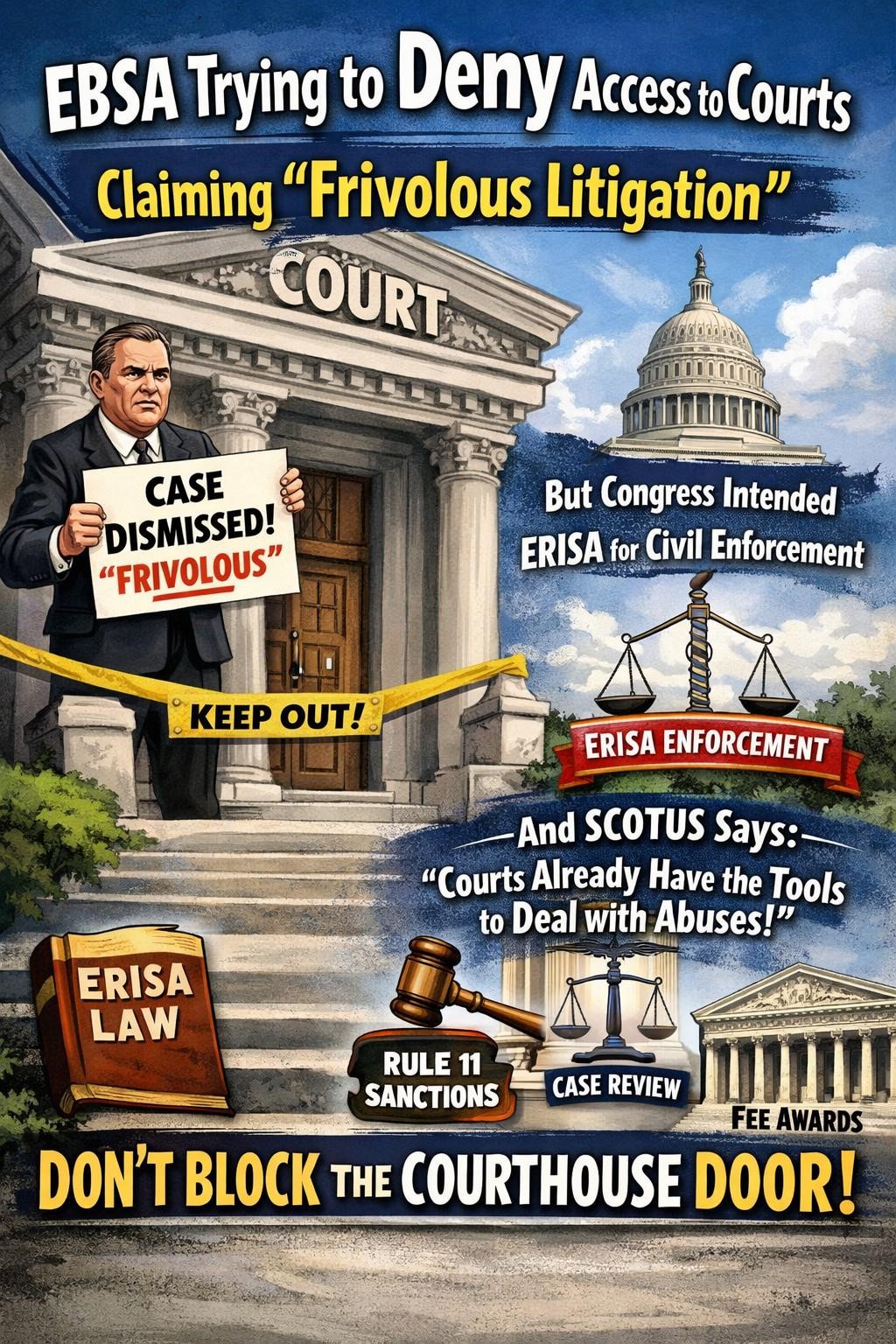

Recent statements by the EBSA leadership and Assistant DOL Secretary, Daniel Aronowitz, frame ERISA litigation as abusive,” “frivolous,” and in need of increased structural restrictions. Aronowitz has called for a “PSLRA” for ERISA, similar to the SEC Act covering the general securities market. Aronowitz has advocated for heightened pleading standards, restricted standing requirements, and judicial doctrines designed to shield ERISA fiduciaries from litigation and liability.

This position, however, is inconsistent with ERISA’s statutory design, controlling Supreme court precedent, and the legislative history of ERISA itself. Properly understood, ERISA depends upon participant-driven litigation as a primary enforcement mechanism. Therefore, efforts to restrict access to the courts undermine -not further- ERISA’s core purposes.

II. THE EBSA’s PRETEXTUAL JUSTIFICATION CONTRADICTS ERISA’S TEXT, PURPOSE, AND LEGISLATIVE DESIGN

A. ERISA Was Deliberately Designed As a Participant-Enforced Statute Providing Broad Access to Federal Courts

Congress’ intent is explicit in both statutory text and legislative history: ERISA is a remedial, litigation-driven enforcement regime.

1.. Statutory Mandate: “Ready Access to the Federal Courts”

ERISA § 2(b), 29 U.S.C. § 1001(b), provides:

“to protect … participants and beneficiaries … by providing for appropriate remedies, sanctions, and ready access to the Federal courts.”

This is not aspirational language; it is a structural directive that civil litigation is the primary enforcement mechanism.

2.. Legislative History Confirms Congress Intended Expansive Participant Litigation

The Senate and House Reports—consistently relied upon by the Supreme Court—state:

- Senate Report No. 93-127: ERISA is “designed specifically to provide… participants and beneficiaries with broad remedies for redressing or preventing violations.”

- Further: to provide “the full range of legal and equitable remedies … and to remove jurisdictional and procedural obstacles … which hampered effective enforcement.”

- House Report No. 93-533: enforcement provisions are to be “liberally construed to provide … broad remedies.”

3. Doctrinal Implications

Congress made three deliberate choices:

- Participants—not regulators—would enforce fiduciary obligations

- Courts—not agencies—would police fiduciary conduct

- Barriers to litigation were to be removed, not erected

IiI. Supreme Court Doctrine Reinforces That Courts Already Possess Adequate Tools to Address Abusive Litigation

Recent Supreme Court oral arguments directly undermine claims that ERISA litigation requires additional gatekeeping.

A. Justice Jackson: Courts Already Police Frivolous Litigation

During oral argument (e.g., fiduciary breach / pleading sufficiency context), Justice Ketanji Brown Jackson emphasized:

“Don’t we already have tools to deal with frivolous litigation?”

She specifically referenced:

- Motions to dismiss under Rule 12(b)(6)

- Rule 11 sanctions

- Judicial control over discovery

And further:

“Why isn’t that sufficient?”

3. Litigation Significance

This line of questioning reflects a critical doctrinal principle:

The federal judiciary—not administrative agencies—controls the calibration of litigation burdens and abuse prevention.

4. Structural Separation: Judicial Case Management vs. Substantive Barriers

The Court’s discussion highlights a distinction:

| Proper Mechanism | Improper Mechanism |

| Rule 12(b)(6) dismissal | Heightened pleading beyond statute |

| Rule 11 sanctions | Categorical limits on claims |

| Managed discovery | Preclusion of participant suits |

ERISA’s design aligns exclusively with the left column.

IV. EBSA’s Amicus Positions Advocating Restrictions on ERISA Litigation Are Doctrinally Inconsistent with Congressional Design

The litigation positions advanced by the Employee Benefits Security Administration—particularly under leadership such as Daniel Aronowitz—frequently assert that ERISA litigation is plagued by “frivolous” claims requiring judicial constraint.

A. EBSA’s “Frivolous Litigation” Thesis

EBSA has argued in multiple amicus contexts that:

- ERISA litigation imposes undue burdens on plan sponsors

- Courts should impose stricter pleading or evidentiary thresholds

- Discovery should be curtailed to prevent abuse

B. Direct Conflict with Congressional Intent

These positions are irreconcilable with ERISA’s legislative design:

| Congressional Intent | EBSA Litigation Position |

| “Ready access to courts” | Restrict access via heightened thresholds |

| “Broad remedies” | Narrow actionable claims |

| Remove procedural obstacles | Introduce new litigation barriers |

| Participant-driven enforcement | Sponsor-protective filtering |

C. Conflict with Supreme Court Reasoning

EBSA’s approach is also inconsistent with the Supreme Court’s expressed view—articulated in questioning by Justice Ketanji Brown Jackson—that:

Existing procedural tools are sufficient to address abusive litigation.

D. Doctrinal Tension

EBSA’s position implicitly asserts:

Courts are incapable of managing ERISA litigation without additional constraints.

The Supreme Court’s response:

Courts already possess—and routinely employ—adequate mechanisms.

V. ERISA’s Trust-Law Foundations Further Undermine EBSA’s Restrictive Approach

ERISA is grounded in the common law of trusts. Under trust law:

- Beneficiaries have broad rights to sue fiduciaries

- Courts serve as the primary forum for enforcement

- Remedies are expansive and equitable in nature

Key Principle

Limiting access to courts is antithetical to fiduciary accountability.

EBSA’s litigation stance effectively inverts this structure by:

- Shielding fiduciaries from scrutiny

- Elevating sponsor interests over beneficiary rights

- Reintroducing the very enforcement barriers ERISA was enacted to eliminate

VI. Conclusion: EBSA’s Litigation Positions Represent a Structural Departure from ERISA’s Core Enforcement Model

The combined weight of:

- Statutory text (“ready access to the Federal courts”)

- Legislative history (“broad remedies,” “remove obstacles”)

- Supreme Court reasoning (courts already control frivolous litigation)

establishes a clear rule:

ERISA enforcement depends on robust participant access to judicial remedies, not administrative or judicial contraction of claims at the threshold.

Accordingly, any argument—whether advanced by EBSA or otherwise—that seeks to curtail participant litigation based on generalized concerns about “frivolous” suits is:

- Contrary to congressional intent

- In tension with Supreme Court doctrine

- Inconsistent with ERISA’s trust-law foundations

VII. ERISA’s Text and Legislative Purpose Affirmatively Enshrine Civil Litigation as a Core Enforcement Mechanism

EBSA’s attempt to characterize participant litigation as “frivolous” or excessive is irreconcilable with the statute Congress enacted.

Congress expressly designed ERISA to expand—not restrict—access to federal courts as a primary enforcement tool. The statute itself provides for “appropriate remedies and access to the federal courts” as a central means of protecting participants.

This was not incidental. It reflects Congress’s deliberate rejection of an exclusively administrative enforcement regime in favor of participant-driven litigation as a necessary enforcement backstop.

A. Legislative Design: Private Enforcement Was Intended to Supplement Limited Government Oversight

ERISA’s civil enforcement scheme (§ 502(a)) was modeled to ensure that plan participants act as “private attorneys general”, filling enforcement gaps left by limited agency resources. Courts have repeatedly recognized that ERISA’s structure depends on private suits to ensure fiduciary accountability.

This design mirrors other federal statutes—such as the False Claims Act—where Congress explicitly empowered private litigants to vindicate statutory violations when government enforcement is insufficient. See, e.g., the qui tam mechanism allowing citizens to sue “on behalf of the government” to enforce statutory compliance.

The analogy is instructive: Congress uses private litigation precisely where violations are difficult to detect and regulators face structural limits—conditions that are equally present in ERISA fiduciary misconduct.

B. Legislative History Confirms Congress Intended Broad, Participant-Friendly Court Access

The legislative history of ERISA repeatedly emphasizes that effective enforcement required ready access to federal courts:

- Congress intended “full and fair access to the courts” for participants and beneficiaries (Conference Report).

- Civil actions were designed as the “primary enforcement mechanism” to ensure fiduciary compliance.

- The statutory scheme reflects concern that without robust litigation rights, fiduciary standards would be “illusory.”

Thus, EBSA’s position willfully ignores congressional intent: what the agency labels “frivolous litigation” is, in fact, the mechanism Congress deliberately empowered to police fiduciary abuse.

VIII. EBSA’s Position Impermissibly Rewrites ERISA by Imposing Extra-Statutory Barriers to Suit

Recent policy arguments—such as heightened pleading standards, discovery stays, or procedural barriers justified by “meritless litigation”—are not neutral refinements. They are substantive restrictions on statutory rights.

As reflected in ongoing legislative proposals aimed at “curb[ing] meritless class actions” by raising pleading burdens and staying discovery, such efforts would materially limit participants’ ability to enforce ERISA rights.

But those restrictions are for Congress—not EBSA—to enact. Agencies cannot:

- Rewrite § 502(a)’s broad grant of standing;

- Narrow judicial remedies Congress deliberately made expansive; or

- Rebalance enforcement away from participants toward regulated entities.

To do so violates basic separation-of-powers principles and the settled rule that agencies may not override statutory enforcement schemes through policy preferences.

IX. The “Frivolous Litigation” Narrative Is Factually and Structurally Misleading

A. ERISA Litigation Is Already Heavily Filtered by Courts

Federal courts already apply:

- Rule 12(b)(6) dismissal standards

- Heightened pleading requirements under modern jurisprudence

- Summary judgment standards

- Sanctions for frivolous claims

Thus, the premise that ERISA litigation proceeds unchecked is demonstrabl false and knowingly disingenous. The judiciary—not EBSA—is the constitutionally designated gatekeeper for merit.

B. Enforcement Data Shows Violations Are Widespread, Not Rare

Even EBSA’s own enforcement reporting demonstrates systemic noncompliance, with investigations resulting in widespread corrective actions affecting millions of participants.

This undercuts any claim that litigation is predominantly frivolous; rather, it reflects pervasive fiduciary violations requiring enforcement.

X. EBSA’s Position Reflects Institutional Bias Favoring Plan Sponsors and Insurers

EBSA’s litigation-restrictive stance is not neutral. It aligns consistently with plan sponsor and insurance industry interests:

- Limiting discovery reduces exposure of fiduciary misconduct

- Raising pleading burdens shields conflicted transactions

- Curtailing class actions reduces aggregate liability

These positions functionally insulate fiduciaries and insurers from accountability, contrary to ERISA’s protective purpose.

XI. Daniel Aronowitz’s Advocacy Further Demonstrates Conflict of Interest

The credibility of the “frivolous litigation” narrative is further undermined by the role of Daniel Aronowitz.

A. Prior Industry Role Creates Structural Conflict

Before his governmental role, Aronowitz was a leading figure in the fiduciary liability insurance industry—a sector that:

- Directly profits from limiting litigation exposure

- Prices risk based on expected claims frequency and severity

- Benefits from procedural barriers that reduce claim viability

Policies restricting ERISA litigation therefore directly align with his prior industry interests.

B. Policy Positions Mirror Insurance Industry Objectives

Aronowitz has publicly advocated for:

- Reducing “excessive” ERISA litigation

- Increasing procedural barriers to participant claims

- Rebalancing enforcement away from private suits

These positions track precisely with insurance industry priorities to reduce claim payouts and litigation risk, reinforcing the appearance—and reality—of a conflict of interest.

XII. Curtailing Participant Litigation Undermines ERISA’s Core Protective Function

ERISA was enacted in response to widespread pension abuses, with Congress concluding that:

- Disclosure alone was insufficient

- Administrative oversight was limited

- Judicial enforcement was essential

Restricting participant access to courts would:

- Weaken fiduciary accountability

- Reduce deterrence of misconduct

- Shift enforcement toward an already resource-constrained agency

In short, it would recreate the very conditions ERISA was designed to eliminate.

XIII. Conclusion

“A tyrant always has a pretext for his tyranny.” – Aesop

Aronowitz and the current EBSA certainly have no shortage of pretextual claims for their biased policies. EBSA’s attempt to justify restricting ERISA litigation as a response to “frivolous claims” is:

- Contrary to statutory text, which guarantees access to federal courts;

- Inconsistent with legislative history, which designates civil litigation as a primary enforcement mechanism;

- Unsupported by empirical reality, given documented widespread violations; and

- Tainted by conflict of interest, particularly in light of Aronowitz’s prior role in the fiduciary insurance industry.

The questionable trends in the EBSA’s recent policies, as well as the willful blindness involved, and the easily foreseeable harm that could result, justifies an urgent call for Congress to immediately exercise Congressional oversight over the DOL, the EBSA, and Aronowitz to ensure compliance with the agency’s stated purposes, acting in the best interests of plan participants and their beneficiaries by ensuring the rights and protections guaranteed under ERISA. The urgency is even greater given the fact that The DOL has apparently suspended the ERISA Advisory Council, an oversight which portentially could have addressed the very issues issues addressed herein and prevented the types of pretexts and betrayal cueently being seen at the DOL and EBSA/

© Copyright 2026 InvestSense, LLC. All rights reserved

This article is for informational purposes only and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

You must be logged in to post a comment.